Stop Embezzlement Before It Starts — Protect Your Financial Operations

Detelix provides real-time continuous monitoring that catches fraudulent transactions the moment they happen, not months later during an audit.

- What Separates Embezzlement from General Employee Theft?

- The Fraud Triangle: Why Trusted Employees Cross the Line

- Which Departments Are Most Vulnerable to Workplace Fraud?

- Recognizing the Red Flags Before Damage Escalates

- Building Segregation of Duties Even in Small Teams

- A Scenario: How a Fictitious Vendor Scheme Unfolds Undetected

- Comparing Periodic Auditing with Continuous Monitoring

- What Should Embezzlement Detection Software Actually Do?

- Common Mistakes That Undermine Even Good Controls

- How Detelix Addresses Real Operational Needs

- Designing a Payment Approval Process That Prevents Fraud

- Building a Whistleblowing Channel That People Actually Use

- When You Suspect Embezzlement: The First 72 Hours

- Access Control Policies That Prevent Concentrated Power

- Measuring the ROI of an Embezzlement Prevention Program

- Quick-Reference Checklist: Immediate Actions

- Frequently Asked Questions

In many organizations, the financial controls that exist on paper — approval workflows, ERP permissions, reconciliation schedules — create a sense of security. Yet employee embezzlement prevention remains one of the most underestimated challenges facing finance leaders today. Embezzlement rarely looks dramatic. It hides inside routine processes: a slightly altered bank account number, a vendor that exists only on paper, a payroll adjustment that no one questions. The damage accumulates quietly over months or years, and by the time it surfaces, the financial and reputational cost can be devastating.

The question for every CFO, controller, and operations leader is not whether their organization could be targeted — it is whether their current controls would detect it in time. This guide provides a structured, practical approach to understanding where embezzlement hides, how to build layered defenses, and why real-time visibility through tools like Detelix’s continuous monitoring platform is transforming the way organizations move from reactive investigation to proactive prevention.

Key Takeaways

- Embezzlement exploits trusted access and routine processes — making it fundamentally different from general theft and far harder to detect with periodic audits alone.

- Accounts Payable, payroll, and expense reimbursement are the three highest-risk functions where fictitious vendor schemes, ghost employees, and duplicate payments thrive.

- Continuous monitoring that scans 100% of transactions in near real-time dramatically shortens the detection window compared to sample-based quarterly or annual audits.

- Segregation of duties, dual authorization, independent bank reconciliation, and whistleblowing channels form the essential control layers every organization needs.

- Detelix operates as an independent monitoring layer over ERP-driven processes, cross-checking vendor data, payment patterns, and user activity to flag exceptions before funds leave the organization.

What Separates Embezzlement from General Employee Theft?

The distinction matters because prevention strategies differ. Employee theft typically involves taking a physical asset — cash from a register, inventory from a warehouse — in a discrete event. Embezzlement, by contrast, is the systematic misappropriation of funds or assets by someone who was entrusted with access to them. The employee leverages legitimate authority — signing checks, approving invoices, managing payroll — to divert money over an extended period.

This reliance on trust and process knowledge is what makes corporate embezzlement detection so difficult using traditional periodic audits alone. The perpetrator knows exactly which controls exist, which transactions are reviewed, and which thresholds trigger additional scrutiny. They design their scheme to operate beneath every one of those thresholds.

Tip

When assessing your fraud risk exposure, focus specifically on employees who hold both data-entry authority and approval authority within the same process. These dual-control positions represent the highest-risk points for embezzlement schemes.

The Fraud Triangle: Why Trusted Employees Cross the Line

Understanding motivation is not about excusing behavior; it is about designing smarter controls. The well-established “Fraud Triangle” identifies three converging factors: perceived financial pressure, rationalization (“I deserve this” or “I will pay it back”), and opportunity. Of these three, opportunity is the only factor an organization can directly control.

Weak segregation of duties, excessive system permissions, infrequent reconciliations, and a culture that discourages questioning — all of these widen the window of opportunity. Effective employee embezzlement prevention therefore focuses on systematically shrinking that window at every critical process point.

