Spot ERP Fraud Before It Hits Your Bottom Line

Detelix helps finance and audit leaders detect red flags across payments, vendors, and master data in real time. Request a tailored walkthrough today.

- What ERP Fraud Red Flags Actually Are

- Critical Warning Signs in Financial Processes

- Vendor Master Data and Payment Anomalies

- Fraud Signals in Procurement and Inventory

- User Behavior and Access Control Vulnerabilities

- Error or Fraud? Telling the Difference

- Common Mistakes When Interpreting Red Flags

- ERP Fraud Red Flags by Risk Area

- Building a Monitoring Framework That Works

- Key Metrics to Track on an Ongoing Basis

- Responding When a Red Flag Appears

- Reducing ERP Fraud Risk Before It Starts

- Frequently Asked Questions

In many organizations, ERP systems form the operational backbone of finance, procurement, inventory, and payments. On paper, the controls look solid: approval flows, user permissions, reconciliations, and periodic reviews. Yet when routines become predictable and oversight depends heavily on after-the-fact reporting, risk can move through the system unnoticed. Identifying ERP fraud red flags early is one of the most practical ways finance and audit leaders can move from the illusion of control to real, continuous control. A single anomaly may be a harmless mistake, but persistent patterns, unusual timing, and combinations of small irregularities often signal something far more serious. Recognizing these indicators early protects revenue, preserves data integrity, and reduces exposure to regulatory, audit, and reputational damage. This guide walks through the most important warning signs across key ERP modules and how to build a framework that detects them before the damage occurs, as explored in How to Crack Errors and Frauds Worth Millions.

Key Takeaways

- Single anomalies rarely prove fraud — clusters of aligned signals across users, vendors, or processes are the real warning.

- Vendor bank account changes shortly before a payment run are one of the strongest leading indicators of payment fraud.

- Broken segregation of duties and tolerated approval bypass are the most reliable predictors of internal fraud schemes.

- Continuous, real-time monitoring detects red flags before money leaves the organization — periodic audits catch them afterward.

- Pattern, intent, and benefit — not volume of exceptions — are what distinguish honest errors from deliberate misconduct.

What ERP Fraud Red Flags Actually Are

ERP fraud red flags are signals, patterns, or anomalies in the system that indicate elevated risk of fraud, manipulation, or control circumvention. They can appear at the user, vendor, transaction, permission, or audit-log level. One isolated event rarely proves wrongdoing — but when several indicators align around the same user, vendor, or process, the probability of intentional misconduct rises sharply. The goal is not to chase every exception, but to recognize combinations that demand a closer look. This mindset shift — from reacting to isolated errors to interpreting patterns — is what separates routine monitoring from real control.

Tip

Build a simple “signal correlation” habit: when an alert appears, immediately check whether the same user, vendor, or approver appears in other recent exceptions. A single isolated flag is noise; three connected flags are a lead worth investigating.

Critical Warning Signs in Financial Processes

Inside the General Ledger and Accounts Payable, warning signs of ERP fraud often hide in plain sight. Manual journal entries posted outside business hours, by users who normally do not touch the GL, or right before period close, deserve scrutiny. Another classic indicator is “round-number transactions” or structured amounts just below approval thresholds — for example, multiple payments of 9,500 or 14,900 that sit deliberately under review limits. Unusually high volumes of adjustments, reversals, or reclassifications near quarter-end can also signal earnings manipulation or cover-up activity. As noted in official internal control guidance from GAO, verifying the business justification for manual entries and exceptions is a foundational control that many organizations under-apply.

Did You Know

Analysis of corporate fraud cases consistently shows that a disproportionate share of fraudulent journal entries are posted in the final days of a reporting period — the exact window when finance teams are most time-pressured and review scrutiny is typically lowest.

Vendor Master Data and Payment Anomalies

Few areas expose an organization faster than weak controls over vendor master data. Suspicious ERP activity indicators in this domain include frequent changes to vendor bank accounts, addresses, or contact details — especially shortly before a scheduled payment run. Duplicate vendors, “ghost” suppliers with minimal transaction history, or vendors that share an address, phone, or bank account with an employee are all high-priority signals. State audit findings have repeatedly highlighted that missing documentation when opening a new vendor or modifying banking details is a primary driver of payment fraud. A strong control environment verifies every bank account change against an independent source, not just an email request. Detelix is designed to cross-check vendor data changes against payments in real time, so a suspicious update does not quietly become a suspicious transfer.

Bank Account Change as a Leading Indicator

A bank account change is one of the strongest single-event red flags in ERP. When it occurs close to an invoice approval, originates from an unusual channel, or is performed by a user who does not normally manage vendor data, it should trigger an immediate review rather than a routine update.

