Stop BEC Attacks Before They Reach Your Payment System

Detelix provides real-time fraud prevention that monitors every sensitive financial transaction — so attackers never get the chance to redirect your funds.

- Why Are Finance and AP Teams the High-Value Targets?

- How a Typical Payment Instruction Change Fraud Unfolds

- Email Spoofing vs. Account Takeover in BEC

- Red Flags Every AP Team Member Should Recognize

- Why a Phone Call Alone Is Not Enough

- Building a Verification Process That Works

- Segregation of Duties and Dual Approval

- How SPF, DKIM, and DMARC Mitigate Email Spoofing

- Defending Against Lookalike Domains

- Common Email Authentication Deployment Mistakes

- Training Finance Teams Without Overwhelming Staff

- Immediate Response to a Suspected Fraudulent Payment

- Measuring Whether Your BEC Defenses Work

- Can Automation Replace Manual Verification?

- Frequently Asked Questions

In many organizations, financial controls appear robust on paper. Approval workflows exist, ERP permissions are configured, and reconciliation procedures are documented. Yet Business Email Compromise — commonly known as BEC — continues to redirect millions of dollars from legitimate businesses into fraudulent accounts every year. The reason is deceptively simple: attackers do not hack systems; they hack trust. They exploit routine communication between Finance teams, Accounts Payable clerks, and vendors to insert a single, devastating instruction — “please update our bank details.” This guide breaks down how BEC attacks target payment workflows, what makes AP teams uniquely vulnerable, and how to build layered defenses that combine technical email controls, process-level safeguards, and continuous transaction monitoring.

Key Takeaways

- BEC attackers exploit trust and routine — not system vulnerabilities — making Accounts Payable teams the primary target for payment redirection fraud.

- Verifying bank detail changes requires out-of-band confirmation through pre-established contact information, never through details provided in the suspicious request itself.

- Email authentication protocols (SPF, DKIM, DMARC) protect against domain spoofing but cannot prevent lookalike domain attacks or compromised vendor accounts — process controls must fill the gap.

- Segregation of duties, dual approval workflows, and immutable audit logs are essential to ensuring no single point of failure exists in the payment chain.

- Continuous, real-time monitoring of vendor master data changes and payment instructions — such as what Detelix provides — shifts defense from reactive investigation to proactive prevention.

Why Are Finance and Accounts Payable Teams the “High-Value” Targets for BEC Attacks?

Business Email Compromise is a social engineering attack in which a threat actor impersonates a trusted party — a vendor, a CEO, a lawyer — to trick someone with payment authority into transferring funds or changing payment details. The FBI’s Internet Crime Complaint Center (IC3) identified the “supplier swindle” as one of the most damaging BEC variants, contributing to billions of dollars in reported losses.

Accounts Payable sits at the intersection of cash outflows, vendor master data, and time-sensitive obligations. AP teams process hundreds or thousands of invoices, often under deadline pressure. They routinely receive bank detail updates, corrected invoices, and urgent payment requests — all via email. This makes AP the ideal entry point for attackers who understand that a single accepted “update” can reroute an entire payment run to a fraudulent account.

Did You Know

According to the FBI’s IC3, BEC losses exceeded $2.9 billion in reported complaints in a single year, making it one of the costliest forms of cybercrime — far surpassing ransomware in total financial damage.

How Does a Typical “Payment Instruction Change” Fraud Scenario Unfold?

The attack follows a predictable lifecycle. First, the attacker researches the target organization: who are the key vendors, who handles payments, when invoices are due, and what language the company uses. Then, the attacker initiates contact — either by spoofing a vendor’s email address or by compromising a real vendor mailbox — and sends what appears to be a routine request to change banking information.

The Spoofed Invoice and the Sense of Urgency

The request typically arrives with a “corrected” invoice, a formal-looking letterhead, and language designed to create pressure. Phrases like “our bank is undergoing an audit,” “effective immediately,” or “please process before end of day” are common. The attacker may also include instructions such as “do not call the old number — use this one instead,” effectively cutting the AP team off from genuine verification channels.

