Detect Financial Crime Before It Costs You Millions

Detelix delivers real-time, automated detection across every sensitive financial process in your ERP. Talk to our experts today.

- What Is Financial Crime Detection?

- Why Is Detecting Financial Crime Critical for Modern Organizations?

- Understanding the Scope of Corporate Financial Crime

- The Pillars of an Effective Detection Framework

- How Does Detection Differ from Prevention?

- Leveraging Technology: When Rules Meet Machine Learning

- Why Do Financial Crime Systems Produce So Many False Positives?

- A Practical Approach to Reducing False Positives

- How Financial Crime Detection Integrates with KYC and KYB

- What Does a Real-Time Detection Capability Look Like in Practice?

- Common Mistakes Organizations Make When Building Detection Programs

- How Do You Measure the Success of a Financial Crime Detection Program?

- Mapping Detection Capabilities to Business Needs

- How Long Does It Take to Implement a Detection System?

- Frequently Asked Questions

Every organization processes thousands of financial transactions daily — payments to vendors, payroll runs, customer refunds, inventory adjustments, and inter-company transfers. Behind each of these flows lies a potential vulnerability. Financial crime detection is the discipline that transforms raw transactional data into actionable intelligence, enabling finance leaders and risk teams to identify suspicious activity before it escalates into material loss, regulatory penalty, or reputational damage. When criminal methods evolve as fast as the technology designed to stop them, understanding how detection works — and where it falls short — is a core business competency for senior decision-makers.

Key Takeaways

- Financial crime detection uses data analytics, rule-based logic, and machine learning to identify unauthorized, illegal, or suspicious monetary activity in real time.

- Detection and prevention are complementary — the strongest posture combines blocking known risks at the source with catching unknown patterns as they emerge.

- False positives remain the industry’s biggest operational burden; reducing them requires data quality investment, customer segmentation, and closed-loop investigator feedback.

- Real-time monitoring over ERP processes — vendor payments, bank account changes, payroll, pricing — shifts organizations from reactive investigation to proactive control.

- Measurable KPIs such as alert-to-case rate, precision, case closure time, and losses prevented are essential for evaluating and improving detection program effectiveness.

What Is Financial Crime Detection?

Financial crime detection is the systematic, technology-driven process of identifying monetary activities that are illegal, unauthorized, or suspicious. It encompasses everything from spotting a single anomalous payment to uncovering complex multi-layered money-laundering schemes that span multiple entities and jurisdictions. At its core, the process relies on data — transaction records, customer profiles, third-party watchlists, and behavioral baselines — combined with analytical methods such as rule-based logic, statistical models, and machine learning algorithms.

The goal is not simply to generate alerts. It is to surface the right signals at the right time so that investigators can act decisively. Regulatory bodies worldwide define the trigger for investigation as activity that “lacks economic or business logic,” a standard reflected in official Israeli auditing observations that distinguish between routine and unusual financial reports. Detection sits at the intersection of compliance obligation and operational protection — making it both a legal requirement and a strategic advantage.

Tip

When evaluating detection platforms, ask vendors to demonstrate how their system distinguishes between a genuine anomaly and a legitimate but infrequent transaction. The quality of that distinction determines your false positive rate and your team’s investigative workload.

Why Is Detecting Financial Crime Critical for Modern Organizations?

The consequences of failing to detect financial crime extend far beyond the immediate monetary loss. Organizations that discover fraud or money laundering too late face a cascade of damage: regulatory fines that can reach millions, suspension of banking relationships, protracted legal proceedings, and a loss of stakeholder confidence that takes years to rebuild. In Israel, the Banking Supervision Sanctions Committee has demonstrated through enforcement actions that non-compliance with AML obligations carries real financial penalties.

Beyond compliance, there is a competitive dimension. Finance leaders who invest in robust detection gain visibility into process integrity — they can verify that payments match approved vendors, that pricing discounts are legitimate, and that no unauthorized changes slip through approval workflows. This level of oversight creates organizational confidence. Companies seeking effective protection against embezzlement and fraud errors recognize that detection is not a cost center; it is a safeguard that preserves profitability and operational stability.

Did You Know

According to the Association of Certified Fraud Examiners, the typical organization loses approximately 5% of its annual revenue to fraud — and the median duration of a fraud scheme before detection is 12 months. Continuous automated monitoring can reduce that detection window from months to hours.

