Strengthen Your Financial Controls with Detelix

Real-time ERP monitoring that catches fraud, policy violations, and process failures before they cost you. Talk to our risk management experts today.

- Why Executive Financial Oversight Now Demands Operational Depth

- What Separates ERM from Traditional Financial Risk Management

- How to Define Risk Appetite in Measurable Terms

- Mapping the Top Risk Categories Every CFO Should Prioritize

- Turning a Risk Register into a Decision-Making Tool

- Why Manual Approvals No Longer Stop Fraud in the Procure-to-Pay Cycle

- A Scenario Where Segregation of Duties Failed

- Preventive Controls vs. Detective Controls

- Managing Liquidity Risk When Forecasts Keep Shifting

- Stress Testing: From Model to Action Triggers

- Why Cybersecurity Belongs on the CFO Risk Dashboard

- Connecting Finance and IT to Close the Cyber-Financial Gap

- How Analytics and Automation Replace Periodic Audits

- Common Mistakes CFOs Make When Building a Risk Management Program

- Benchmarks and Tests: Measuring Control Effectiveness

- Frequently Asked Questions

The role of the CFO has expanded far beyond financial reporting and budget management. Effective CFO risk management strategies must now address a spectrum of threats ranging from payment fraud and vendor manipulation to liquidity shocks and cyber breaches, all while enabling growth. Controls that appear robust on paper often fail in practice because they rely on manual reviews, static reports, and after-the-fact investigations. Moving from reactive oversight to proactive, real-time financial leadership risk control is a fundamental requirement for any executive determined to protect profitability and maintain stakeholder confidence in a volatile operating environment.

Key Takeaways

- CFO risk management must extend beyond treasury risks to cover cyber threats, vendor fraud, and operational disruptions that carry severe financial consequences.

- Manual approval workflows cannot keep pace with modern fraud tactics; continuous, automated monitoring closes the detection gap from months to minutes.

- Risk appetite must be translated into quantitative thresholds and Key Risk Indicators (KRIs) that trigger real-time escalation, not just quarterly reports.

- Layering preventive controls with real-time detective controls creates the strongest defense without paralyzing business operations.

- The 13-week rolling cash-flow forecast and scenario-linked stress testing provide the tactical liquidity visibility CFOs need during periods of uncertainty.

- Cybersecurity is a financial risk that belongs on the CFO dashboard, measured with the same rigor as credit or market exposure.

Why Executive Financial Oversight Now Demands Operational Depth

For decades, financial oversight meant reviewing monthly statements, reconciling balances, and signing off on budgets. That model assumed risks would surface in the numbers eventually. The problem is that “eventually” can mean after significant damage has already occurred: an unauthorized vendor payment processed, a duplicate invoice paid, or a liquidity gap that forces emergency borrowing at unfavorable terms.

Modern executive financial oversight requires drilling into the operational data that feeds the financial statements. It means understanding which ERP transactions deviate from normal patterns, which approval workflows are being bypassed, and where master data changes create exposure. When a CFO can see what is happening inside critical processes in real time, decisions shift from damage control to damage prevention.

Tip

Schedule a weekly review of ERP exception reports rather than waiting for month-end close. Even a 30-minute session focused on flagged anomalies can surface issues weeks before they appear in financial statements.

What Separates ERM from Traditional Financial Risk Management

Enterprise Risk Management (ERM) takes a holistic view. It maps risks across the entire organization: operational disruptions, regulatory shifts, reputational threats, cyber incidents, and climate exposure, connecting each to strategic objectives. Traditional financial risk management, by contrast, focuses on treasury-centric exposures such as interest rate fluctuations, foreign exchange, credit risk, and reporting accuracy.

The distinction matters because a CFO who only manages financial risks in the classical sense may miss vulnerabilities that originate outside the finance function but carry severe financial consequences. A supply-chain disruption, a data breach, or a regulatory enforcement action can each drain cash faster than a missed revenue target. Integrating both lenses gives the CFO a complete picture of where the organization is truly exposed.

Did You Know

According to a 2024 Deloitte Global Risk Management Survey, organizations with mature ERM programs reported 25% fewer material financial surprises than those relying solely on traditional financial risk management frameworks.

How to Define Risk Appetite in Measurable Terms

Risk appetite is meaningless if it remains a paragraph in a board presentation. It must be translated into quantitative thresholds and qualitative boundaries that people across the organization can apply in daily decision-making. For a CFO, this means setting specific limits: a minimum cash reserve floor, a maximum single-vendor concentration percentage, a ceiling on unhedged foreign-currency exposure, or a tolerance band for Days Sales Outstanding (DSO).