Tip

Any request that asks you to avoid contacting the vendor through your usual channels is a strong indicator of fraud. Legitimate vendors have no reason to block you from using the phone number or email address already in your records.

In more sophisticated variants, the attacker inserts themselves into an existing email thread — continuing a real conversation about a real invoice — and quietly changes only the banking details. The result is a payment that leaves the organization to an account controlled by the attacker, often in a different country, where recovery becomes extremely difficult.

What Is the Difference Between Email Spoofing and Account Takeover in a BEC Context?

These two attack methods look similar to the recipient but differ fundamentally in how they are executed and how detectable they are. Spoofing involves manipulating the “From” header of an email so that it appears to come from a legitimate domain. The attacker never actually accesses the real mailbox. As described in NIST Technical Note 1945 on email authentication mechanisms, protocols like SPF, DKIM, and DMARC exist specifically to detect and block this kind of forgery.

Account Takeover, on the other hand, means the attacker has gained actual access to a vendor’s or employee’s email account — usually through stolen credentials or phishing. From inside the real mailbox, the attacker can read previous correspondence, reply to active threads, match the sender’s writing style, and even set up forwarding rules to intercept replies. This makes ATO significantly harder to detect through technical controls alone, and it is precisely why process-level controls in Finance are so critical.

Did You Know

Account Takeover attacks are often undetected for weeks because the attacker operates from the legitimate mailbox. They frequently create inbox rules that auto-delete security alerts and redirect replies, making it invisible to the real account owner.