Tip

Enforce a dual-verification rule for every vendor bank account change: the request must be confirmed through an independent phone call to a previously known number at the vendor — never a number provided in the change request itself.

Fraud Signals in Procurement and Inventory

Within the supply chain, fraud signals in ERP often appear as excessive “emergency” purchases, repeated use of a single preferred vendor without competitive justification, or splitting a large order into smaller ones to stay below approval thresholds. Purchases made without a matching purchase order, or goods receipts entered after the invoice, are also common patterns. On the inventory side, frequent write-offs, unexplained transfers between warehouses, and recurring gaps between physical counts and system records point to possible theft or manipulation. The risk intensifies when the same user initiates, receives, and adjusts inventory records — classic evidence of broken segregation of duties.

Did You Know

“Order splitting” — dividing one purchase into several smaller ones to stay under an approval threshold — is one of the most common procurement fraud schemes, and it is visible in ERP data as multiple orders to the same vendor within days, each suspiciously close to a threshold limit.

User Behavior and Access Control Vulnerabilities

Excessive privileges and weak segregation of duties are among the most reliable predictors of internal fraud. When a single user can create a vendor, post an invoice, and release a payment, the system itself becomes the opportunity. Other access-related red flags include shared or generic accounts, dormant users with active permissions, and privileged administrators performing routine business transactions. System-level indicators such as logins at odd hours, from unusual IP addresses, or repeated failed access attempts often precede or accompany fraudulent activity. Official NIST guidance on privileged account management emphasizes that continuous auditing of high-level accounts is essential to prevent unauthorized overrides.

The Dangers of Approval Workflow Bypassing

Approval bypass rarely looks dramatic. It usually appears as a large invoice split into smaller ones, a manager approving their own requests under a temporary delegation, or senior leadership overriding a control “just this once.” These patterns are especially dangerous because they normalize exceptions. Reports from GAO on weak internal controls repeatedly show that tolerated bypasses are a leading cause of improper payments and long-running fraud schemes.

Tip

Run a quarterly “conflict report” that lists every user who performed two or more of these actions in the same quarter: create/modify vendor, approve invoice, release payment. This is often the fastest way to surface broken segregation of duties.

Waiting for the next audit to find ERP fraud is no longer a strategy — it’s a risk. Detelix monitors your most sensitive transactions continuously, so anomalies are surfaced before they become losses.

Error or Fraud? Telling the Difference

Not every anomaly is fraud. A duplicate invoice may be a data-entry mistake. A late journal entry may reflect a legitimate correction. The distinction lies in pattern, intent, and context. A single error tends to be random, isolated, and easy to explain. A fraud signal tends to repeat, cluster around specific users or vendors, and lack a clear business justification. When the same person keeps appearing at the center of exceptions — across modules, across time, and across sensitive actions — the probability of intentional behavior grows. The real question is not “was this wrong?” but “why did this keep happening, and who benefited?”

Did You Know

Behavioral research on occupational fraud shows that perpetrators rarely commit one large act — the average scheme involves dozens to hundreds of smaller transactions over many months, which is exactly why pattern detection outperforms one-off exception reviews.

Common Mistakes When Interpreting Red Flags

Organizations often stumble in predictable ways. They investigate one alert in isolation instead of correlating it with others. They rely on quarterly audits instead of continuous monitoring. They trust approval workflows without verifying whether approvers actually reviewed the underlying data. They assume that because an ERP has permissions, those permissions are appropriate. And they treat master data changes as administrative rather than financial events. Each of these assumptions creates blind spots that sophisticated fraud schemes are designed to exploit. Effective detection requires connecting small signals into a complete picture, not evaluating them one at a time.