Each threshold should be paired with a Key Risk Indicator (KRI) that is monitored continuously. Unlike KPIs, which measure performance after the fact, KRIs serve as early-warning signals that a limit is approaching. When a KRI crosses a predefined threshold, it should trigger a review or an escalation rather than just a note in next month’s report.

Tip

Map each risk appetite statement to at least one KRI with a green-amber-red threshold structure. Green means within tolerance, amber means approaching the limit and requiring a review, and red means the limit has been breached and requires immediate escalation.

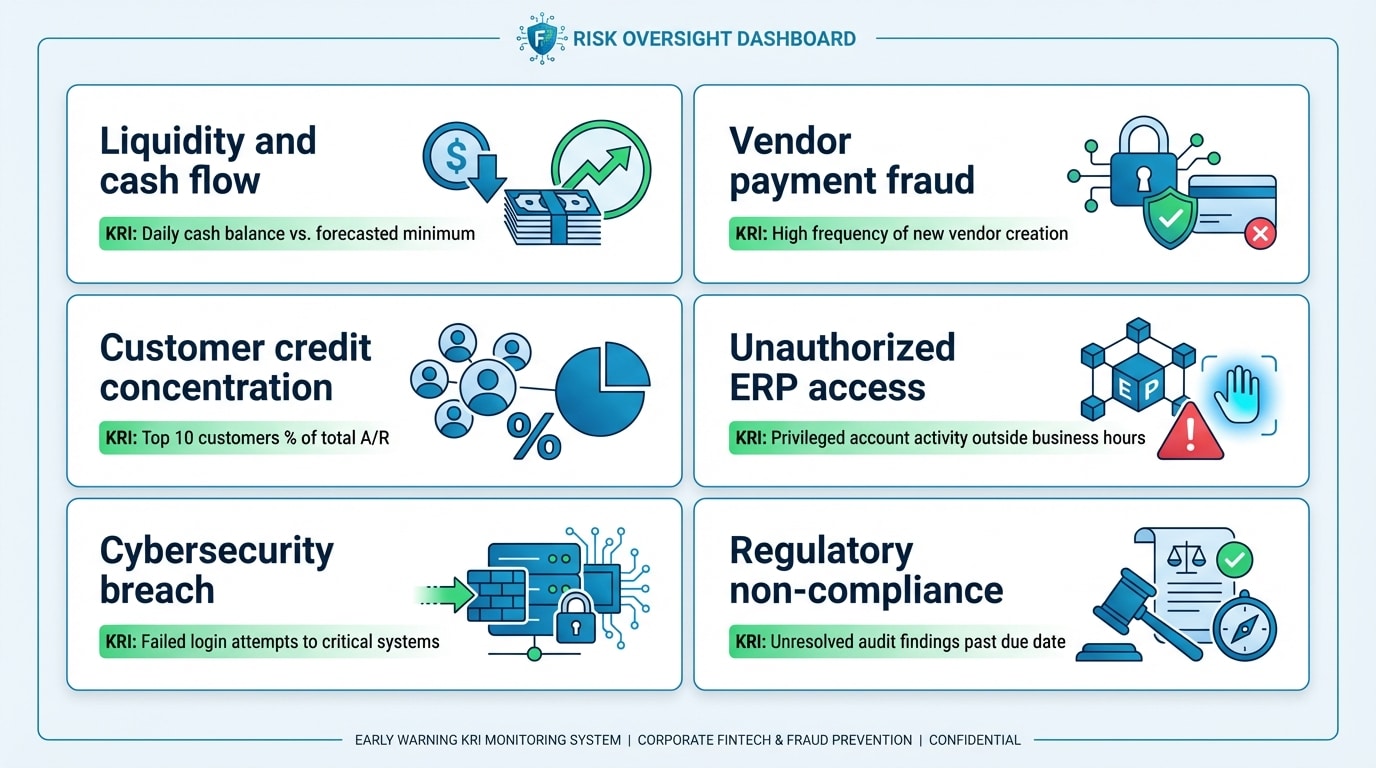

Mapping the Top Risk Categories Every CFO Should Prioritize

Not all risks carry equal urgency. The categories that deserve immediate attention share a common trait: they can impair the organization’s ability to operate or meet obligations quickly. These include liquidity and cash-flow risk, customer credit concentration, vendor payment fraud, unauthorized system access, cybersecurity events, regulatory non-compliance, and over-reliance on a single customer or supplier.

