Transform Your Finance Department into a Proactive Risk Management Powerhouse

Detelix delivers real-time ERP monitoring, automated fraud detection, and continuous controls assurance for CFOs who refuse to wait for the next audit to find problems.

- Why the CFO Has Become the Organization’s Chief Risk Architect

- What Do CFO Risk Management Strategies Actually Include?

- How to Build a Risk Register That Finance Teams Actually Use

- A Common Mistake: Treating All Risks as Equally Urgent

- Defining Risk Appetite in Measurable Terms

- Scenario Planning: Connecting Risk to Budget and Strategy

- How Does a CFO Prevent Payment Fraud Before Money Leaves the Organization?

- Which Internal Controls Matter Most for the Finance Department?

- Implementing SoD Without Paralyzing a Lean Finance Team

- Comparing Financial Risk and Operational Risk

- Liquidity Management: How to Avoid Cash-Flow Surprises

- When Does FX Hedging Make Sense?

- Why the CFO Must Treat Cybersecurity as a Financial Risk

- Does AI Actually Reduce Financial Risk?

- Presenting Risks to the Board

- Which KPIs and KRIs Should a CFO Track?

- Mapping Business Needs to Real-Time Control Capabilities

- Frequently Asked Questions

The modern CFO carries a risk management mandate that extends far beyond quarterly reviews and audit committee presentations. When a single supplier bank-account change slips past manual review, or a payment leaves the organization based on a spoofed email, the gap between perceived control and actual control becomes painfully clear. This article maps out the specific strategies, frameworks, and tools that allow finance leaders to move from reactive reporting to proactive, continuous protection across every critical business process.

Key Takeaways

- The CFO role has evolved into that of a strategic risk architect responsible for fraud prevention, liquidity planning, cybersecurity awareness, and real-time operational oversight.

- Effective risk management requires a living risk register, quantified risk appetite, and layered preventive and detective controls working together continuously.

- Payment fraud prevention demands policy, process, and technology working in tandem — manual reconciliation alone is no longer sufficient.

- Continuous ERP monitoring platforms like Detelix reduce the window between risk occurrence and organizational response from months to minutes.

- Board-level risk communication should be concise and action-oriented, answering what the top risks are, their financial impact, and what decisions are needed.

Why the CFO Has Become the Organization’s Chief Risk Architect

A decade ago, risk management was often delegated to compliance teams or internal audit departments. Today, the CFO sits at the intersection of every data stream that matters: cash flow, vendor payments, payroll, treasury, ERP permissions, and board reporting. That unique vantage point makes the finance leader the natural owner of enterprise-wide risk governance. Regulatory frameworks around the world, including institutional standards for risk governance and oversight, reinforce this expectation by requiring senior financial officers to demonstrate active involvement in identifying, measuring, and mitigating risks across the organization.

The shift is not merely about title or authority. It reflects a practical reality: financial transactions are the earliest signals of operational failure, fraud, or strategic misalignment. A CFO who treats risk management as a core leadership function — rather than a periodic compliance task — gains the ability to detect problems while they can still be prevented, not just reported after the damage is done.

Tip

Schedule a weekly 15-minute review of your top-five risk indicators with your direct reports. Short, frequent conversations build risk awareness far more effectively than quarterly marathon sessions.

What Do CFO Risk Management Strategies Actually Include?

Effective CFO risk management strategies are not a single checklist. They combine four interconnected disciplines: identification, assessment, mitigation, and monitoring. Identification involves mapping every category of exposure — strategic, operational, financial, compliance, and technological. Assessment assigns each risk a likelihood score, a financial-impact estimate, and a speed-of-onset rating. Mitigation selects the right response: prevent, detect, transfer, or accept. And monitoring ensures that controls remain effective over time through continuous measurement and exception reporting.

The framework becomes actionable only when it connects to real business processes. A risk register that sits in a shared drive untouched for six months is not risk management — it is documentation theater. The CFO’s job is to turn that register into a living tool that informs budget decisions, hiring priorities, technology investments, and board-level conversations every quarter.

