Stop Financial Fraud Before It Happens

Detelix provides continuous transaction monitoring that catches anomalies, policy violations, and suspicious patterns in real time. Talk to our experts today.

- What Exactly Is Continuous Transaction Monitoring?

- Why Periodic Reviews Leave Dangerous Blind Spots

- Real-Time Monitoring Compared with Batch Processing

- How Does the Monitoring Pipeline Actually Work?

- What Risks Does Continuous Monitoring Actually Catch?

- Scenario Design: Building Rules That Work Without Drowning in Noise

- The False-Positive Problem and How Leading Teams Solve It

- Should You Rely on Rules, Machine Learning, or Both?

- Measuring Success: Which KPIs Actually Matter?

- What Data Do You Actually Need to Get Started?

- Common Implementation Mistakes and How to Avoid Them

- Linking Alerts to Investigation: Why Case Management Matters

- From MVP to Maturity: A Realistic Implementation Timeline

- How Detelix Addresses Core Monitoring Needs

- Regulatory Expectations Are Tightening

- Frequently Asked Questions

In many organizations, financial controls look solid on paper. Approval workflows exist, ERP permissions are configured, reconciliation procedures run on schedule, and audit reports are filed on time. Yet when a single payment leaves the organization based on manipulated vendor data, or when a pattern of small, structured transfers quietly bypasses threshold-based alerts, it becomes painfully clear that routine oversight is not the same as real control. Continuous transaction monitoring addresses this gap by shifting from periodic, sample-based review to an always-on analytical process that examines every transaction as it occurs. For finance leaders, risk managers, and compliance officers, understanding how this capability works and how to implement it effectively has become a baseline expectation.

Key Takeaways

- Continuous transaction monitoring analyzes 100% of transactions in near real-time, replacing sample-based periodic audits that leave most activity unexamined.

- A hybrid approach combining real-time checks for high-risk scenarios with batch analysis for broader pattern detection delivers the strongest results.

- False-positive rates are the single greatest operational drag on monitoring programs; segmentation and structured feedback loops are the most effective countermeasures.

- A practical MVP covering the top 5-10 risk scenarios can be operational within four to eight weeks, with full maturity developing over 12-18 months.

- Regulatory expectations globally are tightening, making continuous monitoring not just a fraud-prevention measure but an operational requirement for compliance readiness.

What Exactly Is Continuous Transaction Monitoring?

Continuous transaction monitoring is the systematic, automated analysis of 100% of transaction data on an ongoing basis, designed to detect anomalies, policy violations, and suspicious patterns in near real-time. Unlike traditional audit-driven reviews that sample a fraction of activity weeks or months after the fact, a continuous approach ensures that every payment, transfer, refund, and adjustment passes through a set of predefined rules and behavioral models before or immediately after execution.

The concept is straightforward: if your organization processes thousands of transactions daily, relying on manual spot-checks or quarterly audits means most activity is never examined at all. A dedicated transaction monitoring system closes that gap by ingesting event data as it flows through the ERP or payment infrastructure, applying logic, and surfacing exceptions that require human review. When every action in the ERP system is overseen by a dedicated control layer, the window between a risk event and its detection shrinks from weeks to seconds.

Tip

Before evaluating monitoring tools, map every transaction type your organization processes (payments, refunds, adjustments, inter-company transfers) and rank them by risk. This prioritization ensures your monitoring rules target the highest-impact areas first.

Why Periodic Reviews Leave Dangerous Blind Spots

Organizations that rely solely on end-of-period reconciliations or annual audits face a fundamental timing problem. Fraud, errors, and policy deviations do not wait for the audit cycle. A supplier bank-account change that was socially engineered, a duplicate invoice processed by an overwhelmed accounts-payable clerk, or a series of just-below-threshold wire transfers all occur in real time. Discovering them thirty days later means the money is gone, the trail is cold, and recovery options are limited.

Regulatory bodies reinforce this point. The Basel Committee’s guidelines on sound management of ML/TF risks emphasize that ongoing monitoring should be risk-proportionate and continuous, not episodic. Similarly, the Bank of Israel’s supervisory policy documents stress the importance of effective, risk-based control frameworks that operate throughout the customer and transaction lifecycle. The message is consistent: waiting is a risk in itself.

