Stay Ahead of Fraud with Proactive Detection Technology

Detelix delivers real-time fraud prevention across your most sensitive business processes. Talk to our experts and discover where your gaps are.

- What Has Changed in the Fraud Detection Technology Landscape for 2025?

- How Artificial Intelligence Is Redefining Advanced Fraud Detection

- The GenAI and Deepfake Threat: Why 2025 Demands New Defenses

- A Scenario: When a Deepfake Almost Authorized a Wire Transfer

- Real-Time Decisioning: Why Milliseconds Matter

- Behavioral Biometrics: Detecting Fraud When Credentials Are Correct

- Device Intelligence: The First Layer of Defense You Cannot Skip

- Comparing Key Fraud Detection Technologies at a Glance

- Graph Analytics: Uncovering Hidden Fraud Networks

- Common Mistakes Organizations Make When Deploying Fraud Detection

- How to Measure Success in a Fraud Prevention Program

- Rules vs. Machine Learning: Which Approach Wins?

- Step-Up Authentication: Moving Beyond Weak OTP

- Continuous Authentication: Why Login Is No Longer Enough

- How Detelix Addresses Key Business Needs in Fraud Prevention

- Explainable AI: The Regulatory Imperative Behind Model Transparency

- Privacy, Bias, and Ethical Signal Collection

- Building Layered Defenses Without Slowing Down the Business

- Frequently Asked Questions

Fraud detection in many organizations still depends on periodic reviews, static rule sets, and manual reconciliation. These methods served their purpose when threats were predictable and transaction volumes were manageable. But in 2025, attackers wield generative AI, deepfake media, and scalable social engineering campaigns, while instant payment rails leave virtually no window for post-event intervention. The gap between the speed of fraud and the speed of detection is widening fast. For finance and operations leaders, understanding the key fraud detection technology trends shaping this year is the foundation of real organizational control.

Key Takeaways

- Real-time, AI-driven decisioning has replaced batch-based reviews as the standard for effective fraud prevention in 2025.

- Generative AI and deepfakes create new attack vectors that bypass traditional human verification and require system-level controls.

- Behavioral biometrics and device intelligence add detection layers that work even when attackers hold valid credentials.

- Graph analytics reveals organized fraud networks that transaction-level analysis alone cannot detect.

- A hybrid rules-plus-ML architecture delivers both regulatory compliance and adaptive threat detection.

- Measuring false-positive rates and time-to-decision is as critical as tracking fraud detection rates.

What Has Changed in the Fraud Detection Technology Landscape for 2025?

The most significant shift is the move from reactive, report-based investigation to proactive, multi-layered defense that operates in real time. Traditional controls such as approval workflows, segregation of duties, and periodic audits remain important, but they are no longer sufficient on their own. Modern fraud prevention technology now combines behavioral signals, device context, network analysis, and machine-learning models into a single decision pipeline that evaluates risk before a transaction is completed.

Several forces are driving this acceleration. Instant payment schemes mean money moves in seconds, leaving no time for next-day batch reviews. Generative AI gives attackers the ability to craft convincing phishing messages and synthetic identities at scale. And as organizations digitize more processes inside their ERP environments, the attack surface expands beyond traditional payment channels into procurement, payroll, supplier management, and customer refunds. A team of experts that understands both the technology and the business processes it protects has become essential for navigating this complexity.

Tip

Map every payment channel your organization uses, including internal ERP processes like payroll and procurement. Fraud controls that cover only external-facing transactions leave significant blind spots in supplier payments, bank account changes, and employee reimbursements.

How Artificial Intelligence Is Redefining Advanced Fraud Detection

AI and machine learning have moved well beyond the innovation buzzword phase. They are now the primary engine of advanced fraud detection in production environments. At a basic level, supervised models learn from historically labeled fraud cases to score new transactions. Unsupervised models detect anomalies that do not match any known pattern, which is critical for catching novel attack vectors that rules would never anticipate.

What makes 2025 different is the maturity of the implementation. Organizations are shifting from one-off model deployments to continuous learning loops: models are retrained as fraud patterns evolve, performance drift is monitored automatically, and feedback from investigators flows back into the training pipeline. This means the system improves with every case it processes, reducing reliance on static rule maintenance.