| Risk Category | Why It Is Urgent | Typical Early Warning (KRI) |

|---|---|---|

| Liquidity and cash flow | Directly affects ability to pay obligations | Cash runway drops below 8 weeks |

| Vendor payment fraud | Funds leave the organization irreversibly | Bank-account change requests spike |

| Customer credit concentration | Single default can cause material shortfall | Top-3 customers exceed 40% of revenue |

| Unauthorized ERP access | Enables process bypass and data manipulation | Users with conflicting permissions rise |

| Cybersecurity breach | Operational shutdown, ransom, legal liability | Phishing attempts or access anomalies increase |

| Regulatory non-compliance | Fines, sanctions, reputational damage | Overdue compliance reviews or filings |

A practical enhancement to the classic probability-impact matrix is adding a “velocity” dimension: how fast a risk can materialize. A cyber event, for example, can escalate from incident to crisis within hours, demanding controls that respond at the same speed.

Did You Know

The average time between a vendor bank-detail change and the fraudulent payment being discovered is 47 days, according to the Association of Certified Fraud Examiners. Real-time monitoring can reduce this detection window to seconds.

Turning a Risk Register into a Decision-Making Tool

Many organizations maintain a risk register that gathers dust between annual updates. A useful risk register is a living document reviewed at every leadership meeting. Each entry should include a clear risk description, triggering conditions, the assigned risk owner, existing controls, identified gaps, a remediation plan with cost-benefit justification, and a next-review date.

The key shift is connecting the register to actual resource allocation. If a remediation action has a strong return on investment in terms of risk reduction, it should compete for budget alongside growth initiatives. When the CFO frames risk mitigation as protecting expected returns, the board and management team engage differently.

Tip

Add a “cost of inaction” column to your risk register. Quantifying the financial exposure of leaving a gap unaddressed makes it far easier to justify remediation budgets to the board.

Why Manual Approvals No Longer Stop Fraud in the Procure-to-Pay Cycle

The procure-to-pay (P2P) cycle remains one of the highest-risk areas for CFO fraud prevention. Attackers, whether external or internal, exploit the volume and routine nature of supplier payments. A well-crafted social-engineering email convinces a finance clerk to update a vendor’s bank details. A colluding employee splits invoices to stay below approval thresholds. A duplicate payment slips through because nobody cross-references the purchase order, receipt, and invoice in real time.

Manual approval workflows cannot keep pace with these tactics. They rely on a human reviewer catching an anomaly buried in a batch of hundreds of transactions. This is where continuous, automated monitoring changes the equation. A platform like Detelix operates as an independent control layer above the ERP, scanning every transaction as it occurs. It flags a vendor bank-account change seconds after it is entered, identifies a duplicate invoice before payment is released, and alerts when a purchase order is split to circumvent a threshold. The result is that exceptions surface before money leaves the organization, not after an auditor discovers the discrepancy months later.

Did You Know

Invoice fraud schemes account for roughly 20% of all occupational fraud cases globally, with a median loss of $100,000 per incident. Organizations using continuous transaction monitoring detect these schemes 50% faster than those relying on traditional audit cycles.

A Scenario Where Segregation of Duties Failed

Segregation of Duties (SoD) is a foundational control: no single person should be able to initiate, approve, and execute a financial transaction. In theory, SoD prevents fraud. In practice, it often fails. Super-user accounts accumulate permissions over time. Employees cover for colleagues on leave and receive temporary access that is never revoked. Shared logins obscure who actually performed an action.

Consider a real-world pattern: a finance team member has access to both vendor master data and payment execution. They create a fictitious vendor, submit an invoice, and approve the payment, all within their legitimate system access. Traditional SoD reviews, conducted quarterly or annually, would not detect this until long after the funds were gone. Continuous monitoring that cross-checks every master-data change against payment activity in real time would flag the anomaly immediately.

Your ERP holds the data. Detelix watches it in real time. Detect vendor fraud, SoD violations, and payment anomalies before they become losses.

Preventive Controls vs. Detective Controls

Preventive controls stop a risky action before it completes: approval gates, system-enforced transaction limits, mandatory dual signatures. Detective controls identify problems after they occur: reconciliations, exception reports, audit sampling. Neither type alone is sufficient.