Did You Know

According to the Association of Certified Fraud Examiners, the median duration of a fraud scheme before detection is 12 months. Organizations with proactive, continuous monitoring detect fraud approximately 50% faster than those relying on passive controls like tips and manual audits.

Real-Time Monitoring Compared with Batch Processing

One of the most common questions decision-makers ask is whether monitoring must happen in literal real-time or whether batch runs are sufficient. The answer depends on what is at stake. The European Banking Authority has clarified that not all transaction monitoring must be real-time, but that high-risk scenarios, particularly those involving instant payments, demand analysis before or at the moment of execution.

| Dimension | Real-Time Monitoring | Batch Monitoring |

|---|---|---|

| Latency | Milliseconds to seconds | Hours to days |

| Best suited for | Instant payments, high-risk scenarios, fraud prevention | Trend analysis, heavy aggregation, periodic reporting |

| Intervention window | Before or during transaction execution | After execution (post-event review) |

| Infrastructure complexity | Higher (streaming architecture required) | Lower (scheduled jobs on stored data) |

| False-positive management | Requires fast triage to avoid blocking legitimate activity | More time for contextual review |

In practice, most mature organizations use a hybrid approach: real-time checks for high-risk transaction types and near-real-time or batch analysis for broader pattern detection and reporting.

Tip

Start by classifying your transactions into risk tiers. Apply real-time monitoring to Tier 1 (high-value wire transfers, vendor master changes, payment redirections) and batch monitoring to Tier 2 and 3. This balances detection speed with infrastructure cost.

