Detect Financial Crime Before It Costs Your Organization

Real-time ERP monitoring, intelligent alerting, and expert-led fraud prevention — purpose-built for corporate environments.

- Understanding the Fundamentals of Financial Crime Detection

- Why Corporate Financial Crime Is Different

- The Essential Pillars of Financial Crime Prevention

- How Financial Crime Detection Works End to End

- Common Red Flags That Signal Money Laundering or Fraud

- What Separates Effective Sanctions Screening from a Checkbox Exercise

- How KYC, KYB, and CDD Fit into the Detection Framework

- Rules-Based Detection vs. Machine Learning

- The False-Positive Problem

- What Data Does a Detection Program Actually Need

- Graph Analytics: Revealing What Transaction Monitoring Cannot

- Mistakes Organizations Make When Building a Detection Program

- KPIs That Genuinely Measure Detection Effectiveness

- Regulatory Compliance: Detection as a Legal Obligation

- How Detelix Addresses Real Operational Needs

- Choosing a Detection Solution: What to Prioritize

- Frequently Asked Questions

In many organizations, financial controls appear robust on the surface. Approval chains exist, ERP permissions are configured, reconciliations run on schedule, and compliance teams file their reports. Yet beneath this veneer of order, illicit activity can still flow undetected through everyday business processes. A single manipulated vendor record, a cleverly structured series of payments just below reporting thresholds, or an internal actor exploiting a gap in segregation of duties can cause damage that surfaces only months later — if it surfaces at all. Financial crime detection is the discipline that closes this gap, moving organizations from a reactive posture to one of real-time awareness and actionable control.

Key Takeaways

- Financial crime detection operates continuously within ERP and payment systems, surfacing suspicious patterns that periodic audits routinely miss.

- Corporate financial crime hides inside legitimate processes — procurement, payroll, vendor management — and is frequently perpetrated by insiders with authorized access.

- A hybrid approach combining rules-based monitoring with machine learning delivers superior precision and adapts to evolving tactics.

- False positives are not a minor inconvenience — at scale they consume investigator capacity and create the alert fatigue that lets real threats pass unnoticed.

- Graph analytics reveals relationship-based schemes (circular payments, shared bank accounts) that linear transaction monitoring cannot detect.

- Regulatory compliance requires not just detection technology but a documented, auditable investigation workflow from alert through disposition.

Understanding the Fundamentals of Financial Crime Detection

Financial crime detection is a systematic, technology-driven process designed to identify, flag, and prioritize suspicious financial activity before it results in material loss or regulatory exposure. It encompasses transaction monitoring, entity screening, identity and ownership verification, and relationship analysis — all working in concert to surface patterns that human review alone would miss.

Unlike traditional auditing, which typically operates after the fact, modern detection systems run continuously. They ingest transaction data as it flows through banking platforms, ERP systems, and payment gateways, then apply a combination of rules, statistical models, and behavioral baselines to determine whether any given action deviates from expected norms. According to an official audit report on Israel’s financial intelligence authority, the sheer volume of reports submitted by regulated entities makes manual analysis impractical without automated triage and prioritization. This reality applies equally to corporations managing thousands of supplier payments, employee reimbursements, and customer transactions every month.

Tip

Map every data source that feeds financial transactions in your organization — ERP, banking portals, expense management tools, and payroll systems. Detection coverage is only as strong as the data it ingests, and blind spots in ingestion create blind spots in monitoring.

Why Corporate Financial Crime Is Different

When most people think of financial crime, they picture consumer-facing fraud — stolen credit cards or phishing attacks. Corporate financial crime operates on a different plane entirely. It hides inside processes that appear legitimate: procurement cycles, payroll runs, intercompany transfers, and vendor onboarding workflows. The perpetrator is often an insider with authorized access, or an external actor who has compromised a trusted business relationship.

