Stay Ahead of Financial Crime with Intelligent Fraud Detection

Detelix delivers real-time, multi-layered fraud prevention for enterprise ERP environments. Get expert guidance tailored to your organization.

- What Are the Defining Fraud Detection Technology Trends for 2025?

- How Is Modern Fraud Prevention Technology Evolving to Meet AI-Driven Threats?

- Why Is Fraud Technology Innovation Shifting Toward Real-Time Decisioning?

- A Common Mistake: Treating Fraud Detection and Fraud Prevention as the Same Thing

- How Can Businesses Implement Advanced Fraud Detection Without Increasing Friction?

- What Does a 2025 Fraud Prevention Stack Actually Look Like?

- When Does a Hybrid Approach (Rules + ML) Outperform Either Method Alone?

- Graph Analytics: Uncovering Fraud Networks That Transaction-Level Analysis Misses

- Scenario: How Account Takeover Attacks Evolve Past the Login Page

- Measuring Success: Which KPIs Actually Matter for Fraud Detection Systems?

- How Privacy Regulations Shape the Technology You Can Deploy

- Five Mistakes Organizations Make When Building a Fraud Detection Capability

- How Detelix Addresses Core Fraud Prevention Needs Across Business Processes

- Why Explainability Is Becoming a Non-Negotiable Requirement

- The Privacy-Security Balance: Behavioral Monitoring Without Overreach

- Frequently Asked Questions

Financial crime attack methods are advancing at a pace that outstrips most organizations’ defensive capabilities. In 2025, the divide between companies clinging to legacy controls and those deploying real-time, intelligent defense has never been wider. Digital transactions dominate, remote operations have broadened the attack surface, and generative AI has armed fraudsters with tools that were unavailable even two years ago. For senior leaders responsible for revenue protection, operational continuity, and regulatory compliance, mastering the latest fraud detection technology trends is a strategic imperative — not a technical footnote.

Key Takeaways

- Real-time decisioning — stopping fraud at the moment of execution — is replacing post-incident investigation as the standard for effective fraud prevention.

- Hybrid architectures combining rules-based logic with adaptive machine learning consistently outperform either approach used in isolation.

- Graph analytics reveal coordinated fraud networks and synthetic identity clusters invisible to transaction-level monitoring alone.

- Continuous session monitoring after authentication is critical, as modern account takeover attacks increasingly occur post-login.

- Explainability and regulatory compliance are non-negotiable — every automated decision must be traceable to specific signals and logic.

- Balancing security with privacy requires data minimization, purpose limitation, and passive behavioral analysis that reduces friction for legitimate users.

What Are the Defining Fraud Detection Technology Trends for 2025?

The most significant shift this year is the move from reactive investigation to proactive, real-time decisioning. Organizations no longer have the luxury of reviewing suspicious activity days or weeks after it occurs. By then, the money is gone, the data is compromised, and the damage is done. The fraud tech trends 2025 landscape is defined by three converging forces.

First, the integration of diverse data signals — device, behavioral, transactional, and relational — into a unified risk score that updates in milliseconds. Second, the deployment of machine learning models that adapt continuously to new attack patterns without waiting for a human analyst to write a new rule. Third, the expansion of monitoring from single checkpoints (like login or payment) to continuous session-level oversight.

Tip

Audit your current fraud detection stack against all three forces: unified data signals, adaptive ML models, and continuous session monitoring. If any one of these is missing, you have a structural blind spot that sophisticated attackers will exploit.

These three forces together represent a fundamental change in how organizations think about fraud detection technology trends: the goal is no longer to catch fraud after it happens, but to prevent damage before it occurs. Organizations seeking genuine control over their financial processes need a team of experts who combine deep domain knowledge with cutting-edge technology to stay ahead of emerging threats.

How Is Modern Fraud Prevention Technology Evolving to Meet AI-Driven Threats?

Generative AI has fundamentally altered the threat landscape. Attackers now use large language models to craft phishing emails indistinguishable from legitimate corporate communications. They employ voice-cloning tools to impersonate executives on phone calls. They generate synthetic documents — invoices, identity papers, contracts — that pass visual inspection. Modern fraud prevention technology must therefore evolve beyond pattern matching into something far more nuanced.

Did You Know

Voice-cloning technology has reached the point where a three-second audio sample can generate a convincing replica of a person’s voice, making phone-based social engineering attacks dramatically more effective than traditional impersonation attempts.