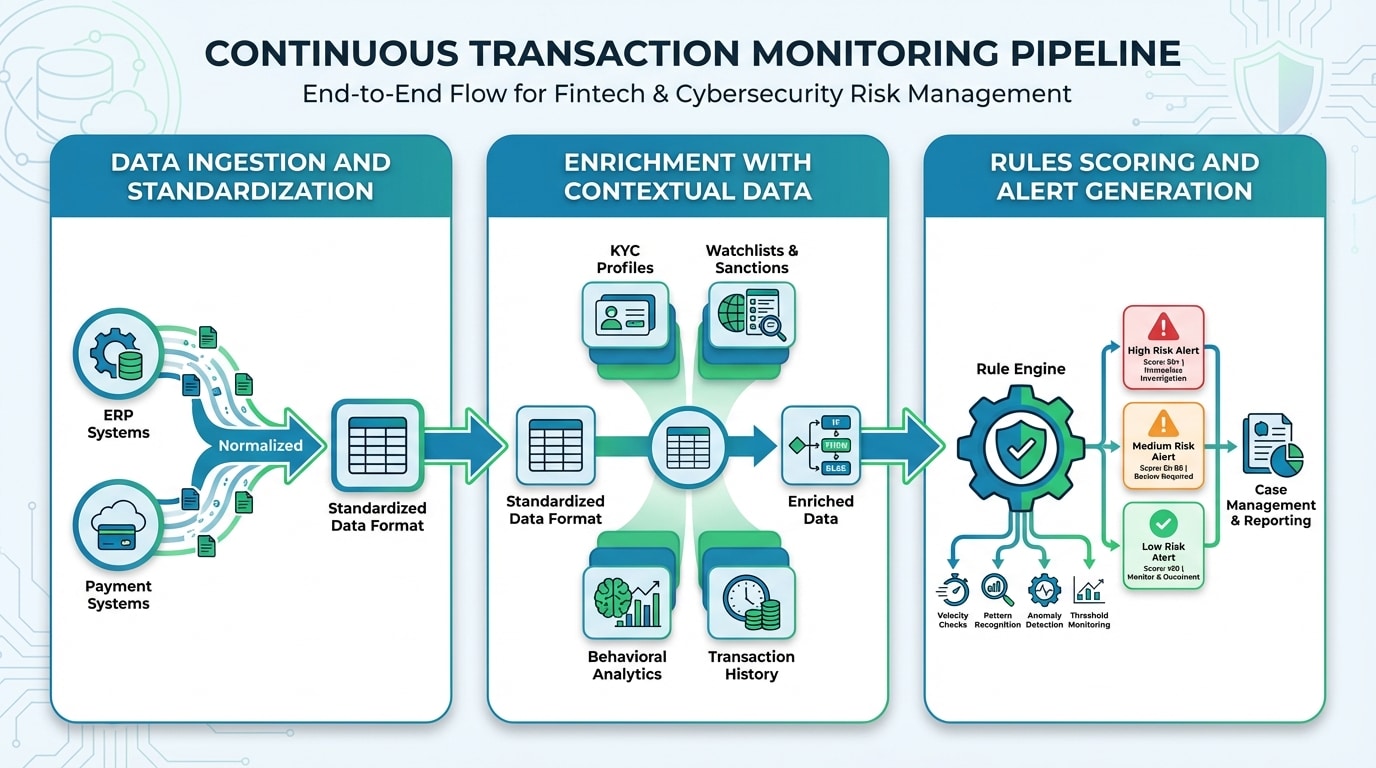

How Does the Monitoring Pipeline Actually Work?

Understanding the end-to-end flow helps demystify continuous transaction monitoring and reveals where value is created and where things can break.

Data Ingestion and Standardization

Every monitoring system starts with data. Transaction events are collected from ERP modules, payment gateways, core banking platforms, or other source systems. These events must be normalized into a consistent format so that downstream rules can operate reliably regardless of the originating system.

Enrichment with Contextual Data

Raw transaction data alone is rarely sufficient. Effective monitoring enriches each event with customer risk ratings, KYC profiles, geographic indicators, device information, historical behavior baselines, and external watchlists. The FATF’s guidance on digital identity highlights how robust identity and due-diligence data feeds directly into monitoring accuracy.

Rules, Scoring, and Alert Generation

The enriched event is then evaluated against a library of scenarios: threshold breaches, velocity checks, geographic anomalies, counterparty risk signals, and behavioral deviations. When conditions are met, the system generates an alert with a risk score and routes it to the appropriate queue for human review.

Did You Know

A single vendor bank-account change in an ERP system can trigger a fraudulent payment within hours. Continuous monitoring platforms that cross-check bank detail modifications against approval workflows and historical patterns can intercept these changes before any funds are disbursed.

What Risks Does Continuous Monitoring Actually Catch?

The scope extends well beyond anti-money-laundering. A well-configured system identifies operational errors such as duplicate payments or incorrect currency conversions, internal fraud indicators like fictitious vendors or ghost employees on payroll, policy violations such as unapproved payment channels, and external threats including business-email-compromise schemes that redirect legitimate payments. Organizations that treat monitoring as a multi-risk discipline covering compliance, fraud, and operational integrity simultaneously extract significantly more value from their investment.

Tip

When scoping your monitoring program, do not limit it to AML compliance. Build a unified rule library that covers fraud, operational errors, and policy violations. The incremental cost of adding non-compliance scenarios to an existing platform is minimal compared to running separate systems.

Scenario Design: Building Rules That Work Without Drowning in Noise

Defining effective monitoring scenarios is both an art and an engineering discipline. Start too broad and the team is buried in false positives; start too narrow and genuine risks slip through undetected.

Threshold-Based Rules vs. Behavioral Rules

Threshold rules flag transactions that exceed a fixed value, occur above a certain frequency, or involve sanctioned jurisdictions. Behavioral rules compare current activity against a customer’s or account’s historical baseline and flag statistically significant deviations. The strongest frameworks combine both: thresholds catch known typologies, while behavioral logic surfaces emerging patterns that no one has written a rule for yet.

A practical starting point is a core set of 15 to 25 scenarios covering the most common risk typologies for your business, calibrated against six to twelve months of historical data. From there, iterative tuning based on investigation outcomes steadily improves precision.

Did You Know

Organizations that calibrate their monitoring thresholds using at least 6 months of historical transaction data typically achieve a 30-40% reduction in false-positive rates compared to those that deploy default vendor settings without customization.

Your transaction data holds the answers. Let Detelix help you build a monitoring framework that catches real risks without burying your team in false alerts.

The False-Positive Problem and How Leading Teams Solve It

High false-positive rates are the single greatest operational drag on monitoring programs. When 90% or more of generated alerts turn out to be benign, investigator fatigue sets in, genuine risks get buried, and the organization is effectively paying for a system that creates work rather than insight. The root causes are predictable: overly generic rules, poor data quality, missing segmentation, and a lack of feedback loops between investigators and rule designers.