Did You Know

According to the Association of Certified Fraud Examiners, the typical occupational fraud scheme lasts 12 months before detection — and organizations with proactive continuous monitoring cut that duration nearly in half compared to those relying solely on periodic audits.

Which Departments Are Most Vulnerable to Workplace Fraud?

Not every function carries equal risk. Finance operations research consistently highlights three areas where the combination of transaction volume, payment authority, and data complexity creates the ideal conditions for undetected schemes.

Accounts Payable: The Largest Attack Surface

Accounts Payable processes thousands of invoices, manages vendor master data, and triggers outgoing payments. Fictitious vendor schemes — where an employee creates a shell supplier and routes payments to a personal account — remain among the most common forms of embezzlement. The FBI warns that business email compromise (BEC) has dramatically increased the ease with which payment details can be manipulated, whether by an outside attacker or a complicit insider.

Payroll and Expense Reimbursement

Payroll fraud may involve “ghost employees,” unauthorized salary increases, or redirection of wages to the perpetrator’s bank account. Expense reimbursement fraud includes duplicate claims, inflated receipts, and fictitious travel. In high-volume environments, these anomalies blend into the noise unless automated exception reporting is in place.

Tip

Run a quarterly cross-match between your HR employee roster and your payroll disbursement list. Any payroll payment going to an individual not on the active HR roster is an immediate red flag that warrants investigation.