Did You Know

Organizations that implement continuous model retraining loops detect up to 40% more emerging fraud patterns compared to those that deploy ML models on a static, train-once basis. The difference widens as attacker tactics shift quarter over quarter.

Supervised vs. Unsupervised Learning: When Does Each Excel?

Supervised learning excels when an organization has rich historical data with clear fraud labels, covering scenarios like payment fraud, account takeover, and chargeback abuse. Unsupervised learning shines in scenarios where fraud is rare or entirely new, such as synthetic identity schemes or insider collusion. The most effective deployments combine both: a supervised model provides a strong baseline score, while an anomaly layer flags unexpected deviations that fall outside historical patterns. Platforms like Detelix integrate ML-based fraud detection into the monitoring of sensitive business processes, ensuring that pricing anomalies and revenue leakage are caught alongside traditional transactional fraud.

The GenAI and Deepfake Threat: Why 2025 Demands New Defenses

Generative AI has lowered the barrier to producing hyper-realistic phishing emails, voice clones, and even video deepfakes. An attacker no longer needs advanced technical skills to impersonate a CFO on a video call or generate a convincing supplier invoice. According to research published by the Institute for National Security Studies (INSS), deepfake technology poses growing risks not only to national security but also to financial institutions and corporate environments.

For finance and operations leaders, the practical implications are immediate. Onboarding processes that rely on document uploads and selfie verification must now include liveness detection capable of spotting synthetic media. Voice-based authentication is increasingly vulnerable. And any approval process that depends on verbal or visual confirmation, such as authorizing a large wire transfer, needs an additional cryptographic or system-level verification layer that cannot be spoofed by generated media.

Tip

Never rely solely on voice or video confirmation for high-value payment approvals. Require a secondary system-level verification step inside your ERP, such as a digital signature or multi-party workflow approval, that cannot be replicated by synthetic media.

A Scenario: When a Deepfake Almost Authorized a Wire Transfer

Consider a mid-size manufacturing company whose CFO receives a video call from what appears to be the CEO, requesting an urgent payment to a new supplier. The voice, the face, and the conversational style are convincing. Without a system-level control that cross-checks the payment against known supplier records, bank account change history, and approval policy inside the ERP, the finance team might process the transfer before discovering the call was generated by AI. This scenario is no longer theoretical; it reflects reported incidents across multiple industries in 2024 and 2025.

The takeaway is clear: human judgment alone cannot reliably distinguish authentic from synthetic communication. Organizations need automated, real-time controls that validate the business logic of every sensitive action, regardless of how convincing the request appears on the surface.

Did You Know

A 2024 incident in Hong Kong resulted in a $25 million loss when a finance employee was deceived by a deepfake video conference call that convincingly impersonated multiple senior executives simultaneously. The entire interaction was AI-generated.

Real-Time Decisioning: Why Milliseconds Matter

In an era of instant payments and digital operations, the window between initiating a transaction and completing it has collapsed. Fraud technology innovation in 2025 is therefore obsessed with latency: how quickly can a system evaluate risk and return a decision without degrading the user experience?

Modern decision engines operate in the sub-second range, analyzing dozens of signals simultaneously: device reputation, behavioral patterns, network context, transaction velocity, and historical baselines. The goal is not to block every suspicious action outright but to route risk intelligently. Low-risk actions proceed seamlessly. Medium-risk actions trigger step-up authentication. High-risk actions are held for review or blocked entirely.

Balancing Security and Experience

The most common mistake organizations make is treating fraud prevention as a binary gate: approve or deny. This approach generates excessive false positives, frustrates legitimate users, and creates operational bottlenecks in manual review queues. A well-designed decision engine uses dynamic thresholds that adapt to context. A repeat customer on a known device performing a routine action should face minimal friction, while a new device executing an unusual payment pattern warrants additional verification.

Tip

Implement at least three risk tiers in your decision engine: auto-approve for low risk, step-up authentication for medium risk, and hold-for-review or block for high risk. This approach reduces false positives by up to 60% compared to binary approve-or-deny logic.

Behavioral Biometrics: Detecting Fraud When Credentials Are Correct

One of the most significant fraud detection technology trends in recent years is the rise of behavioral biometrics. This technology analyzes how a person interacts with a device, including typing rhythm, mouse movement patterns, scrolling speed, and touch pressure on mobile, to build a behavioral profile that is extremely difficult to replicate.

