Automate Financial Controls Across Your Shared Services Center

Stop relying on sampling and manual reviews. Detelix embeds real-time, rule-based controls into every transaction — so exceptions surface before they become losses.

- Why Finance Shared Services Control Automation Is No Longer an IT Luxury

- What Separates Shared Services Finance Controls from GBS Governance

- A Scenario: When a Missing Quality Gate Costs More Than You Expect

- How Automation Improves Both Speed and Compliance Simultaneously

- Enhancing Transactional Finance Quality through Leading Indicators

- Implementing Continuous Risk Monitoring in the SSC

- How Automated Controls Enforce Segregation of Duties in Practice

- Building a Controls Library That Scales across Entities and Processes

- Which AP Processes Are the Best Candidates for Automated Controls

- Where AR and Collections Benefit Most from Control Automation

- How Control Automation Shortens Month-End Close Without Increasing Risk

- Exception Handling: The Process That Makes or Breaks Scalability

- Which KPIs Prove That Automated Controls Are Actually Working

- What Does a GBS Governance Model Look Like When It Sustains Controls

- Creating an Automated Audit Trail That Satisfies Auditors

- Common Mistakes When Automating Controls and How to Avoid Them

- How Long Does Implementation Take and What Drives the Cost

- Moving from Detective Controls to Predictive Governance

- Matching Business Needs to Platform Capabilities

- Frequently Asked Questions

In many finance shared services centers, controls exist on paper — approval matrices, reconciliation schedules, segregation of duties policies, and periodic audit reviews. Yet when transaction volumes scale across multiple entities and geographies, the gap between documented controls and actual operational protection widens. A single duplicate payment that slips through a manual review can cascade across business units, distorting cash positions and eroding stakeholder confidence. Finance shared services control automation addresses this gap by embedding continuous, rule-based checks directly into transactional workflows — so that exceptions surface in real time, not weeks later in an audit finding.

Key Takeaways

- Full-population transaction scanning replaces statistical sampling, closing the coverage gap that grows with volume.

- Automated controls enforce segregation of duties, duplicate detection, and approval thresholds in real time — before payments execute.

- Leading indicators measured during processing replace lagging indicators discovered at month-end, compressing close cycles and reducing audit surprises.

- A structured controls library with defined ownership, SLAs, and evidence trails prevents the silent degradation of controls over time.

- Predictive governance layers historical exception patterns and behavioral baselines onto rule-based checks, transforming controls from a cost center into operational intelligence.

Why Finance Shared Services Control Automation Is No Longer an IT Luxury

The traditional model of internal controls inside a shared services center relied on sampling. A team would review a percentage of invoices, a subset of journal entries, or a monthly reconciliation output. When the center processed a few thousand transactions, that approach provided reasonable coverage. Today, many SSCs handle hundreds of thousands of transactions monthly across dozens of legal entities. The math is straightforward: if the error rate stays constant, the absolute number of undetected exceptions grows in direct proportion to volume.

Tip

Calculate your current control coverage ratio by dividing the number of transactions reviewed by the total processed each month. If coverage falls below 100%, every unreviewed transaction represents unmanaged risk — and the gap widens every time volume increases.

This is the “Volume vs. Risk” paradox. A duplicate payment worth a few hundred dollars matters little in isolation, but when it repeats undetected across entities, the cumulative financial impact becomes material. Automation of controls shifts coverage from statistical sampling to full-population scanning. Every invoice, every payment instruction, every vendor master change is tested against predefined rules — without requiring additional headcount. Regulatory frameworks for operational risk management, such as the Bank of Israel Directive 350 on operational risk, explicitly call for a strong control environment that includes continuous monitoring mechanisms and clear reporting lines. The same principle applies to any organization operating at scale: when volume increases, manual vigilance alone is no longer sufficient.

What Separates Shared Services Finance Controls from GBS Governance

Many organizations conflate “controls” with “governance,” yet the distinction is critical. Shared services finance controls are the tactical checks executed at the transaction level — a three-way match between purchase order, goods receipt, and invoice; an approval threshold enforced before payment release; or a duplicate-detection algorithm that flags matching amounts and vendor references. These controls answer the question: Is this specific transaction correct?

Did You Know

Organizations that formally separate control execution from control governance report 40% fewer instances of controls degrading silently after initial deployment, according to shared services maturity benchmarks. The distinction between “who runs the check” and “who ensures the check still works” is the single largest predictor of long-term control sustainability.