Machine learning models trained on behavioral and contextual signals are becoming essential. These models do not simply compare a transaction against a static list of rules; they evaluate whether the entire sequence of actions — from login to navigation to data entry to payment submission — is consistent with the known profile of the legitimate user. When applied to specific business processes like pricing and discount monitoring, ML-based fraud detection can identify revenue leakage patterns that would remain invisible to manual review.

The Rise of Synthetic Identity and Deepfake Detection

Synthetic identity fraud combines real and fabricated personal details to create entirely new “people” who can open accounts, build credit, and extract value over months or years. Because there is often no real victim to file a complaint, these schemes can operate undetected for extended periods. Advanced fraud detection models now analyze digital footprint consistency — does the email age match the claimed identity? Does the device history align with the stated geography? Are there network connections to known fraudulent entities? These cross-referencing capabilities, impossible for human analysts to perform at scale, represent the frontline of fraud technology innovation.

Why Is Fraud Technology Innovation Shifting Toward Real-Time Decisioning?

The answer is straightforward: speed determines loss. In an era of instant payments, same-day settlements, and automated ERP workflows, a fraudulent transaction that is not stopped at the moment of execution may be irreversible within minutes. Post-mortem analysis, no matter how thorough, cannot recover funds that have already left the organization.

Tip

Map the time-to-irrecoverability for your highest-value transaction types. If your fraud detection system’s average decision latency exceeds that window, you are operating a detection system, not a prevention system — and the gap represents direct financial exposure.

Real-time decisioning requires a specific architectural approach. Data must flow from multiple sources into a centralized engine that can evaluate risk, apply models, and return a decision — approve, challenge, or block — within milliseconds. This is not merely a technology challenge; it requires organizational alignment between fraud teams, IT, operations, and compliance. The trend toward government-level real-time monitoring reinforces this point. Israel’s “Israel Invoices” initiative, for example, introduced real-time tracking and authentication of invoices to combat identity theft and fake invoicing — a model that illustrates how real-time verification is becoming a regulatory expectation, not just a competitive advantage.