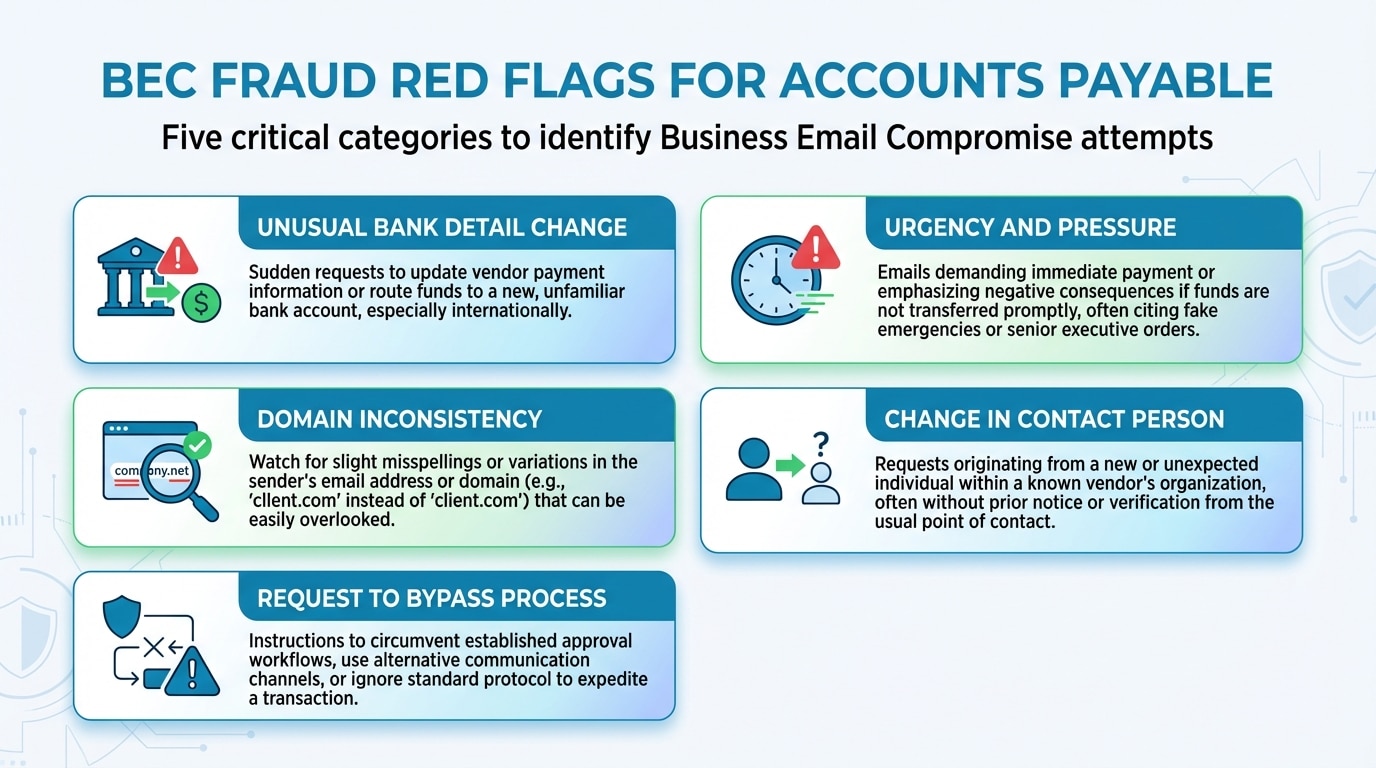

Red Flags That Every AP Team Member Should Recognize

Not every fraudulent email is perfectly crafted. There are patterns that, when recognized, can stop a payment before it leaves. The challenge is making sure these signals are part of the team’s daily workflow rather than relying on memory alone.

| Red Flag Category | What to Watch For | Recommended Action |

|---|---|---|

| Unusual bank detail change | Request to update IBAN, ABA, or account number — especially to a different country or bank | Pause processing; initiate out-of-band verification using contact details on file |

| Urgency and pressure | “Must be processed today,” “confidential — do not discuss with others” | Treat urgency as a warning sign, not a reason to skip controls |

| Domain inconsistency | Slight misspelling in sender domain (e.g., suppIier vs. supplier) | Inspect the full email address carefully; report to IT security |

| Change in contact person | “Your usual contact is unavailable — please work with me instead” | Verify independently through the vendor’s known main line |

| Request to bypass process | “Skip the usual approval — the CFO already approved this verbally” | Never bypass documented approval procedures without written, verified authorization |

Tip

Print a condensed version of this red flag table and keep it at every AP workstation. When recognition cues are physically visible, staff are far more likely to pause and verify before processing a suspicious request.

Why a Phone Call Alone Is Not Enough to Prevent BEC Fraud

Many organizations rely on a simple rule: “call the vendor to confirm.” While this is better than no verification at all, it is far from foolproof. As J.P. Morgan’s analysis of callback failures demonstrates, the most common mistake is calling the phone number provided in the suspicious email or the new invoice. The attacker controls that number. The employee believes they have verified the request, when in reality they have spoken to the fraudster.

A second failure mode occurs when the vendor’s own contact person has been compromised. If the attacker has access to the vendor’s mailbox, they may also have access to the vendor’s voicemail or mobile phone. This is why verification must be “out-of-band” — meaning through a completely separate channel and using contact information that was established and verified before the suspicious request arrived.

Did You Know

In several documented BEC cases, attackers set up professional-sounding call centers specifically to handle verification callbacks. The AP clerk called the number on the fraudulent invoice, spoke with a “representative,” and received convincing confirmation — all from the attacker’s team.

Building a Payment Instruction Verification Process That Actually Works

The most effective verification processes share three characteristics: they do not rely on information provided in the request itself, they require more than one person to complete, and they are documented. Here is a practical framework that balances security with operational speed.

The “Out-of-Band” Verification Rule

Every request to change payment details — whether it involves a new bank account, a new beneficiary name, or even a new mailing address — must be confirmed through a phone call to a number already stored in the ERP system or the approved vendor file. If no number is on file, the request is escalated to a manager before any change is made. This single rule, consistently enforced, eliminates the majority of BEC payment fraud attempts.

