Stop B2B Payment Fraud Before It Reaches Your Bank Account

Detelix monitors every sensitive action inside your ERP in real time — from vendor bank changes to payment releases. Get a free security assessment today.

- What Defines B2B Payment Fraud in the Digital Age?

- Why Is Business Email Compromise the Silent Killer of AP?

- How Does Bank Account Change Fraud Bypass ERP Controls?

- A Scenario Every CFO Should Run Through

- Detecting Invoice Fraud: Duplicates to Fictitious Billing

- Is Your Vendor Onboarding Process a Security Loophole?

- Comparing Common B2B Payment Fraud Types

- How Does AI Strengthen Payment Fraud Detection?

- Building Segregation of Duties That Actually Works

- What Mistakes Do Finance Teams Keep Making?

- How Detelix Addresses Key Business Needs

- Securing Access, Identity, and Permissions

- Measuring What Matters: KPIs for Fraud Protection

- How to Measure the ROI of Fraud Protection

- Training Your Team to Recognize Social Engineering

- Is Your Organization Truly in Control of Its Payments?

- Frequently Asked Questions

In many organizations, financial controls appear robust on the surface. Approval workflows exist, ERP permissions are configured, segregation of duties policies are documented, and periodic reconciliations occur on schedule. Yet every year, businesses across every sector lose significant sums to payment fraud that slips through these very controls. The core challenge is not a lack of rules — it is a lack of real-time visibility into what is actually happening inside sensitive payment processes. B2B payment fraud protection is a foundational layer that determines whether your organization truly controls its outgoing cash or merely believes it does.

Key Takeaways

- B2B payment fraud encompasses internal manipulation, business email compromise, vendor master data corruption, and fictitious invoicing — not just external cyberattacks.

- The most dangerous frauds bypass standard ERP approval workflows by corrupting upstream data such as vendor bank account details.

- Effective protection requires both preventive controls (blocking fraud before execution) and detective controls (identifying anomalies in real time).

- Continuous, automated monitoring of every sensitive action from vendor onboarding to payment release replaces the illusion of control with actual control.

- Measuring KPIs like Mean Time to Detect (MTTD), false positive rate, and bank detail verification rate quantifies your fraud protection effectiveness.

What Defines B2B Payment Fraud in the Digital Age?

B2B payment fraud is not limited to external hackers breaching a firewall. In practice, it encompasses any scenario where money leaves your organization under false pretenses — whether triggered by a manipulated invoice, a compromised email thread, an altered bank account in your vendor master file, or an internal employee exploiting weak process controls. The scope of corporate payment security therefore extends well beyond cybersecurity. It covers process integrity, data accuracy, authorization controls, and behavioral monitoring.

Tip

Map every touchpoint in your payment lifecycle — from vendor creation to final bank transfer — and identify which steps rely on a single person’s judgment without independent verification. Those are your highest-risk points.

A useful distinction to keep in mind: payment fraud prevention refers to the controls and procedures that stop fraudulent transactions before they execute — such as dual authorization for bank account changes or automated three-way matching. Payment fraud detection, on the other hand, identifies suspicious patterns in real time or near-real time so your team can investigate and intervene. The most effective B2B payment fraud protection programs combine both: preventive controls that reduce the attack surface and detective controls that catch what prevention misses.

Why Is Business Email Compromise the Silent Killer of Accounts Payable?

Business Email Compromise (BEC) remains the single most financially damaging attack vector for B2B payments worldwide. The reason is straightforward: BEC does not require any malware, any system vulnerability, or any technical sophistication. It exploits human trust. An attacker impersonates a vendor, a CFO, or a trusted business partner — often through a near-identical email domain — and requests a change to payment details or an urgent wire transfer. By the time the finance team realizes the payment went to a fraudulent account, the funds have typically been moved beyond recovery.

Did You Know

The Bank of Israel has issued public warnings about impersonation-based fraud across phone, text, and email channels, highlighting how widespread social engineering techniques have become in the Israeli financial ecosystem.

BEC attacks targeting AP departments often combine urgency (“the payment is overdue”), authority (“the CEO approved this”), and subtle detail changes (a new IBAN, a different beneficiary name) to bypass manual review. The attacker relies on the fact that busy finance teams process dozens or hundreds of payments weekly and cannot scrutinize every detail with equal rigor.