Consider the risk embedded in a typical accounts-payable workflow. A fictitious supplier is created with plausible details, invoices are submitted for services never rendered, and payments are approved because the amounts fall within standard authorization limits. Without cross-referencing bank account ownership, verifying supplier legitimacy at onboarding, and monitoring for duplicate or circular payment patterns, this scheme can persist for years. Organizations that rely on effective protection against embezzlement and fraud errors gain a critical advantage: specialized oversight of the ERP layer where these manipulations actually occur.

Did You Know

According to the Association of Certified Fraud Examiners, the median duration of an occupational fraud scheme is 12 months before detection, and organizations lose an estimated 5% of annual revenue to fraud. The longer a scheme runs undetected, the greater the cumulative financial and reputational damage.

The Essential Pillars of Financial Crime Prevention

Detection and prevention are two sides of the same coin. Prevention aims to stop illicit activity before it enters the system, while detection catches what slips through. Together, they form a feedback loop — every investigated alert teaches the organization something about its vulnerabilities, which in turn strengthens preventive controls.

Key preventive measures include rigorous segregation of duties so that no single person can create a vendor, approve an invoice, and authorize payment; thorough due diligence on new business partners; and ongoing employee awareness programs. Israel’s central bank has emphasized public awareness campaigns as a critical line of defense against financial fraud, and the same principle applies inside corporations. When employees understand what red flags look like — an unusually urgent payment request, a last-minute change to banking details, a vendor with no verifiable address — they become human sensors that complement automated systems.

Tip

Run quarterly tabletop exercises where finance and procurement teams walk through realistic fraud scenarios. This builds pattern-recognition skills that no amount of slide-based training can replicate, and it exposes procedural gaps before a real attacker finds them.