Segmentation is the most impactful lever. Instead of applying a single set of thresholds across all customers, leading organizations define segments by product type, geography, transaction volume, and risk rating, then set context-appropriate parameters for each segment. Pairing this with a structured feedback loop, where disposition data from closed cases is systematically fed back into rule calibration, creates a virtuous cycle of continuous improvement.

Tip

Establish a monthly calibration meeting between your investigation team and your rule designers. Review the top 10 most frequently triggered scenarios, examine the true-positive rate for each, and adjust thresholds or add segmentation criteria based on actual investigation outcomes.

Should You Rely on Rules, Machine Learning, or Both?

Rules provide transparency and regulatory defensibility: you can explain exactly why an alert fired. Machine learning excels at detecting complex, non-linear patterns and reducing noise by learning from historical outcomes. In most environments, a hybrid approach delivers the best results. Rules handle well-defined typologies and regulatory requirements; ML models sit on top to re-score alerts, surface anomalies that no rule anticipated, and prioritize the investigation queue.

The key governance requirement is explainability. Regulators expect organizations to articulate why a transaction was flagged or cleared. Any ML model used in production must therefore be accompanied by documentation of its training data, feature importance, validation results, and ongoing performance metrics.

Did You Know

The European Banking Authority requires that any automated decision-making system used in transaction monitoring be accompanied by documentation of its logic, validation methodology, and ongoing performance metrics. “Black box” models without explainability documentation are not considered compliant.

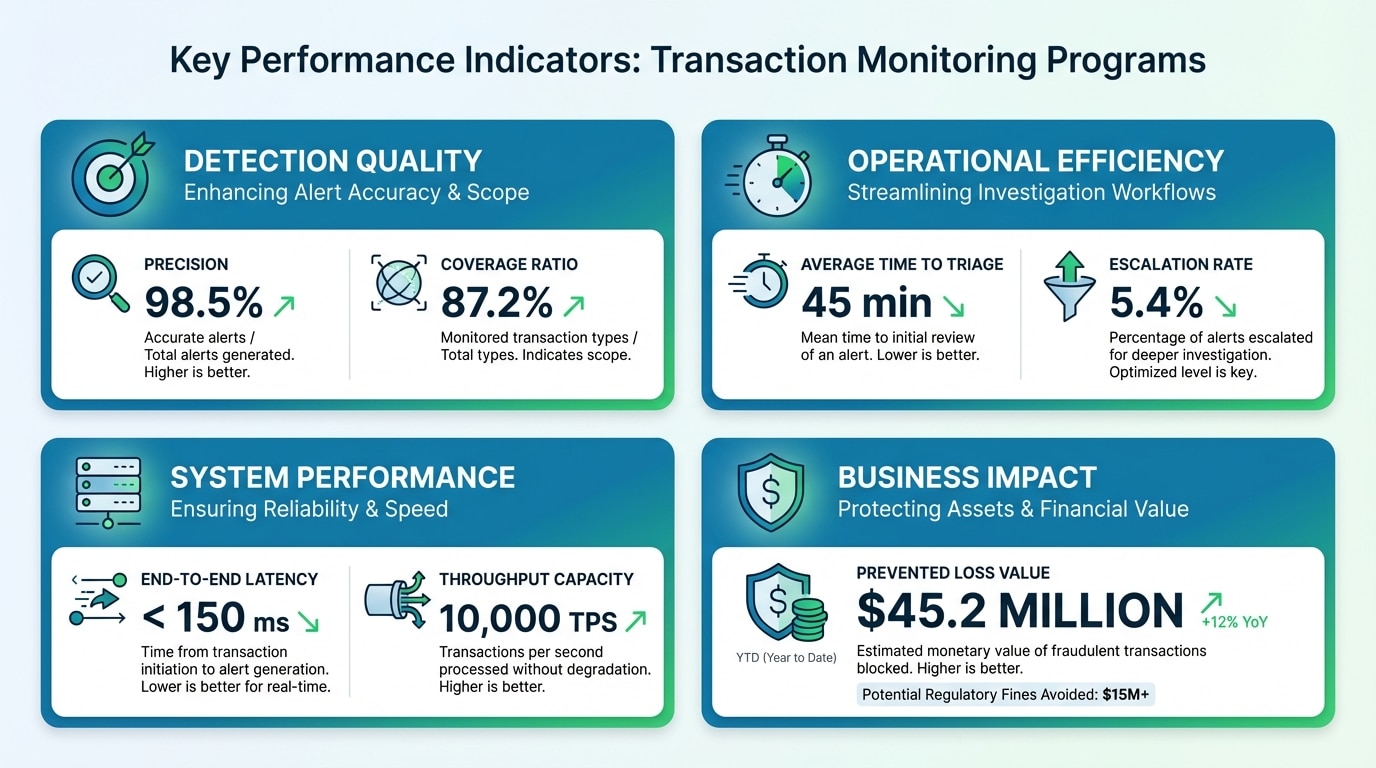

Measuring Success: Which KPIs Actually Matter?