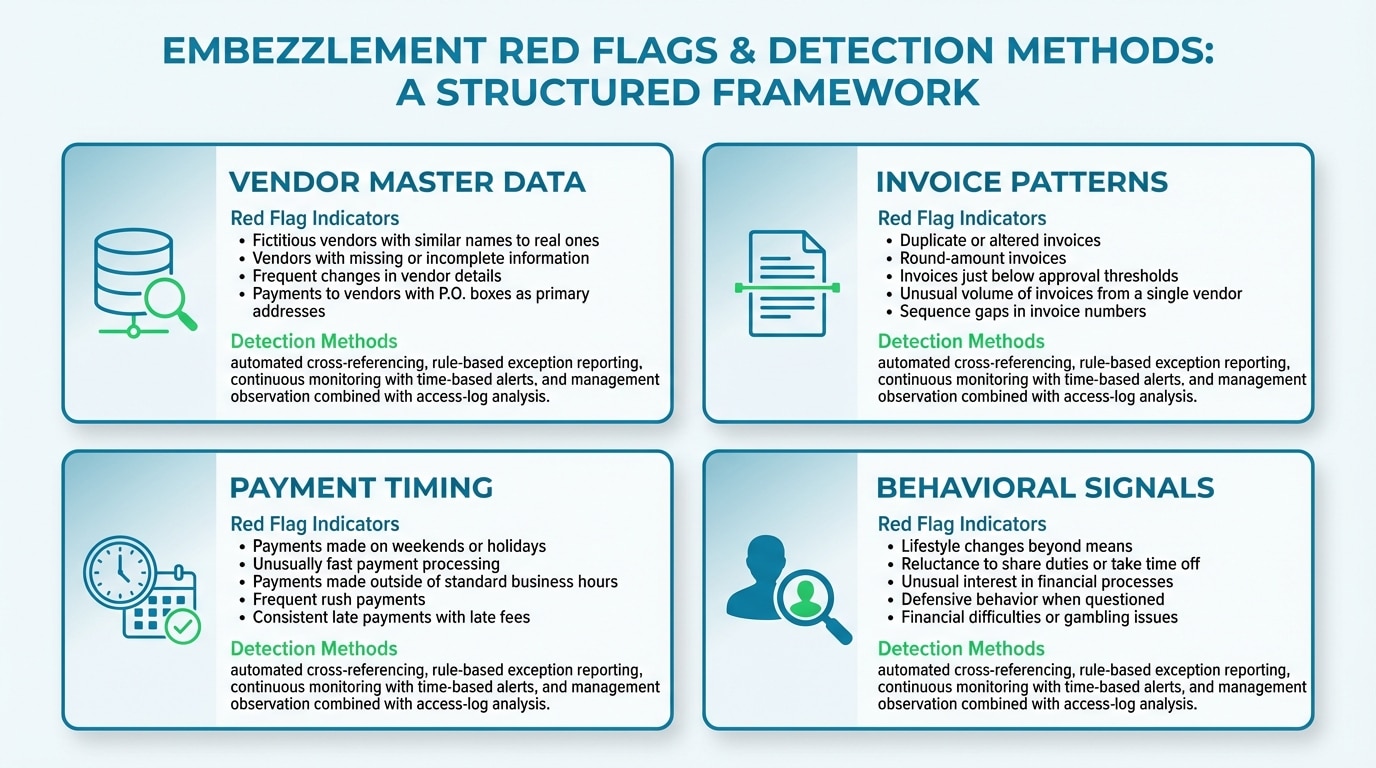

Recognizing the Red Flags Before Damage Escalates

Red flags fall into two categories. Data-driven indicators include duplicate invoice numbers, payments in suspiciously round amounts, vendors sharing a bank account or address with an employee, and transactions processed outside normal business hours. Behavioral indicators are equally telling: an employee who never takes vacation, resists job rotation, becomes defensive when processes are reviewed, or insists on handling both vendor setup and payment approval.

The challenge is that in organizations processing hundreds or thousands of transactions daily, spotting these signals manually is nearly impossible. This is precisely where workplace fraud prevention technology closes the gap — scanning every transaction against defined risk rules and flagging anomalies for human review.

| Red Flag Category | Example Indicators | Detection Method |

|---|---|---|

| Vendor Master Data | Duplicate bank accounts, PO Box addresses, employee-linked details | Automated cross-referencing of vendor and employee databases |

| Invoice Patterns | Sequential invoice numbers from different vendors, rounded amounts, just-below-threshold values | Rule-based exception reporting |

| Payment Timing | Transactions processed on weekends, holidays, or outside approval windows | Continuous monitoring with time-based alerts |

| Behavioral Signals | Refusal to delegate, no vacations, resistance to audits | Management observation combined with access-log analysis |

Did You Know

Payments processed in round numbers (e.g., exactly $5,000 or $10,000) are statistically far more likely to be fraudulent than payments with irregular amounts. Continuous monitoring systems flag these patterns automatically, while manual reviewers almost never catch them in high-volume environments.

Building Segregation of Duties Even in Small Teams

Segregation of duties (SoD) is the foundational control principle: the person who creates a vendor record should not be the person who approves payment to that vendor. The person who runs payroll should not be the person who adds new employees to the system. In large organizations, this is relatively straightforward. In smaller teams where one person wears multiple hats, compensating controls become essential.

These include mandatory dual authorization for payments above a threshold, periodic independent review of master data changes, and system-enforced approval workflows that prevent a single user from completing end-to-end transactions. According to NIST NCCoE guidelines on Access Rights Management, applying the principle of least privilege — granting only the minimum access necessary for each role — significantly reduces the risk of unauthorized actions.

Tip

If your team is too small to fully separate vendor creation from payment approval, implement a compensating control: require the business owner or a senior manager outside the finance function to review and approve all new vendor setups and any changes to existing vendor bank details.

A Scenario: How a Fictitious Vendor Scheme Unfolds Undetected

Consider this realistic sequence. A purchasing clerk with vendor creation rights registers a new supplier with a generic business name. The bank details route to an account the clerk controls. Over the following months, invoices arrive for “consulting services” at amounts just below the threshold requiring senior approval. Each payment is processed normally through the ERP.

Without continuous monitoring, the scheme may persist for years. The cumulative loss often reaches six or seven figures before an external audit or a chance observation triggers an investigation. The takeaway is not that approval workflows are useless — it is that approvals alone, without independent cross-checking and anomaly detection, leave critical blind spots.

