Stop Vendor Fraud Before It Drains Your Bottom Line

Real-time ERP monitoring, automated controls, and expert-driven fraud prevention — tailored for finance teams that demand actual protection.

- Most Common Vendor Fraud Schemes in Modern Business

- How to Identify Vendor Fraud Red Flags Before the Payment Run

- Why Vendor Bank Account Change Fraud Is the Biggest Threat

- Vendor Master File Governance: The Foundation of Prevention

- How 3-Way Matching Acts as a Primary Defense

- Segregation of Duties in the Payment Chain

- Preventing Kickbacks and Internal Collusion

- Key Features of Effective Vendor Fraud Prevention Software

- Building an Incident Response Process

- Measuring Success: KPIs Without Alert Fatigue

- Frequently Asked Questions

Every organization that pays vendors operates within a landscape of financial risk. Approval workflows exist, ERP permissions are configured, and reconciliation reports are generated on schedule. Yet vendor fraud continues to grow in both sophistication and frequency. The reason is straightforward: most control environments are designed around routine, and fraud thrives in the gap between what a procedure covers on paper and what actually happens in real time. Vendor fraud prevention is not a single policy or a software checkbox — it is a strategic framework that embeds verification, segregation, and continuous monitoring into the procure-to-pay cycle so that losses are stopped before money leaves the organization. When manual checks can no longer keep pace with the volume and complexity of modern transactions, an efficient protection system becomes essential for any finance team that wants to move from the illusion of control to actual control.

Key Takeaways

- Vendor fraud exploits trust, routine, and gaps in data verification — not necessarily weak technology.

- Bank account change fraud (BEC-driven payment diversion) is the single most damaging and irreversible vendor fraud vector today.

- A clean, well-governed Vendor Master File is the foundation upon which every other prevention control depends.

- Three-way matching, segregation of duties, and continuous ERP monitoring form the core defense triad against invoice and payment fraud.

- Effective prevention software must operate in real time — catching anomalies before payment release, not weeks later in an audit report.

- Measuring KPIs like true positive rate and mean time to resolve alerts prevents alert fatigue and keeps the prevention program actionable.

What Are the Most Common Vendor Fraud Schemes in Modern Business?

Understanding how vendor fraud works is the first step toward preventing it. The attack vectors are diverse, but they share a common trait: they exploit trust, routine, and gaps in data verification. Below are the schemes finance leaders encounter most frequently.

Invoice fraud involves receiving bills for goods or services that were never delivered, or for quantities that exceed what was actually received. In some cases, the invoice is entirely fictitious — issued by a shell entity with no real operations. The phenomenon of fictitious invoices has been documented extensively by Israel’s State Comptroller, highlighting the massive financial damage and the systemic challenges of detection at scale.

Did You Know

According to the Association of Certified Fraud Examiners, billing schemes — including fictitious invoices and inflated charges — account for roughly 22% of all occupational fraud cases, with a median loss of $100,000 per incident.

Price inflation is subtler. A legitimate vendor gradually increases unit prices, adds undisclosed surcharges, or bills for premium service tiers that were never agreed upon. Without a disciplined match between the purchase order and the invoice, these overcharges accumulate unnoticed over months or years.

Fictitious vendors represent one of the most damaging schemes. An employee — or an external attacker — creates a vendor record in the ERP for a company that does not exist, then submits invoices and approves payments to that entity. Because the vendor master file is the source of truth for payment routing, a single fraudulent record can open a channel for repeated theft.

Tip

Run a quarterly cross-reference of all vendor bank account numbers against employee bank account numbers in your payroll system. A match between a vendor’s receiving account and an employee’s personal account is one of the strongest indicators of a fictitious vendor scheme.

How to Identify Vendor Fraud Red Flags Before the Payment Run

Detection begins with knowing what to look for. Red flags are not proof of fraud, but they are signals that warrant investigation before a payment is released. The most reliable indicators fall into two categories: data anomalies and behavioral patterns.

Data anomalies include sequential invoice numbers from the same vendor over long periods, rounded-dollar amounts that appear too “clean,” mismatches between the vendor’s registered address and its tax identification, and bank account details that match those of another vendor or an employee. When a vendor’s mailing address is identical to an employee’s home address, the risk of a fictitious vendor scheme rises sharply.