Tip

Build the verification step directly into your ERP workflow as a mandatory checkbox. The system should not allow a vendor bank detail change to be saved without a documented confirmation reference — who was called, when, and what was verified.

For high-value payments or first-time payments to a new account, consider adding a second verification layer: a confirmation through the vendor’s official portal, a signed letter on file, or a test deposit to validate account ownership. Every verification step — who called, who answered, what was confirmed, and the date — must be recorded in the ERP or a controlled log.

Your AP team processes hundreds of payments. How many vendor bank changes went through without proper verification last month? Detelix monitors every sensitive transaction in real time.

Implementing Segregation of Duties and Dual Approval in the AP Workflow

The principle is straightforward: the person who updates vendor bank details in the ERP should never be the same person who approves or releases the payment. This “Four Eyes” approach ensures that a single compromised or negligent employee cannot independently redirect funds. The GAO Standards for Internal Control identify segregation of duties as a foundational control that separates authorization, custody, and recording functions.

In small teams where one person may wear multiple hats, compensating controls become essential. These include mandatory manager approval for any vendor master data change, weekly or daily review of all changes to bank details, immutable audit logs that cannot be edited or deleted, and periodic surprise reconciliations. The goal is not to create bureaucracy but to ensure that no single point of failure exists in the payment chain.

| Business Need | How Detelix Supports It in Practice |

|---|---|

| Real-time detection of vendor master data changes | Continuously monitors ERP transactions and flags unauthorized or unusual modifications to supplier bank details before payments are released |

| Segregation of Duties enforcement | Cross-checks user roles and actions across the payment workflow, alerting when the same individual initiates and approves a sensitive change |

| Audit-ready documentation | Maintains a complete, tamper-resistant log of every alert, action, and resolution — ready for internal or external audit review |

| Reducing dependence on manual checks | Automates cross-referencing of payment instructions against historical vendor data, reducing the risk of human error without slowing down the AP cycle |

Tip

When reviewing your segregation of duties matrix, pay special attention to “emergency access” or “firefighter” accounts in the ERP. These accounts often bypass normal approval chains and represent a high-risk vector if misused or compromised.