Understanding the Scope of Corporate Financial Crime

Corporate financial crime differs from street-level fraud in its complexity, scale, and concealment methods. It occurs within the enterprise itself — perpetrated by employees, vendors, or external actors who exploit trusted business relationships. Examples include fictitious invoicing, where a vendor submits inflated or entirely fabricated bills; procurement kickbacks routed through third-party intermediaries; payroll ghost employees; and sophisticated shell-company structures used to launder illicit funds through legitimate-looking commercial transactions.

What makes corporate financial crime particularly dangerous is that it often leverages the organization’s own systems. An ERP environment with weak segregation of duties, for instance, allows a single individual to create a vendor, approve a purchase order, and authorize payment. Without continuous monitoring that cross-checks these actions in real time, such schemes can persist undetected for months or even years, compounding losses with every transaction cycle.

Tip

Map your organization’s critical financial workflows — vendor creation, purchase order approval, payment authorization, and bank account changes — and identify any process where a single person controls more than one step. These are your highest-priority targets for continuous monitoring.

The Pillars of an Effective Detection Framework

Transaction Monitoring and Behavioral Analysis

Transaction monitoring is the engine of financial crime detection. It involves continuous analysis of financial flows to identify patterns that deviate from established baselines. These baselines are built from historical data — a customer’s typical transaction volume, frequency, counterparties, and geographic footprint. When activity falls outside the expected range — sudden spikes in volume, transactions at unusual hours, rapid movement of funds between accounts, or structuring amounts just below reporting thresholds — the system flags the deviation for review.

Behavioral analysis adds a deeper layer. Rather than relying solely on static thresholds, it evaluates whether a sequence of actions tells a coherent “economic story.” A newly opened account that immediately receives large wire transfers and disperses them to multiple overseas entities within days raises questions that a simple volume check might miss.

Did You Know

Structuring — the deliberate splitting of large transactions into smaller amounts to avoid reporting thresholds — is itself a criminal offense in most jurisdictions, regardless of whether the underlying funds are legitimate. Detection systems specifically look for patterns of transactions just below mandatory reporting limits.

Sanctions and Adverse Media Screening

Sanctions screening matches customers, counterparties, and beneficiaries against international prohibited-party lists — including those maintained by OFAC, the EU, and the UN. The challenge lies in accuracy: name variations, transliterations across languages, and common surnames generate significant numbers of false matches. Israel’s Banking Supervision authority has addressed this tension directly, requiring institutions to balance rigorous screening with the ability to continue providing services to legitimate customers.

Adverse media screening complements watchlist checks by scanning open-source information for negative news coverage — links to corruption, litigation, regulatory action, or criminal investigation. It is most useful during onboarding and periodic reviews, but it demands high-quality filtering to separate genuinely relevant signals from background noise.