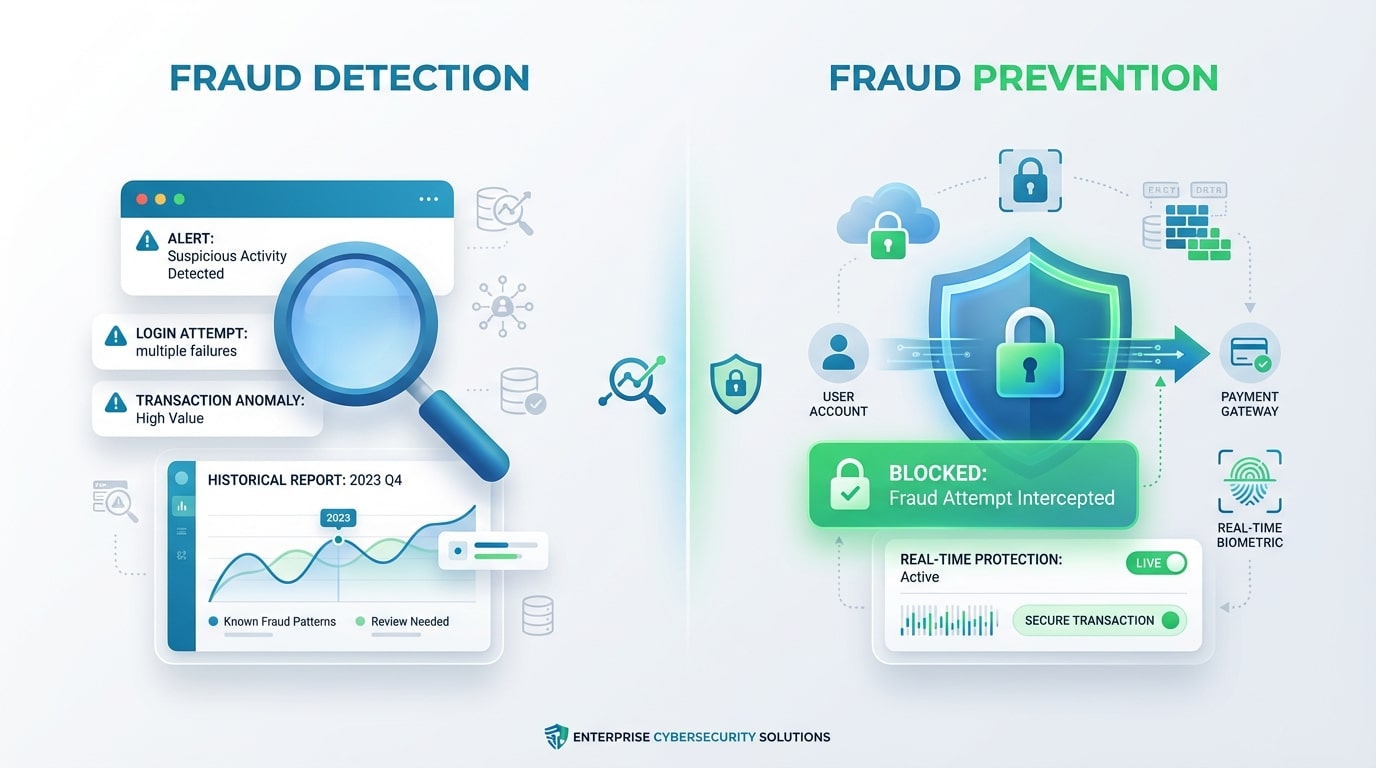

A Common Mistake: Treating Fraud Detection and Fraud Prevention as the Same Thing

Many organizations conflate detection with prevention, and this confusion creates dangerous gaps. Fraud detection identifies suspicious events. Fraud prevention stops those events from causing damage. A system that generates alerts without the ability to intervene in real time is a detection tool. A system that can pause a payment, trigger a step-up authentication challenge, or route a transaction for manual review before it is executed is a prevention tool.

Did You Know

Organizations that rely solely on detection-only systems typically discover fraud an average of 14 days after the initial unauthorized action, by which time recovery of funds drops below 20% in most cases involving electronic transfers.

The practical consequence of this distinction is significant. Detection-only systems produce reports that arrive after the fact. Prevention systems integrate directly into the transaction workflow, acting as an organizational gatekeeper. The most effective modern architectures combine both: they detect anomalies using advanced analytics and then prevent damage through automated decisioning and case management workflows that ensure every flagged event receives appropriate action.

How Can Businesses Implement Advanced Fraud Detection Without Increasing Friction?

This is perhaps the most critical question for any organization that serves customers directly. Every additional verification step — every CAPTCHA, every SMS code, every manual review delay — creates friction that can drive legitimate customers away. The business cost of false positives is not just operational; it includes lost revenue, damaged brand trust, and increased customer support costs. Data from the Bank of Israel’s consumer information center shows that customer complaints related to banking and payment services often stem from exactly this kind of friction.

Tip

Calculate your false positive cost per incident — including customer support time, lost revenue from abandoned transactions, and brand impact. Compare this figure against your fraud loss rate. Many organizations discover that false positive costs exceed actual fraud losses by a factor of three to five.

The solution lies in passive authentication and behavioral analysis. Instead of asking the user to prove their identity, the system observes how they interact with the application — typing speed, mouse movement patterns, scrolling behavior, navigation sequences — and compares these signals against their established profile. When the algorithms ensure every action within a system is validated in the background, legitimate users experience zero friction while suspicious sessions are flagged for escalation. This is the essence of modern fraud prevention technology: invisible to the good actor, impenetrable for the bad one.

What Does a 2025 Fraud Prevention Stack Actually Look Like?

A modern fraud prevention stack is not a single product. It is a layered architecture where each layer addresses a different dimension of risk. The table below maps the core layers, their function, and the signals they analyze.

| Layer | Function | Key Signals |

|---|---|---|

| Device Intelligence | Identify and assess the device used for access | Device fingerprint, emulator detection, known fraud device lists |

| Behavioral Biometrics | Verify user identity through interaction patterns | Typing cadence, mouse dynamics, touch pressure, navigation flow |

| Transactional Analysis | Evaluate individual transactions against risk models | Amount, frequency, recipient, timing, deviation from baseline |

| Session Monitoring | Continuous oversight from login to logout | Page sequence, time-on-page, data entry patterns, session hijack indicators |

| Network/Graph Analytics | Detect connections between entities across accounts | Shared devices, shared addresses, linked beneficiaries, mule network patterns |

Detelix focuses on the intersection of these layers within complex ERP environments, where sensitive business processes like supplier payments, bank account changes, and payroll modifications require continuous, real-time cross-checking that goes beyond what any single layer can provide.