Did You Know

According to the Association of Certified Fraud Examiners, organizations lose an estimated 5% of revenue to fraud each year. The median loss per fraud case exceeds $117,000, and schemes typically run for 12 months before detection.

How to Build a Risk Register That Finance Teams Actually Use

A practical risk register for a finance department should include, at minimum, the following fields for each identified risk: a clear description, the process owner, trigger events, estimated financial impact range, likelihood rating, existing controls, control effectiveness score, and remediation status. The register should be reviewed monthly — not annually — and updated whenever a new vendor relationship, system change, or regulatory development alters the risk landscape.

The key to adoption is simplicity. If the register requires thirty minutes to update, it will be ignored. If it takes five minutes because the data feeds are automated and the format is consistent, it becomes part of the management routine. Finance leaders who integrate the register into monthly close meetings and quarterly board packages find that risk awareness becomes embedded in the culture rather than bolted on as an afterthought.

Tip

Link each risk register entry to a specific ERP transaction type or process. This makes the register actionable — your team can trace any flagged risk directly to the system behavior that creates the exposure.

A Common Mistake: Treating All Risks as Equally Urgent

One of the most frequent errors in financial risk management is the failure to prioritize. When every risk is flagged as “high,” nothing receives adequate attention. Effective prioritization uses a multi-dimensional lens: financial impact, probability, speed of materialization, and difficulty of detection. A fraud scheme that can drain funds over months without triggering any existing alert deserves a higher priority than a well-monitored foreign-exchange exposure with daily mark-to-market visibility.

CFOs who adopt this layered approach typically identify five to ten “super-risks” for concentrated quarterly attention, while managing the remaining exposures through standard controls and periodic reviews. The discipline of forced ranking prevents resource dilution and ensures that the organization’s limited control budget is deployed where it matters most.

Did You Know

Research from Gartner shows that organizations with a formal risk-prioritization framework detect material control failures 40% faster than those that treat all risks with equal urgency.

Defining Risk Appetite in Measurable Terms

Risk appetite is the amount of volatility an organization is willing to accept in pursuit of its objectives. Too often, this concept remains an abstract boardroom phrase. The CFO’s role is to translate it into specific, measurable thresholds: minimum cash balance, maximum open foreign-currency exposure, cap on single-vendor concentration, tolerance for budget variance, and approval ceilings for non-routine payments.

When risk appetite is quantified, it becomes enforceable. ERP systems can be configured to flag transactions that breach defined limits. Treasury policies can require hedging when exposure exceeds a set percentage of revenue. And board reporting can show, in a single dashboard, whether the organization is operating within or outside its agreed boundaries. This is the difference between managing risk and actually controlling it.

Tip

Express each risk-appetite threshold as a number that can be monitored automatically. “Low tolerance for payment fraud” is a statement; “zero unauthorized vendor bank-account changes per quarter” is a control metric your ERP can enforce.

Scenario Planning: Connecting Risk to Budget and Strategy

Enterprise risk management gains strategic relevance when it is woven into the annual planning cycle. CFOs who build best-case, base-case, and worst-case scenarios for each major budget line create a natural bridge between risk analysis and resource allocation. The question shifts from “What is our revenue target?” to “What is our revenue target under each plausible risk scenario, and what controls protect us if the worst case materializes?”

Institutional guidelines on effective management of climate-related financial risks illustrate this approach well: they require organizations to conduct scenario analyses that stress-test financial assumptions against non-traditional threats. The same logic applies to interest-rate shocks, supply-chain disruptions, or sudden regulatory changes. Embedding scenarios into every budget discussion ensures that risk is not a separate conversation — it is the conversation.

Did You Know

Companies that integrate scenario planning into their annual budgeting process are 2.3 times more likely to meet or exceed financial targets during periods of economic volatility, according to McKinsey research.

How Does a CFO Prevent Payment Fraud Before Money Leaves the Organization?