Global business services governance, by contrast, answers a broader set of questions: Who owns each control? How do we measure whether controls are effective? How do we decide when to add, modify, or retire a control? Who resolves disputes between the SSC and local finance teams? Governance operates through RACI matrices, steering committees, service-level agreements, and policy-exception frameworks. Without governance, even well-designed controls degrade over time as processes change, personnel rotate, and business requirements evolve. Organizations that invest in effective protection against embezzlement and fraud errors recognize that sustainable control depends on both layers working together — tactical enforcement backed by strategic oversight.

A Scenario: When a Missing Quality Gate Costs More Than You Expect

Consider a mid-size multinational with a finance shared services center in Eastern Europe processing accounts payable for twelve entities. The team follows a standard approval matrix, but there is no automated check for vendor bank-account changes. An employee in one subsidiary updates a vendor’s bank details based on a spoofed email. The payment runs on schedule. No alert fires. Four weeks later, during month-end reconciliation, the finance team discovers the funds went to a fraudulent account. The loss is compounded by the delayed detection: recovery options are limited, and the audit trail — consisting of a single email approval — offers little forensic value.

Tip

Map every vendor master data change to a mandatory secondary confirmation step — ideally via a channel independent of email. Phone callbacks to a verified number or an automated confirmation request through a dedicated portal reduce the attack surface for business email compromise schemes targeting bank-account modifications.

This scenario illustrates why quality gates must be embedded before the payment execution step, not after. An automated control that cross-references vendor bank-account changes against an independent confirmation workflow would have flagged the modification in real time, before funds left the organization.

How Automation Improves Both Speed and Compliance Simultaneously

A common concern among SSC leaders is that adding more controls will slow down processing and jeopardize service-level agreements. In practice, well-designed automation achieves the opposite. Instead of requiring a human reviewer to inspect every transaction, the system applies rules at machine speed and routes only genuine exceptions to qualified staff. The result is faster straight-through processing for clean transactions and focused attention on the items that actually carry risk.

Did You Know

Shared services centers that implement full-population automated controls typically see straight-through processing rates increase by 25-35%, because staff time previously consumed by manual sampling is redirected entirely to genuine exception resolution — the transactions that actually require human judgment.

This shift from “check everything manually” to “manage by exception” also strengthens compliance. Every automated check generates a timestamped evidence record: which rule was applied, what data was evaluated, what the outcome was, and who handled the exception. State audit reports examining computerized payment controls have emphasized the need for rigorous exception reports and management information to identify failure points in payment processes. Automation delivers exactly this capability — structured, repeatable, and auditable.

Enhancing Transactional Finance Quality through Leading Indicators

Transactional finance quality is typically measured after the fact: error rates found during reconciliation, journal entries reversed during close, or audit adjustments. These are lagging indicators. By the time they surface, the damage — whether financial, operational, or reputational — has already occurred.

Leading indicators flip the perspective. They measure control effectiveness during processing, not after it. Examples include the percentage of invoices that pass three-way match on first attempt, the number of vendor master changes reviewed within the defined SLA, and the ratio of exceptions resolved before the close cutoff. When these indicators trend in the wrong direction, management can intervene before the problem reaches the financial statements.

Where to Place Quality Gates Without Creating Bottlenecks

The most effective quality gates sit at natural decision points in the process: before a payment batch is released, before a credit note exceeds a defined threshold, and before a new vendor is activated. Placing them here ensures that clean transactions flow without delay while risky ones are intercepted. The key is calibrating thresholds carefully — too tight, and the team drowns in false positives; too loose, and genuine risks pass through undetected.

Tip

Start threshold calibration with six months of historical exception data. Identify the distribution of legitimate vs. false-positive alerts at different threshold levels, then set your initial threshold at the point where the false-positive rate drops below 20%. Refine quarterly based on actual resolution outcomes.

Implementing Continuous Risk Monitoring in the SSC

SSC risk monitoring extends beyond traditional controls. It is a continuous analytical layer that scans transactional patterns for anomalies — not just rule violations. A control catches an invoice that exceeds an approval limit. Risk monitoring catches a pattern of invoices deliberately split to stay below that limit. A control verifies that a payment matches an approved purchase order. Risk monitoring notices that a specific user has been creating and approving purchase orders for the same vendor repeatedly, bypassing the intended segregation.

