Stop Financial Fraud Before It Happens

Continuous transaction monitoring from Detelix gives your organization real-time visibility into every payment, transfer, and master data change across your ERP.

- What Exactly Is Continuous Transaction Monitoring?

- Why Spot Checks and Periodic Reviews Fall Short

- Real-Time vs. Batch: A Comparison That Shapes Your Risk Posture

- Inside the Engine: How a Transaction Monitoring System Works

- What Does the System Actually Monitor?

- A Common Mistake: Applying the Same Rules to Every Customer

- Rules-Based Detection vs. Machine Learning

- How Do You Reduce False Positives Without Missing Real Risk?

- Alert Prioritization: Not Every Flag Deserves the Same Urgency

- Building Your Scenario Library

- What the Investigation Process Should Look Like

- Must-Have Capabilities in a Modern Platform

- How Long Does Implementation Take?

- Where Ongoing Transaction Oversight Is Heading

- Frequently Asked Questions

In many organizations, financial controls appear robust on the surface. Approval workflows are in place, ERP permissions are configured, and compliance checklists are completed on schedule. Yet when a payment leaves the organization based on a fraudulently modified bank account, or when structured transactions evade a quarterly review undetected, the gap between perceived control and actual control becomes unmistakable. Continuous transaction monitoring addresses this gap head-on, replacing point-in-time snapshots with persistent, automated oversight that identifies risk as it develops rather than after the damage is done.

Key Takeaways

- Continuous transaction monitoring replaces periodic spot-checks with always-on, automated detection of anomalies across every financial event in your ERP or core banking system.

- Real-time monitoring can block or pause suspicious transactions before funds leave your organization, shifting your posture from reactive investigation to proactive prevention.

- Risk-based segmentation — calibrating detection thresholds to each customer or process type — is essential for reducing false positives while maintaining strong detection coverage.

- A layered approach combining rules-based detection with machine learning scoring delivers the best balance of regulatory transparency and novel-pattern identification.

- Effective monitoring extends beyond individual transactions to cover process-level events such as vendor master data changes, approval workflow modifications, and segregation-of-duties violations.

What Exactly Is Continuous Transaction Monitoring?

Continuous transaction monitoring is an automated, always-on process that scans financial transactions — transfers, deposits, withdrawals, payments, and adjustments — against predefined rules, behavioral baselines, and risk parameters. Unlike periodic audits or batch-based reviews, the process operates across every relevant transaction in real time or near real time. The objective is straightforward: detect deviations, flag suspicious patterns, and alert the right people before funds are irreversibly lost or compliance obligations are breached.

At its core, the concept rests on three pillars. First, data ingestion — capturing transactional events the moment they occur within the ERP or core banking environment. Second, a rules and analytics engine that compares each event against thresholds, historical behavior, and risk profiles. Third, alert management — routing exceptions to analysts or compliance officers with enough context to act quickly. When these pillars work in concert, organizations shift from reactive investigation to proactive prevention. Platforms like Detelix operationalize this shift by embedding hundreds of algorithms that ensure every action in the ERP system is continuously cross-checked against expected behavior.

Tip

Before evaluating any monitoring platform, document your three highest-risk financial processes (e.g., supplier payments, bank account changes, payroll disbursements). This ensures your proof-of-concept focuses on the scenarios that matter most to your organization rather than generic demo workflows.

Why Spot Checks and Periodic Reviews Fall Short

A quarterly compliance review examines a sample of transactions — sometimes less than five percent of total volume. Between review cycles, fraudsters, malicious insiders, and even well-intentioned employees making honest mistakes operate in a blind spot. Consider a scenario where a supplier’s bank details are changed in the master file on a Tuesday, a payment is executed on Wednesday, and the next scheduled review happens in six weeks. By that time, the funds have cleared, and the trail has cooled.