Behavioral patterns are equally telling. A request for immediate payment outside of standard net-terms, especially when accompanied by language such as “urgent” or “confidential,” is a classic pressure tactic. Vendors that resist providing supporting documentation, or that submit invoices only to a specific person rather than through a centralized AP channel, deserve additional scrutiny. The combination of two or more red flags on a single transaction should trigger a hold before the payment run proceeds.

Did You Know

Fraudulent invoices frequently use round-number amounts just below organizational approval thresholds. If your approval limit is $10,000, a spike in invoices at $9,900 or $9,950 from the same vendor category is a statistically meaningful red flag worth investigating.

Why Is Vendor Bank Account Change Fraud the Biggest Threat Today?

Of all vendor fraud scenarios, payment diversion through a fraudulent bank account change causes the most immediate and irreversible damage. Once funds are transferred to the wrong account, recovery is rarely possible. The attack typically begins with a Business Email Compromise (BEC): a hacker gains access to a vendor’s email account — or creates a convincing lookalike domain — and sends a message to the Accounts Payable team requesting an update to the vendor’s IBAN or ACH routing number.

The email often looks legitimate. It may come from an address the AP clerk has corresponded with before, reference a real invoice number, and include a PDF on the vendor’s letterhead. The Bank of Israel has issued public warnings about this exact pattern, noting that impersonation via email, SMS, and phone calls is a growing threat to financial operations. What makes this scheme particularly dangerous is that the ERP record is updated “legitimately” by an authorized user who believes the request is genuine. There is no system error to catch — only a process failure.

Understanding the hidden risks of verifying a supplier’s bank account is critical because even well-intentioned manual phone calls can be circumvented by sophisticated attackers who provide a callback number controlled by the fraudster rather than the real vendor.

Tip

Never use contact details provided within a bank account change request to verify that request. Always call the vendor using a phone number already stored in your ERP system or sourced from the original signed contract. This single discipline blocks the majority of BEC-driven payment diversion attempts.

A Recommended Six-Step Verification Process

Effective prevention requires a structured workflow: (1) receive the change request and log it as a high-risk event, (2) verify the request by calling the vendor at a phone number already stored in the ERP — never at a number provided in the new email, (3) cross-check the new bank details against known databases and existing vendor records, (4) require dual approval from two separate individuals before the change is saved, (5) document every step with timestamps and approver identities, and (6) monitor the first payment to the new account with an additional review before release.

Common Mistakes That Enable Payment Diversion

The most frequent errors include replying directly to the sender’s email without verifying the “reply-to” address, accepting a new phone number provided within the change request itself, and rushing the update due to an approaching payment deadline. Each of these mistakes removes a layer of protection and gives the attacker a clear path to the organization’s funds.

Did You Know

The FBI’s Internet Crime Complaint Center reported that Business Email Compromise schemes caused over $2.9 billion in reported losses in a single year. The majority of those losses involved fraudulent payment instructions sent via compromised or spoofed vendor email accounts.

Vendor Master File Governance: The Foundation of Prevention

The Vendor Master File (VMF) is the single source of truth for every supplier relationship. It stores the vendor’s legal name, tax ID, address, bank account, contact details, payment terms, and status. When VMF governance is weak, the door is open for fictitious vendors, duplicate records, and unauthorized changes that redirect payments.

Strong governance starts with defined data ownership: a specific role or team is responsible for creating, modifying, and deactivating vendor records. Access is restricted by role, and every change triggers an audit log entry. Periodic reviews — quarterly at minimum — identify inactive vendors that should be archived, duplicate records that share the same bank account or address, and missing fields that undermine downstream controls.

Digitizing the vendor onboarding process further reduces risk. As demonstrated by automated supplier registration portals, moving from manual data entry to structured digital workflows cuts keying errors, enforces mandatory fields, and creates a transparent record of who submitted what and when.

Tip

Set your ERP to require a secondary approval for any vendor record where the bank account, tax ID, or payment terms are modified. This single configuration change adds a human checkpoint at the exact moment when fraud risk is highest — the point of data change.