| Category | Key Metric | What It Tells You |

|---|---|---|

| Detection quality | Precision (true-positive rate) | How many alerts represent genuine risk |

| Detection quality | Coverage ratio | Percentage of known risk typologies covered by active scenarios |

| Operational efficiency | Average time to triage | Speed from alert generation to initial review |

| Operational efficiency | Escalation rate | Proportion of alerts requiring full investigation or filing |

| System performance | End-to-end latency | Time from transaction event to alert availability |

| System performance | Throughput capacity | Transactions processed per second without degradation |

| Business impact | Prevented loss value | Monetary value of fraud or errors stopped before completion |

Tracking these metrics monthly and reviewing trends quarterly gives management a clear, evidence-based view of whether the monitoring program is improving or stagnating.

What Data Do You Actually Need to Get Started?

A common misconception is that continuous monitoring requires a massive data-engineering project before any value can be delivered. In reality, a practical MVP can be built on a focused data set: transaction records (amount, currency, date, time, originator, beneficiary, channel), basic customer or vendor profiles (risk rating, onboarding date, country), and account-level metadata. This core set is sufficient to activate threshold and velocity rules for the highest-risk scenarios.

Enrichment Data That Significantly Improves Accuracy

Once the baseline is running, adding device fingerprints, IP geolocation, historical behavioral profiles, external watchlist matches, and corporate-structure data can dramatically improve detection precision and reduce false positives. Each enrichment layer adds context that helps the system distinguish between a legitimate spike in activity and a genuinely suspicious pattern.

Tip

Do not wait for perfect data to start monitoring. Launch with your core transaction and vendor data, then systematically add enrichment layers (behavioral baselines, watchlist feeds, device data) in subsequent iterations. Each layer measurably improves detection accuracy.

Common Implementation Mistakes and How to Avoid Them

After observing dozens of monitoring programs across industries, a clear set of recurring pitfalls emerges. First, deploying rules without calibrating them against real data leads to immediate alert overload. Second, neglecting data quality, including missing fields, inconsistent formats, and stale risk ratings, undermines even the best rule logic. Third, treating the system as “set and forget” without a structured governance process for rule changes, model revalidation, and threshold adjustments causes performance to degrade over time. Fourth, failing to align compliance, risk, product, and technology teams around shared objectives creates organizational friction that slows response times and dilutes accountability.

The antidote is a cross-functional governance framework with clear ownership, regular calibration cycles, documented change-management procedures, and KPI-driven performance reviews. The Bank of Israel’s supervisory policy on AML/CFT explicitly calls for effectiveness-oriented controls and risk-based governance, principles that apply equally to any organization’s internal monitoring program.

Did You Know

A study by Deloitte found that organizations with dedicated cross-functional governance committees for their transaction monitoring programs achieved 2.5x higher true-positive rates and 40% faster alert resolution times compared to those where monitoring was managed by a single department.

Linking Alerts to Investigation: Why Case Management Matters

An alert without a clear path to investigation, decision, and documentation is just noise. Effective continuous monitoring systems integrate tightly with case-management workflows: when an alert is generated, it automatically creates an investigation record pre-populated with relevant transaction data, customer context, and prior alert history. Investigators follow a structured triage process, document their findings, record a disposition, and close the case, creating a full audit trail that satisfies both internal policy and external regulatory requirements.

This is an area where platforms like Detelix add tangible value. By continuously cross-checking actions inside the ERP environment and surfacing exceptions with full contextual data, the platform reduces the time investigators spend gathering evidence and increases the time they spend making decisions. The result is faster response, stronger documentation, and greater confidence that nothing material was missed.

Tip

Ensure your monitoring platform auto-populates investigation records with the full transaction chain, counterparty details, and historical alert context. Investigators who receive pre-assembled case files resolve alerts 60% faster than those who must manually pull data from multiple systems.