Did You Know

Fictitious vendor schemes account for a significant portion of all AP fraud cases, and the median loss per scheme is substantially higher than other fraud types because they tend to run undetected for longer periods. Automated vendor-employee data cross-matching can identify these schemes within days of the first fraudulent payment.

Comparing Periodic Auditing with Continuous Monitoring

Traditional internal audits are valuable but inherently limited. They typically review a sample of transactions after the fact — sometimes months after the activity occurred. Continuous monitoring, by contrast, evaluates every transaction as it happens or shortly after, applying rule-based and anomaly-based checks across the full data set. The result is a dramatically shorter detection window.

| Dimension | Periodic Audit | Continuous Monitoring |

|---|---|---|

| Coverage | Sample-based (5-15% of transactions) | 100% of transactions |

| Timing | After the fact (quarterly/annually) | Near real-time or daily |

| Detection Speed | Weeks to months after occurrence | Hours to days |

| Cost of Missed Fraud | High (long exposure window) | Lower (early intervention) |

| Audit Trail | Reconstructed during investigation | Built continuously and preserved |

Detelix operates in this continuous monitoring space, functioning as an independent control layer over ERP-driven processes. Rather than replacing internal audit, it complements it by providing real-time visibility into sensitive actions — vendor creation, bank detail changes, payment anomalies, and more — so that exceptions can be investigated before funds leave the organization.

Your current controls may look strong on paper — but are they catching fraud in real time? Detelix monitors 100% of your financial transactions and flags anomalies before losses accumulate.