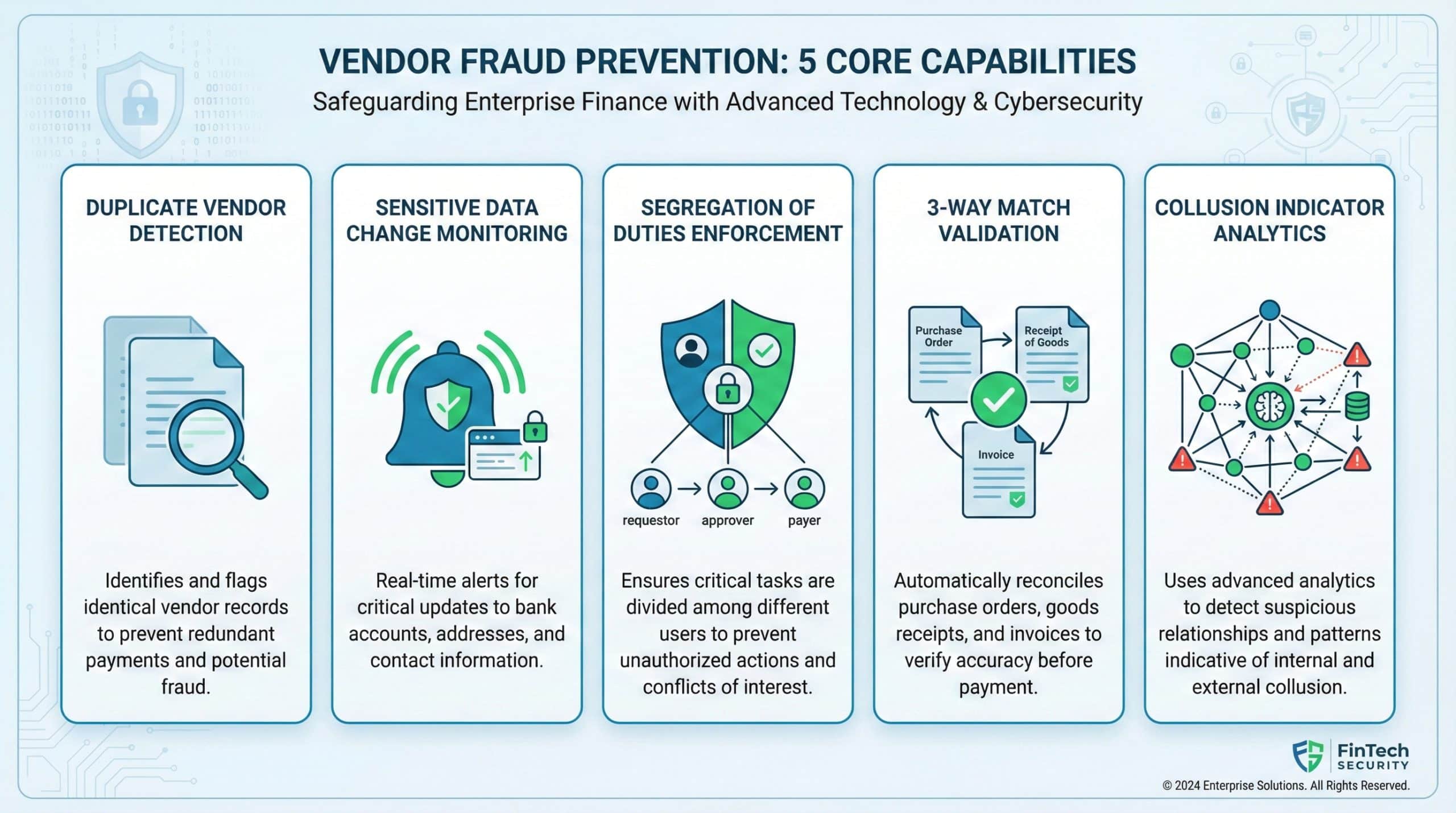

How Does 3-Way Matching Act as a Primary Defense?

Three-way matching is one of the oldest and most effective controls in Accounts Payable. The logic is simple: before a payment is approved, the system compares the Purchase Order (what was ordered), the Goods Receipt Note (what was received), and the Invoice (what the vendor is charging). If all three align within defined tolerances, the invoice is cleared. If they do not, the invoice is held for review.

This control prevents payment for shipments that never arrived, catches price discrepancies before they become losses, and makes it far harder to slip a fictitious invoice through the system. However, in high-volume environments, manual 3-way matching becomes a bottleneck. Vendor fraud detection software automates this comparison across thousands of transactions, flagging exceptions instantly.

| Matching Type | What Is Compared | When It Is Sufficient | Key Risk If Used Alone |

|---|---|---|---|

| 2-Way Match | PO and Invoice | Low-value, non-inventory purchases | No verification that goods or services were actually received |

| 3-Way Match | PO, GRN, and Invoice | Standard procurement of goods and materials | Tolerance thresholds set too high can allow inflated charges |

| 4-Way Match | PO, GRN, Invoice, and Inspection Report | High-value or regulated items requiring quality checks | Adds processing time; requires disciplined inspection logging |

Setting deviation tolerances is a balancing act. Too tight, and the AP team drowns in false exceptions. Too loose, and real fraud slips through. A risk-based approach assigns tighter thresholds to high-value or high-risk vendor categories and wider tolerances to low-risk, recurring purchases.