The practical value is straightforward: even when an attacker has stolen valid login credentials, their behavioral pattern will differ from the legitimate user’s. A paste action where the user normally types, an unusually fast navigation sequence, or a completely different touch pattern on a mobile device all generate risk signals that complement traditional authentication. This is particularly powerful for detecting account takeover (ATO) attacks, where the attacker enters the correct password but interacts with the application in a fundamentally different way.

Did You Know

Behavioral biometrics can distinguish between a legitimate user and an impersonator with over 95% accuracy based solely on typing cadence and mouse dynamics, even when the attacker has the correct username and password.

Device Intelligence: The First Layer of Defense You Cannot Skip

Device intelligence goes beyond simple device fingerprinting. While fingerprinting assigns a unique identifier to a browser or device, intelligence adds a risk interpretation layer: Is this an emulator? Has the device been associated with fraud in other contexts? Is the browser configuration consistent with the claimed geography? Are there signs of automation or remote access tools?

This layer is critical because it operates before the user even enters credentials. A device flagged as an emulator or linked to a known fraud network can be challenged or blocked immediately, reducing the volume of attacks that reach downstream controls. Combined with behavioral biometrics, device intelligence creates a strong pre-authentication barrier that significantly raises the cost for attackers.

Fraud moves faster than manual controls can react. Discover how Detelix provides real-time visibility into your most sensitive ERP processes and stops threats before money leaves your organization.