Payment fraud prevention requires a combination of policy, process, and technology. On the policy side, every supplier bank-account change should require verification through an independent channel — never through the same email thread that requested the change. On the process side, separation of duties must ensure that no single individual can create a vendor, approve an invoice, and release a payment. On the technology side, pattern-recognition systems must flag anomalies — unusual amounts, first-time payees, payments outside business hours, or sudden spikes in transaction volume — before the payment is authorized.

Regulatory expectations reinforce this layered approach. Guidelines on prevention and handling of employee fraud and embezzlement emphasize that organizations must maintain preventive measures, not merely detective ones. Waiting until the monthly reconciliation reveals a discrepancy is too late. The goal is to intercept the irregular transaction in real time, before funds are irrecoverable.

Your organization’s financial controls are only as strong as the weakest manual step in the payment process. Replace guesswork with real-time monitoring.

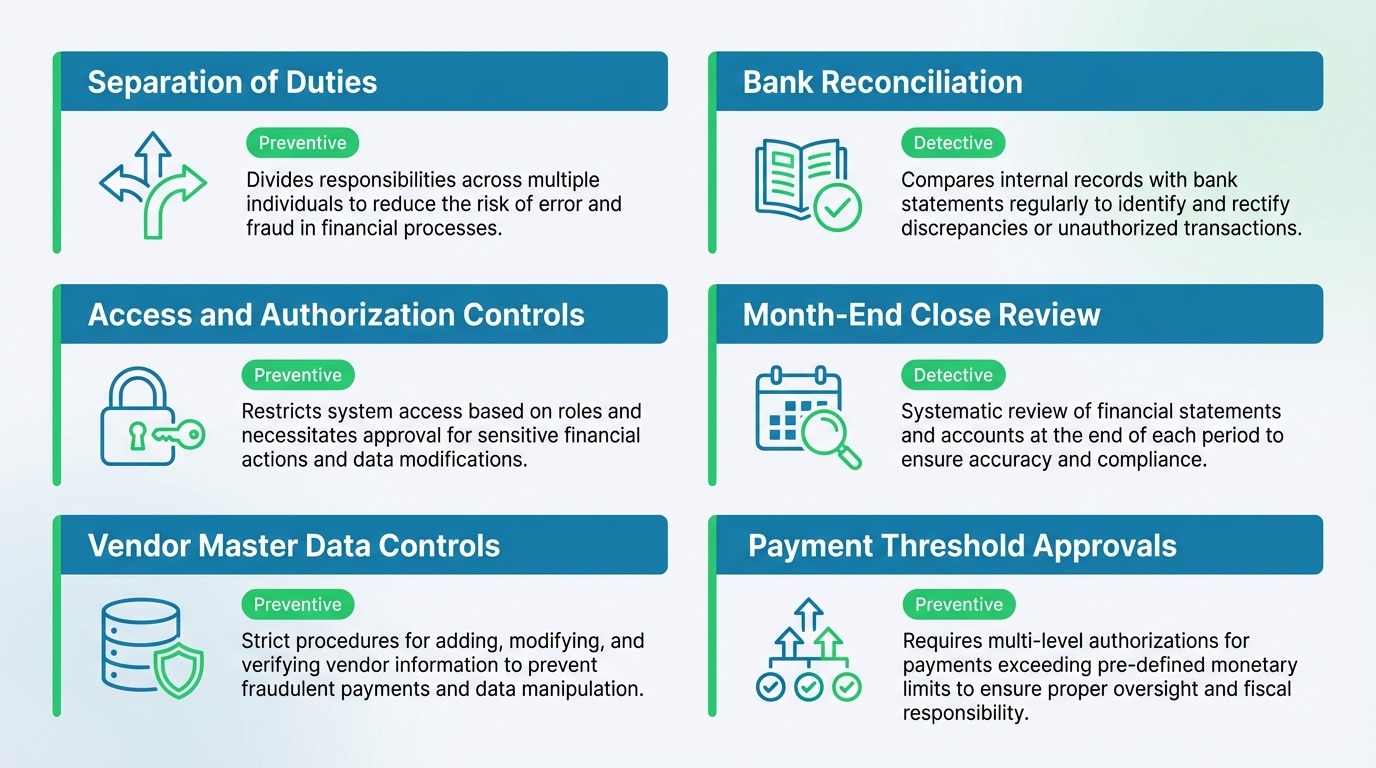

Which Internal Controls Matter Most for the Finance Department?