Your ERP holds the data — Detelix turns it into real-time fraud prevention. See how continuous monitoring closes the gaps that manual controls miss.

Segregation of Duties: Why One Person Should Never Control the Entire Payment Chain

Most successful vendor fraud schemes share a structural enabler: insufficient segregation of duties. When the same individual can create a vendor, approve an invoice, and release a payment, the organization has effectively removed every internal checkpoint. The “Model of Three” is the minimum standard: one person onboards and maintains vendor records, a second verifies and approves invoices, and a third authorizes the payment release.

This principle extends beyond AP. Corporate governance frameworks for preventing embezzlement and internal fraud consistently emphasize that role-based access controls, periodic permission reviews, and mandatory rotation of sensitive duties are foundational requirements — not optional enhancements. Detelix supports this by continuously monitoring ERP user permissions and alerting when a single user accumulates conflicting roles that violate segregation policies.

Did You Know

Organizations with strong segregation of duties controls experience fraud losses that are, on average, 50% lower than those without such controls. The key is not just defining the policy — it is continuously monitoring that ERP permissions actually enforce it.

How Can Organizations Prevent Kickbacks and Internal Collusion?

Kickbacks occur when an employee receives a personal benefit — cash, gifts, travel, or future employment — in exchange for steering contracts or payments to a specific vendor. Unlike external fraud, collusion involves a trusted insider who deliberately bypasses controls. This makes it harder to detect through standard approval workflows alone.

Analytical Tests That Reveal Collusion Patterns

Three data-driven checks are particularly effective. Spend concentration analysis identifies vendors receiving a disproportionate share of spend within a category without competitive bidding. Price variance tracking flags consistent above-market pricing from a specific vendor compared to peers. Split order detection catches instances where purchase orders are deliberately kept below an approval threshold to avoid review. These analytics can run continuously inside an ERP environment, turning raw transaction data into actionable risk signals.

Tip

Configure your fraud prevention system to flag any purchasing pattern where more than 70% of spend in a single procurement category flows to one vendor without a documented competitive bidding process. This threshold catches the majority of spend concentration anomalies before they become entrenched.

Conflict of Interest Policies and Declarations

A written policy is necessary but not sufficient. Employees involved in procurement and payment processes should sign annual conflict-of-interest declarations. Official vendor registration guidelines in Israel already incorporate explicit conflict-of-interest prohibitions for suppliers and their employees, demonstrating that this practice is both legally supported and operationally practical. The policy should define clear thresholds for gifts and hospitality, require disclosure of any personal relationship with a vendor, and establish consequences for non-compliance.

What Are the Key Features of Effective Vendor Fraud Prevention Software?

Technology does not replace good processes — it enforces them at scale. Effective vendor fraud prevention software must deliver three capabilities: anomaly detection, real-time alerting, and deep ERP integration.

| Business Need | How a Real-Time Control Platform Addresses It |

|---|---|

| Detecting duplicate vendors or invoices | Automated cross-referencing of names, tax IDs, bank accounts, and addresses across the entire vendor master file |

| Monitoring sensitive data changes | Instant alerts when bank details, payment terms, or contact information are modified, with full audit trail |

| Enforcing segregation of duties | Continuous scanning of user permissions to flag conflicting roles before a violation leads to a payment |

| Validating 3-way match compliance | Automated comparison of PO, GRN, and invoice data with configurable tolerance thresholds |

| Identifying collusion indicators | Spend concentration, split order, and price variance analytics across vendor and buyer dimensions |

Detelix operates as a continuous control layer that sits directly on top of ERP systems such as SAP and Priority. Rather than generating retrospective reports, it cross-checks every action in real time — so that exceptions are reviewed before they become losses. This shifts the finance team’s posture from reactive investigation to proactive prevention.

Before any vendor enters the system, a structured verification process is essential. Following a checklist of 5 Essential Checks Before Adding a Supplier ensures that the ERP environment remains clean from the start and reduces the workload of downstream detection controls.