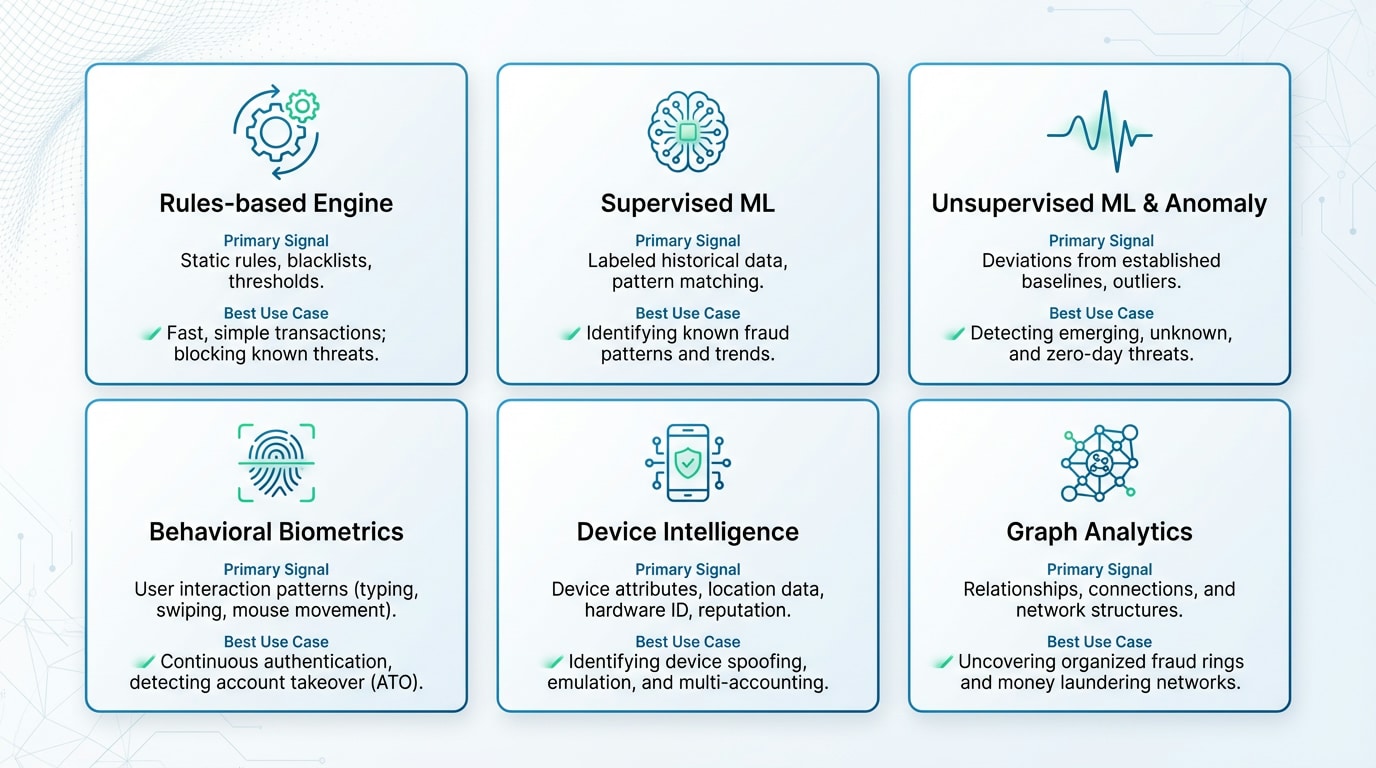

Comparing Key Fraud Detection Technologies at a Glance

| Technology | Primary Signal | Best Use Case | Key Limitation |

|---|---|---|---|

| Rules-based engine | Known patterns and thresholds | Regulatory compliance, clear policy enforcement | Cannot adapt to novel attack methods |

| Supervised ML | Historical labeled fraud data | High-volume transaction scoring | Requires quality labeled data and retraining |

| Unsupervised ML / Anomaly | Statistical deviation from normal | Detecting unknown or emerging fraud | Higher false-positive rate without tuning |

| Behavioral biometrics | User interaction patterns | Account takeover detection | Needs sufficient session data to build profile |

| Device intelligence | Device and environment attributes | Bot mitigation, emulator detection | Privacy constraints may limit signal depth |

| Graph analytics | Entity relationships and networks | Fraud ring and mule network detection | Computational cost at scale |

Graph Analytics: Uncovering Hidden Fraud Networks

Many fraud schemes are not isolated events. They are organized networks. A single mule account may be linked to dozens of synthetic identities, shared devices, and common IP addresses. Traditional tabular models evaluate each transaction independently, missing the web of connections that reveals the broader operation.

Graph analytics maps entities such as accounts, devices, addresses, phone numbers, and payment destinations as nodes and their interactions as edges. Community detection algorithms then identify clusters of suspicious activity, even when individual transactions appear legitimate. This is the technology behind busting chargeback rings, detecting promo abuse at scale, and identifying synthetic identity schemes where multiple fabricated personas share underlying real data points. Platforms whose algorithms ensure every action is monitored for interconnected risk signals can surface these network-level threats in near real time.

Tip

When evaluating fraud detection platforms, ask whether the system can map entity relationships across accounts, devices, and payment destinations. Transaction-level scoring alone will miss coordinated fraud rings that operate across multiple seemingly independent accounts.

Common Mistakes Organizations Make When Deploying Fraud Detection

Despite significant investment, many organizations undermine their own fraud detection capabilities through avoidable errors. The first is over-reliance on rules without ML augmentation. Static thresholds erode quickly as attackers adapt. The second is treating fraud prevention as a one-time project rather than a continuous operational function that requires monitoring, tuning, and feedback loops.

A third common mistake is ignoring the false-positive cost. Every legitimate transaction that is blocked or delayed has a business impact: lost revenue, customer frustration, and wasted analyst time. Organizations that do not measure and actively manage their false-positive rate often discover that their fraud controls are causing more financial damage than the fraud itself. Finally, siloed data, where payment data, identity data, and behavioral data sit in separate systems, prevents the holistic view that modern detection requires.

Did You Know

Research indicates that for every dollar of actual fraud loss, organizations spend an average of $4.41 in associated costs, including investigation time, manual review labor, customer friction, and false-positive handling. Reducing false positives delivers outsized financial returns.

How to Measure Success in a Fraud Prevention Program

| Metric | What It Tells You | Target Direction |

|---|---|---|

| Fraud detection rate | Percentage of actual fraud caught by the system | Higher is better |

| False-positive rate | Percentage of legitimate actions incorrectly flagged | Lower is better |

| Manual review rate | Proportion of decisions requiring human intervention | Lower (without increasing fraud rate) |

| Time-to-decision | Latency from event to approve/deny | Lower (sub-second for real-time channels) |

| Cost per review | Operational cost of each manual investigation | Lower through automation |

| Chargeback / loss rate | Financial loss from fraud that was not prevented | Lower |

Tracking these metrics consistently allows leadership to make data-driven decisions about where to invest in additional controls, where to relax thresholds, and where process changes, rather than technology changes, will have the greatest impact.