Real-Time versus Periodic Monitoring — What Fits Financial Transactions?

For high-risk processes such as payment execution and vendor master changes, real-time monitoring is essential because the window for prevention closes the moment funds leave the account. For lower-risk processes such as accrual accuracy or intercompany matching, daily or weekly monitoring may be sufficient. The decision depends on the reversibility of the action: if you cannot easily undo the consequence, monitor in real time.

Did You Know

The average time between a fraudulent vendor bank-account change and the resulting payment execution is less than 72 hours in most SSC environments. Once funds leave the account, recovery rates drop below 30%. Real-time monitoring of master data changes closes this window entirely by flagging modifications the moment they occur.

Calibrating Risk Thresholds to Avoid Alert Fatigue

The most common failure in risk monitoring implementations is excessive false positives. When 80% of alerts turn out to be benign, reviewers stop taking them seriously. Effective calibration starts with historical data analysis to understand normal transaction patterns, followed by iterative tuning based on resolution outcomes. Platforms like Detelix approach this challenge by combining rule-based logic with behavioral baselines, so that alerts reflect genuine deviations rather than normal business variability.

Your shared services center processes thousands of transactions daily. How many slip through without a single automated check? Talk to Detelix about closing the gap between documented controls and real operational protection.

How Automated Controls Enforce Segregation of Duties in Practice

Segregation of duties is one of the most fundamental internal controls, yet it is also one of the most frequently compromised — especially in lean SSC teams where staff members cover multiple roles. Manual SoD monitoring typically relies on periodic access reviews, which reveal conflicts only after the fact. Automated enforcement operates differently: it evaluates user permissions and transactional activity continuously, flagging conflicts as they occur rather than during a quarterly review cycle.

For example, if a user who normally processes invoices is temporarily granted payment-release authority due to a colleague’s absence, an automated SoD control immediately identifies the conflict, logs it, and routes an alert to the control owner. This approach does not prevent the business from operating — the exception can be approved if justified — but it ensures that every deviation is documented, reviewed, and traceable.

Tip

Build your SoD matrix around transactional actions, not just system roles. Two users may hold different role names but perform conflicting actions in practice. Monitor actual transaction execution patterns — who created, who approved, who released — rather than relying solely on role-based access definitions.