Continuous oversight eliminates this window of exposure. Every change, every payment, every anomaly is evaluated the moment it occurs. The result is not just better detection — it is prevention. When the system flags a bank account change that does not match historical patterns, the payment can be paused and verified before money leaves the organization. This distinction between “finding out later” and “knowing right now” is the operational foundation of continuous transaction monitoring.

Did You Know

According to the Association of Certified Fraud Examiners, the median duration of an occupational fraud scheme before detection is 12 months. Continuous monitoring significantly compresses this detection window by identifying anomalies in days or hours rather than months.

Real-Time vs. Batch: A Comparison That Shapes Your Risk Posture

The terms “real-time” and “batch” describe fundamentally different approaches to when a transaction is analyzed. Real-time transaction monitoring evaluates an event within milliseconds of its occurrence — often before it is fully settled — enabling immediate intervention such as blocking a payment, requesting additional authentication, or escalating to a supervisor. Batch monitoring, by contrast, collects transactions over a period (hours to days) and processes them together.

| Criterion | Real-Time Monitoring | Batch Monitoring |

|---|---|---|

| Detection speed | Milliseconds to seconds | Hours to days |

| Prevention capability | Can block or pause transactions | Post-event investigation only |

| Infrastructure demand | Higher (streaming architecture) | Lower (scheduled jobs) |

| False-positive handling | Immediate triage possible | Queued for next review cycle |

| Regulatory alignment | Meets strictest AML/CTF expectations | Acceptable for lower-risk segments |

For many organizations, a hybrid approach is practical: real-time monitoring for high-risk processes (supplier payments, bank account changes, large transfers) and batch processing for lower-risk, high-volume activity. The key is making this decision deliberately based on a documented risk assessment rather than defaulting to batch simply because it is easier to implement.

Tip

Map each of your financial processes to either real-time or batch monitoring based on a formal risk assessment. High-value supplier payments and master data changes warrant real-time oversight, while routine low-value internal transfers may be safely reviewed in daily batches.