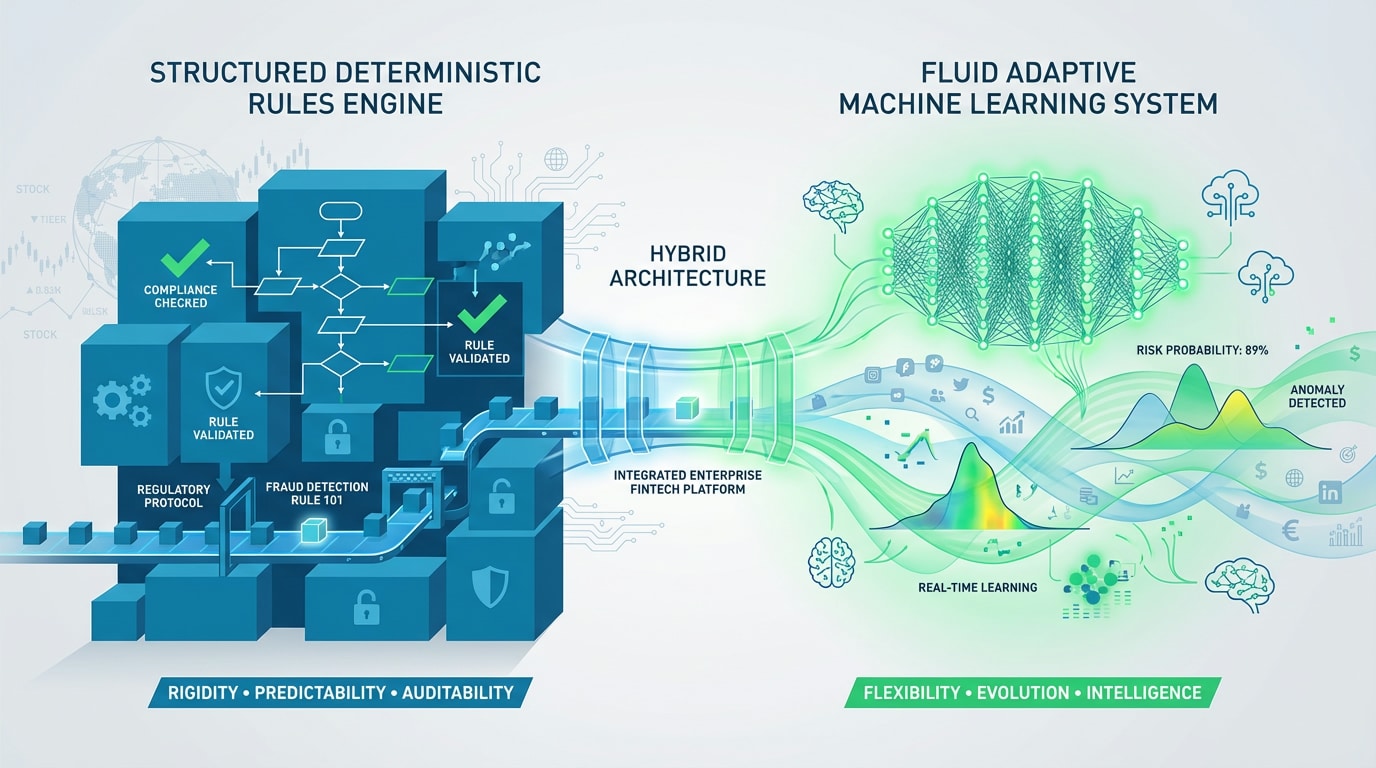

Rules vs. Machine Learning: Which Approach Wins?

The honest answer is neither, on its own. Rules provide transparency and deterministic behavior, which is essential for regulatory compliance and for blocking clearly prohibited actions such as transactions to sanctioned entities. Machine learning provides adaptability and pattern recognition across high-dimensional data that no human rule-writer could replicate.