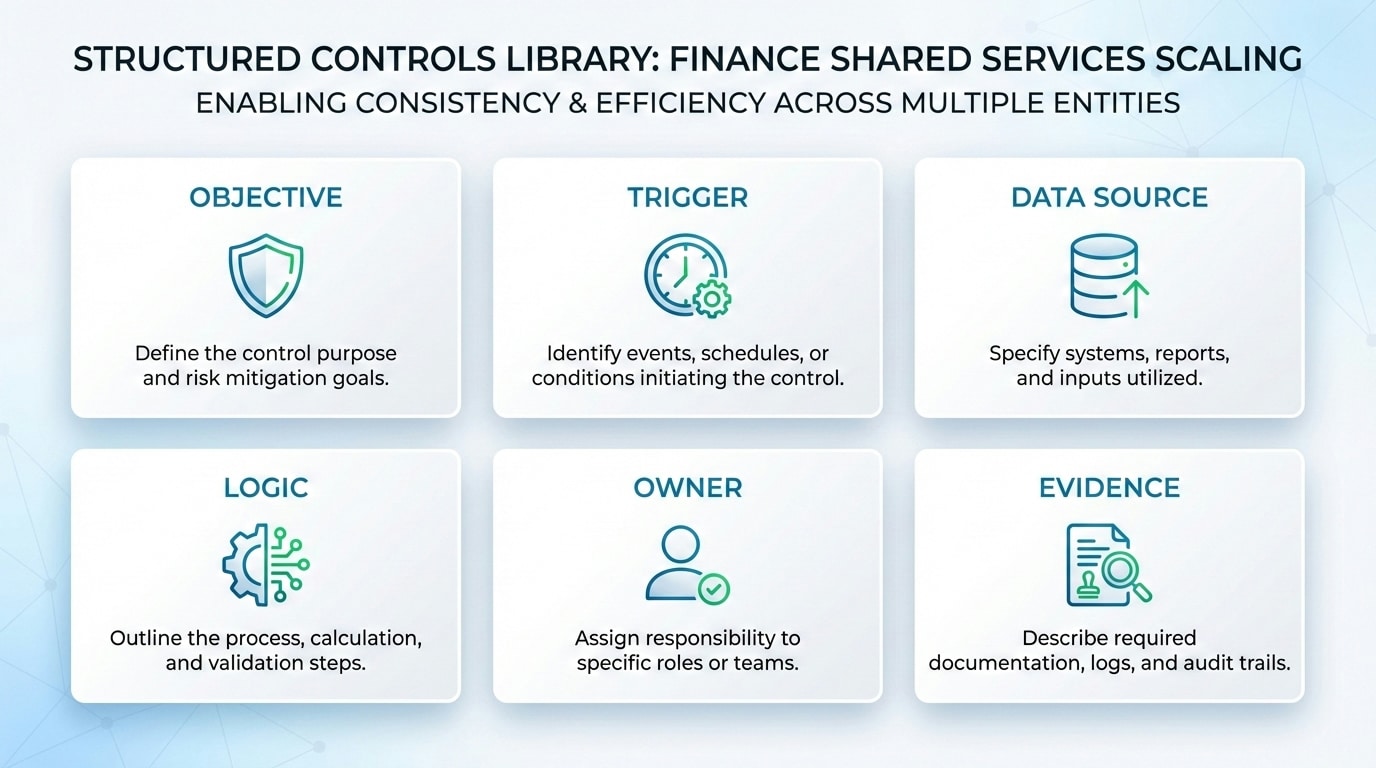

Building a Controls Library That Scales across Entities and Processes

A controls library is a structured catalogue of every automated check, organized by process area, risk category, frequency, ownership, required evidence, and success metric. Without this catalogue, control coverage becomes fragmented: one entity may have robust duplicate-payment detection while another relies on manual spot checks. The library creates standardization.

| Component | Description | Example |

|---|---|---|

| Objective | What risk does this control mitigate? | Prevent duplicate vendor payments |

| Trigger | When does the control execute? | Before every payment batch release |

| Data Source | Which ERP fields are evaluated? | Invoice number, amount, vendor ID, date |

| Logic | What rule is applied? | Flag if same amount + vendor within 30 days |

| Owner | Who reviews flagged exceptions? | AP Team Lead |

| SLA | How quickly must the exception be resolved? | Within 4 business hours |

| Evidence | What is recorded for audit? | Rule output, reviewer decision, timestamp |

This structure prevents overlap between SSC controls and local business-unit controls by clearly assigning ownership and eliminating ambiguity about who is responsible for what.

Which AP Processes Are the Best Candidates for Automated Controls

Accounts payable consistently offers the highest return on control automation because it combines high volume, high financial exposure, and frequent fraud targeting. The strongest initial candidates include duplicate invoice detection, purchase-order-to-invoice matching, approval-limit enforcement, payment-term compliance, and vendor master data change monitoring. Each of these can be implemented with clear rules, measurable outcomes, and immediate risk reduction — making them ideal pilot processes before expanding to other areas.

Did You Know

Duplicate payments account for an estimated 0.1% to 0.5% of total AP disbursements across industries. For an SSC processing $500 million annually, that represents $500,000 to $2.5 million in recoverable losses — most of which go undetected under manual sampling approaches.

Where AR and Collections Benefit Most from Control Automation

On the receivables side, the risks are different but equally consequential. Unauthorized credit notes reduce revenue. Incorrect cash application distorts aging reports and collection priorities. Unapproved changes to customer credit limits expose the organization to bad-debt risk. Automated controls in AR focus on flagging credit notes above defined thresholds, validating cash-application matching accuracy, monitoring write-off patterns, and detecting deviations from approved pricing agreements. These controls protect revenue integrity — a dimension often overlooked when organizations focus primarily on payables fraud.

How Control Automation Shortens Month-End Close Without Increasing Risk

The month-end close is where control weaknesses become most visible — and most painful. Unresolved exceptions, incomplete reconciliations, and last-minute journal adjustments consume time and introduce errors. Control automation compresses the close by resolving issues continuously throughout the month rather than accumulating them for a single close cycle.