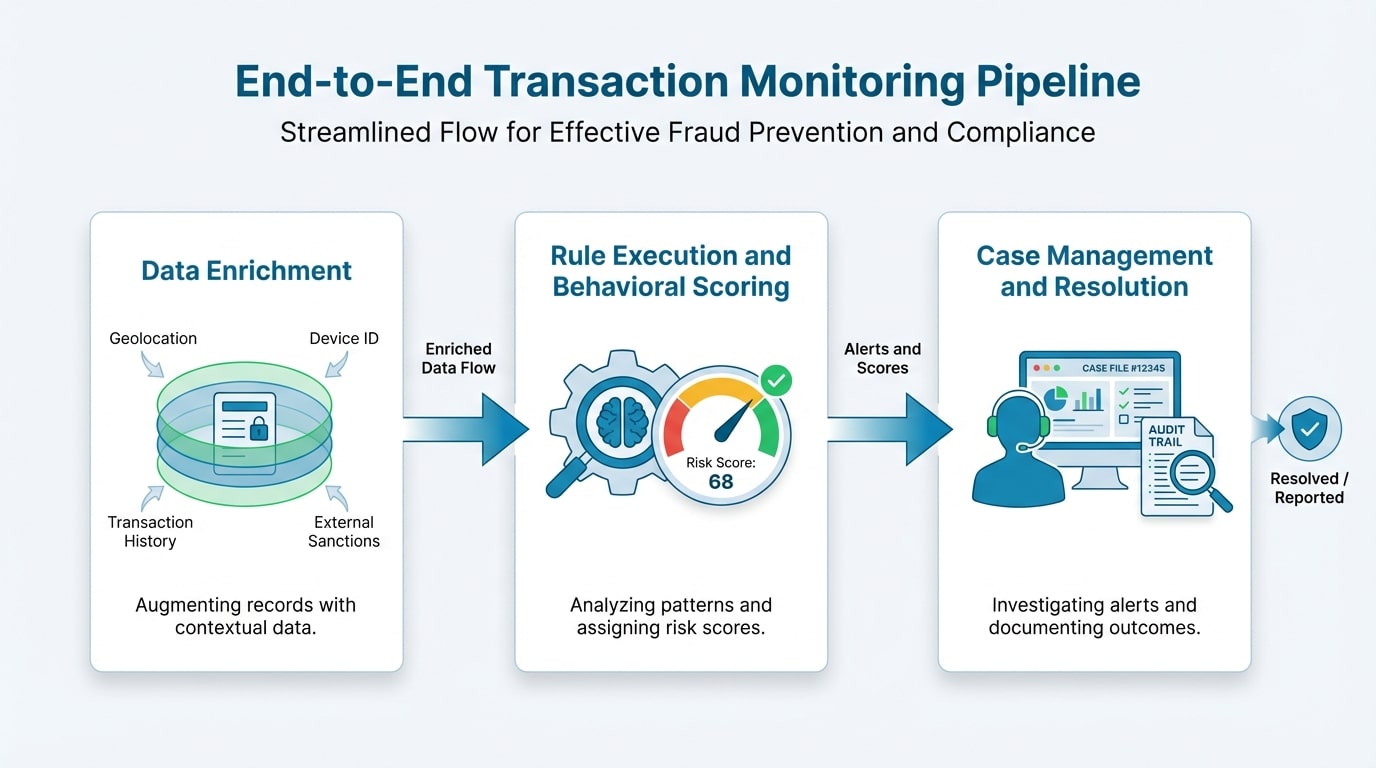

Inside the Engine: How a Transaction Monitoring System Works End to End

Understanding the architecture of a transaction monitoring system helps decision-makers ask better questions during vendor selection and implementation planning. The workflow generally follows a structured pipeline that transforms raw transactional data into actionable intelligence.

Data Enrichment and Contextualization

Raw transaction data alone — an amount, a timestamp, an account number — is insufficient for meaningful detection. The system enriches each event with contextual information: the customer’s risk profile, geographic indicators, the device or channel used, historical transaction patterns, and relationships to other entities. This enrichment transforms a simple payment record into an analyzable event with dozens of attributes.

Did You Know

A single outbound payment event can be enriched with over 40 contextual attributes before reaching the detection engine — including the beneficiary’s risk classification, the last time the bank account was modified, the approver’s authorization level, and the historical average payment amount for that supplier.

Rule Execution and Behavioral Scoring

Enriched events pass through the detection engine. Rules may check for specific conditions (a transfer above a defined threshold to a newly added beneficiary in a high-risk jurisdiction), while behavioral models compare the event against the entity’s baseline activity. A score is assigned based on the severity and combination of triggered rules. This scoring is what enables prioritization — not every alert carries the same urgency.

Case Management and Resolution

Alerts that exceed the scoring threshold become cases. An analyst reviews the supporting evidence, documents their findings, and decides on an action: close as benign, escalate for further review, file a regulatory report, or trigger a preventive measure. Throughout this process, a complete audit trail is maintained. Regulatory frameworks, such as Bank of Israel Directive 411 on AML/CTF risk management, explicitly require that organizations maintain documented investigation records available for supervisory review.

What Does the System Actually Monitor? A Practical Breakdown

The scope of continuous monitoring extends well beyond simple amount thresholds. Effective systems evaluate multiple dimensions simultaneously: the transaction amount relative to historical norms, the frequency of activity within a defined time window, the counterparty and its risk classification, the geographic origin and destination, the channel or device, and the time of day. Velocity checks — measuring how quickly transactions accumulate in volume or count — are particularly effective at identifying structuring, where amounts are deliberately kept below reporting thresholds.

Network analysis adds another layer. Rather than examining transactions in isolation, the system maps relationships between entities: shared addresses, linked accounts, common beneficiaries. This approach is essential for detecting mule account networks and layering schemes that would appear unremarkable when viewed one transaction at a time.