The winning architecture in 2025 is hybrid. Rules serve as guardrails, enforcing hard boundaries that cannot be overridden. ML models operate within those boundaries, scoring risk on a continuous scale and enabling nuanced decisions like dynamic step-up authentication. This combination ensures that compliance requirements are met while the system continuously adapts to new fraud techniques without requiring manual rule updates for every emerging threat.

Tip

Maintain a clear separation between compliance rules (hard blocks for sanctioned entities, regulatory limits) and risk-scoring models (ML-driven, adaptive). Review compliance rules quarterly and retrain risk models monthly to keep both layers effective against evolving threats.

Step-Up Authentication: Moving Beyond Weak OTP

One-time passwords (OTP) delivered via SMS have been a standard second factor for years, but they are increasingly vulnerable. SIM-swap attacks, phishing pages that capture OTPs in real time, and social engineering calls that trick users into sharing codes have all eroded OTP reliability. As noted in official guidance from the Bank of Israel on digital financial fraud, social engineering and phishing remain among the most prevalent attack vectors targeting financial consumers.

The trend in 2025 is toward phishing-resistant authentication: cryptographic device-bound credentials, biometric verification with liveness detection, and context-aware challenges that adapt to the risk level of the specific action. Step-up should be triggered dynamically, not applied uniformly, so that low-risk actions proceed without friction while high-risk moments receive genuinely stronger verification.

Did You Know

SIM-swap attacks increased by over 300% between 2021 and 2024 globally. Financial regulators in multiple jurisdictions now explicitly recommend against SMS-based OTP as a sole second factor for high-value transactions.

Continuous Authentication: Why Login Is No Longer Enough

A successful login proves identity at a single point in time. But what happens if a session is hijacked mid-use, or if a user hands off their device to someone else after authenticating? Continuous authentication addresses this gap by evaluating behavioral and contextual signals throughout the session, not just at the front door.

If the behavioral profile shifts significantly during a session, such as a different typing rhythm, sudden use of remote access tools, or navigation to sensitive areas that the user has never accessed before, the system can trigger a re-authentication challenge or limit the available actions. This is particularly relevant for ERP environments where a single authenticated session may grant access to supplier payments, bank account changes, and payroll modifications. Detelix continuously monitors these sensitive processes, flagging deviations from expected behavior so that organizations can act before damage occurs.

Tip

For ERP users with access to payment and payroll functions, enable continuous session monitoring that tracks behavioral consistency. A session that starts on a desktop and suddenly shows mobile touch patterns, or navigates to admin functions the user has never accessed, should trigger an immediate re-verification challenge.