Your fraud prevention architecture should match the sophistication of the threats targeting your organization. Speak with Detelix experts to assess your current defenses and identify critical gaps.

When Does a Hybrid Approach (Rules + ML) Outperform Either Method Alone?

There is an ongoing debate in the fraud prevention community about rules-based systems versus machine learning. The reality is that the debate is largely settled: hybrid approaches win in almost every operational scenario. Rules provide transparency and explainability — essential for regulatory compliance and audit trails. Machine learning provides adaptability and pattern recognition across high-dimensional data — essential for catching novel attack vectors.

Did You Know

Pure rules-based fraud systems typically require 60 to 90 days to create and deploy a new rule after a novel attack pattern is identified. Machine learning models trained on behavioral data can detect similar emerging patterns within hours of their first appearance in the data stream.

A pure rules-based system breaks down when attackers introduce variations that fall outside predefined parameters. A pure ML system can produce opaque decisions that are difficult to explain to regulators or to internal stakeholders. The hybrid model uses rules as guardrails and ML as the adaptive engine. Rules handle known fraud typologies and compliance requirements. ML models handle the unknown — emerging patterns, subtle anomalies, and cross-signal correlations that no human analyst could write a rule for in advance.

Graph Analytics: Uncovering Fraud Networks That Transaction-Level Analysis Misses

One of the most powerful fraud detection technology trends in 2025 is the adoption of graph-based analytics. Traditional transaction monitoring evaluates each event in isolation: is this payment suspicious? Graph analytics asks a different question: is this payment connected to other suspicious activity across the network?

Consider a scenario where a single fraudulent transaction might appear normal in isolation — a reasonable amount, to a known vendor, during business hours. But graph analysis reveals that the vendor’s bank account was recently changed, the new account is linked to three other vendors who also recently changed accounts, and all three share a device fingerprint. This pattern — invisible at the transaction level — is immediately obvious when viewed through a relational graph. Graph analytics is particularly effective against mule networks, coordinated fraud rings, and synthetic identity clusters that operate across multiple accounts and entities.

Tip

Start your graph analytics initiative by mapping vendor bank account changes against shared device fingerprints and IP addresses. This single cross-reference often reveals coordinated fraud rings that transactional monitoring alone would never surface.

Scenario: How Account Takeover Attacks Evolve Past the Login Page

A common misconception is that account takeover (ATO) is a login-stage problem. If you protect the login with multi-factor authentication, the account is safe. This assumption is dangerously incomplete. Modern ATO attacks increasingly occur after successful authentication. An attacker who has obtained valid credentials — through phishing, credential stuffing, or social engineering — logs in legitimately and then changes account settings, redirects payments, or exfiltrates data.

This is why continuous session monitoring is becoming a non-negotiable requirement. The system must evaluate not just whether the login was valid, but whether the post-login behavior matches the expected profile. A legitimate user who logs in and navigates directly to their usual workflow looks fundamentally different from an attacker who logs in and immediately accesses settings, changes contact information, and initiates an unusual payment. Behavioral signals throughout the session — not just at the gate — are what separate real control from the illusion of control.

Did You Know

Research indicates that over 60% of successful account takeover attacks involve valid credentials obtained through phishing or data breaches, meaning the initial login passes multi-factor authentication without triggering any alert. Post-authentication behavior monitoring is the only layer that catches these intrusions.

Measuring Success: Which KPIs Actually Matter for Fraud Detection Systems?

Many organizations measure their fraud systems by a single metric: how many fraudulent transactions were caught. While important, this metric alone is dangerously incomplete. A system that catches 95% of fraud but blocks 10% of legitimate transactions is destroying business value. The table below outlines the KPIs that provide a balanced view of system performance.

| KPI | What It Measures | Why It Matters |

|---|---|---|

| Detection Rate (True Positive Rate) | Percentage of actual fraud correctly identified | Core effectiveness metric |

| False Positive Rate | Percentage of legitimate transactions incorrectly flagged | Directly impacts customer experience and operational cost |

| False Negative Rate | Percentage of actual fraud that was missed | Measures residual risk exposure |

| Decision Latency | Time from event to decision (approve/block/challenge) | Determines whether prevention is truly real-time |

| Investigation Efficiency | Average time to resolve a flagged case | Reflects operational scalability |

| Net Fraud Loss Rate | Total fraud losses as percentage of transaction volume | The bottom-line financial impact |

Detelix provides organizations with this kind of multi-dimensional visibility across their ERP processes, ensuring that the measurement framework captures not only what was caught but also what the controls cost in terms of operational efficiency and customer impact.