An over-reliance on preventive controls can slow the business to a crawl. An over-reliance on detective controls means losses accumulate before they are found. The optimal approach is a layered model: strong preventive controls for the highest-impact risks, supplemented by real-time detective controls that catch anything that slips through. Platforms such as Detelix strengthen the detective layer by operating continuously rather than periodically, reducing the window between a control failure and its detection from weeks to minutes.

Tip

Audit your current control inventory and classify each control as preventive or detective. If more than 80% of your controls are preventive, you likely have a significant blind spot for risks that bypass those gates.

Managing Liquidity Risk When Forecasts Keep Shifting

Liquidity is the oxygen of any business. When cash runs short, even profitable organizations can fail. During periods of economic uncertainty, rising interest rates, supply-chain disruptions, or geopolitical tension, traditional annual or quarterly cash-flow forecasts become dangerously stale.

The 13-week rolling cash-flow forecast has emerged as the standard tactical tool for chief financial officer risk management. It tracks expected inflows and outflows on a weekly basis, using actual data from accounts receivable, accounts payable, payroll, debt service, and capital expenditures. Each week, the forecast is updated with actuals and the horizon extends by one week. Deviations between forecast and actual are analyzed immediately, revealing whether the variance is a timing issue or a structural problem.

Regulatory frameworks reinforce this discipline. The Bank of Israel’s Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) requirements provide quantitative benchmarks that, while designed for banks, offer a useful reference point for any organization seeking to measure the adequacy of its liquid reserves against short-term and long-term obligations.

Did You Know

Organizations that maintain a 13-week rolling cash-flow forecast are 3x more likely to identify liquidity shortfalls at least 30 days before they materialize, compared to those relying on monthly or quarterly forecasting cycles.

Stress Testing: From Model to Action Triggers

Building scenario models is valuable only if each scenario is linked to a concrete action trigger. A stress test that shows the organization survives a 20% revenue decline is reassuring, but what happens at 30%? More importantly, at what point does leadership activate cost-reduction measures, draw on credit facilities, or defer capital spending?

Effective stress testing defines three to five scenarios (base, moderate stress, severe stress, recovery) and maps each one to specific financial metrics: cash runway in weeks, covenant headroom, EBITDA margin, and debt-service coverage. When a metric breaches a predefined threshold in real life, the corresponding action plan activates automatically. Israel’s State Comptroller has repeatedly emphasized the importance of maintaining financial reserves for emergencies, noting that organizations without pre-committed contingency plans face significantly worse outcomes when crises hit.

Tip

For each stress scenario, pre-approve specific actions at the board level. When conditions deteriorate rapidly, having pre-authorized playbooks eliminates the delays caused by convening emergency meetings and debating options under pressure.

Why Cybersecurity Belongs on the CFO Risk Dashboard

A ransomware attack is not just an IT incident. It is a financial event with quantifiable costs: ransom payments, business interruption losses, forensic investigation fees, legal defense, regulatory fines, and long-term reputational damage that erodes customer trust and revenue. For chief financial officer risk management, this means cyber risk must be measured, budgeted, and monitored with the same rigor applied to credit or market risk.

Practical steps include quantifying maximum financial exposure from a cyber event, ensuring cyber insurance coverage aligns with that exposure, integrating cyber KRIs into the finance risk dashboard (mean time to detect, percentage of critical systems backed up, number of privileged-access accounts), and establishing a clear incident-response protocol that includes financial documentation. Authorities such as Israel’s Privacy Protection Authority require formal reporting of severe security incidents, including detailed logs and evidence, making pre-event preparation a regulatory necessity rather than a best practice.

Did You Know

IBM’s 2024 Cost of a Data Breach Report found that the average total cost of a data breach reached $4.88 million globally. Organizations with an incident response team and tested plans saved an average of $2.66 million per breach compared to those without.

Connecting Finance and IT to Close the Cyber-Financial Gap

The most dangerous cyber-financial vulnerabilities sit at the intersection of finance processes and IT systems: vendor bank-detail changes executed through phishing, unauthorized payment runs triggered by compromised credentials, and ERP data manipulation that distorts financial reporting. The CFO and CISO must collaborate on specific controls: multi-factor authentication for payment approvals, automated alerts when master data changes occur outside normal patterns, and regular reconciliation of ERP access logs against HR records.

Detelix addresses this gap directly by monitoring ERP-level actions, such as changes to supplier bank accounts, creation of new vendors, and unusual payment patterns, independently of the ERP’s own permission structure. This means that even if an attacker gains legitimate credentials, the anomalous behavior is still flagged and escalated.