Continuous Controls Monitoring as Part of a Modern Close

Instead of waiting until day one of the close to begin bank reconciliations, an automated system performs matching daily and flags unreconciled items immediately. Instead of discovering an intercompany imbalance on close day three, continuous monitoring identifies it the moment a posting creates a mismatch. This approach — sometimes called “continuous close” — does not eliminate the formal close process, but it dramatically reduces the volume of work and surprises that the close team must handle under time pressure.

Tip

Track the number of open exceptions at each day of the close cycle month over month. A declining trend proves that continuous monitoring is resolving issues earlier. If the number plateaus or increases, investigate whether new transaction types or process changes have introduced gaps in rule coverage.

Exception Handling: The Process That Makes or Breaks Scalability

Detecting exceptions is only half the equation. What happens after an alert fires determines whether the control adds value or simply adds noise. Scalable exception handling requires a defined workflow: each exception is categorized by type and severity, assigned to a specific owner, tracked against an SLA, and escalated automatically if not resolved in time. The exception record must capture the original alert, the reviewer’s analysis, the decision taken, and the supporting evidence.

Organizations that treat exception handling as an afterthought end up with growing backlogs, inconsistent resolution quality, and an audit trail full of gaps. Detelix addresses this by embedding the exception workflow directly into the detection process — so that every flagged item arrives with context, recommended actions, and a clear resolution path. This reduces the cognitive load on reviewers and keeps resolution times predictable even as transaction volumes grow.