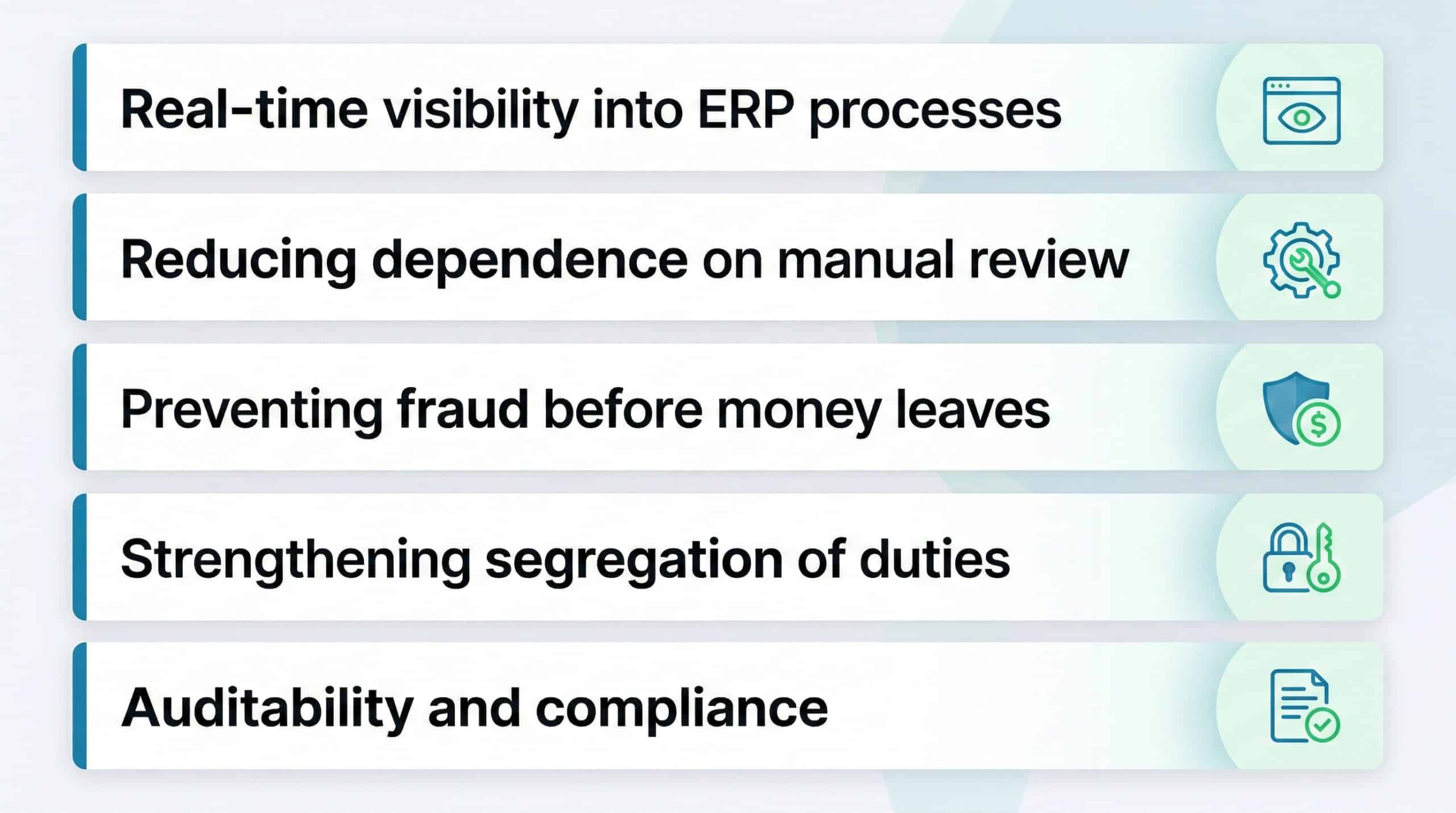

How Detelix Addresses Key Business Needs in Fraud Prevention

| Business Need | How Detelix Helps in Practice |

|---|---|

| Real-time visibility into ERP processes | Continuously scans and cross-checks actions across procurement, payments, payroll, and bank reconciliation, alerting teams to exceptions as they happen |

| Reducing dependence on manual review | Automates detection of human errors, policy deviations, and suspicious patterns, freeing analysts to focus on high-priority cases |

| Preventing fraud before money leaves | Flags unauthorized bank account changes, duplicate payments, and unusual supplier activity before transactions are finalized |

| Strengthening segregation of duties | Monitors SoD violations in real time, identifying when the same individual initiates and approves a sensitive action |

| Auditability and compliance | Maintains a clear trail of alerts, decisions, and investigations to support internal audit and regulatory requirements |

Explainable AI: The Regulatory Imperative Behind Model Transparency

As AI-driven decisions affect more financial processes, regulators increasingly demand that organizations explain why a model flagged or approved a specific transaction. Black-box models that produce a score without a rationale create legal, ethical, and operational risks. An inter-ministerial effort in Israel is already developing regulatory principles for AI use in the financial sector, signaling that explainability requirements will tighten.

In practice, explainable AI (XAI) means providing investigators and auditors with the top contributing factors behind each risk score, such as “new device,” “unusual transaction amount,” “velocity exceeds historical pattern,” or “linked to flagged entity.” This transparency not only satisfies compliance but also improves operational efficiency: analysts who understand why a case was escalated can resolve it faster and provide more accurate feedback to the model.

Did You Know

The EU AI Act, which entered into force in 2024, classifies financial fraud detection systems as high-risk AI applications. This classification requires organizations to maintain documentation of model logic, conduct regular bias assessments, and provide meaningful explanations for automated decisions.

Privacy, Bias, and Ethical Signal Collection

Collecting behavioral, device, and network signals raises legitimate privacy concerns. Organizations must balance fraud prevention effectiveness with data minimization principles, consent frameworks, and evolving privacy regulations. The practical approach in 2025 is to collect only the signals that demonstrably improve detection accuracy, anonymize or pseudonymize where possible, and maintain clear data retention policies.