Tip

Ensure your monitoring system includes velocity checks across multiple time windows (1 hour, 24 hours, 7 days, 30 days). Structuring schemes often spread transactions across different windows to avoid single-period detection thresholds.

A Common Mistake: Applying the Same Rules to Every Customer

One of the most frequent errors in transaction monitoring programs is a “one-size-fits-all” rule set. When the same thresholds and triggers apply to a student account and a corporate treasury operation, the inevitable result is either a flood of irrelevant alerts on the corporate side or dangerous blind spots on the retail side. Risk-based monitoring solves this by calibrating detection sensitivity to each segment’s profile.

High-risk customers — politically exposed persons, entities in sanctioned jurisdictions, businesses in cash-intensive industries — receive tighter thresholds and more granular checks. Stable, long-standing relationships with predictable behavior patterns receive appropriately wider tolerances. This segmentation is not optional; it is a regulatory expectation reflected in international standards set by the FATF and domestic directives alike. The benefit is dual: better detection rates where risk is highest, and significantly fewer false positives where risk is low.

Did You Know

Organizations that implement risk-based segmentation in their monitoring rules typically see a 40-60% reduction in false-positive alert volume within the first six months, freeing analyst capacity for genuine high-priority investigations.

Are your current controls catching anomalies in real time — or are you relying on quarterly reviews and hoping nothing slipped through? Detelix provides continuous, automated oversight across every sensitive ERP process.

Rules-Based Detection vs. Machine Learning: Which Approach Wins?

The honest answer is that neither approach alone is sufficient, and the strongest monitoring programs combine both. Rules-based detection offers transparency and auditability — a regulator can examine a rule, understand its logic, and assess its effectiveness. It excels at catching known typologies: structuring, rapid movement of funds, transactions with sanctioned entities.

Machine learning complements rules by identifying anomalies that no one thought to write a rule for. It establishes behavioral baselines and detects deviations that are statistically significant but may not match any predefined pattern. The trade-off is interpretability: a machine learning model may flag a transaction as suspicious without providing a simple, human-readable explanation. This is why model governance — documentation of training data, validation methods, performance metrics, and periodic review — is critical.

| Dimension | Rules-Based | Machine Learning |

|---|---|---|

| Transparency | High — logic is explicit | Lower — requires explanation layer |

| Detecting known patterns | Strong | Moderate (depends on training data) |

| Detecting novel patterns | Weak (requires rule creation) | Strong (anomaly detection) |

| False-positive rate | Can be high without tuning | Typically lower after calibration |

| Regulatory acceptance | Well-established | Growing, with governance requirements |

In practice, many organizations use ML-based scoring to rank and prioritize alerts generated by rules. This layered approach preserves regulatory transparency while reducing the operational burden of investigating low-quality alerts.

Tip

When deploying machine learning models alongside your rule set, maintain a detailed model governance log that records training data sources, validation methodology, performance metrics, and review dates. Regulators increasingly expect this documentation during supervisory examinations.