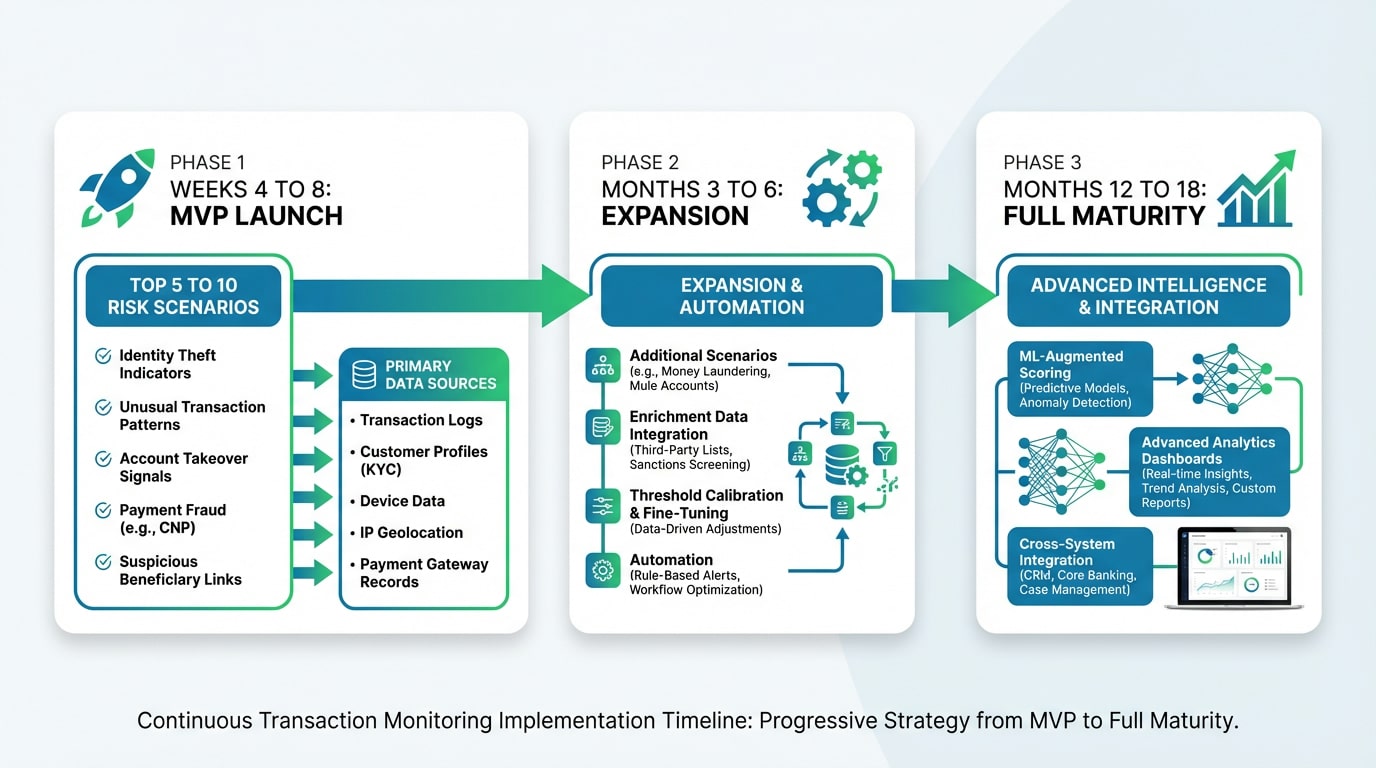

From MVP to Maturity: A Realistic Implementation Timeline

Organizations often delay implementation because they believe the project will take years. A phased approach changes that equation. In the first four to eight weeks, a focused MVP covers the top five to ten risk scenarios, connected to primary transaction data sources. Over the following three to six months, additional scenarios are activated, enrichment data is integrated, thresholds are calibrated based on live investigation feedback, and automation is introduced for low-risk alert disposition. Full maturity, including ML-augmented scoring, advanced analytics dashboards, and cross-system integration, typically develops over twelve to eighteen months of iterative improvement.

Detelix supports this phased model by offering pre-built control logic for sensitive ERP processes such as supplier payments, bank-account changes, and procurement flows. This means organizations do not need to design every rule from scratch; they start with proven scenarios and tailor them to their specific data and risk profile, significantly accelerating time to value.