| Control Area | Control Type | Why It Is Critical |

|---|---|---|

| Separation of Duties (SoD) | Preventive | Eliminates the ability of one person to complete a high-risk process end-to-end |

| Bank Reconciliation | Detective | Identifies unauthorized or erroneous transactions before they compound |

| Access and Authorization Controls | Preventive | Restricts system capabilities to only what each role requires |

| Month-End Close Review | Detective | Catches misstatements, accrual errors, and unusual journal entries |

| Vendor Master Data Controls | Preventive | Prevents creation of fictitious vendors or unauthorized bank-detail changes |

| Payment Threshold Approvals | Preventive | Requires escalation for transactions above defined limits |

The most effective control environments combine preventive and detective controls in layers. A preventive control stops the error or fraud attempt; a detective control catches anything that slips through. When both layers are automated and continuously monitored, the organization moves from periodic assurance to real-time protection — a distinction that matters enormously when the cost of a single undetected payment error can exceed an entire quarter’s control budget.

Implementing SoD Without Paralyzing a Lean Finance Team

Full separation of duties is straightforward in a large corporation with dozens of finance staff. In a mid-market company with five people in the finance department, it requires creative design. The principle remains the same: no single person should control the entire lifecycle of a sensitive transaction. But the implementation may rely on compensating controls — such as mandatory manager review of all payments above a threshold, dual authorization for vendor master changes, or automated alerts when a user performs two conflicting actions within the same process.

Technology plays a decisive role here. Platforms like Detelix can continuously monitor ERP activity and flag SoD violations as they occur, rather than waiting for an annual audit to discover that the same person has been creating vendors and approving their invoices for months. This kind of real-time visibility transforms SoD from a policy document into an active organizational safeguard — especially valuable for growing companies where roles and permissions evolve rapidly.

Tip

Map your five most sensitive transaction flows end-to-end. For each, identify who can initiate, approve, and execute. If any individual appears in two or more of those roles, implement a compensating control immediately — even a simple email-based dual approval adds a meaningful barrier.

Comparing Financial Risk and Operational Risk: Where the CFO’s Attention Should Go

| Dimension | Financial Risk | Operational Risk |

|---|---|---|

| Definition | Exposure to market, credit, liquidity, or interest-rate movements | Exposure to failures in internal processes, people, systems, or external events |

| Examples | FX volatility, rising borrowing costs, customer default | Payment errors, ERP misconfiguration, employee fraud, cyber intrusion |

| Typical Owner | Treasury / CFO | Operations / CFO / CRO |

| Measurement | VaR, sensitivity analysis, stress tests | Loss-event databases, KRI dashboards, incident frequency |

| Control Approach | Hedging, diversification, policy limits | SoD, automation, monitoring, access controls |

In practice, these two categories overlap constantly. A cyber breach (operational risk) can trigger liquidity stress (financial risk). A poorly hedged currency exposure (financial risk) can force emergency cost-cutting that weakens internal controls (operational risk). The CFO who manages both categories in an integrated framework — rather than in separate silos — builds a far more resilient organization.

Did You Know

The Basel Committee on Banking Supervision found that operational risk losses frequently cascade into financial risk events — with 37% of major operational incidents triggering liquidity or credit stress within 90 days.

Liquidity Management: How to Avoid Cash-Flow Surprises

Liquidity risk is the silent threat that can bring down even a profitable company. The 13-week cash flow forecast is one of the most effective tools available. It translates expected collections, scheduled payments, payroll, tax obligations, and debt service into a week-by-week view of available cash. Updated every Monday, compared against actuals every Friday, and refined continuously, it gives the CFO a granular, real-time picture of the organization’s financial runway.

Beyond forecasting, liquidity management requires structural buffers: committed credit lines, minimum-cash policies, and diversified funding sources. Frameworks for liquidity risk management emphasize the importance of stress-testing these buffers under adverse scenarios — what happens if the largest customer delays payment by 60 days, or if a credit facility is unexpectedly withdrawn? CFOs who answer these questions proactively avoid the crisis-mode decision-making that destroys value.