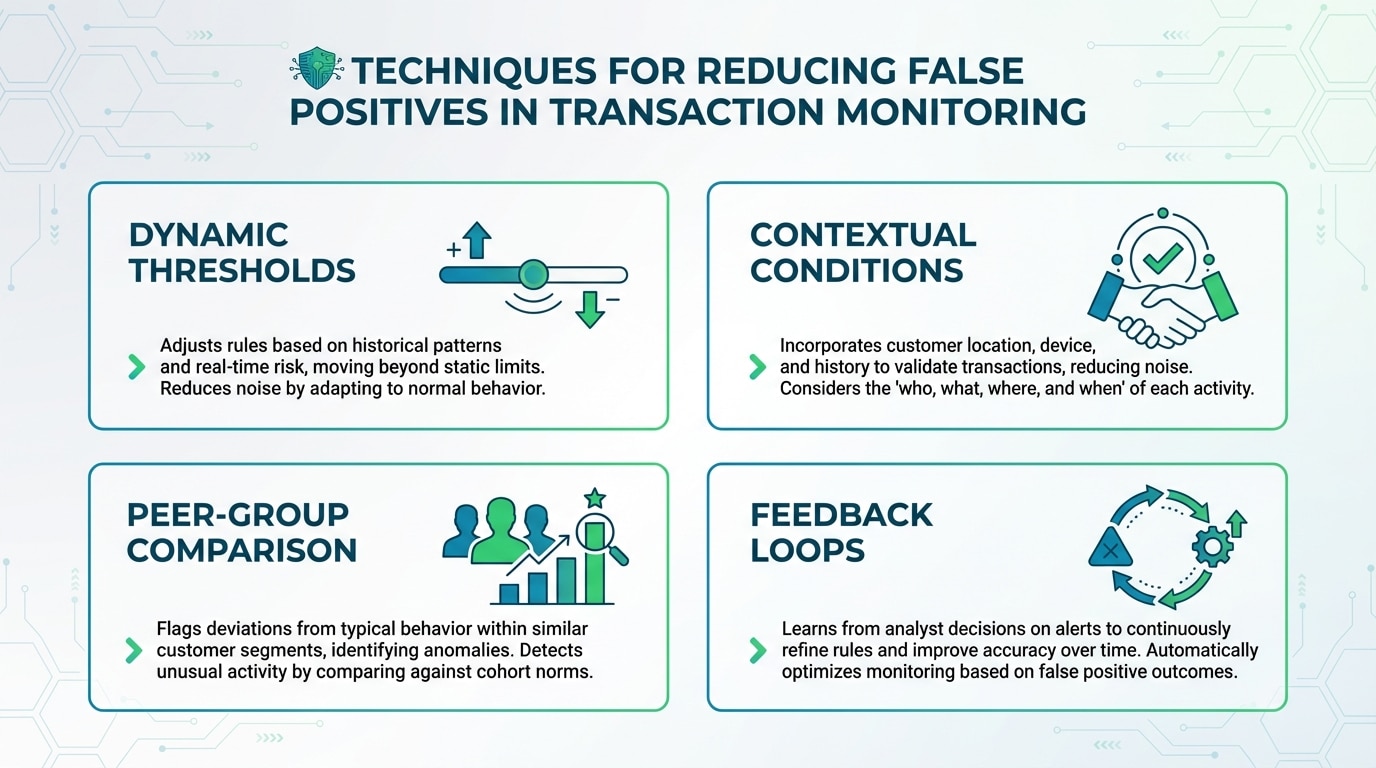

How Do You Reduce False Positives Without Missing Real Risk?

False positives — alerts that, upon investigation, turn out to be legitimate activity — are the single largest operational cost in transaction monitoring. When ninety percent or more of alerts are closed as benign, analyst fatigue sets in, investigation quality drops, and genuine risks are more likely to be overlooked. Reducing false positives is therefore not just an efficiency goal; it is a risk management imperative.

Effective techniques include dynamic thresholds that adjust to an entity’s own historical behavior, contextual conditions that suppress alerts when the counterparty is a known and verified partner, peer-group comparison (is this behavior unusual for this type of customer, not just for this individual?), and regular feedback loops where closure outcomes are analyzed to identify rules that consistently produce noise. Organizations that implement these practices can reduce false-positive rates substantially while maintaining or even improving detection coverage.

Did You Know

A feedback loop analysis — reviewing which rules generate the highest percentage of alerts closed as benign — can identify the top 10% of noise-generating rules responsible for up to 60% of total false-positive volume. Tuning or retiring these rules delivers immediate operational relief.

Alert Prioritization: Not Every Flag Deserves the Same Urgency

When a monitoring system generates hundreds of alerts daily, the ability to prioritize becomes essential. A composite risk score — combining the severity of the triggered rule, the customer’s inherent risk rating, the transaction amount, and the geographic or product context — determines where each alert falls in the queue. High-priority alerts may trigger immediate workflow escalation, while lower-priority items can be batched for periodic review.