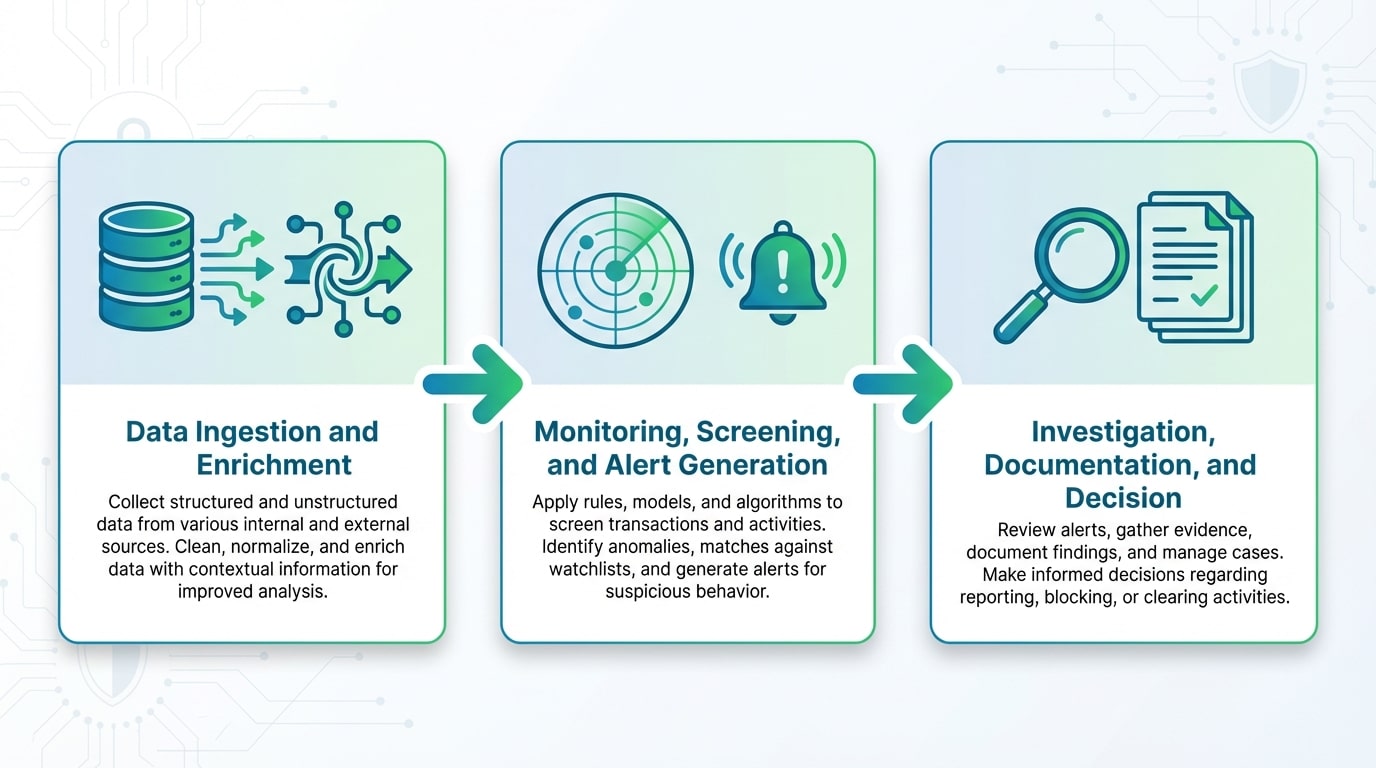

How Financial Crime Detection Works End to End

A mature detection program follows a clear operational lifecycle. Understanding each stage helps organizations identify where their own gaps exist and where automation delivers the greatest return.

Data Ingestion and Enrichment

Everything begins with data. Transaction logs, customer and vendor master files, beneficial ownership records, device metadata, and external watchlists must be collected, normalized, and linked. Data quality is not a secondary concern — it is foundational. Duplicate records, inconsistent naming conventions, and missing fields are the primary sources of both missed detections and false alerts. The goal is to create a unified, reliable view of every entity and every financial action.

Monitoring, Screening, and Alert Generation

Once data flows into the detection engine, algorithms evaluate each transaction or entity event against predefined rules, behavioral baselines, and risk scores. A payment that exceeds a threshold, a new supplier whose bank account matches a known shell-company pattern, or a sudden spike in refund activity all generate alerts. Platforms like Detelix ensure every action in the ERP system is monitored continuously, so anomalies surface in real time rather than during a quarterly review cycle.

Investigation, Documentation, and Decision

Alerts are only as valuable as the investigation process that follows. Case management systems allow analysts to collect evidence, annotate findings, collaborate across departments, and reach a documented decision — escalate, dismiss with rationale, or file a suspicious activity report. Without structured case management, even the most sophisticated detection engine produces inconsistent outcomes and fails under regulatory scrutiny.

Did You Know

Organizations that implement structured case management alongside automated detection reduce their average investigation time by up to 60%, freeing analyst capacity to focus on genuinely complex cases rather than administrative documentation.

Common Red Flags That Signal Money Laundering or Fraud

Experienced investigators recognize certain patterns that recur across industries and geographies. Structuring — splitting a large sum into multiple transactions just below a reporting threshold — remains one of the most common tactics. Rapid movement of funds through multiple accounts with no clear business rationale is another persistent indicator. In a corporate context, watch for vendors that share bank details with employees, invoices with round-number amounts and no supporting documentation, and sudden changes to a long-standing supplier’s payment instructions.

Other signals include activity that is inconsistent with a customer’s or vendor’s known profile, payments routed through high-risk jurisdictions without a clear commercial purpose, and refunds or credits issued to parties different from the original payer. Each flag on its own may have an innocent explanation; the power of detection lies in correlating multiple weak signals into a strong composite indicator.

Tip

Create a documented red-flag matrix specific to your organization’s operations. Generic checklists miss industry-specific risks. A construction company’s red flags (inflated material costs, phantom subcontractors) differ fundamentally from those of a financial services firm (layered wire transfers, dormant account reactivation).

What Separates Effective Sanctions Screening from a Checkbox Exercise

Sanctions screening compares every entity your organization interacts with against published lists of sanctioned individuals, companies, and jurisdictions. The challenge is not the concept — it is the execution. Name-matching algorithms must handle transliterations across languages, common aliases, partial matches, and entities that deliberately alter their names to evade detection.