Tip

Build your 13-week cash flow forecast with three scenarios: expected, optimistic, and stressed. Compare actuals against the expected scenario weekly. If actuals consistently track closer to the stressed scenario, escalate to the board before liquidity becomes a crisis.

When Does FX Hedging Make Sense — and When Does It Create More Risk?

Foreign-exchange hedging is appropriate when there is a clear, identifiable cash-flow exposure that can be matched with a defined hedge instrument and horizon. A company that invoices in euros but pays costs in dollars has a natural exposure that benefits from a disciplined hedging program. The policy should specify what percentage of forecasted exposure is hedged, over what time horizon, and which instruments are permitted.

The Difference Between Operational and Financial Hedging

Operational hedging — also called natural hedging — involves structuring the business to reduce exposure without derivatives. Examples include sourcing raw materials in the same currency as revenue, or locating production facilities in the market where goods are sold. Financial hedging uses forwards, options, or swaps to offset residual exposure. The most robust programs combine both approaches, using operational hedging as the first line of defense and financial instruments to manage the remainder within defined risk-appetite limits.

Did You Know

A study by the Journal of Corporate Finance found that firms with formal FX hedging policies experienced 22% less earnings volatility than peers without such policies — yet over-hedging (covering more than 80% of exposure) actually increased risk-adjusted costs for 1 in 4 companies surveyed.

Why the CFO Must Treat Cybersecurity as a Financial Risk

A ransomware attack that halts operations for two weeks is not an IT problem — it is a financial emergency. The direct costs include ransom payments, forensic investigation, legal fees, and regulatory fines. The indirect costs — lost revenue, damaged customer trust, and increased insurance premiums — often exceed the direct costs by a factor of three or more. Standards for managing IT, information security, and cyber protection risks make clear that executive oversight of cyber risk is not optional; it is a governance expectation.

For the CFO, this means ensuring that cyber risk is quantified in financial terms and included in the enterprise risk register alongside credit, market, and liquidity exposures. It also means verifying that access controls within the ERP environment are robust, that payment-related systems have multi-factor authentication, and that incident-response plans include financial containment procedures — not just technical recovery steps.

Tip

Ask your IT security team to quantify the financial impact of three specific cyber scenarios: a ransomware lockout, a business email compromise targeting vendor payments, and an unauthorized data exfiltration. Include those figures in your next board risk report alongside traditional financial exposures.

Does AI Actually Reduce Financial Risk, or Does It Introduce New Blind Spots?

Artificial intelligence can dramatically improve anomaly detection, cash-flow forecasting, and pattern recognition across large transaction volumes. However, it also introduces risks that many organizations underestimate: data-quality dependencies, model bias, lack of explainability, and over-reliance on automated recommendations. A model that flags ninety-eight percent of fraudulent transactions is valuable — until the two percent it misses includes a material loss event that no human reviewed because the team trusted the algorithm.

The CFO’s governance role here is critical. Every AI-driven control should have a defined owner, documented logic, periodic validation, and a clear boundary between “recommendation” and “approval.” The machine can flag, score, and prioritize. The decision to release a payment, approve a vendor, or accept a journal entry must remain with an accountable human — supported by technology, not replaced by it.

Did You Know

A 2024 Deloitte survey found that 61% of CFOs plan to increase AI investment in financial controls, yet only 23% have established formal governance frameworks for AI-driven decisions. This governance gap represents one of the fastest-growing categories of operational risk.

Presenting Risks to the Board: A Format That Drives Decisions

Board members do not need a sixty-page risk report. They need a concise package that answers four questions: What are our top risks right now? What is the estimated financial impact of each? Are our controls working? And what do we need from the board — a decision, a budget allocation, or a policy change? A single-page heat map, a ranked list of five to seven critical risks with status indicators, and a remediation timeline with clear ownership will generate more productive discussion than a dense narrative ever could.