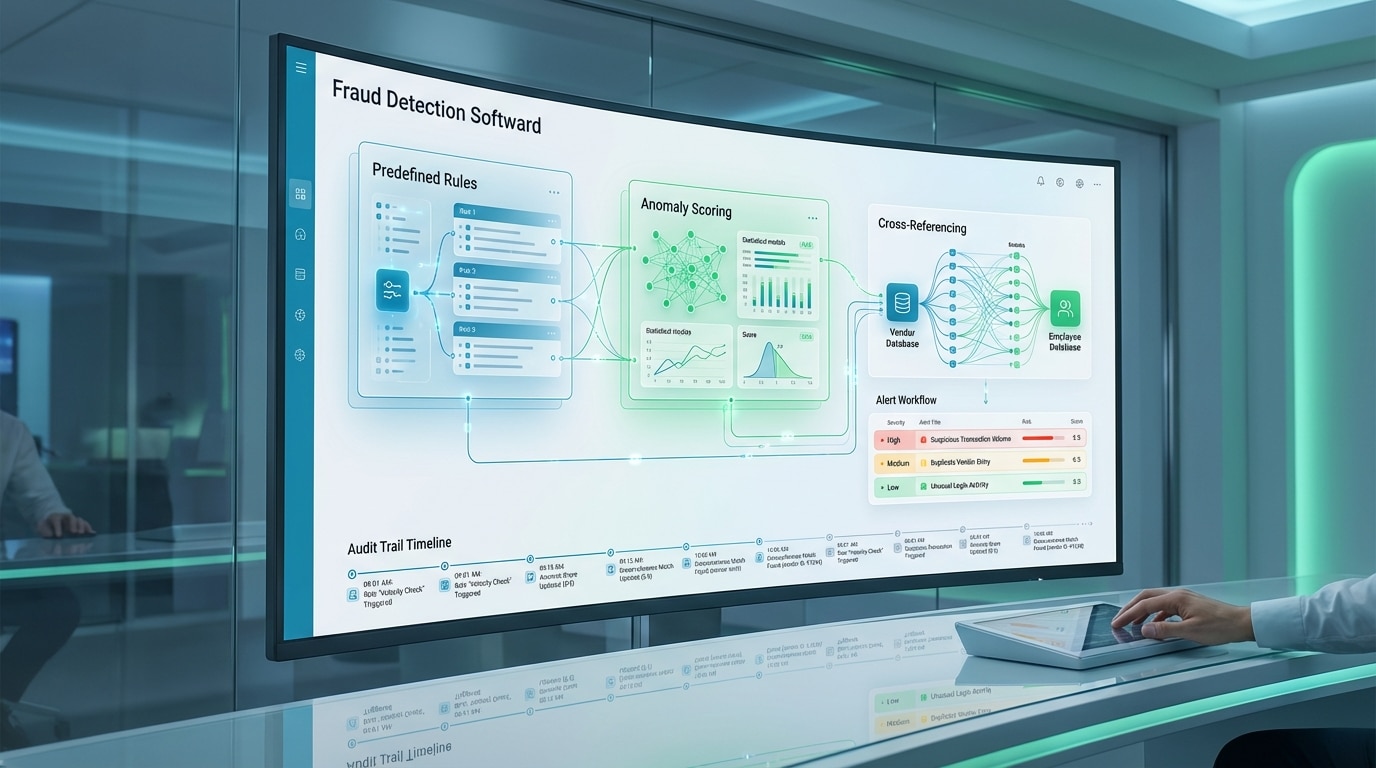

What Should Embezzlement Detection Software Actually Do?

Not every monitoring tool is designed for fraud prevention. When evaluating embezzlement detection software, finance leaders should look for specific capabilities that go beyond standard reporting. The system should connect to your core data sources — ERP, banking, HR, and procurement — and apply layered detection logic: predefined rules for known fraud patterns, anomaly scoring for deviations from baseline behavior, and cross-referencing between data sets (for example, matching vendor bank accounts against employee bank accounts).

Equally important is the quality of the alert workflow. A system that generates hundreds of unqualified alerts creates fatigue and is quickly ignored. Effective platforms prioritize alerts by risk severity, provide supporting evidence within the alert itself, and maintain a full audit trail of every action taken during the investigation process. As NIST SP 800-12 emphasizes, robust audit trails are essential not only for detection but for reconstructing events during a formal investigation.

Tip

When evaluating fraud detection platforms, request a demonstration using your own anonymized transaction data rather than the vendor’s sample data set. This reveals how the system performs against your specific transaction patterns, volume, and complexity — and exposes whether alert thresholds are calibrated for your environment.

Common Mistakes That Undermine Even Good Controls

Organizations often invest in policies and tools yet still suffer losses because of implementation gaps. One frequent mistake is granting “temporary” elevated access that is never revoked. Another is allowing a single employee to serve as the sole point of contact for a critical vendor relationship — creating both dependency and opportunity.

A third is treating the ERP’s built-in approval workflow as a substitute for independent monitoring: approvals confirm intent, but they cannot verify whether the underlying data (vendor details, invoice legitimacy, pricing accuracy) has been manipulated. Finally, neglecting to reconcile bank statements independently — relying instead on the same team that processes payments — removes a vital external checkpoint.

Did You Know

A significant percentage of fraud-enabling access rights are the result of “access creep” — permissions accumulated over years of role changes and system migrations that were never cleaned up. Organizations that conduct quarterly access reviews reduce their exposure to insider fraud by removing stale privileges before they can be exploited.

How Detelix Addresses Real Operational Needs

| Operational Need | How Detelix Helps in Practice |

|---|---|

| Detecting vendor master data manipulation | Cross-checks every change to vendor bank details, addresses, and identifiers against employee data and historical patterns, generating an alert when a match or anomaly is found |

| Preventing duplicate or fictitious payments | Scans 100% of payment transactions for duplicates, just-below-threshold amounts, and payments to newly created vendors with limited history |

| Enforcing segregation of duties | Monitors ERP user activity to flag instances where one user performed conflicting actions (e.g., created a vendor and approved payment to that vendor) |

| Maintaining investigation-ready audit trails | Logs every alert, every review action, and every data change with timestamps, supporting both internal investigation and regulatory compliance |

| Reducing alert fatigue | Prioritizes exceptions by risk score so that finance teams focus on the highest-impact items first, rather than drowning in low-risk noise |

Designing a Payment Approval Process That Prevents Fraud Without Slowing Operations

The goal is not to add bureaucratic layers but to embed smart checkpoints at the moments of highest risk. Define approval thresholds by amount and risk category: routine recurring payments below a set threshold may follow a streamlined path, while new vendors, changed bank details, and payments above the threshold require dual authorization.