Which Red Flags Should Immediately Halt a Payment?

Finance teams should treat the following as non-negotiable stop signals: a request to change vendor bank details that arrives alongside pressure for immediate payment; an invoice bearing correct company details but a new or unfamiliar destination account; a shift in the vendor’s contact email address or phone number shortly before a payment request; and any instruction to bypass standard approval steps “just this once.” Each of these scenarios warrants out-of-band verification — meaning a phone call to a known, pre-registered contact number, not a reply to the suspicious email thread.

Tip

Maintain a verified contact registry for every active vendor. When a bank detail change request arrives, always verify through the pre-registered phone number on file — never through contact details provided in the change request itself.

How Does Bank Account Change Fraud Bypass Traditional ERP Controls?

One of the most dangerous blind spots in corporate payment security is the vendor master data update process. In many ERP environments, changing a vendor’s bank account details is treated as an administrative task — handled by a single clerk, approved with minimal scrutiny, and executed without any downstream alert. The fraud is elegant in its simplicity: once the bank account in the master file points to an attacker’s account, every subsequent “legitimate” payment to that vendor flows directly to the wrong destination.

This means the vulnerability is not in the payment itself. The payment passes every approval check because it matches a valid purchase order and a valid invoice. The corruption happened upstream, in the master data layer. Many organizations fail to recognize the hidden risks of verifying a supplier’s bank account manually, which often leaves gaps that social engineering exploits with ease.

Did You Know

Vendor master data changes are responsible for a disproportionate share of B2B payment fraud losses because the corrupted data causes every subsequent payment to flow to the wrong account — not just one transaction, but potentially months of payments before detection.

What Controls Should Govern Every Bank Detail Change?

Effective protection requires treating every bank account modification as a high-risk event. This means enforcing segregation of duties between the person requesting the change and the person approving it. It means implementing a mandatory “cooling period” before any payment is released to a newly updated account. It means requiring ownership verification — ideally through an independent channel such as a bank confirmation letter or a direct call to the vendor’s finance department using a number on file before the change request arrived. And it means maintaining a complete audit trail: who requested, who approved, which channel was used for verification, and when.

A Scenario Every CFO Should Run Through: The Friday Afternoon Wire

Consider this realistic scenario. It is Friday at 14:00. A finance clerk receives an email from what appears to be a long-standing vendor, informing them of a “bank migration” and requesting that the next scheduled payment — due Monday — be sent to a new account. The email includes a signed letter on the vendor’s letterhead and a sense of urgency: “Please update before the weekend so the payment is not delayed.” The clerk updates the master file, the payment runs on Monday morning through the normal batch, and the funds reach a fraudulent account in a foreign jurisdiction.

This is not a hypothetical exercise. It is a pattern that repeats across organizations of every size. The control that would have stopped it is not more training alone — it is real-time monitoring that flags any master data change to a bank account field and triggers a structured verification workflow before payment execution. This is precisely the type of control that platforms like Detelix are designed to enforce automatically within the ERP environment, providing the CFO with immediate visibility into sensitive changes rather than discovering them during a monthly reconciliation.

Tip

Implement a mandatory 48-hour cooling period for any newly changed bank account before releasing payments. This single control would have prevented the Friday Afternoon Wire scenario entirely by creating a buffer for verification.

Detecting Invoice Fraud: From Duplicates to Fictitious Billing

Invoice fraud takes many forms. At the simpler end, it involves duplicate invoices — the same service billed twice, sometimes with a slightly altered invoice number. At the more sophisticated end, it involves entirely fictitious vendors created within the ERP by an internal employee who then submits invoices for services never rendered. Between these extremes lie inflated invoices, invoices for partial deliveries billed as complete, and invoices from shell companies controlled by insiders.

The economic impact of fictitious invoices is significant enough that Israel’s State Comptroller has published dedicated audit reports on the phenomenon, and the Israel Tax Authority has introduced the “Invoice Israel” allocation number system to help organizations verify that invoice details match the vendor’s official tax reporting. This digital verification framework, with expanding thresholds taking effect in 2026, reflects a regulatory recognition that manual invoice review is no longer sufficient.

Did You Know

Israel’s “Invoice Israel” system assigns allocation numbers to invoices above certain thresholds, enabling buyers to verify that the invoice was legitimately issued and reported to the Tax Authority — a powerful tool against fictitious billing that many organizations have yet to fully integrate into their AP workflows.