Did You Know

Organizations that implement real-time transaction monitoring detect fraud an average of 58% faster than those relying solely on periodic audits. Faster detection directly correlates with smaller financial losses, as fraudulent payment channels are shut down before they can be exploited repeatedly.

How to Build an Incident Response Process When Vendor Fraud Is Suspected

Even the strongest prevention framework cannot guarantee zero incidents. What separates well-prepared organizations from vulnerable ones is the speed and discipline of their response. When a suspicious transaction or vendor record is identified, the first action is to place an immediate hold on all pending payments to that vendor. No funds should leave the organization until the investigation is complete.

The response team should include finance, information security, and legal. Key steps include reviewing all recent VMF changes for the vendor in question, examining email correspondence for signs of BEC, cross-referencing the vendor’s bank details against other records in the system, and checking whether similar invoices have been submitted to other entities within the organization. Every action taken during the investigation must be documented with timestamps and responsible parties. Once the incident is resolved, a post-mortem review should identify the specific control gap that was exploited and implement corrective measures — whether a policy update, an additional system rule, or a change in access permissions.

Tip

Maintain a pre-approved incident response checklist that AP staff can activate immediately upon suspicion — without waiting for management authorization. The first 24 hours after detection are critical. A payment hold costs nothing; a released fraudulent payment may be unrecoverable.