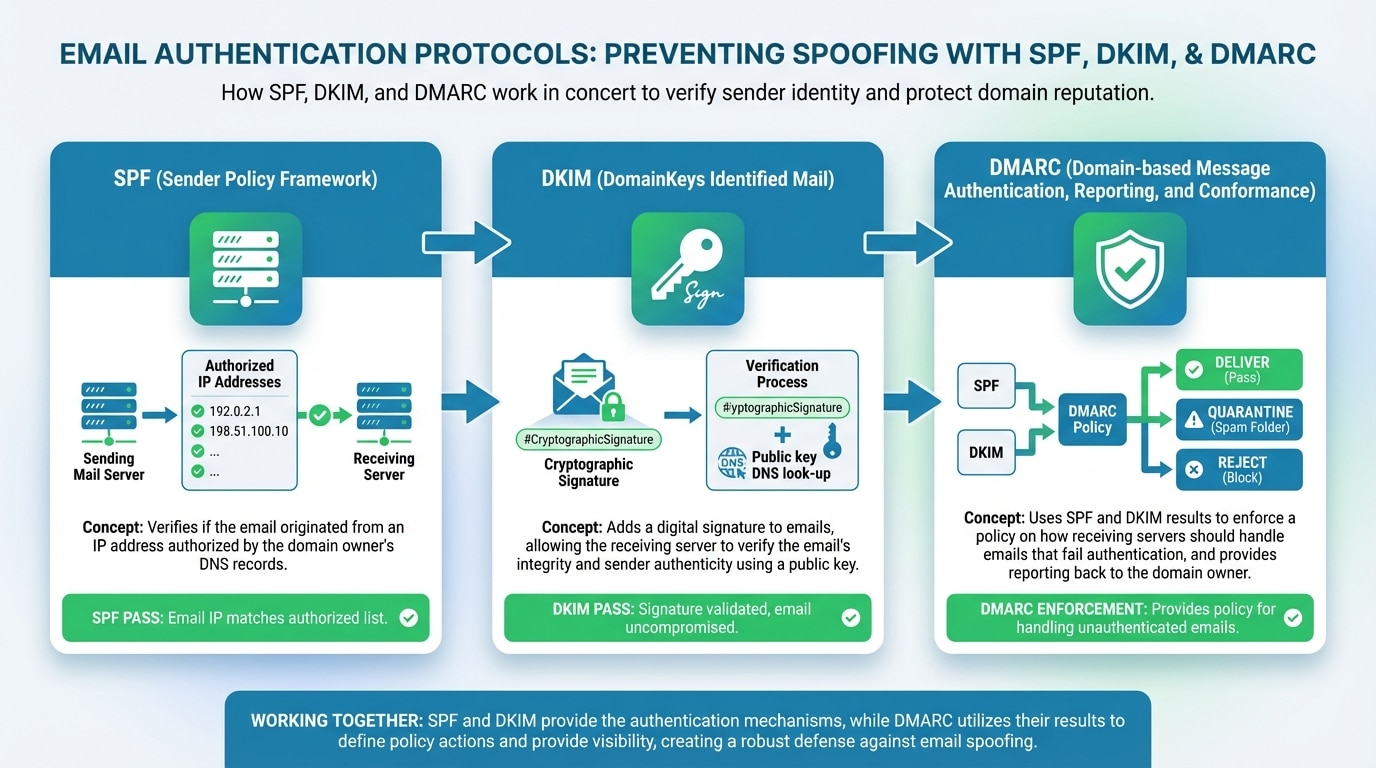

How Do SPF, DKIM, and DMARC Mitigate Email Spoofing Risks?

These three protocols form the technical backbone of email authentication. SPF (Sender Policy Framework) publishes a list of IP addresses authorized to send email on behalf of a domain. DKIM (DomainKeys Identified Mail) attaches a cryptographic signature to outgoing messages, allowing the receiver to verify that the content has not been altered in transit. DMARC (Domain-based Message Authentication, Reporting, and Conformance) ties SPF and DKIM together and instructs receiving mail servers on what to do when authentication fails — monitor, quarantine, or reject.

As outlined in CISA’s Binding Operational Directive 18-01, a DMARC policy set to “reject” provides the strongest protection because it tells receiving servers to discard unauthenticated messages entirely. However, many organizations deploy DMARC in “none” (monitoring) mode and never progress to enforcement, leaving a significant gap. Finance leaders should actively verify with their IT teams that the organization’s DMARC policy has reached “reject” status and that third-party senders (marketing platforms, CRM tools) are properly authorized.

Did You Know

A study of Fortune 500 companies found that fewer than one-third had a DMARC policy set to “reject.” The majority remained at “none” or “quarantine,” meaning spoofed emails using their domain could still reach recipients at other organizations.

Defending Against Lookalike Domains and Vendor Impersonation

Even with perfect DMARC enforcement on your own domain, attackers can register a near-identical domain — substituting a lowercase “L” for an uppercase “I,” adding a hyphen, or appending a country code — and send emails that pass all authentication checks because they are legitimately sent from the attacker’s own domain. This technique, known as typo-squatting or domain impersonation, bypasses sender-side controls entirely.

Mitigation requires a combination of technical and procedural measures. On the technical side, organizations can register common misspellings of their own domain and deploy email gateway rules that flag messages from domains that closely resemble known vendors. On the procedural side, the defense is the same: never trust the contact information in the email itself. Verify through established channels. Detelix adds a continuous monitoring layer here — by scanning vendor-related transactions and flagging anomalies such as a payment instruction change arriving shortly after a new contact email was registered, it helps teams catch impersonation attempts that slip past email filters.