When Is It a Mistake and When Is It Fraud?

Distinguishing between human error and deliberate fraud matters for your response protocol. An honest mistake typically shows a one-time pattern, the vendor cooperates fully when contacted, and supporting documentation exists. Fraud, by contrast, tends to involve urgency, inconsistencies in payment details, resistance to verification, and sometimes a repeating pattern across multiple invoices or periods. Your payment fraud detection software should flag both — but the escalation path for each should differ.

Is Your Vendor Onboarding Process a Security Loophole?

The payment lifecycle does not begin with the invoice. It begins with vendor onboarding — the moment a new supplier enters your system. If fraudulent or inaccurate data enters the vendor master file at this stage, every subsequent control operates on a corrupted foundation. Effective onboarding requires a structured KYB (Know Your Business) process that validates the entity’s legal registration, verifies the ownership of the declared bank account, and confirms the identity of authorized contacts through independent channels.

Organizations operating in Israel can leverage official systems such as System 1000 from the Israel Tax Authority to verify a vendor’s tax deduction rates and bookkeeping status before the first payment is ever made. This kind of structured, data-driven onboarding reduces the risk that a fraudulent entity — or a legitimate vendor with compromised details — enters your payment ecosystem undetected.

Tip

Before activating any new vendor in your ERP, require independent verification of their bank account ownership through a micro-deposit test or a signed bank letter. Never rely solely on details provided by the vendor themselves during onboarding.

Comparing Common B2B Payment Fraud Types: A Practical Reference

| Fraud Type | Attack Vector | Primary Target | Key Preventive Control |

|---|---|---|---|

| Business Email Compromise (BEC) | Social engineering via email impersonation | AP clerks, finance managers | Out-of-band verification for any payment detail change |

| Bank Account Change Fraud | Vendor master data manipulation | ERP master file administrators | Dual approval + cooling period + ownership verification |

| Duplicate / Fictitious Invoices | Submission of false or repeated billing | Invoice processing teams | Automated 3-way match + duplicate detection rules |

| Account Takeover (ATO) | Credential theft (phishing, brute force) | ERP user accounts with payment authority | MFA + anomalous login detection + RBAC enforcement |

| Ghost Vendor | Internal creation of fictitious supplier | Vendor master file + procurement | Periodic vendor audits + segregation of onboarding duties |

Your ERP approval workflows alone cannot catch upstream data corruption or behavioral anomalies. Detelix adds the independent monitoring layer your finance team needs.

How Does AI Strengthen Payment Fraud Detection Software?

Rule-based controls are essential but inherently limited. They catch what you already know to look for. AI and behavioral analytics add a layer that identifies anomalies you have not yet defined as rules — a vendor that suddenly invoices twice in one week when the historical pattern is monthly, a payment released at an unusual hour by a user who has never processed that vendor before, or a subtle shift in invoice formatting that correlates with known fraud patterns.

The practical value of AI in payment fraud detection software lies in its ability to process thousands of transactions simultaneously and surface the small number that warrant human review. However, for AI-driven alerts to be actionable, they must be explainable. Finance professionals need to understand why a transaction was flagged — not just that it was flagged. Detelix addresses this by providing clear, context-rich alerts that connect the anomaly to specific data points, enabling finance teams to make fast, informed decisions rather than drowning in opaque risk scores.

Did You Know

Behavioral analytics can detect fraud patterns that no human auditor would catch in batch review — such as a vendor whose invoicing frequency gradually increases by 5% each quarter, a pattern invisible in individual transactions but clearly anomalous over time.

Reducing False Positives Without Reducing Protection

A common concern with automated detection is alert fatigue. If the system generates too many false positives, the team begins to ignore alerts — which defeats the purpose entirely. Effective approaches include dynamic thresholds that adjust by vendor category or transaction type, graduated verification (requesting additional confirmation rather than blocking outright), and closed-loop feedback where the outcome of each investigation trains the model to improve future accuracy.

Building Segregation of Duties That Actually Works

Segregation of duties (SoD) is a foundational control principle, but its effectiveness depends entirely on implementation. In theory, no single individual should be able to create a vendor, approve an invoice, and release a payment. In practice, many ERP environments contain conflicting permissions that have accumulated over years of role changes, temporary access grants, and organizational restructuring. The result is that SoD exists on paper but is routinely violated in the system.