How Privacy Regulations Shape the Technology You Can Deploy

Advanced fraud detection technology does not operate in a regulatory vacuum. Behavioral biometrics, device fingerprinting, and session monitoring all involve the collection and processing of personal data. In Israel, the Privacy Protection Authority requires registration of databases that contain sensitive personal information, and organizations must ensure their fraud prevention systems comply with data minimization, purpose limitation, and security requirements under the Privacy Protection Regulations (Information Security) 2017.

Tip

Before deploying any new behavioral monitoring or device fingerprinting technology, conduct a Data Protection Impact Assessment using the Privacy Protection Authority’s structured framework. This proactive step reduces legal exposure and demonstrates due diligence to regulators and auditors.

Organizations deploying new fraud detection technologies should conduct a Data Protection Impact Assessment (DPIA) to evaluate privacy risks. The Privacy Protection Authority’s digital DPIA tool provides a structured framework for assessing technologies like session monitoring and behavioral signals before deployment. This is not merely a compliance exercise — it is a business protection measure that reduces legal exposure and builds customer trust.

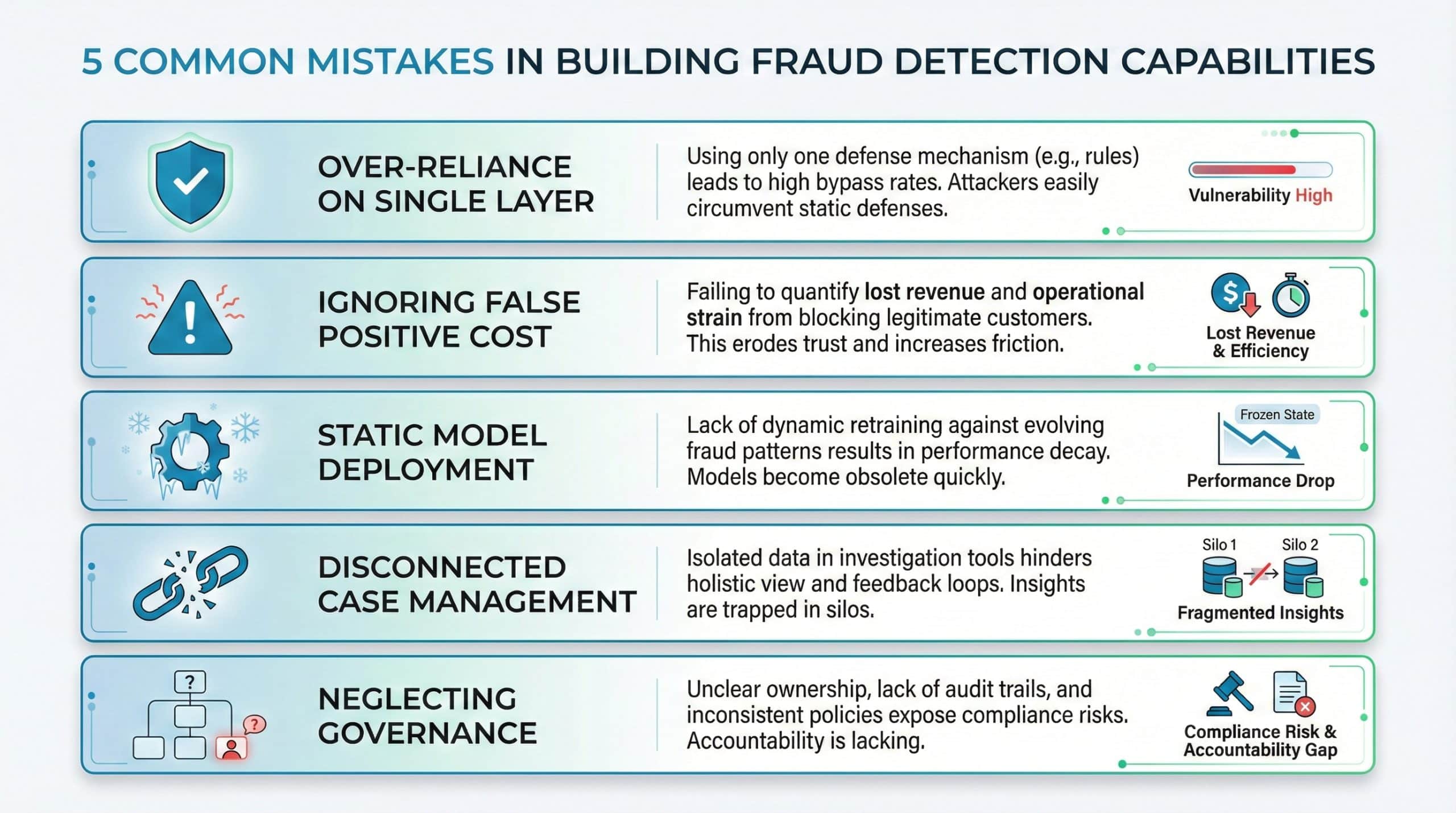

Five Mistakes Organizations Make When Building a Fraud Detection Capability

Building an effective fraud detection capability is as much about avoiding common pitfalls as it is about adopting the right technology. Based on patterns observed across finance, banking, and enterprise operations, the following mistakes appear consistently.

Mistake 1: Over-reliance on a single layer. Organizations that depend entirely on transaction rules or entirely on ML models leave blind spots that sophisticated attackers exploit. A multi-layered approach is essential.

Mistake 2: Ignoring the false positive cost. Measuring only detection rate without tracking how many legitimate customers or transactions are impacted creates a distorted picture of system performance. The business cost of false positives often exceeds the cost of the fraud itself.

Mistake 3: Static model deployment. Fraud patterns evolve continuously. Models that are trained once and deployed without regular retraining and recalibration degrade rapidly in effectiveness.

Did You Know

Machine learning models used in fraud detection typically experience measurable performance degradation within 45 to 60 days of deployment if they are not retrained on fresh data. Automated retraining pipelines that run on weekly or bi-weekly cycles maintain detection accuracy significantly better than quarterly manual updates.