The CFO who masters this communication format builds board confidence and accelerates decision-making. When directors understand risks in business terms — not technical jargon — they can fulfill their oversight function effectively and support the investments in controls, technology, and staffing that the organization actually needs.

Which KPIs and KRIs Should a CFO Track to Measure Control Effectiveness?

Key Performance Indicators measure how well the finance function operates. Key Risk Indicators measure how exposed the organization is to adverse events. Both are necessary. KPIs such as days-to-close, forecast accuracy, and cost-per-transaction tell the CFO whether the team is efficient. KRIs such as the percentage of manual payments, the number of vendor bank-detail changes per month, the count of SoD violations, the aging of unresolved audit findings, and the gap between forecasted and actual cash flow tell the CFO whether the organization is safe.

Platforms designed for continuous controls monitoring can automate KRI collection and present it in real-time dashboards. Detelix, for example, tracks exception patterns across sensitive ERP processes — flagging unusual supplier activity, unauthorized access attempts, and payment anomalies — so that risk indicators are based on actual system behavior, not self-reported assessments. This shifts KRI reporting from a lagging snapshot to a leading signal that enables intervention before losses materialize.

Tip

Establish a “KRI of the Month” spotlight in your management meeting. Each month, select one key risk indicator, present its trend data, discuss what it reveals about control effectiveness, and assign an action item. This builds a risk-aware culture one metric at a time.