Tip

Run a quarterly SoD conflict scan across your ERP and compare results against your documented policy. If the gap between documented policy and actual system permissions is growing, you have a systemic governance issue that needs immediate attention.

Continuous monitoring of SoD conflicts — not just periodic access reviews — is what separates real control from the illusion of control. A platform that cross-checks every sensitive action against defined SoD policies in real time can alert management the moment a conflict occurs, rather than months later during an internal audit. This is one of the core capabilities that organizations gain when deploying Detelix across their ERP environment: automated, always-on enforcement of separation rules that would otherwise depend on manual oversight.

What Mistakes Do Finance Teams Keep Making?

Several recurring errors consistently undermine B2B payment fraud protection, even in otherwise well-managed organizations. First, relying on email as the verification channel for bank detail changes — the same channel that may already be compromised. Second, treating vendor master data changes as low-risk administrative tasks instead of high-risk events requiring the same scrutiny as payment approvals. Third, conducting access reviews on an annual cycle when permissions change monthly. Fourth, assuming that ERP approval workflows alone constitute sufficient control, without any independent monitoring layer.

Did You Know

Organizations that conduct access reviews only once per year accumulate an average of 11 months of undetected SoD conflicts between reviews — meaning that for most of the year, their documented controls do not match their actual system state.

These are not technology failures. They are process and mindset gaps. Closing them requires a deliberate shift from point-in-time auditing to continuous, real-time oversight — and a willingness to treat payment security as an ongoing operational discipline rather than a compliance checkbox.

How Detelix Addresses Key Business Needs in Practice

| Business Need | How Real-Time ERP Monitoring Helps |

|---|---|

| Detecting unauthorized bank account changes | Automatic alert the moment a bank detail field is modified, with full context on who changed it and whether proper authorization occurred |

| Preventing duplicate or fictitious invoices | Cross-referencing invoice data (number, amount, IBAN, date) against historical records to flag anomalies before payment |

| Enforcing segregation of duties | Continuous SoD conflict detection across vendor creation, invoice approval, and payment release |

| Identifying unusual payment patterns | Behavioral analytics that surface deviations from established vendor/transaction norms |

| Maintaining a complete audit trail | Every flagged event, investigation, and resolution documented automatically for internal and external audit readiness |

Beyond fraud prevention, real-time monitoring platforms also help finance teams monitor pricing and discounts to prevent revenue leakage that often goes unnoticed in high-volume transaction environments.

Securing Access, Identity, and Permissions Across the Payment Lifecycle

Account takeover (ATO) is an increasingly common precursor to B2B payment fraud. If an attacker gains access to an ERP user account with payment authority, they can modify vendor data, approve invoices, and release payments — all under the guise of a legitimate user. The defense against ATO requires multi-factor authentication (MFA), role-based access control (RBAC) with the principle of least privilege, regular access certification, and monitoring for anomalous login behavior such as connections from unfamiliar devices or locations followed by a sensitive action.

Tip

Configure your ERP monitoring to flag any sequence where a login from a new device or IP address is followed within 30 minutes by a bank account change or a payment above your defined threshold. This pattern is a strong indicator of account takeover.

Identity and access controls are not just IT hygiene — they are a critical payment security layer. Every organization should treat a login from a new device followed by a bank account change or a large payment release as a high-priority alert, not a routine event.