A checkbox approach screens names at onboarding and never revisits them. Effective screening, by contrast, runs continuously against updated lists and re-evaluates existing relationships whenever a list changes. It also incorporates fuzzy matching, phonetic algorithms, and secondary identifiers like dates of birth and national IDs to reduce both false positives and dangerous misses.

| Screening Dimension | Checkbox Approach | Effective Approach |

|---|---|---|

| Frequency | At onboarding only | Continuous, with every list update |

| Name Matching | Exact string match | Fuzzy, phonetic, and alias-aware |

| Entity Coverage | Primary counterparty | Beneficial owners, directors, related parties |

| Alert Review | Bulk dismiss without documentation | Documented triage with rationale for every decision |

| List Sources | Single national list | Multiple lists (OFAC, EU, UN, local) consolidated |

Did You Know

OFAC updates its Specially Designated Nationals list multiple times per month. Organizations that screen only at onboarding can operate for weeks or months with an active business relationship with a newly sanctioned entity — a compliance failure that carries severe penalties regardless of intent.

Your ERP processes thousands of transactions daily. How many of them receive real-time scrutiny for fraud indicators, sanctions exposure, or segregation-of-duties violations?

How KYC, KYB, and CDD Fit into the Detection Framework

Know Your Customer (KYC) verifies the identity of individual clients. Know Your Business (KYB) does the same for corporate entities, including the critical step of identifying ultimate beneficial owners. Customer Due Diligence (CDD) is the broader framework that determines the depth of verification based on the risk profile of each relationship.

Beneficial Ownership: The Most Common Point of Failure

In B2B environments, layered holding structures, nominee directors, and cross-border registrations can obscure who truly controls a company. When beneficial ownership is not verified — or is verified only once and never updated — shell companies enter the supply chain, and payments flow to parties whose identities are effectively unknown. Regulatory frameworks, including Israeli requirements enforced through financial sanctions on non-compliant institutions, explicitly mandate ongoing verification of ownership and control.

Tip

Schedule automated re-verification of beneficial ownership data for all active suppliers and business partners at least annually. Ownership structures change — through acquisitions, restructurings, or deliberate obfuscation — and what was legitimate at onboarding may not remain so.