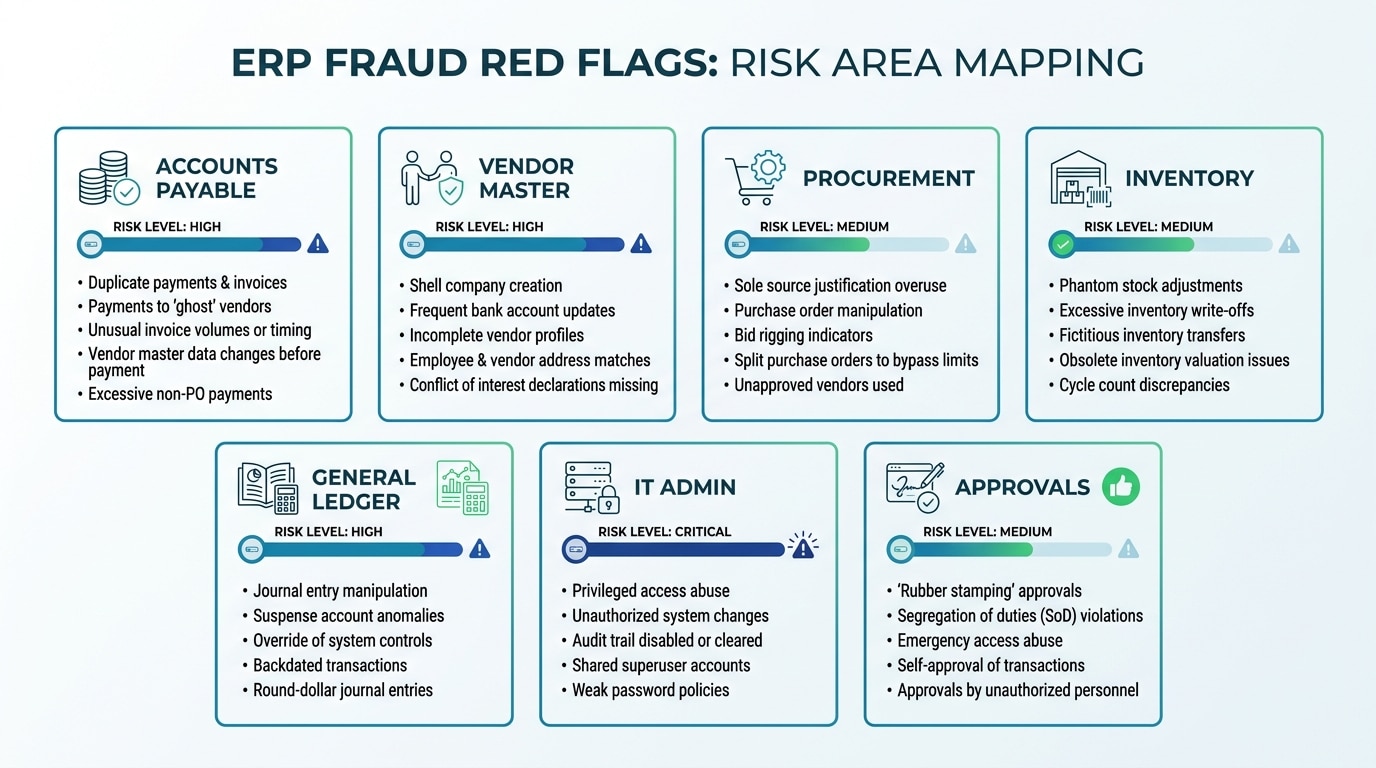

ERP Fraud Red Flags by Risk Area

The table below maps common red flags to the ERP module where they appear, the relative risk level, and the recommended first action. It is designed as a practical reference for finance, audit, and operations teams building their monitoring priorities.

| System Module | Red Flag | Risk Level | Recommended Action |

|---|---|---|---|

| Accounts Payable | Duplicate invoices or near-identical amounts | High | Cross-check vendor, amount, and invoice number; review approver |

| Vendor Master | Bank account change close to payment run | High | Verify change with independent source before release |

| Procurement | Split orders below approval threshold | Medium | Aggregate by vendor and requester; review pattern |

| Inventory | Recurring write-offs or count gaps | Medium | Reconcile physical vs. system; review adjusting user |

| General Ledger | Manual entries outside business hours | High | Review justification, supporting docs, and user role |

| IT / Admin | Shared logins or dormant active accounts | High | Disable, review access history, enforce unique IDs |

| Approvals | Repeated use of override or emergency flags | Medium | Analyze override frequency by user and amount |

Building a Monitoring Framework That Actually Works

Detecting warning signs of ERP fraud consistently requires moving beyond periodic sampling to continuous controls monitoring. A practical framework starts with mapping the organization’s highest-risk processes — payments, vendor changes, journal entries, inventory adjustments, and privileged access — and defining what “normal” looks like for each. From there, thresholds and behavioral baselines are set, and deviations generate alerts that are triaged by severity. Every alert should produce a documented outcome: cleared, escalated, or investigated. This is where automated tools change the equation. Detelix cross-checks sensitive ERP actions in real time, correlates signals across modules, and alerts the right people before money leaves the organization — not weeks later during an audit.