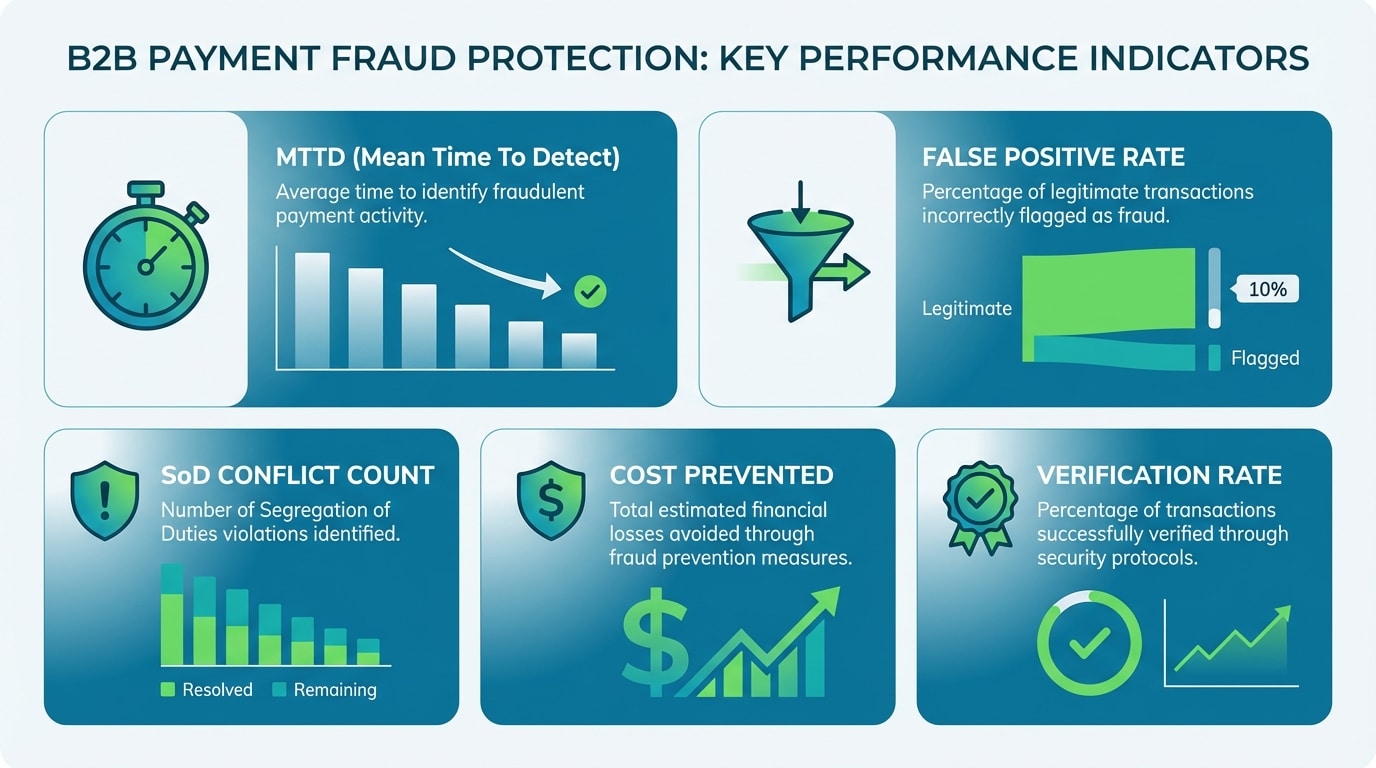

Measuring What Matters: KPIs for B2B Payment Fraud Protection

| KPI | What It Measures | Why It Matters |

|---|---|---|

| Mean Time to Detect (MTTD) | Average time between a fraudulent or suspicious action and its identification | Shorter MTTD directly reduces financial loss and increases recovery probability |

| False Positive Rate | Percentage of alerts that turn out to be legitimate after investigation | High rates cause alert fatigue; target below 20% for actionable programs |

| SoD Conflict Count | Number of active segregation-of-duties violations in the ERP at any point | Persistent conflicts signal systemic control weaknesses |

| Bank Detail Change Verification Rate | Percentage of vendor bank changes verified through an independent channel before payment | Should be 100% for effective fraud prevention |

| Cost of Fraud Prevented | Total value of payments stopped or recovered due to detection controls | Core ROI metric for justifying investment in detection systems |

How to Measure the ROI of Your Fraud Protection Investment

Finance leaders frequently ask whether the cost of a payment fraud detection system can be justified. The answer lies in a straightforward comparison: the cost of a single undetected fraudulent payment — including the lost principal, the investigation effort, the legal fees, and the reputational damage — versus the annual cost of an automated monitoring platform. In most mid-to-large organizations, a single prevented incident covers several years of system investment.

Did You Know

The average cost of a single successful B2B payment fraud incident — including direct losses, investigation, legal fees, and remediation — often exceeds three to five years of investment in an automated detection platform, making the ROI case strongly positive after just one prevented event.

But ROI extends beyond fraud events alone. Automated monitoring reduces the manual workload of AP and finance teams by eliminating repetitive verification tasks. It accelerates audit preparation by providing a continuous, documented control record. And it improves process discipline across the organization by making every sensitive action visible and accountable in real time. These operational efficiencies compound over time, making the investment case increasingly favorable the longer the system is in place.