Detelix approaches this challenge by applying layered scoring logic that evaluates not just the individual transaction but its relationship to broader process behavior within the ERP environment. When a bank account change is followed by an unusually large payment to a new beneficiary within the same business day, the combined signal receives a higher priority than either event would independently. This contextual awareness is what separates effective prioritization from simple threshold counting.

Building Your Scenario Library: Practical Examples of Monitoring Rules

Strong monitoring programs maintain a documented library of detection scenarios, each mapped to a specific risk typology. Below are examples that illustrate the breadth of what continuous transaction monitoring can cover.

Structuring detection: Multiple cash deposits just below the reporting threshold within a rolling 24-hour window. Velocity anomaly: A dormant account suddenly processes ten outbound transfers in a single day. Geographic risk: A wire transfer to a jurisdiction flagged by the organization’s risk policy where the customer has no declared business relationship. New beneficiary risk: A payment exceeding a defined amount directed to a beneficiary added to the system within the last 48 hours. Behavioral deviation: Transaction volume for a customer exceeds three standard deviations above their six-month average without a corresponding change in declared business activity.

Each rule should be segmented by customer risk tier so that a high-net-worth business client executing large international transfers does not generate the same alert as a retail customer exhibiting the same pattern for the first time.

Tip

Review and update your scenario library at least quarterly. New fraud typologies emerge continuously, and rules that were effective twelve months ago may no longer address current threat patterns. Assign a scenario owner responsible for each rule’s performance metrics and tuning schedule.

What the Investigation Process Should Look Like After an Alert Fires

An alert without a clear investigation workflow is just noise. The case management process typically follows a structured path: triage (initial assessment of alert quality and priority), evidence gathering (pulling transaction history, KYC documentation, and related alerts), analysis (determining whether the activity is consistent with the customer’s profile), decision (close, escalate, or report), and documentation (recording the rationale for the decision taken).

Regulatory expectations around documentation are explicit. The Israeli AML Order for banking corporations requires that identification, reporting, and record-keeping obligations are met with sufficient detail to support supervisory examination. Every step of the investigation — who reviewed it, what data was considered, what conclusion was reached — must be preserved in a tamper-resistant audit trail. Collaboration between compliance, fraud, and operational teams is critical here; siloed investigations miss connections that cross departmental boundaries.

Did You Know

Cross-departmental investigation teams that include both compliance and operations personnel resolve cases 35% faster on average than siloed teams, primarily because they can access and interpret contextual business information without waiting for inter-departmental requests.