How Detelix Supports Real Control

The table below maps common business needs to how a real-time control layer supports them in practice. The goal is not to replace internal controls but to reinforce them where routine reviews cannot keep up.

| Business Need | How a Real-Time Control Layer Helps |

|---|---|

| Prevent fraudulent vendor payments | Cross-checks bank changes, duplicate vendors, and payment timing automatically |

| Enforce segregation of duties | Flags users who perform conflicting actions across vendor, invoice, and payment |

| Monitor privileged access | Tracks admin activity, unusual logins, and off-hours behavior continuously |

| Detect procurement manipulation | Identifies split orders, threshold avoidance, and single-vendor concentration |

| Strengthen audit readiness | Maintains a continuous, documented trail of exceptions and resolutions |

Key Metrics to Track on an Ongoing Basis

A strong monitoring program tracks measurable indicators, not just incidents. Useful KPIs include the ratio of manual to automated journal entries, the frequency of vendor master data changes per month, the number of payments released within 24 hours of a bank account change, the percentage of transactions approved under override or emergency flags, and login activity outside standard business hours. Trends matter more than isolated spikes. A steady rise in manual entries from one team, or a slow drift in override usage, often reveals more than a single dramatic event.

Did You Know

In many long-running fraud schemes, the earliest detectable signal was not a suspicious transaction — it was a gradual, unexplained increase in override usage or manual journal entries by a single user over several months before the first loss occurred.

Responding When a Red Flag Appears

When a credible indicator surfaces, the response should be structured and discreet. First, preserve logs, user activity records, and supporting documents before anything changes. Second, confirm the facts by comparing ERP data with independent sources such as bank records or original vendor correspondence. Third, limit further exposure — which may mean temporarily restricting a user’s access or pausing a payment. Fourth, escalate through the defined internal channel: audit, compliance, legal, or executive leadership. Avoid early accusations; the goal at this stage is clarity, not conclusion. A calm, documented response protects both the organization and the individuals involved until facts are established.

Tip

Before acting on a suspected fraud signal, export and secure a snapshot of the relevant ERP logs — user activity, approval history, and master data change history. Evidence collected after a user is alerted is often compromised.

Reducing ERP Fraud Risk Before It Starts

The most effective way to handle red flags is to make them less likely in the first place. That means designing controls into the process rather than bolting them on afterward: enforced segregation of duties, tight permission reviews, mandatory dual verification for sensitive changes, and automated cross-checks on payments and master data. It also means cultivating a culture where employees understand that transparency is protective, not punitive. When prevention, detection, and response work together — supported by real-time visibility — fraud becomes significantly harder to commit and far easier to catch early.

Detelix ERP Control & Fraud Prevention Solutions

Proactive Monitoring

Continuous oversight of sensitive ERP activity — vendor changes, payments, and journal entries — so anomalies surface as they happen, not at audit time.

Real-Time Alerts

Immediate, prioritized notifications on high-risk patterns — bank account changes before payments, split orders, off-hours GL entries — routed to the right owner.

Gatekeeper Controls

Preventive checks that block or pause suspicious transactions before funds move, enforcing segregation of duties across vendor, invoice, and payment actions.

Proven Experience

Years of hands-on implementation across finance, healthcare, and enterprise ERPs — translating complex control requirements into practical, continuous oversight.

See Detelix in Action

Frequently Asked Questions

What is the difference between an ERP error and a fraud signal?

An error is typically isolated, random, and easy to explain. A fraud signal tends to repeat, cluster around specific users or vendors, and lack a clear business reason. Pattern, intent, and benefit are the key differentiators.

How often should internal audits check for red flags?

Periodic audits remain important, but continuous monitoring is the modern standard. High-risk areas such as payments, vendor changes, and privileged access should be monitored in real time rather than quarterly.

Can real-time alerts prevent ERP fraud before it happens?

Yes. When alerts fire during the action — for example, when a payment is about to release after a recent bank change — teams can intervene before funds leave the organization, rather than investigating after the loss.

What are the most common behavioral red flags in employees using ERP?

Repeated activity outside business hours, reluctance to take leave, resistance to role rotation, unusual interest in vendor relationships, and a pattern of exceptions centered on one user are among the most frequently observed behavioral indicators.

Is a bank account change always a red flag?

Not always, but it is always worth verifying. The risk rises significantly when the change occurs close to a payment, is requested via an unusual channel, or lacks independent documentation.

How many red flags should trigger a formal investigation?

There is no fixed number. One high-severity indicator may be enough; several medium-severity indicators clustered around the same user, vendor, or process usually justify a deeper review.

Ready to Strengthen Control Over Your ERP?

If most red flags are still detected after the fact, critical risks may be slipping through right now. Move from routine reviews to real-time visibility with Detelix.