Training Your Team to Recognize Social Engineering in Payment Contexts

Technology alone does not eliminate fraud risk. People remain both the strongest defense and the most exploitable vulnerability. Effective training programs go beyond annual compliance slideshows. They simulate realistic scenarios — a BEC email requesting a bank detail change, a phone call from someone claiming to be a vendor’s new finance director, a spoofed portal login page. The goal is not to create paranoia but to build instinctive verification habits.

Tip

Run quarterly simulated BEC exercises targeting your AP team. Track response rates over time. Organizations that conduct regular simulations reduce successful social engineering attacks by a measurable margin within the first year.

Organizations should establish clear escalation protocols: if an employee suspects a fraudulent request, they should know exactly who to contact, how to verify independently, and that they will not be penalized for delaying a payment to perform due diligence. This cultural element — where caution is rewarded rather than seen as an obstacle — is what separates organizations that catch fraud early from those that discover it in their quarterly reconciliation.

Is Your Organization Truly in Control of Its Payments?

The distance between believing your payments are secure and actually knowing they are secure is measured in visibility, speed, and independence of oversight. If your controls rely primarily on manual review, periodic audits, and the assumption that approval workflows will catch everything, you may be operating with a gap that only becomes visible after a loss. Real-time, automated monitoring of every sensitive action within your payment processes — from vendor onboarding to bank detail changes to payment release — is what transforms the illusion of control into actual control. Achieving effective protection against embezzlement and fraud errors requires more than policy documents — it demands continuous, automated oversight across every stage of the payment lifecycle.

Detelix Fraud Prevention Solutions

Proactive Monitoring

Continuous surveillance of your ERP environment to detect unauthorized changes, policy violations, and suspicious activities before they result in financial loss.

Real-Time Alerts

Instant notifications when high-risk events occur — bank detail changes, SoD conflicts, unusual payment patterns — so your team can act before damage is done.

Gatekeeper

Automated enforcement of verification workflows for sensitive master data changes, ensuring no payment is released to unverified bank accounts.

Experience & Expertise

Decades of combined expertise in ERP security, internal audit, and financial controls — translating deep domain knowledge into practical, deployable protection.

See Detelix in Action

Frequently Asked Questions

Does B2B payment fraud protection only apply to large enterprises?

No. Mid-sized organizations are often more vulnerable because they process significant payment volumes with smaller finance teams and fewer layers of control. Automated monitoring scales to fit the complexity and volume of any organization, making it relevant regardless of company size.

How long does it take to implement a payment fraud detection platform?

Implementation timelines vary based on ERP complexity and the number of processes being monitored. Many organizations achieve initial coverage of their highest-risk processes — such as vendor bank detail changes and payment releases — within weeks rather than months, with broader coverage phased over time.

Can payment fraud detection software integrate with existing ERP systems?

Modern platforms are designed to integrate with major ERP environments including SAP, Oracle, Priority, and others. The monitoring layer operates alongside the ERP without altering existing workflows, reading transaction and master data in real time to flag anomalies.

What is the difference between a payment fraud detection system and an ERP’s built-in approval workflow?

ERP approval workflows enforce predefined authorization steps — such as requiring a manager’s sign-off above a certain amount. A fraud detection system adds an independent analytical layer that cross-checks data across multiple dimensions (vendor history, behavioral patterns, SoD compliance, timing) to identify risks that pass through standard approvals undetected.

How does continuous monitoring differ from periodic internal audits?

Internal audits typically examine a sample of transactions after the fact — weeks or months after they occurred. Continuous monitoring analyzes every transaction as it happens, enabling intervention before money leaves the organization rather than after it has already been lost.

What should we do if we suspect a BEC attack has already succeeded?

Immediately contact your bank to attempt a payment recall. Preserve all related emails, documents, and system logs. Report the incident to the relevant authorities — in Israel, this includes reporting to the National Cyber Directorate and, where applicable, to law enforcement. Then conduct a thorough review of all recent vendor data changes and pending payments to identify any additional compromised transactions.

Ready to Close the Gaps in Your Payment Security?

Every day without real-time monitoring is another day of exposure. Talk to our team about protecting your organization’s payment processes with continuous, automated oversight.