How Detelix Addresses Core Monitoring Needs

| Business Need | How the Platform Helps |

|---|---|

| Detecting unauthorized vendor-master changes | Continuous cross-checking of bank-account modifications against approval workflows and historical patterns |

| Preventing duplicate or fraudulent payments | Real-time comparison of payment instructions against invoice records, prior payments, and vendor profiles |

| Maintaining segregation of duties | Automated flagging when a single user performs conflicting actions across the procure-to-pay cycle |

| Ensuring audit-ready documentation | Full event logs with timestamps, user identifiers, and decision records for every flagged transaction |

| Reducing manual review burden | Risk-scored alerts with contextual data so investigators focus on genuine exceptions, not routine activity |

Regulatory Expectations Are Tightening

Global regulatory trends leave little room for ambiguity. The FATF’s updated Recommendation 16 on payment transparency expands information requirements across the payment chain. The EU’s Delegated Regulation 2018/389 mandates transaction monitoring mechanisms for payment service providers, specifying minimum risk factors that must be considered. In Israel, the Bank of Israel’s draft update to Directive 411 reinforces ongoing AML/CFT risk-management obligations, including documentation and record-keeping requirements that directly depend on robust monitoring infrastructure.

Organizations that invest in continuous monitoring now are not just preventing losses; they are building the operational foundation that regulators increasingly expect to see during examinations. Those that delay face both financial exposure and the reputational cost of enforcement actions, as evidenced by the Bank of Israel’s published sanctions decisions against banking corporations for AML/CFT violations.

Did You Know

The Bank of Israel has publicly sanctioned multiple banking corporations for deficiencies in their AML/CFT monitoring programs. Published enforcement actions specifically cite inadequate ongoing transaction monitoring, insufficient documentation, and failure to maintain risk-proportionate controls as primary violations.

Detelix Continuous Monitoring Solutions

Proactive Monitoring

Continuous oversight of ERP transactions with automated detection of anomalies, policy violations, and suspicious patterns before they cause damage.

Real-Time Alerts

Instant notifications when critical thresholds are breached, enabling rapid response to high-risk transactions and unauthorized changes.

GateKeeper

Pre-transaction validation that blocks fraudulent payments and unauthorized vendor changes before funds leave your organization.

Experience & Expertise

Decades of domain knowledge in financial controls, fraud prevention, and regulatory compliance built into every monitoring scenario.

See Detelix in Action

Frequently Asked Questions

Who needs continuous transaction monitoring — only banks?

No. While banking regulators were early drivers of the requirement, any organization that processes significant transaction volumes faces similar risks: payment fraud, vendor manipulation, duplicate payments, and internal policy violations. Enterprises, fintech companies, insurance firms, and large retailers all benefit from continuous oversight of their financial processes.

Can monitoring happen both before and after a transaction is executed?

Yes. Pre-transaction monitoring evaluates a payment instruction before funds leave the organization, enabling blocking or hold actions. Post-transaction monitoring analyzes completed activity to detect patterns that only become visible over time. The most effective programs use both approaches in combination, calibrated by risk level.

How do you balance detection sensitivity with operational workload?

Through segmentation, risk-based thresholds, and continuous calibration. Instead of applying uniform rules to all activity, organizations define distinct parameters for different customer or transaction segments. Investigation outcomes are fed back into the rule engine to adjust sensitivity, ensuring that detection remains sharp without overwhelming the review team.

Does continuous monitoring replace internal audit?

It complements rather than replaces audit. Internal audit provides independent, periodic assurance over the design and operating effectiveness of controls, including the monitoring system itself. Continuous monitoring provides day-to-day detection and prevention. Together, they form a more complete control framework than either could achieve alone.

What happens when the system generates an alert — who is responsible?

Alert ownership depends on organizational design, but best practice assigns initial triage to a dedicated operations or compliance team, with escalation paths to senior risk officers or legal counsel for complex cases. Clear SLAs, role definitions, and documented procedures ensure accountability and prevent alerts from languishing unresolved.

Ready for Always-On Financial Control?

If your oversight model still depends on periodic reviews and manual spot-checks, the gap between what you think is happening and what is actually happening may be wider than you realize. Let Detelix show you what real-time transaction visibility looks like.