Bias is equally important. If a model disproportionately flags transactions from certain demographics or geographies without a genuine risk basis, it creates both ethical harm and regulatory exposure. Regular bias audits, diverse training data, and human review of edge cases are becoming standard components of responsible fraud detection programs.

Tip

Schedule quarterly bias audits on your fraud detection models. Examine whether alert rates vary disproportionately across customer segments without a corresponding difference in confirmed fraud rates. Document findings and remediation steps for regulatory readiness.

Building Layered Defenses Without Slowing Down the Business

The concept of layered defense is well established, but the challenge lies in implementation. Too many layers without orchestration create latency, conflicting decisions, and alert fatigue. The 2025 approach is signal orchestration: a single decision engine ingests signals from multiple sources, including device, behavior, identity, network, and business rules, and produces one unified risk assessment per event.

This architecture allows organizations to add or remove signal sources without redesigning the entire detection flow. It also enables consistent policy enforcement across channels, whether web, mobile, or API, so that a fraudster cannot simply switch channels to bypass controls. For ERP-centric organizations, this means the same detection logic that monitors online payments also watches internal procurement approvals and payroll changes.

Did You Know

Organizations using a unified signal orchestration approach report 35% fewer false positives and 25% faster investigation times compared to those running multiple disconnected fraud detection tools that each produce independent alerts.

Detelix Fraud Prevention Solutions

Proactive Monitoring

Continuous scanning of ERP processes to detect anomalies, policy violations, and suspicious patterns before they result in financial loss.

Real-Time Alerts

Instant notifications when high-risk actions occur across procurement, payments, payroll, and bank account management workflows.

Gatekeeper

Automated enforcement of segregation of duties and approval policies, blocking unauthorized actions before transactions are finalized.

Experience & Expertise

Deep domain knowledge in financial controls, ERP security, and regulatory compliance, backed by ISO 27001 and ISO 27799 certifications.

See Detelix in Action

Frequently Asked Questions

What is the single most important fraud detection technology trend in 2025?

The convergence of real-time decisioning with AI-driven analysis is the most impactful trend. Organizations are moving from batch-based, after-the-fact reviews to systems that evaluate risk within milliseconds, before a transaction is completed and before money leaves the organization. This shift is driven by instant payment adoption and the increasing sophistication of attacks that exploit any delay in detection.

Can rules-based systems still play a role alongside machine learning?

Yes. Rules remain essential for enforcing clear regulatory requirements, blocking known prohibited actions, and providing deterministic guardrails. The most effective deployments use a hybrid architecture where rules handle hard boundaries and ML handles nuanced risk scoring. This combination delivers both compliance and adaptability.

How does an organization reduce false positives without increasing fraud exposure?

By enriching the decision with higher-quality signals such as behavioral biometrics, device intelligence, and network context, and by using dynamic thresholds that adjust based on transaction value, customer history, and channel risk. Step-up authentication for medium-risk cases, rather than outright blocking, preserves revenue while maintaining security.

Why is continuous authentication gaining importance over traditional login-based security?

Login-based authentication validates identity only once. If a session is hijacked or a device is handed to another person after login, traditional security offers no protection. Continuous authentication monitors behavioral and contextual signals throughout the session, detecting anomalies that indicate the authenticated user is no longer in control.

What role does graph analytics play in detecting organized fraud?

Graph analytics maps relationships between entities such as accounts, devices, addresses, and payment destinations and identifies clusters of connected suspicious activity. This is critical for detecting fraud rings, mule networks, and synthetic identity schemes where individual transactions may appear legitimate but the network-level pattern reveals coordinated abuse.

How should organizations approach the build-vs-buy decision for fraud detection?

Building an in-house system offers maximum customization but requires significant investment in data science talent, infrastructure, and ongoing maintenance. Buying a specialized platform provides faster time-to-value, pre-built models, and continuous updates. Most organizations benefit from a hybrid approach: a core platform that handles detection and decisioning, with custom rules and integrations tailored to their specific ERP processes and risk profile.

Ready to Close the Gaps in Your Fraud Defenses?

Is your organization confident that its current controls can detect fraud before damage occurs? Move from routine monitoring to real, continuous control across your most sensitive business processes.