Tip

Establish a monthly joint review between the CFO and CISO focused exclusively on the intersection of financial processes and IT security. Review vendor master data changes, privileged ERP access logs, and any payment anomalies together rather than in silos.

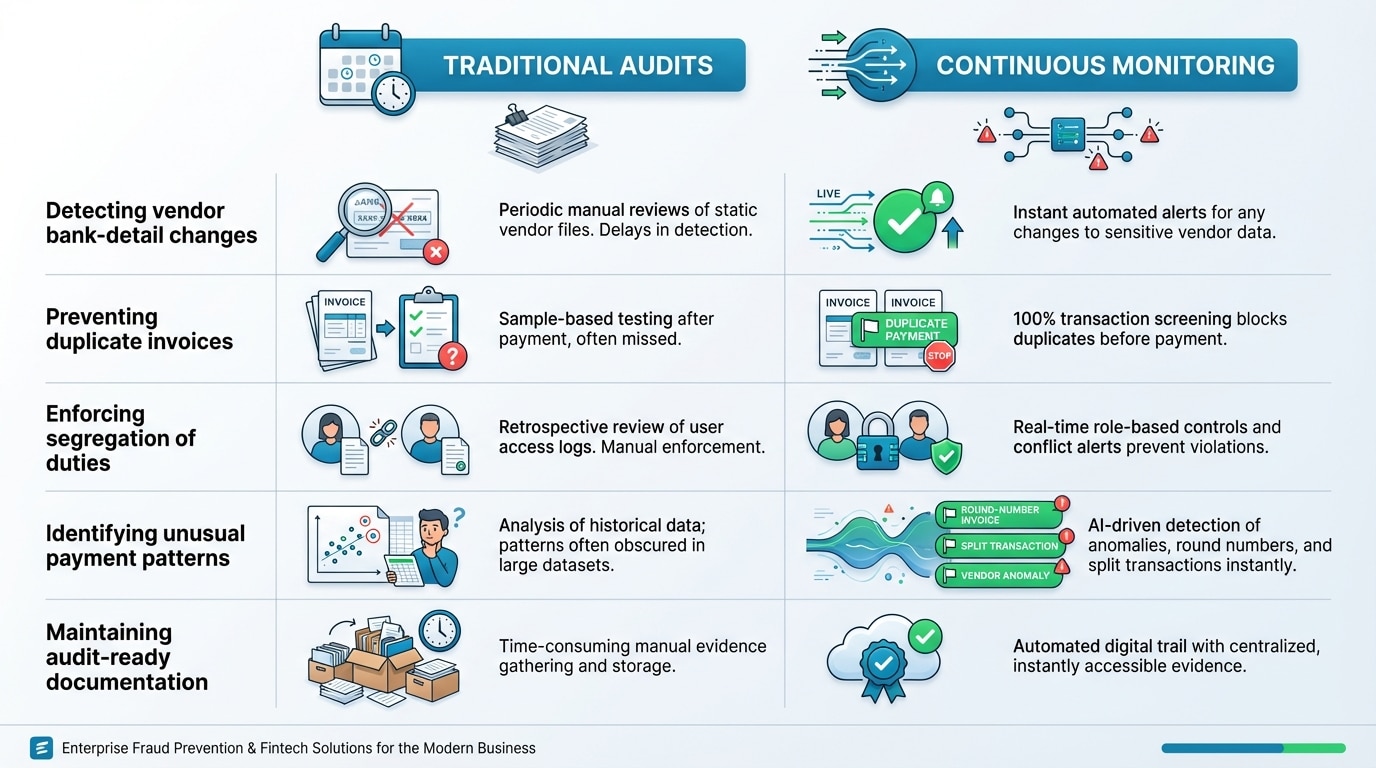

How Analytics and Automation Replace Periodic Audits with Continuous Assurance

Traditional audits, whether internal or external, are snapshots. They examine a sample of transactions from a defined period and extrapolate conclusions. The gap between audits is a window of vulnerability where errors, fraud, and policy deviations can accumulate undetected.