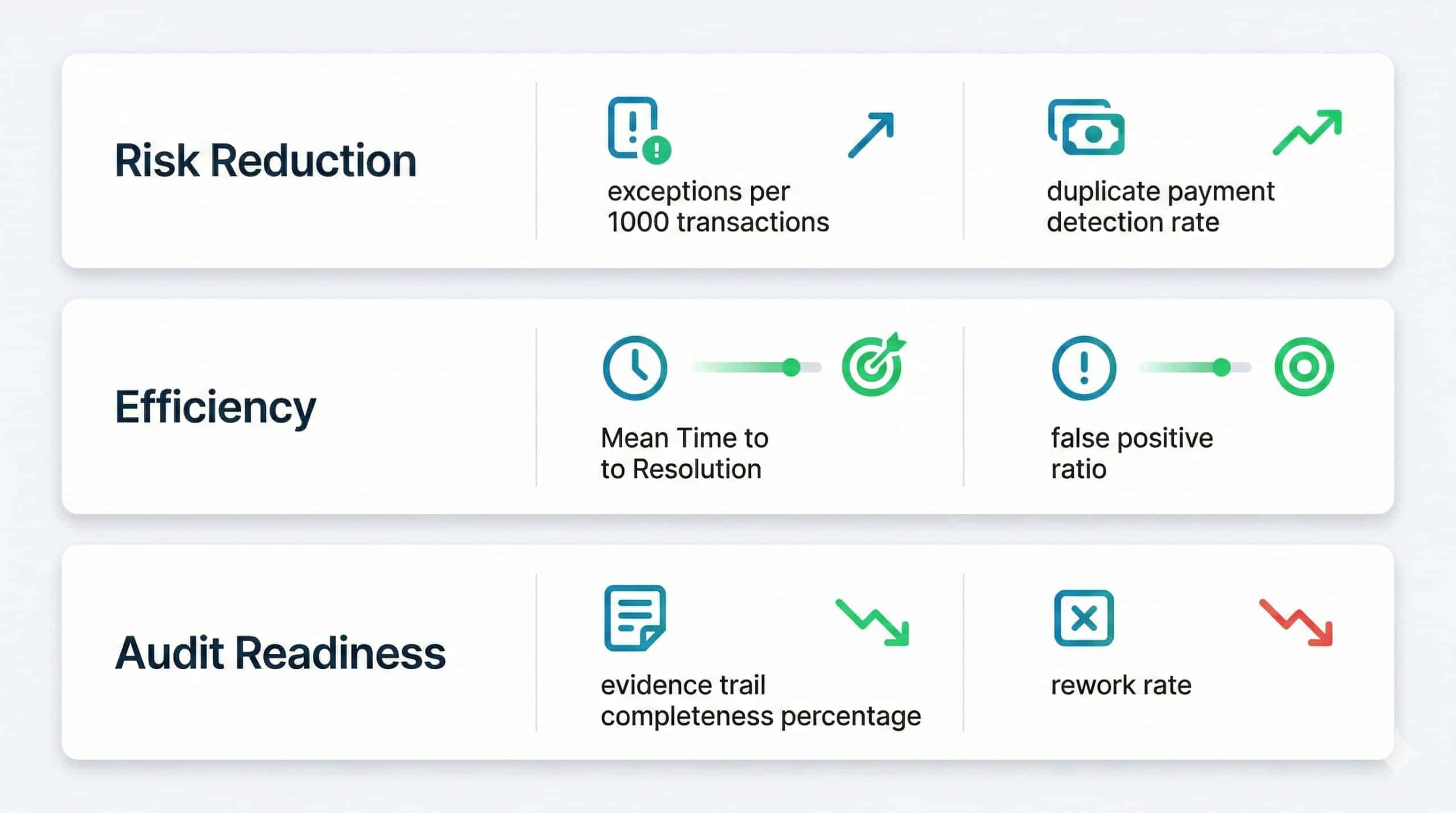

Which KPIs Prove That Automated Controls Are Actually Working

Measuring control effectiveness requires metrics that go beyond simple counts. The table below maps key performance indicators across three dimensions: risk reduction, operational efficiency, and audit readiness.

| Dimension | KPI | Target Direction |

|---|---|---|

| Risk Reduction | Material exceptions per 1,000 transactions | Decreasing |

| Risk Reduction | Duplicate payments detected before release | Increasing (as % of total duplicates) |

| Efficiency | Mean Time to Resolution (MTTR) for exceptions | Decreasing |

| Efficiency | False positive ratio | Below 20% |

| Audit Readiness | % of controls with complete evidence trail | Above 95% |

| Audit Readiness | Rework rate (post-posting corrections) | Decreasing |

Balancing Service KPIs and Control KPIs

A tension often exists between service metrics (processing speed, cost per transaction) and control metrics (exception rates, compliance scores). The risk is that teams optimize for speed at the expense of control quality — or vice versa. The solution is to report both dimensions together in governance reviews, ensuring that improvements in one area do not come at the cost of the other.

Did You Know

SSCs that report service KPIs and control KPIs in the same governance dashboard — rather than in separate reports to different stakeholders — resolve the speed-vs-control tension 60% faster, because tradeoffs become visible to decision-makers in a single view rather than surfacing as competing narratives in different meetings.

What Does a GBS Governance Model Look Like When It Sustains Controls

Governance is not a one-time design exercise. It is a recurring operating rhythm. A governance model that sustains controls over time typically includes a monthly operational review (exception trends, KPI performance, SLA adherence), a quarterly governance board (control changes, policy updates, risk-appetite adjustments), and an annual strategic review (control maturity assessment, technology roadmap, regulatory alignment).

RACI for Control Ownership between SSC, Finance, and Business Units

Ambiguity about who owns a control is the most common reason controls fail silently. A RACI matrix should specify who is Responsible for executing the control, who is Accountable for its effectiveness, who is Consulted when changes are needed, and who is Informed about outcomes. In most GBS models, the SSC is Responsible for execution, the global process owner is Accountable, local finance teams are Consulted, and internal audit is Informed.

Tip

Review your RACI matrix every time a control owner changes roles or leaves the organization. Orphaned controls — those with no active Accountable owner — are the most likely to fail silently. Set a quarterly reminder to verify that every control in the library has a named, active owner who acknowledges their accountability.

Creating an Automated Audit Trail That Satisfies Auditors

An audit trail is only as useful as its completeness and accessibility. Automated controls generate evidence by design: every rule execution produces a record of the data evaluated, the logic applied, the result, and the subsequent action. This eliminates the common audit frustration of chasing down evidence after the fact. The Israel National Cyber Directorate’s reporting guidelines emphasize the importance of system logs and technical documentation as foundational evidence — a principle that applies equally to financial control environments. When every control action is logged with timestamps, user identities, and data snapshots, audit preparation shifts from a stressful evidence-gathering exercise to a straightforward report extraction.

Common Mistakes When Automating Controls and How to Avoid Them

Automation introduces its own risks. The most frequent mistakes include deploying rules based on assumptions rather than historical data analysis, failing to update rules as business processes change, granting excessive override permissions that neutralize the control’s intent, and treating automation as a replacement for human judgment rather than a complement to it. Each of these can be mitigated through disciplined change control — reviewing and revalidating rules on a defined schedule, monitoring rule-drift indicators, restricting override access, and maintaining a human review layer for high-impact exceptions.