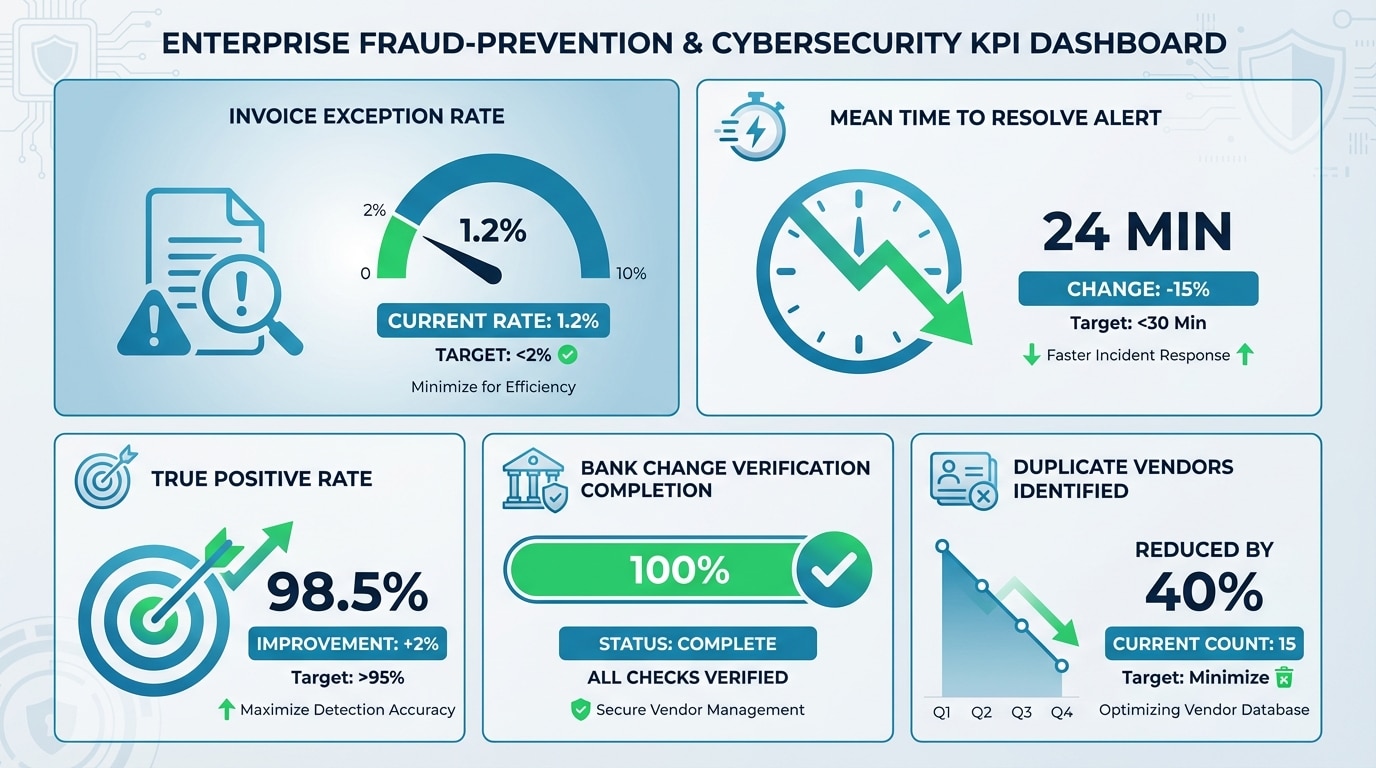

Measuring Success: KPIs for Vendor Fraud Prevention Without Alert Fatigue

A prevention program that generates thousands of unactionable alerts is worse than no program at all — it creates a false sense of security while burying real signals in noise. Effective measurement balances prevention metrics with operational efficiency indicators.

| KPI | What It Measures | Target Direction |

|---|---|---|

| Invoice exception rate | Percentage of invoices held for mismatch or anomaly | Stable or declining (indicates cleaner vendor data) |

| Mean time to resolve alert | Average hours from alert to closure | Declining (indicates efficient triage) |

| True positive rate | Percentage of alerts that led to a confirmed issue | Rising (indicates better-tuned rules) |

| Bank change verification completion | Percentage of bank account changes that completed the full verification process | 100% |

| Duplicate vendors identified and merged | Count of duplicate records found during periodic reviews | Declining over time |

Risk-based thresholds are essential. High-value vendors and sensitive change types (bank account, payment terms) should trigger alerts at lower deviation levels, while low-risk, recurring transactions can tolerate wider bands. Detelix allows finance teams to configure these thresholds by vendor category, transaction type, and risk score — so the system surfaces what matters most without overwhelming the team with false positives.

Did You Know

Finance teams that tune their alert thresholds quarterly — rather than setting them once and forgetting — achieve true positive rates 3 to 4 times higher than those using static rules. Continuous calibration is what separates a useful monitoring system from an ignored one.

Detelix Fraud Prevention Solutions

Proactive Monitoring

Continuous surveillance of ERP transactions and vendor data changes to detect anomalies before they result in financial loss.

Real-Time Alerts

Instant notifications for high-risk events including bank account changes, segregation violations, and suspicious invoice patterns.

GateKeeper

Automated pre-payment validation that blocks suspicious transactions from proceeding until verified by authorized personnel.

Experience & Expertise

Decades of domain knowledge in ERP security, internal controls, and fraud prevention across industries and regulatory environments.

See Detelix in Action

Frequently Asked Questions

What is the difference between vendor fraud prevention and vendor fraud detection?

Prevention focuses on stopping fraudulent transactions before payment is made — through controls like segregation of duties, 3-way matching, and verified vendor onboarding. Detection identifies anomalies after activity has occurred, using analytics and pattern recognition. The strongest programs combine both: prevention reduces the attack surface, while detection catches what slips through.

How often should the Vendor Master File be reviewed and cleaned?

At a minimum, a full VMF review should be conducted quarterly. This includes deactivating vendors with no transactions in the past 12 months, merging duplicates, verifying tax IDs, and confirming that bank account details are current and legitimate. Organizations with high vendor turnover or large supplier bases may benefit from monthly targeted reviews of high-risk categories.

Can small and mid-sized businesses afford vendor fraud prevention controls?

Yes. Many of the most effective controls — segregation of duties, documented approval workflows, periodic VMF reviews, and conflict-of-interest policies — require process discipline rather than large technology investments. Automated tools further reduce the cost by replacing manual checks with continuous, rule-based monitoring that scales without adding headcount.

What should I do if I suspect a vendor’s bank account change request is fraudulent?

Do not process the change. Place a hold on any pending payments to that vendor. Contact the vendor using a phone number already on file in your system — not a number provided in the suspicious communication. Involve your information security team to check for email compromise. Document every step and escalate according to your incident response procedure.

How does real-time monitoring differ from periodic auditing?

Periodic auditing reviews transactions after the fact, often weeks or months later. Real-time monitoring evaluates every transaction, data change, and user action as it happens, generating alerts that allow intervention before funds are released. The practical difference is the ability to prevent a loss rather than merely quantify it after it has occurred.

Ready to Close the Gaps in Your Vendor Payment Controls?

If your current defenses rely on manual reviews and periodic audits, your organization may be more exposed than you realize. Discover how real-time ERP monitoring stops vendor fraud before the money leaves.