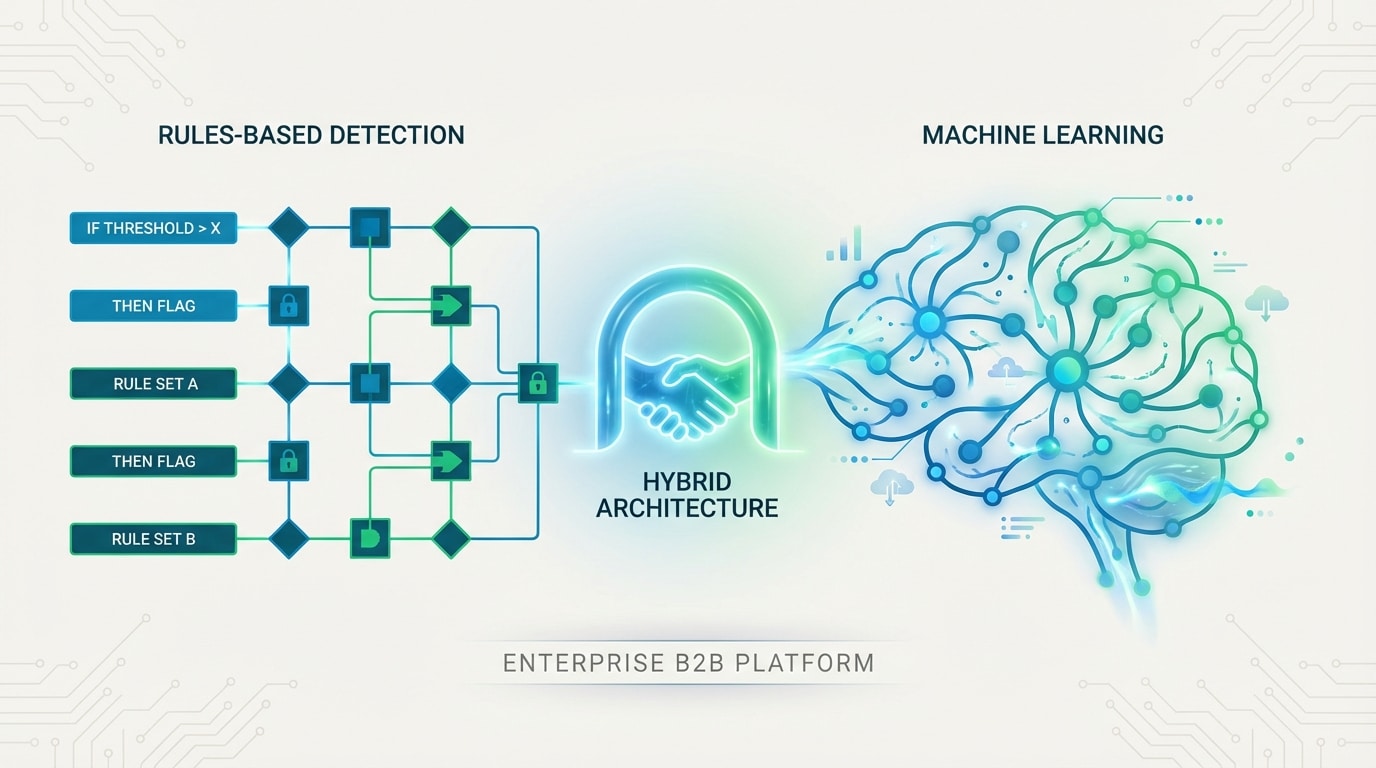

Rules-Based Detection vs. Machine Learning: Which Approach Wins?

This is not an either-or question. Rules-based systems excel at enforcing clearly defined regulatory thresholds and policy limits. They are transparent, auditable, and straightforward to explain to regulators. However, static rules are also predictable — sophisticated actors learn the thresholds and structure their activity to stay just beneath them.

Where Machine Learning Changes the Equation

Machine learning models identify behavioral anomalies that no predefined rule would catch. They learn what “normal” looks like for each entity, segment, or process and flag deviations. Detelix applies machine learning to monitor pricing and discounts, for example, identifying subtle patterns of revenue manipulation that would be invisible to a human auditor reviewing individual transactions. The best practice today is a hybrid architecture: rules for regulatory compliance and policy enforcement, ML for adaptive detection of evolving threats, and a “challenger” model framework that tests improvements without disrupting production.

Did You Know

A hybrid detection architecture that combines static rules with machine learning models typically reduces false-positive rates by 30-50% compared to rules-only systems, while simultaneously improving detection of previously unknown fraud patterns through behavioral anomaly scoring.

The False-Positive Problem — and Why It Matters More Than You Think

A false positive is an alert triggered by legitimate activity. In isolation, it seems like a minor inconvenience. At scale, false positives consume the majority of investigator time, delay legitimate business, erode trust in the detection system, and — most dangerously — create alert fatigue that causes real threats to be overlooked.

The root causes are well understood: rigid thresholds that ignore context, poor data quality that generates phantom matches, and screening algorithms that treat every partial name overlap as a potential hit. Addressing false positives is not about lowering sensitivity; it is about increasing precision without sacrificing recall.

| False-Positive Driver | Impact | Mitigation Strategy |

|---|---|---|

| Static thresholds | High-volume, low-value alerts | Dynamic, risk-segmented thresholds |

| Poor name matching | Excessive screening hits | Fuzzy matching with secondary identifiers |

| Duplicate entity records | Same entity flagged multiple times | Entity resolution and master data management |

| Missing context | Normal behavior flagged as anomalous | Behavioral profiling by segment and product |

| No feedback loop | Same errors repeated | Investigation outcomes fed back into model tuning |

Tip

Track your false-positive rate by rule and by segment every month. When a single rule generates more than 80% false positives consistently, it needs recalibration — not just more investigators to process the queue. Targeted rule tuning based on investigation feedback is the fastest path to meaningful precision improvement.

What Data Does a Financial Crime Detection Program Actually Need?