Tip

Register the five to ten most likely misspellings and character substitutions of your company domain. It costs very little annually to hold these domains defensively, and it prevents attackers from using them to impersonate your organization to your own vendors and partners.

What Mistakes Do Organizations Make When Deploying Email Authentication?

The most common error is treating SPF, DKIM, and DMARC as a “set it and forget it” task. DNS records become outdated when third-party services change IP addresses. New marketing tools or CRM platforms are added without updating SPF records, causing legitimate emails to fail authentication. DMARC reports — which provide visibility into who is sending email on behalf of the domain — are often ignored entirely.

A second mistake is assuming that email authentication protects against all impersonation. It does not. SPF/DKIM/DMARC protect your domain from being spoofed. They do nothing to prevent an attacker from sending mail from a lookalike domain or from a compromised vendor account. This is why email controls must be paired with strong process controls in Finance — the two layers complement each other, and neither is sufficient alone.

Did You Know

Organizations that add new SaaS tools without updating their SPF records often exceed the DNS lookup limit of 10, which causes SPF validation to fail entirely — effectively disabling their own email authentication for all outbound messages.

How Should Finance Teams Train Without Overwhelming Staff?

Annual awareness training sessions rarely change behavior. What works is role-specific micro-learning — short, focused exercises designed for AP staff — combined with operational checklists that are embedded into the daily workflow. Instead of asking an AP clerk to remember twenty types of fraud, give them a five-item checklist that they complete before processing any payment with changed details: verify the request source, confirm via number on file, check the domain spelling, document the verification, and obtain dual approval.

Tip

Replace annual hour-long training sessions with monthly 10-minute micro-modules focused on a single BEC scenario. Follow each module with a brief quiz. Short, frequent reinforcement produces measurably better retention than infrequent, lengthy sessions.

Periodic simulations — sending realistic but harmless “test” BEC emails to the AP team — provide measurable data on how the team responds without relying on self-reported confidence. Organizations that combine brief quarterly simulations with clear, accessible escalation procedures see measurably stronger detection rates than those relying on lengthy annual workshops.

What Should the Finance Team Do Immediately If a Fraudulent Payment Is Suspected?

Minutes matter. According to FinCEN Advisory FIN-2016-A003, the likelihood of recovering fraudulently transferred funds drops sharply after the first 24 hours. The Finance team’s immediate response should follow a structured “Golden Hour” sequence.

First, contact the originating bank and request an urgent recall or hold on the wire transfer. Provide the transaction reference, amount, date, and beneficiary details. Second, notify IT security to preserve the email thread, headers, and any attachments as forensic evidence — do not delete or forward them. Third, report the incident to law enforcement, including filing a complaint with IC3 or the relevant national authority. Fourth, freeze any additional pending payments to the same vendor until the investigation is complete. Fifth, document every action taken, by whom, and at what time. This documentation is essential for insurance claims, law enforcement cooperation, and internal audit review.

Did You Know

FinCEN’s rapid response mechanism — the Financial Fraud Kill Chain — has successfully frozen and recovered funds in numerous BEC cases, but only when the victim organization reported the fraud within 24 to 48 hours of the wire transfer. After that window, international fund recovery rates drop below 30%.