Did You Know

Override permissions are the leading cause of automated control failures. In a study of SSC control environments, 73% of material exceptions that bypassed automated checks were processed using override credentials that had been granted temporarily but never revoked. Time-bound override access with automatic expiration eliminates this risk entirely.

One advantage of working with a purpose-built platform is that these safeguards are embedded into the system design. Detelix, for instance, enables organizations to ensure every action in the ERP system is validated against current rules, with version history maintained for every rule change — creating accountability not just for transactions, but for the controls themselves.

How Long Does Implementation Take and What Drives the Cost

Most organizations begin with a focused pilot: a defined set of controls for one or two process areas (typically AP and bank-account changes) across a limited number of entities. A pilot of this scope typically runs six to ten weeks from kickoff to production. Scaling from pilot to full deployment depends on several factors: ERP complexity and the number of instances involved, the degree of process standardization already in place, data quality and accessibility, integration requirements with downstream systems, and the maturity of the existing governance framework.

Organizations with a single ERP instance and standardized processes can scale relatively quickly. Those with fragmented landscapes or significant local process variations should plan for a phased rollout, entity by entity or process by process, with governance checkpoints between phases.

Moving from Detective Controls to Predictive Governance

The evolution of SSC controls follows a clear trajectory. The first generation focused on detective controls — finding errors after they occurred. The second generation, now mainstream, emphasizes preventative controls — stopping errors before they cause financial impact. The emerging third generation adds predictive capability: using historical exception patterns, process-mining data, and behavioral baselines to anticipate where the next control failure is likely to occur.

Predictive governance does not replace rules-based controls. It adds an intelligence layer that helps GBS leaders prioritize their attention, allocate review resources more effectively, and address systemic process weaknesses before they produce exceptions. This is where finance shared services control automation delivers its highest strategic value — transforming the control function from a cost center into a source of operational intelligence.