The answer is broader than most organizations initially assume. Transaction records are the obvious starting point — amounts, dates, counterparties, channels. But effective detection also requires entity data (names, addresses, registration details, ownership structures), behavioral metadata (login times, device fingerprints, geolocation), and external reference data (sanctions lists, PEP databases, adverse media feeds, court records).

Data lineage and quality governance are equally critical. If a vendor’s name is spelled three different ways across three systems, the detection engine may treat them as three separate entities — missing the pattern that connects them. Organizations that invest in master data management and entity resolution before deploying detection technology consistently achieve better precision and lower investigation workloads.

Did You Know

Research consistently shows that data quality issues — duplicate records, inconsistent formatting, and missing fields — are responsible for up to 70% of false-positive alerts in financial crime detection systems. Fixing data upstream eliminates downstream noise more effectively than any algorithmic tuning.

A Scenario Where Graph Analytics Reveals What Transaction Monitoring Cannot

Traditional transaction monitoring evaluates each payment in relative isolation: Does this amount exceed a threshold? Does this frequency deviate from the norm? Graph analytics takes a fundamentally different approach by mapping relationships — between people, companies, accounts, devices, and addresses — and analyzing the structure of those connections.

Imagine a network where five seemingly unrelated suppliers all share a single bank account, or where funds move in a circular pattern: Company A pays Company B, B pays C, C pays a subsidiary of A. No individual transaction looks suspicious. The graph, however, reveals a closed loop designed to create the appearance of legitimate commercial activity. Graph-based metrics like centrality (which nodes are most connected), community detection (which clusters form tightly linked groups), and path analysis (which routes funds travel) surface risks that linear monitoring simply cannot see.

Mistakes Organizations Make When Building a Detection Program

The most consequential mistake is starting with technology before strategy. An organization that deploys a transaction-monitoring platform without first defining its risk appetite, documenting its most vulnerable processes, and establishing a clear investigation workflow will generate thousands of alerts that no one knows how to handle.

Other frequent errors include neglecting data quality (garbage in, garbage out), failing to involve operational teams in rule design (compliance writes rules that do not reflect how the business actually operates), skipping champion-challenger testing (deploying untested model changes directly to production), and treating detection as a one-time project rather than a continuously evolving program. Every model, every rule, and every threshold must be reviewed, tested, and refined on an ongoing basis.

Tip

Before selecting any detection technology, complete a formal risk assessment that maps your top ten highest-exposure processes, quantifies potential loss scenarios, and defines investigation workflows. Technology should be configured to address documented risks — not deployed in search of problems to solve.

Which KPIs Genuinely Measure Detection Effectiveness?

Many organizations track alert volume and case closure rates — metrics that say very little about whether the program is actually catching financial crime. More meaningful KPIs include precision (what percentage of alerts lead to genuine findings), recall (what percentage of known suspicious activity is actually detected), mean time to investigate a case, escalation rate to law enforcement or regulators, and coverage across risk segments.

Equally important is tracking the cost per alert and the investigator-to-alert ratio over time. If a rule change increases alert volume by 40 percent but yields no additional true positives, it has made the program less efficient, not more effective. The feedback loop between investigation outcomes and model tuning is where real improvement happens.

Regulatory Compliance: Detection as a Legal Obligation

For many organizations, financial crime detection is not optional — it is a legal requirement. International standards set by the Financial Action Task Force (FATF) establish baseline expectations for anti-money laundering (AML) and counter-terrorism financing (CTF) programs, and local regulators translate these into binding obligations. In Israel, the Bank of Israel has issued detailed orders specifying identification, reporting, and record-keeping requirements for banking corporations, and the authority to impose financial sanctions for non-compliance is actively exercised.

Failure carries consequences beyond fines. Organizations that are found to have inadequate controls face reputational damage, loss of correspondent banking relationships, and in severe cases, criminal liability for officers and directors. Maintaining a clear audit trail — from initial alert through investigation to final disposition — is essential both for regulatory examination and for demonstrating good-faith effort.