Enforce a strict policy that any request to change vendor banking information must be verified through an independent channel — a phone call to a known contact number, not the number provided in the email requesting the change. This single control can prevent a significant percentage of both internal manipulation and external BEC attacks.

Tip

Maintain a verified contact directory for all critical vendors, separate from your ERP vendor master data. When a bank detail change request arrives, verify it by calling the number in your independent directory — never the contact information provided in the change request itself.

Building a Whistleblowing Channel That People Actually Use

Research from the Association of Certified Fraud Examiners consistently shows that tips are the number-one method by which occupational fraud is discovered — ahead of internal audits, management review, and automated monitoring. Yet many organizations either lack a formal reporting channel or have one that employees do not trust.

An effective whistleblowing program requires three elements: confidentiality (the reporter’s identity is protected), a credible non-retaliation policy, and visible follow-through (employees see that reports are taken seriously). The OECD Public Integrity Handbook stresses that organizations should offer multiple reporting paths — internal and external — and clearly communicate the process so that potential reporters understand what happens after they file a concern.

Did You Know

Organizations with formal anonymous reporting hotlines detect fraud faster and experience lower median losses than those without. The presence of a hotline alone acts as a deterrent — employees who know their colleagues have a safe way to report suspicious activity are less likely to attempt fraud in the first place.

When You Suspect Embezzlement: The First 72 Hours

The instinct to confront a suspect immediately is understandable but counterproductive. A rushed confrontation risks destroying evidence, alerting accomplices, and creating legal liability for the organization. Instead, follow a structured response.

In the first 24 hours, discreetly restrict the suspect’s system access and payment authority without raising alarm — this can often be framed as a routine IT security update. Simultaneously, preserve all relevant logs, documents, and email records. Within 48 to 72 hours, engage legal counsel and, if warranted, a forensic accounting specialist. Document the chain of evidence meticulously: who accessed what, when, and how the data was preserved. Only after the scope of the activity is understood should formal disciplinary or legal proceedings begin.

Equally critical is the remediation step: identify the specific control gap that allowed the scheme and close it immediately to prevent recurrence.

Tip

Before any suspected fraud investigation begins, ensure you have a pre-established relationship with a forensic accounting firm and legal counsel experienced in occupational fraud cases. Scrambling to find these resources during an active investigation wastes critical time and increases the risk of evidence mishandling.

Access Control Policies That Prevent Concentrated Power

A disproportionate number of embezzlement cases involve employees who accumulated broad access over time — often as a result of role changes, system migrations, or simple administrative neglect. Preventing this requires a proactive access governance framework.

Conduct quarterly reviews of user permissions across the ERP, paying particular attention to users with access to multiple sensitive functions (vendor maintenance, payment execution, bank reconciliation). Implement “break-glass” procedures for emergency access, ensuring that every use of elevated privileges is logged and reviewed. Rotate responsibilities where feasible, and require managerial sign-off for any change to master data fields — vendor bank accounts, employee salary records, and customer credit terms.

Did You Know

Mandatory vacation policies are one of the most effective — and most overlooked — fraud prevention controls. Many long-running embezzlement schemes collapse when the perpetrator is away from their desk for two consecutive weeks because a substitute discovers transactions or processes that do not align with normal procedures.

Measuring the ROI of an Embezzlement Prevention Program

Prevention programs often struggle for budget because their value is measured in losses that did not happen. Shift the conversation from “did we catch someone?” to measurable operational metrics: reduction in the average time from anomaly occurrence to detection, decrease in the number of unresolved exceptions at month-end, improvement in the percentage of transactions covered by automated controls, and reduction in false-positive alert rates over time.