Mistake 4: Disconnected case management. Alerts without a structured investigation and resolution workflow create backlogs, missed escalations, and incomplete audit trails. When a security incident does occur, organizations must be prepared to file an immediate incident report with supporting evidence — logs, screenshots, and documented actions.

Mistake 5: Neglecting governance. Technology without clear ownership, accountability, and policy frameworks fails to deliver sustained value. The appointment of a dedicated information security officer and the establishment of clear data handling procedures are not optional extras — they are foundational requirements, as highlighted in official audit findings that documented organizational failures in these exact areas.

How Detelix Addresses Core Fraud Prevention Needs Across Business Processes

| Business Need | How Detelix Helps in Practice |

|---|---|

| Real-time visibility into ERP transactions | Continuous monitoring of sensitive processes — supplier payments, bank account changes, payroll — with automated alerts before damage occurs |

| Reducing manual review workload | Automated cross-checking and risk scoring that surfaces only genuine exceptions, allowing teams to focus on high-priority cases |

| Compliance and audit readiness | Structured documentation of every flagged event, decision, and resolution — ready for internal audit, external regulators, or forensic review |

| Adapting to evolving threats | Flexible rule and model configuration that can be updated as new fraud patterns emerge, without requiring full system replacement |

| Segregation of duties enforcement | Automated detection of SoD violations across ERP roles and permissions, flagging conflicts before they enable unauthorized actions |

Tip

When evaluating fraud prevention vendors, ask specifically how their system handles segregation of duties enforcement within your ERP. SoD violations are one of the most common enablers of internal fraud, and many solutions overlook this critical control layer entirely.

Why Explainability Is Becoming a Non-Negotiable Requirement

As organizations deploy increasingly sophisticated ML models for fraud detection, a new challenge emerges: can you explain why a transaction was blocked? Regulators, auditors, and customers all demand transparency. A system that blocks a payment with no clear rationale creates legal risk, compliance exposure, and customer dissatisfaction.