Did You Know

Global AML fines exceeded $5 billion in recent years, with penalties increasingly targeting not only financial institutions but also non-financial corporations that failed to implement adequate controls. Regulatory enforcement has expanded to cover any entity that processes significant financial flows, regardless of industry classification.

How Detelix Addresses Real Operational Needs Across the Detection Lifecycle

| Operational Need | How Detelix Helps in Practice |

|---|---|

| Continuous ERP monitoring | Scans every transaction, master-data change, and approval action in real time, flagging deviations before funds leave the organization |

| Reducing manual review burden | Applies risk-based prioritization so investigation teams focus on high-impact alerts rather than processing noise |

| Detecting insider manipulation | Cross-checks relationships between employees, vendors, and bank accounts to surface conflicts of interest and unauthorized changes |

| Strengthening segregation of duties | Monitors actual behavior against policy — not just role assignments — to identify when controls are bypassed in practice |

| Supporting audit readiness | Maintains a documented trail of every alert, investigation step, and decision, ready for internal audit or regulatory review |

What distinguishes this approach is its focus on the ERP layer where business processes actually execute. Many detection tools operate at the banking or payment-gateway level; Detelix operates where procurement, payroll, inventory, and supplier management decisions are made — the exact point where corporate financial crime originates.

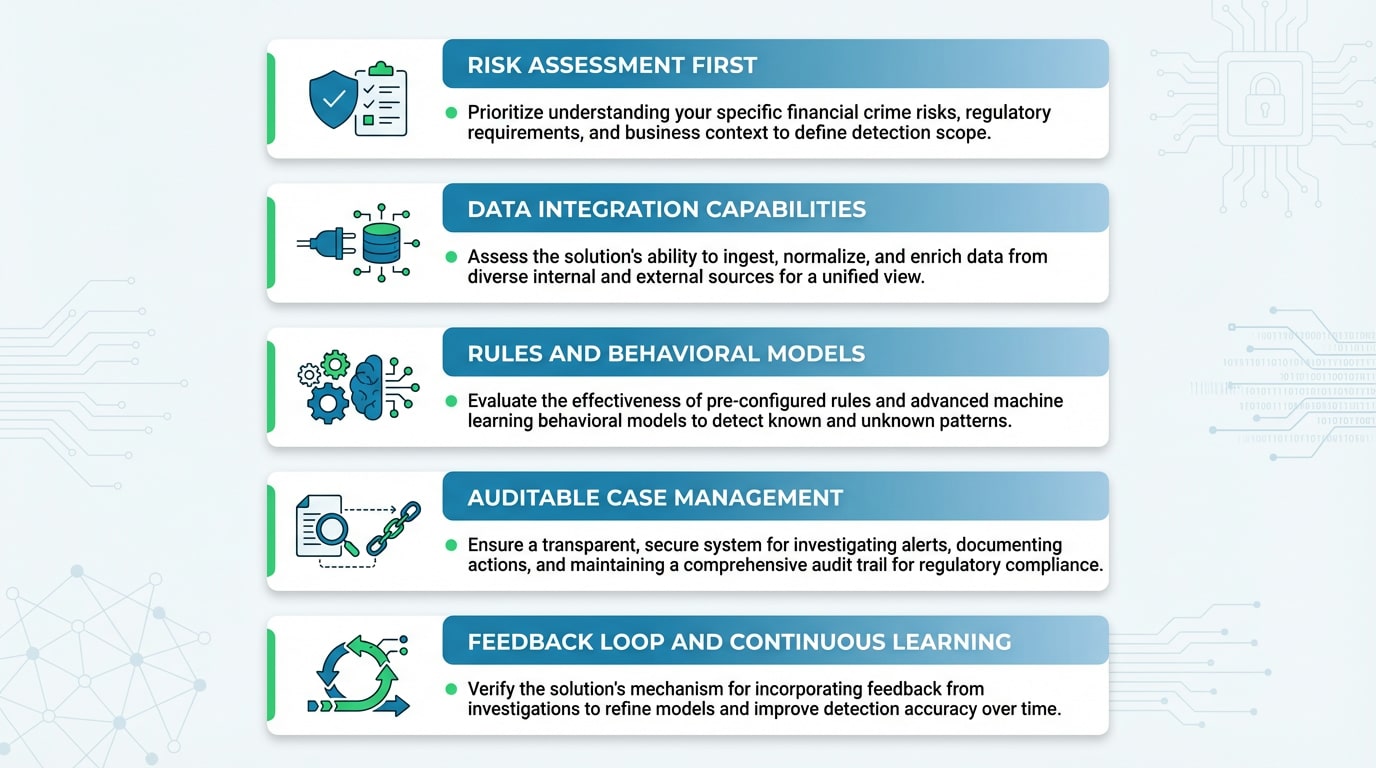

Choosing a Detection Solution: What Should You Prioritize?

Start with your risk assessment, not with a vendor shortlist. Identify which processes carry the highest exposure — supplier payments, customer refunds, bank account changes, payroll — and evaluate solutions based on their ability to monitor those specific workflows. A platform that excels at consumer-banking transaction monitoring may have no capability for ERP-level procurement oversight.

Evaluate data integration capabilities: Can the platform ingest data from your specific ERP environment without months of custom development? Assess the alerting logic: Does it support both rules and behavioral models? Review the case management workflow: Is investigation documented, auditable, and measurable? And critically, ask about the feedback loop: How does the system learn from investigation outcomes to improve future detection accuracy?

Tip

During vendor evaluation, request a proof-of-concept that uses your actual data — not a demo dataset. The most revealing test of any detection platform is how it handles the specific data quality challenges, naming conventions, and process flows unique to your environment.

Detelix Financial Crime Detection Solutions

Proactive Monitoring

Continuous, real-time surveillance of ERP transactions and master data changes to detect anomalies before they result in financial loss.