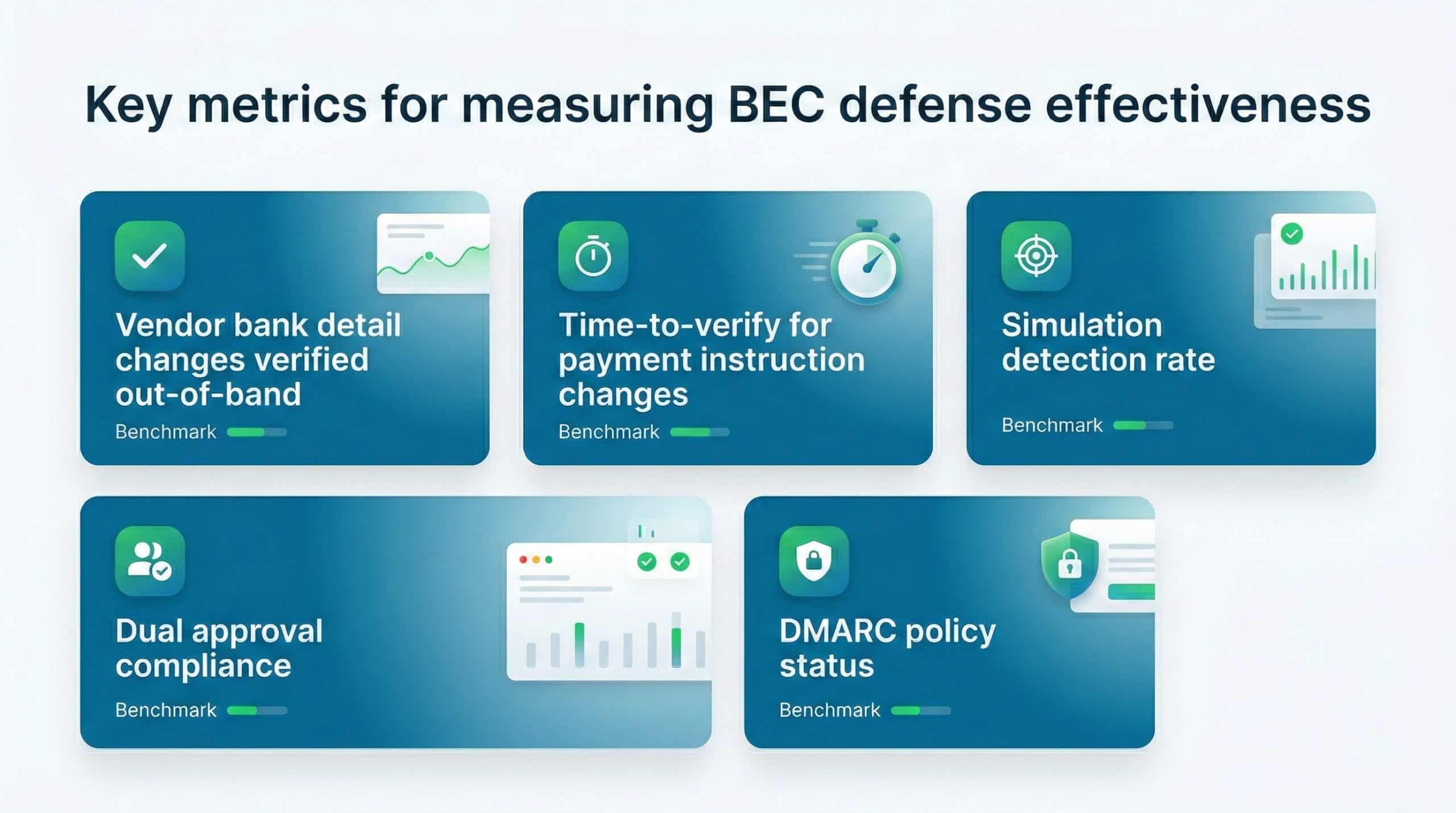

Measuring Whether Your BEC Defenses Actually Work

Controls that are not measured tend to decay. Finance leaders should track a small set of meaningful indicators to evaluate the effectiveness of their BEC prevention program over time.

| Metric | What It Measures | Target Benchmark |

|---|---|---|

| Vendor bank detail changes verified out-of-band | Compliance with callback policy | 100% of changes verified before processing |

| Time-to-verify for payment instruction changes | Operational efficiency of the verification process | Under 48 hours for standard changes |

| Simulation detection rate | Staff ability to identify test BEC emails | Above 80% across the AP team |

| Dual approval compliance | Adherence to segregation of duties policy | Zero payments released with single approval above the defined threshold |

| DMARC policy status | Email authentication enforcement level | “Reject” policy active on all organizational domains |

Detelix supports this measurement process by providing real-time dashboards that track vendor data changes, approval chain compliance, and exception patterns across ERP-driven payment workflows. Rather than compiling reports after the fact, finance leaders gain continuous visibility into whether their controls are functioning as designed — or whether gaps are emerging that require attention.