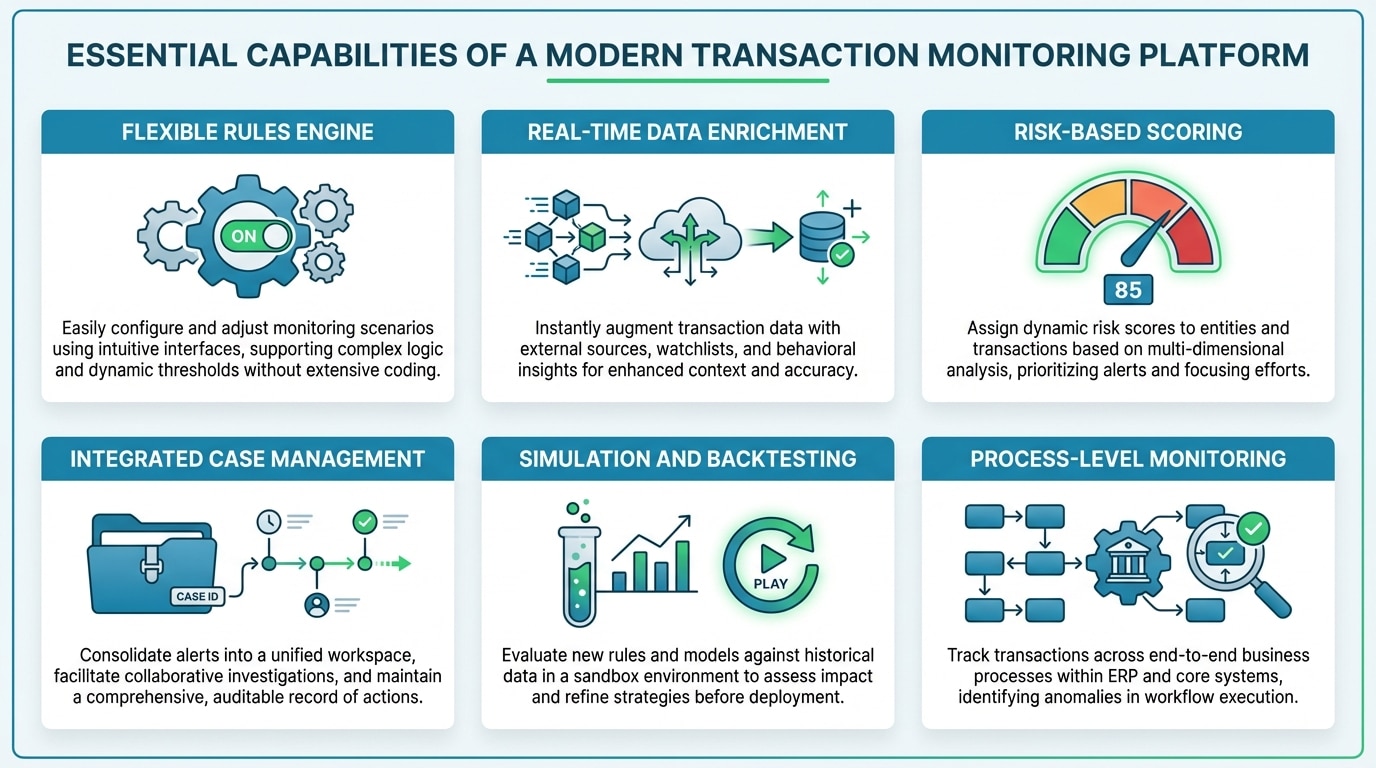

Must-Have Capabilities in a Modern Transaction Monitoring Platform

Organizations evaluating monitoring solutions should assess capabilities against a structured checklist rather than relying on feature-list comparisons. The essentials include a flexible rules engine that non-technical users can configure, time-window aggregations for velocity and cumulative checks, real-time data enrichment from internal and external sources, risk-based scoring and alert prioritization, integrated case management with full audit trail, simulation and backtesting tools for validating rule changes before deployment, role-based access controls, and comprehensive reporting for both operational management and regulatory submission.

Beyond these, look for the ability to monitor process-level events — not just individual transactions. Changes to vendor master data, modifications to payment approval workflows, and segregation-of-duties violations are all process events that a transaction-focused system may miss but that carry significant fraud and error risk. Detelix was built with this broader perspective, covering sensitive ERP processes including procurement, payroll, bank reconciliation, and supplier payments alongside traditional transaction-level monitoring.

Tip

During vendor evaluation, request a backtesting demonstration using your own historical data. A platform that can simulate its detection rules against six months of your actual transactions will reveal both its detection coverage and its expected false-positive rate far more accurately than a canned demo environment.

How Long Does Implementation Take, and What Should You Prepare?

Implementation timelines vary significantly depending on data readiness, system complexity, and the scope of scenarios. A realistic range for a mid-size organization is eight to sixteen weeks from project kickoff to initial production deployment, with ongoing tuning extending several months beyond that. The most common source of delays is not technology — it is data. Incomplete customer risk classifications, inconsistent transaction categorization, and fragmented data sources across multiple ERPs or core systems create integration challenges that must be resolved before rules can be meaningfully applied.