Did You Know

Regulatory bodies across multiple jurisdictions are increasingly requiring that automated financial decisions — including fraud blocks — come with human-readable explanations. Organizations unable to provide this audit trail face growing exposure to regulatory penalties and customer litigation.

Explainability means that every decision produced by the fraud detection system can be traced back to specific signals, rules, or model outputs. This is where the hybrid approach — combining interpretable rules with ML — proves its value again. Rules provide a clear, auditable logic trail. ML models, when designed with explainability in mind (using techniques like SHAP values or decision trees alongside neural networks), can surface the top contributing factors for each risk score. The result is a system that is both powerful and accountable.

The Privacy-Security Balance: Behavioral Monitoring Without Overreach

Continuous behavioral monitoring — tracking how a user interacts with an application throughout their session — raises legitimate privacy concerns. Organizations must draw a clear line between security-motivated monitoring and surveillance. The key principles are data minimization (collect only what is necessary for risk assessment), purpose limitation (use behavioral data exclusively for fraud prevention, not marketing), and transparency (inform users about what data is collected and why).

When these principles are followed, behavioral monitoring becomes a privacy-enhancing technology rather than a privacy-threatening one. It reduces the need for intrusive identity verification steps, replaces them with passive signals, and creates a more secure environment without increasing the data burden on the user. Organizations operating in Israel should align their practices with the guidance provided by the Population and Immigration Authority’s cybersecurity division, which advocates a “defense circles” model encompassing physical, technological, and policy-level controls.

Tip

Document your behavioral monitoring scope in a clear, accessible privacy notice that specifies exactly what signals are collected, how they are processed, and how long they are retained. This transparency builds user trust and provides a defensible position in the event of a regulatory inquiry.

Detelix Fraud Prevention Solutions

Proactive Monitoring

Continuous oversight of sensitive ERP transactions with automated alerts that flag anomalies before they cause financial damage.

Real-Time Alerts

Instant notifications on high-risk activities across your financial systems, enabling immediate intervention and investigation.

GateKeeper

Automated transaction validation that acts as a digital gatekeeper, blocking unauthorized changes to vendor details, bank accounts, and payroll data.

Experience & Expertise

Deep domain knowledge in ERP security and financial process controls, backed by ISO 27001 and ISO 27799 certifications.

See Detelix in Action

Frequently Asked Questions

Can fraud detection systems work without storing sensitive personal data?

Yes, many modern systems use tokenization, hashing, and behavioral signals that do not require storing raw personal identifiers. Device fingerprints and behavioral profiles can be generated and stored as anonymized risk indicators rather than personally identifiable information. The key is designing the system architecture with privacy by design principles from the start.

How long does it take to implement a real-time fraud detection system?

Implementation timelines vary significantly depending on the complexity of the existing technology stack, the number of data sources to integrate, and the maturity of the organization’s risk framework. A focused deployment targeting specific high-risk processes — such as supplier payment monitoring within an ERP — can be operational within weeks. A full enterprise-wide deployment across multiple business lines and geographies typically takes several months.

Is machine learning always better than rules-based detection?

No. Machine learning excels at detecting novel and complex patterns, but rules-based systems are superior for enforcing known compliance requirements and providing clear, auditable decision logic. The most effective approach is hybrid: rules handle known threats and regulatory mandates, while ML models adapt to emerging and unknown attack vectors. Neither approach alone delivers optimal results.

What happens when a legitimate transaction is incorrectly blocked (false positive)?

A well-designed system does not simply block — it challenges. Instead of rejecting a transaction outright, the system can trigger a step-up authentication request (such as a secondary approval or biometric check) that allows the legitimate user to proceed while still stopping an unauthorized actor. Dynamic thresholds based on contextual risk further reduce the likelihood of blocking good transactions.

How do you measure whether your fraud detection investment is delivering value?

Value measurement should go beyond the detection rate. Track net fraud losses (total losses as a percentage of volume), false positive rates and their associated costs (operational and revenue impact), investigation efficiency (time to resolve each case), and customer impact metrics (complaints, abandonment rates). A system that catches more fraud but alienates more customers may not be delivering positive ROI.

Ready to Move From Monitoring to Real-Time Fraud Prevention?

The gap between detecting fraud after it happens and preventing it in real time is the gap between managing risk and eliminating loss. Discover how Detelix delivers continuous, intelligent oversight for your most sensitive business processes.