Can Automation Replace Manual Verification for BEC Defense?

Automation does not eliminate the need for human judgment, but it dramatically reduces the attack surface by catching anomalies that manual review misses. When a vendor’s bank details are changed in the ERP, an automated control layer can instantly compare the new details against historical records, flag mismatches, verify whether the change followed the required approval path, and alert the right people before a payment is released.

This is where platforms like Detelix provide a distinct operational advantage. Instead of relying on periodic audits or sample-based reviews, Detelix acts as a continuous organizational gatekeeper — scanning every sensitive transaction in real time and cross-checking it against established patterns, policies, and approval requirements. The result is not just faster detection but the ability to prevent damage before funds leave the organization. For Finance teams managing high transaction volumes, this shift from reactive investigation to proactive prevention represents a fundamental improvement in control quality.

Tip

When evaluating automated fraud prevention tools, ask vendors specifically how they handle the gap between email authentication and ERP-level controls. The most effective solutions monitor both layers — flagging suspicious emails and monitoring the downstream transaction changes those emails are designed to trigger.

Detelix Fraud Prevention Solutions

Proactive Monitoring

Continuous surveillance of ERP transactions and vendor master data changes to detect unauthorized modifications before payments are released.

Real-Time Alerts

Instant notifications when anomalies are detected in payment workflows, enabling immediate intervention before funds leave the organization.

GateKeeper

Automated cross-checking of vendor bank details, approval chains, and segregation of duties policies across every sensitive financial transaction.

Industry Experience

Deep expertise in financial process controls, ERP security, and fraud prevention across healthcare, finance, and enterprise sectors.

See Detelix in Action

Frequently Asked Questions

Is BEC only a risk for large enterprises?

No. Small and mid-sized organizations are frequently targeted precisely because they tend to have fewer formal controls, smaller AP teams with less segregation of duties, and less investment in email security infrastructure. The same attack techniques that target multinational corporations are used against businesses of every size.

How often should vendor bank details be reviewed for accuracy?

At minimum, every vendor master data record should be reviewed annually. However, any change to bank details should trigger an immediate out-of-band verification regardless of the review cycle. Organizations with high vendor turnover or frequent international payments should consider quarterly reviews of their active vendor file.

What is the difference between dual approval and segregation of duties?

Dual approval means that two separate individuals must authorize a transaction before it is processed. Segregation of duties is broader: it ensures that different people handle different stages of a process — for example, one person creates a vendor record, another verifies the bank details, and a third approves the payment. Dual approval is one component of a well-designed SoD framework.

Does implementing DMARC at “reject” level risk blocking legitimate emails?

It can, if the transition is not managed carefully. Organizations should begin with a DMARC policy of “none” to collect reporting data, then move to “quarantine,” and finally to “reject” once they have confirmed that all legitimate sending sources are properly authorized in SPF and DKIM records. Rushing to “reject” without this validation phase can disrupt legitimate business communications.

How does Detelix differ from a standard ERP audit log?

An ERP audit log records what happened after the fact. Detelix monitors what is happening in real time and applies cross-checks, policy rules, and anomaly detection to flag risks before a transaction is completed. It transforms passive record-keeping into active, continuous control — giving finance leaders the ability to intervene before damage occurs rather than investigating after the money has left.

Ready to Close the Gaps in Your Payment Security?

Are your current controls strong enough to stop a well-crafted BEC attack before it reaches your payment system? Find out how Detelix delivers real-time, continuous protection over every sensitive financial process.