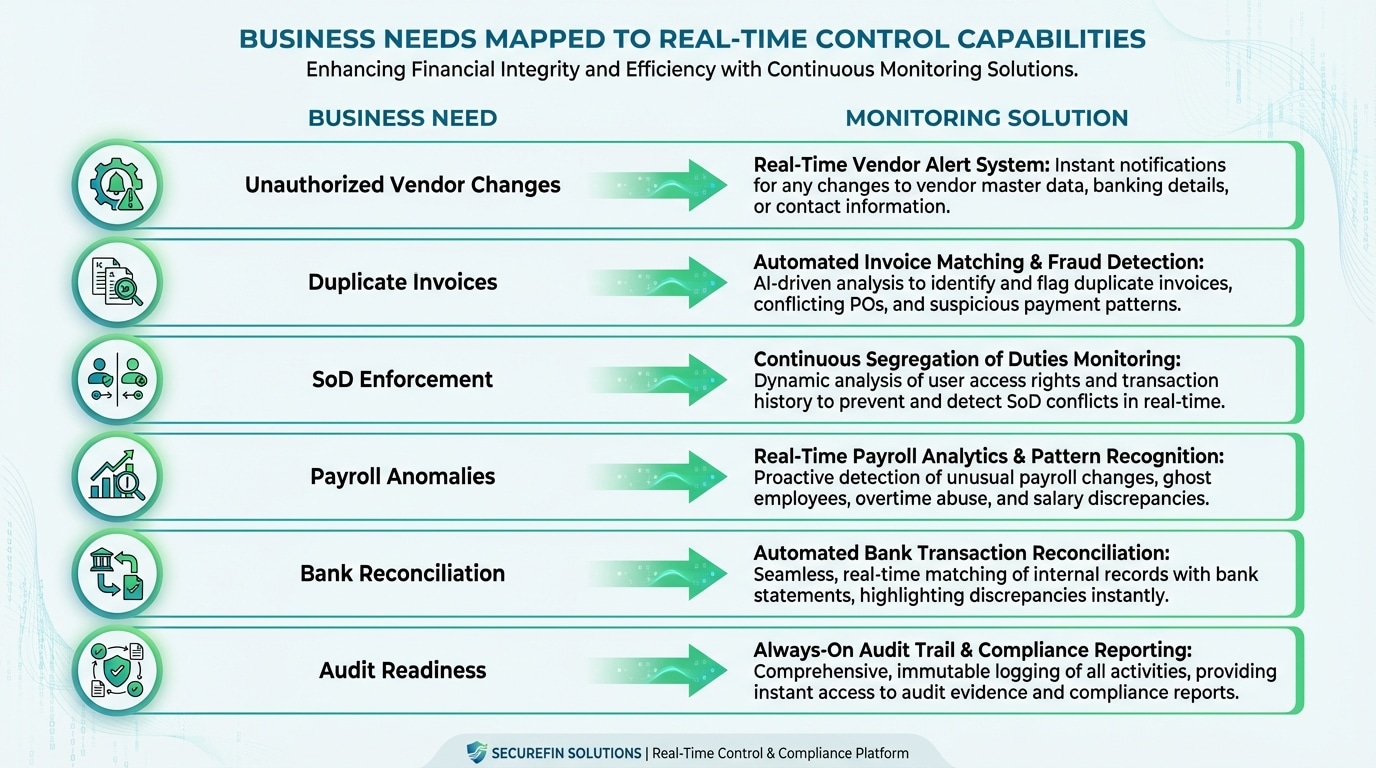

Mapping Business Needs to Real-Time Control Capabilities

| Business Need | How Continuous Monitoring Addresses It |

|---|---|

| Prevent unauthorized vendor bank-account changes | Automatic cross-check of every change against approval records; instant alert on mismatches |

| Detect duplicate or fictitious invoices | Pattern analysis across invoice numbers, amounts, dates, and vendor identifiers |

| Enforce SoD policies in a growing team | Real-time monitoring of user actions within ERP; flag when conflicting roles are exercised |

| Identify payroll anomalies | Comparison of current payroll run against historical baselines; alert on unusual additions or changes |

| Strengthen bank reconciliation | Automated matching of bank transactions to ERP entries; exception list generated daily |

| Support audit readiness year-round | Continuous documentation of control execution, exceptions, and resolutions |

This kind of always-on oversight is precisely what Detelix delivers across ERP-driven financial processes. Rather than relying on quarterly sample testing or manual spreadsheet reviews, finance leaders gain continuous visibility into the transactions and process behaviors that matter most — reducing the window between risk occurrence and organizational response to minutes instead of months.

Detelix Continuous Controls Monitoring Solutions

Proactive Monitoring

Continuous oversight of ERP transactions and financial processes to detect anomalies before they become losses.

Real-Time Alerts

Instant notifications when suspicious activity, SoD violations, or unauthorized changes are detected in your systems.

GateKeeper

Automated enforcement of approval workflows and payment thresholds across your entire vendor and payment lifecycle.

Experience & Expertise

Decades of combined expertise in financial controls, ERP security, and regulatory compliance across multiple industries.

See Detelix in Action

Frequently Asked Questions

What are the top CFO risk management strategies for 2025?

The highest-impact strategies center on automated fraud prevention, real-time ERP monitoring, liquidity stress testing, integrated cyber-financial governance, and structured board communication. CFOs who combine these disciplines create a control environment that is both resilient and adaptive to emerging threats.

How can a CFO prevent payment fraud effectively?

By implementing digital separation of duties, requiring independent verification of every supplier bank-account change, setting automated thresholds that block or escalate unusual payments, and deploying pattern-recognition technology that identifies anomalies before funds are released.

What is the difference between financial risk and operational risk?

Financial risk involves exposure to market movements, credit defaults, liquidity shortfalls, and interest-rate changes. Operational risk involves failures in internal processes, people, systems, or external events — such as payment errors, ERP misconfigurations, or employee fraud. Both categories frequently interact and should be managed within a single integrated framework.

How often should a risk register be updated?

At minimum, monthly — aligned with the financial close cycle. Material changes in the business environment, such as new vendor relationships, system migrations, or regulatory developments, should trigger immediate updates regardless of the regular schedule.

Is automation a risk or a risk-reduction tool?

It is both. Automation dramatically reduces human error, accelerates detection, and enables continuous monitoring at scale. However, it introduces new risks related to data quality, model accuracy, and over-reliance. The key is governance: every automated control must have a human owner, documented logic, and periodic validation.

Ready to Move from Periodic Review to Continuous Protection?

If your organization still depends on quarterly audits and manual reconciliations to catch errors and fraud, the gap between what you know and what is actually happening may be wider than you think. Close that gap with Detelix.