Real-Time Alerts

Intelligent alerting engine that prioritizes high-risk events and delivers actionable notifications to the right stakeholders instantly.

Gatekeeper

Automated enforcement of segregation-of-duties policies and approval workflows, blocking unauthorized actions at the point of execution.

Experience & Expertise

Decades of domain knowledge in corporate fraud prevention, compliance, and ERP security — delivering solutions grounded in operational reality.

See Detelix in Action

Frequently Asked Questions

What is the difference between financial crime detection and fraud detection?

Fraud detection is a subset of financial crime detection. Financial crime detection covers a broader spectrum including money laundering, sanctions evasion, terrorism financing, bribery, and corruption — in addition to fraud. The tools and processes overlap significantly, but the regulatory obligations and investigative pathways differ depending on the crime type.

Can small and mid-sized companies benefit from financial crime detection?

Yes. Smaller organizations often face proportionally higher risk because they lack the dedicated compliance teams that large institutions maintain. Automated detection platforms reduce the dependency on headcount by handling high-volume monitoring and screening tasks, making professional-grade detection accessible to organizations that cannot staff a full investigations unit.

How long does it take to implement a financial crime detection program?

Timelines vary widely based on data readiness, system complexity, and organizational scope. A focused deployment covering a single high-risk process — such as supplier payment monitoring within an existing ERP — can go live in weeks. Enterprise-wide programs that span multiple geographies and business units typically require several months of phased rollout.

What role does employee training play in detection?

Technology catches patterns; people catch context. Employees who understand red flags — unusual urgency, pressure to bypass approval chains, unexplained changes to payment details — serve as a critical first line of defense. Training should be practical, scenario-based, and refreshed regularly rather than delivered as an annual compliance checkbox.

Is real-time detection always better than batch processing?

For high-risk processes like payment execution and bank account changes, real-time detection is essential because it allows intervention before funds leave the organization. For lower-risk analytical tasks like periodic behavioral profiling or trend analysis, batch processing can be sufficient and more resource-efficient. Most mature programs use both approaches in combination.

Ready to Close the Gaps in Your Financial Controls?

Whether you need real-time ERP monitoring, smarter alerting, or a documented investigation workflow that withstands regulatory scrutiny — the right time to act is before the next incident, not after.