Continuous monitoring flips this model. Every transaction is evaluated against predefined rules and behavioral baselines as it occurs. Duplicate payments, round-number invoices, vendors with P.O. box addresses, transactions just below approval thresholds, and sudden spikes in refunds or credits are all flagged automatically. The finance team reviews prioritized alerts rather than sifting through raw data. This shift from periodic sampling to continuous assurance is what transforms the CFO’s role from reactive detection to proactive prevention.

| Business Need | How Real-Time Monitoring Helps in Practice |

|---|---|

| Detecting vendor bank-detail changes before payment | Alerts finance the moment a bank account is modified, requiring verification before funds are released |

| Preventing duplicate or fictitious invoices | Cross-references invoice numbers, amounts, and dates across the entire vendor ledger continuously |

| Enforcing segregation of duties | Monitors actual user behavior against role definitions and flags conflicts as they happen |

| Identifying unusual payment patterns | Detects split transactions, round-amount payments, and off-cycle runs in real time |

| Maintaining audit-ready documentation | Logs every alert, response, and resolution automatically for regulatory and audit review |

Did You Know

Organizations using continuous transaction monitoring detect fraud an average of 58% faster than those relying on periodic audits, according to the ACFE 2024 Report to the Nations. The median loss for schemes detected by continuous monitoring was less than half that of schemes found through traditional methods.

Common Mistakes CFOs Make When Building a Risk Management Program

Even experienced finance leaders fall into predictable traps. The first is treating risk management as a compliance exercise rather than a strategic function, producing documents for regulators instead of insights for decision-makers. The second is under-investing in detective controls because the organization “already has approvals in place.” Approvals prevent known risks; detective controls catch unknown ones.

A third mistake is failing to assign clear ownership. If every risk is “everyone’s responsibility,” no one is accountable. Each risk in the register needs a named owner with the authority and budget to act. Finally, many CFOs review risk metrics on a quarterly cycle when the underlying exposures can shift daily. Continuous monitoring closes this timing gap, ensuring that the leadership team is working with current information rather than historical summaries.

Tip

Assign each risk a single named owner at the director level or above. Shared ownership dilutes accountability. The risk owner should present their risk status and remediation progress at every leadership meeting, not just during annual reviews.

Benchmarks and Tests: Measuring Control Effectiveness Over Time

A control that worked last year may not work today. Measuring effectiveness requires ongoing testing, not just one-time validation. Practical benchmarks include the percentage of exceptions resolved within a defined SLA, the number of control overrides per period (and whether they are declining), false-positive rates in automated monitoring (too high means alert fatigue; too low may mean rules are too loose), and the average time between a control failure and its detection.

Tracking these metrics quarterly and presenting them to the board creates accountability and drives improvement. It also provides the CFO with evidence-based answers when the board asks, “Are our controls actually working?”

Detelix Real-Time Monitoring Solutions

Proactive Monitoring

Continuous, independent oversight of ERP transactions to detect anomalies, policy violations, and fraud attempts before they result in financial loss.

Real-Time Alerts

Instant notifications when critical events occur: vendor bank changes, duplicate invoices, segregation of duties violations, and unusual payment patterns.

GateKeeper

Automated enforcement of business rules and approval workflows across your ERP, preventing unauthorized transactions from being executed.

Experience & Expertise

Backed by deep domain knowledge in finance, compliance, and cybersecurity, Detelix delivers tailored solutions built on decades of real-world experience.

See Detelix in Action

Frequently Asked Questions

What is the first step a CFO should take to improve risk management?

Start by conducting a current-state assessment: identify which critical processes lack real-time monitoring, where segregation of duties is weak, and which risk categories have no assigned owner. This gap analysis becomes the foundation for a prioritized action plan.

How often should a risk register be updated?

At minimum, the risk register should be reviewed monthly by the risk owner and presented to the leadership team quarterly. However, any material change in the business environment, such as a new regulation, a significant customer loss, or a cyber incident, should trigger an immediate update.

Can small and mid-sized organizations benefit from continuous monitoring?

Yes. Smaller organizations often face higher relative risk because they have fewer staff and less built-in redundancy. A single employee may handle both vendor setup and payment execution. Continuous monitoring compensates for limited headcount by providing automated, independent oversight of sensitive processes.

How does real-time monitoring differ from a traditional ERP audit trail?

An ERP audit trail records what happened. Real-time monitoring analyzes what is happening and compares it against rules and behavioral patterns to flag anomalies before a transaction is completed. The difference is between a security camera that records footage for later review and a guard who intervenes the moment something looks wrong.

What role does the board play in CFO risk management?

The board sets the risk appetite, approves the risk management framework, and holds management accountable for staying within defined limits. The CFO translates the board’s risk appetite into operational metrics and reports back on adherence, exceptions, and emerging threats.

Is Your Organization Operating with Real Control, or Just the Appearance of It?

The gap between having procedures and having actual visibility into your financial processes is where the greatest risk lives. Move from periodic oversight to continuous, real-time protection with Detelix.