Track the number of policy deviations identified and remediated before financial impact occurred. These metrics demonstrate that the program is actively strengthening the organization’s control environment — which is the true return on investment.

Quick-Reference Checklist: Immediate Actions to Strengthen Employee Embezzlement Prevention

1. Enforce segregation of duties across vendor creation, invoice approval, and payment release. 2. Require dual authorization for all payments above a defined threshold. 3. Verify every vendor bank detail change through an independent channel. 4. Conduct monthly bank reconciliations performed by someone outside the AP team. 5. Review ERP user access rights quarterly and revoke unnecessary privileges. 6. Implement continuous monitoring software that scans 100% of transactions. 7. Establish an anonymous whistleblowing channel with a clear non-retaliation policy. 8. Train all finance staff on red-flag recognition at least annually. 9. Require mandatory vacation for employees in sensitive financial roles. 10. Log and review all changes to master data (vendors, employees, bank accounts). 11. Define a documented incident response protocol for suspected fraud. 12. Measure and report prevention program KPIs to senior leadership quarterly.

Detelix Fraud Prevention Solutions

Proactive Monitoring

Continuous, automated scanning of every financial transaction against risk rules and anomaly baselines to catch fraud before losses accumulate.

Real-Time Alerts

Intelligent, risk-prioritized alerts delivered the moment an anomaly is detected — enabling investigation within hours, not months.

Gatekeeper

Automated enforcement of segregation of duties, approval workflows, and vendor master data integrity across your ERP environment.

Industry Experience

Deep domain expertise in financial controls, regulatory compliance, and fraud prevention across healthcare, government, and enterprise sectors.

See Detelix in Action

Frequently Asked Questions

Can embezzlement detection software replace internal auditors?

No. Embezzlement detection software and internal audit serve complementary functions. Software provides continuous, automated scanning of every transaction and generates real-time alerts for anomalies. Internal auditors bring judgment, context, and the ability to conduct deeper investigations. The most effective control environments use both — technology to ensure nothing slips through unmonitored, and experienced professionals to interpret findings and recommend process improvements.

How do you prevent embezzlement in a small business with limited staff?

When you cannot fully segregate duties due to team size, implement compensating controls. Require the business owner or a senior manager to review bank statements independently each month. Use dual-signature requirements for payments above a threshold. Leverage technology — even a basic continuous monitoring tool — to flag anomalies that a small team cannot manually review. Rotate tasks periodically so that no single person controls an end-to-end process indefinitely.

What is the typical financial impact of employee embezzlement before detection?

Industry research indicates that the median loss from occupational fraud schemes runs into tens of thousands of dollars, but long-running schemes involving trusted employees with broad access can reach hundreds of thousands or even millions. The longer the detection window, the greater the cumulative damage. This is why shortening the time between occurrence and discovery — through continuous monitoring and alert-driven review — is the single most impactful investment an organization can make.

Is it possible to build an effective prevention program without specialized software?

It is possible to build a foundational program using manual controls, segregation of duties, and periodic audits. However, manual programs cannot scale with transaction volume, and they leave gaps between audit cycles where fraud can go undetected. Specialized embezzlement detection software dramatically increases coverage, consistency, and speed of detection. For organizations processing significant payment volumes, the risk of relying solely on manual controls typically outweighs the investment in automation.

How does Detelix differ from standard ERP reporting tools?

Standard ERP reports show you what happened — after the fact, based on the data fields you choose to query. Detelix operates as an independent monitoring layer that continuously cross-checks ERP activity against risk rules, anomaly baselines, and external data points. It does not wait for someone to run a report. It proactively flags exceptions, prioritizes them by risk severity, and provides the evidence trail needed for investigation — shifting the organization from reactive discovery to real-time control.

Are Your Current Controls Actually Protecting Your Organization?

The difference between believing you have control and actually having it comes down to visibility. If your organization relies primarily on approvals and periodic audits, critical blind spots likely exist. Find out where your exposure is — before someone exploits it.