Pre-implementation preparation should include a thorough data mapping exercise (what fields are available, where they reside, and how current they are), a risk assessment that identifies priority scenarios, agreement on alert routing and escalation procedures, and allocation of analyst resources for the initial tuning phase. Organizations that invest in this groundwork before selecting a platform consistently achieve faster time-to-value and lower false-positive rates from day one.

Did You Know

Organizations that complete a formal data mapping and risk assessment before vendor selection reduce their average implementation timeline by 30-40% compared to those that begin data discovery after contract signing.

Where Ongoing Transaction Oversight Is Heading

The trajectory is clear: monitoring is becoming perpetual, contextual, and increasingly automated. Regulatory bodies worldwide are moving toward expectations of “always-on” compliance rather than periodic attestation. AI-based scoring will continue to reduce the manual burden of alert triage, allowing human analysts to focus on complex, judgment-intensive cases. The integration of monitoring with broader organizational controls — procurement oversight, payroll validation, inventory management — will blur the line between “transaction monitoring” and “enterprise process assurance.”

For finance and compliance leaders, the strategic question is no longer whether to implement continuous monitoring but how to do it in a way that is proportionate, effective, and sustainable. Manual spot-checks and quarterly reviews served their purpose in a slower, less digital era. In an environment where transactions move at digital speed and threat actors adapt continuously, real control requires real-time visibility.

Detelix Continuous Monitoring Solutions

Proactive Monitoring

Automated, continuous oversight of every sensitive ERP process — from vendor payments to payroll — with real-time anomaly detection.

Real-Time Alerts

Instant notifications when suspicious activity is detected, enabling your team to intervene before funds leave the organization.

GateKeeper

Advanced fraud prevention that cross-references master data changes, approval workflows, and payment patterns to catch manipulation attempts.

Industry Experience

Purpose-built detection scenarios refined across banking, insurance, healthcare, and enterprise environments with proven results.

See Detelix in Action

Frequently Asked Questions

Is continuous transaction monitoring a regulatory requirement?

In most regulated financial sectors, yes. Directives such as Bank of Israel Directive 411 and equivalent regulations in other jurisdictions explicitly require ongoing monitoring of customer activity, not just onboarding-stage due diligence. The specific technical approach (real-time vs. near real-time) may depend on the organization’s risk profile, but the expectation of continuous oversight is well established.

How is continuous monitoring different from KYC?

KYC (Know Your Customer) focuses on identifying and verifying the customer at the point of onboarding and at periodic refresh intervals. Continuous transaction monitoring evaluates what the customer actually does with their account on an ongoing basis. The two are complementary: KYC establishes the risk profile, and monitoring validates whether actual behavior is consistent with that profile over time.

What is the typical false-positive rate, and what is considered acceptable?

Industry benchmarks vary, but many organizations report that over 90% of alerts generated by first-generation rule sets are false positives. Well-tuned systems with segmentation, behavioral baselines, and ML-assisted scoring can reduce this to 50-70%, with leading programs pushing below 50%. The acceptable rate depends on the organization’s risk appetite, regulatory expectations, and analyst capacity.

Can a single platform handle both AML transaction monitoring and internal fraud detection?

Architecturally, the detection logic is similar — both involve comparing observed behavior against expected patterns. However, the rule sets, data sources, and escalation workflows differ. Some organizations use a single platform for both functions, while others maintain separate systems. The critical requirement is that each function has access to the data and rules it needs without creating conflicting or redundant alert streams.

How does continuous monitoring apply to ERP processes beyond banking?

Any process involving financial transactions, master data changes, or approval workflows benefits from continuous oversight. In an ERP context, this includes vendor payments, purchase order modifications, payroll runs, customer refunds, and inventory adjustments. The principles are identical: ingest events, enrich with context, apply detection logic, and alert when something deviates from policy or expected behavior.

Ready to Move from Periodic Reviews to Real-Time Oversight?

Your financial processes generate thousands of events daily. Detelix ensures every one of them is monitored, scored, and flagged when it matters — before funds are lost, not after.