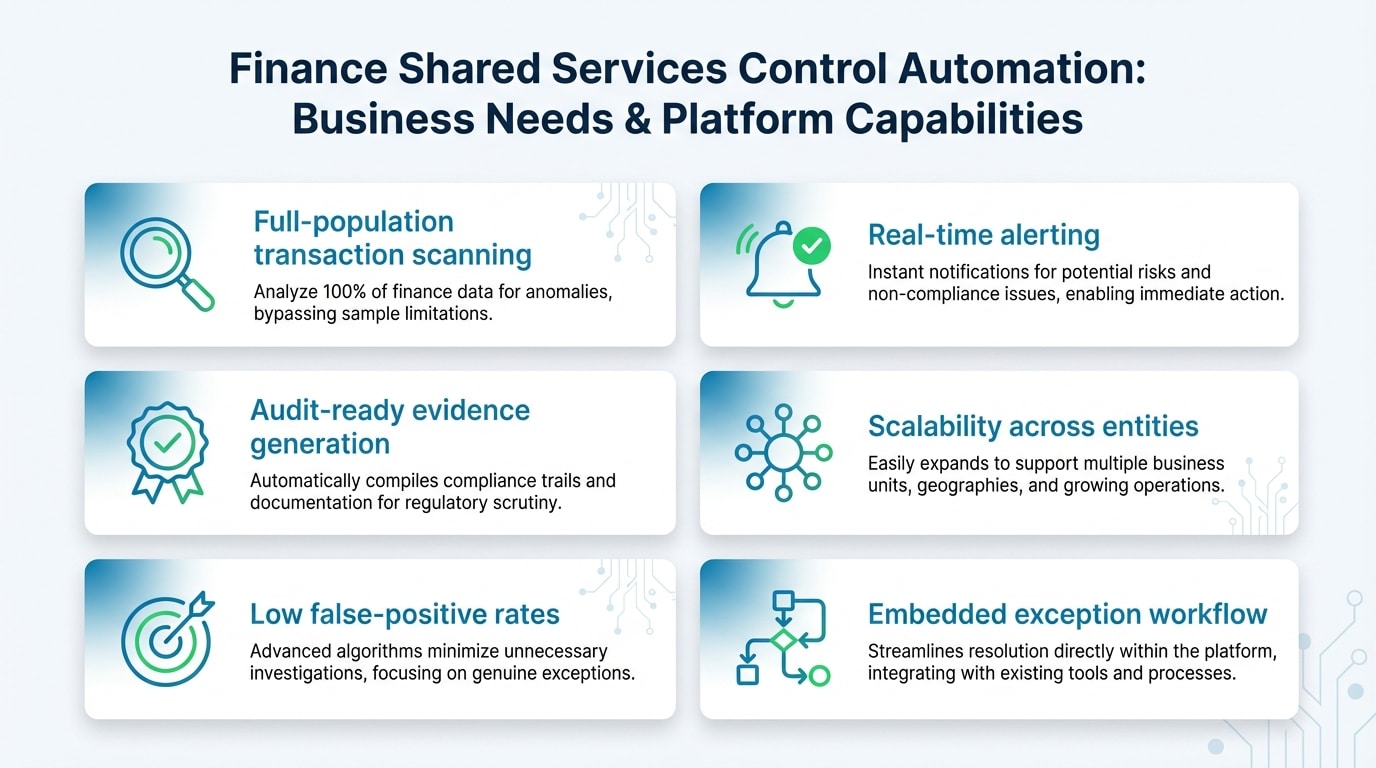

Matching Business Needs to Platform Capabilities

| Business Need | What to Look for in Practice |

|---|---|

| Full-population transaction scanning | The platform tests 100% of transactions, not samples, without requiring manual uploads |

| Real-time alerting for high-risk actions | Alerts on vendor bank changes, split payments, and SoD conflicts fire immediately, not in a batch report |

| Audit-ready evidence generation | Every control execution is logged with data, logic, outcome, and reviewer action — exportable for auditors |

| Scalability across entities and ERPs | The same control rules deploy across multiple legal entities with local threshold adjustments |

| Low false-positive rates | Rule calibration is data-driven, with continuous tuning based on resolution feedback |

| Embedded exception workflow | Exceptions route to owners with context and SLA tracking, not just a list of alerts |

Detelix is designed around these exact requirements. It operates as a continuous protection layer over ERP-driven financial processes, providing real-time visibility into sensitive actions — from vendor payments and procurement to payroll and inventory — so that finance and operations leaders can act before damage occurs rather than investigate after the fact.

Detelix Continuous Control and Fraud Prevention Solutions

Proactive Monitoring

Continuous scanning of every ERP transaction against predefined rules, catching exceptions before they cause financial damage.

Real-Time Alerts

Instant notifications for high-risk actions such as vendor bank changes, split payments, and segregation of duties violations.

GateKeeper

Automated quality gates that block unauthorized or suspicious transactions before payment execution, with full audit trail.

Experience & Expertise

Decades of domain expertise in financial controls, fraud prevention, and ERP security across industries and geographies.

See Detelix in Action

Frequently Asked Questions

Does automating controls mean eliminating the internal control team?

No. Automation handles repetitive, high-volume checks that would be impractical for humans to perform consistently. The control team’s role shifts from manual testing to exception review, rule management, root-cause analysis, and governance oversight — higher-value work that requires judgment and experience.

Can automated controls integrate with multiple ERP systems in the same SSC?

Yes, provided the platform is designed for multi-system environments. The key requirement is the ability to normalize data from different ERPs into a common control framework, so that the same rule logic applies regardless of the source system.

How do you prevent automated rules from becoming outdated as processes change?

Through a formal change-control process: every rule has a defined owner, a review schedule, and version history. When a process changes — a new approval threshold, a revised vendor onboarding workflow — the corresponding rules are updated, tested, and redeployed with full documentation.

What is the typical ROI timeline for finance shared services control automation?

Most organizations see measurable results within the first quarter after pilot deployment. The fastest returns come from duplicate-payment prevention and vendor-fraud detection, where a single prevented incident can exceed the annual cost of the platform. Longer-term ROI accumulates through reduced close times, lower audit costs, and improved transactional finance quality.

Is real-time monitoring necessary for all SSC processes, or only high-risk ones?

Real-time monitoring is most critical for irreversible, high-impact actions such as payment execution and master-data changes. For processes where corrections are straightforward — such as accrual adjustments or intercompany allocations — daily or weekly monitoring typically provides sufficient coverage without over-engineering the control environment.

Ready to Move from Routine Monitoring to Real Control?

If your shared services center is scaling faster than your control framework, the risk is operational and financial. Discover how continuous, real-time control automation protects your organization’s financial integrity.