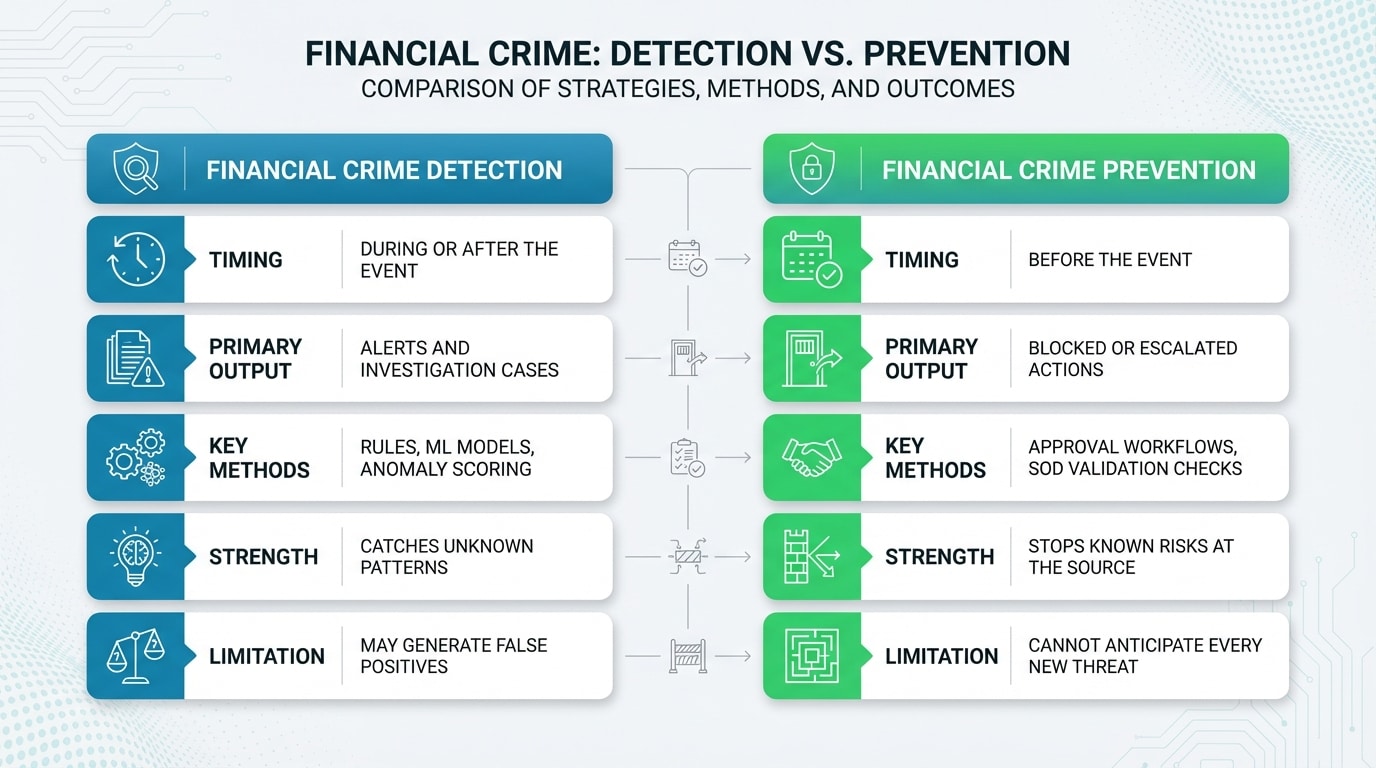

How Does Detection Differ from Prevention?

Detection and prevention are complementary, but they operate at different points in the risk lifecycle. Detection identifies suspicious activity that has already occurred or is in progress — it finds the anomaly, generates an alert, and triggers an investigation. Prevention, by contrast, aims to stop the crime before it happens by hardening processes, enforcing controls, and blocking unauthorized actions at the point of execution.

Consider a scenario where a fraudster attempts to change a vendor’s bank account details to redirect a payment. A detection system would flag the change after it was made, based on unusual patterns. A prevention-oriented control would intercept the change request itself — requiring dual authorization, verifying the new account against known records, and alerting the finance team immediately. The strongest posture combines both: prevention reduces the attack surface, while detection catches what slips through.

Platforms like Detelix embody this dual approach by providing real-time alerts across sensitive ERP processes — from bank account changes to supplier payments — so that organizations can intervene before money leaves the company, not just investigate after the fact.

| Dimension | Detection | Prevention |

|---|---|---|

| Timing | During or after the event | Before the event |

| Primary Output | Alerts and investigation cases | Blocked or escalated actions |

| Key Methods | Rules, ML models, anomaly scoring | Approval workflows, SoD, validation checks |

| Strength | Catches unknown or evolving patterns | Stops known risks at the source |

| Limitation | May generate false positives | Cannot anticipate every new threat |

Tip

Audit your current control environment by categorizing each control as either detective or preventive. If more than 70% of your controls are detective, you are likely spending too much time investigating incidents that could have been blocked outright. Rebalance toward prevention for your highest-risk processes.

Leveraging Technology: When Rules Meet Machine Learning

Traditional financial crime detection systems rely on rule-based logic: if a transaction exceeds a defined threshold, or if a customer’s profile matches certain risk criteria, the system fires an alert. Rules are transparent, easy to explain to regulators, and effective for well-known scenarios. However, they are inherently static. Criminals learn the thresholds and adjust their behavior to stay just below detection limits — a tactic known as structuring.

Machine learning changes the equation by identifying patterns that rules cannot anticipate. Supervised models learn from historical cases of confirmed fraud or money laundering; unsupervised models detect anomalies relative to peer-group behavior without needing labeled examples. The result is a significant improvement in the signal-to-noise ratio: fewer false positives, faster identification of genuinely suspicious activity, and the ability to adapt as criminal methods evolve.

The most effective approach is hybrid. Rules handle clear-cut regulatory requirements — such as mandatory reporting thresholds — while ML models surface emerging risks and complex behavioral patterns. Organizations that apply machine learning to monitor pricing and discounts, for example, can catch revenue leakage and manipulation that static rules would never flag. The key is governance: every model must be validated, documented, and monitored for drift to maintain both accuracy and regulatory defensibility.

Did You Know

A hybrid detection approach combining static rules with machine learning models has been shown to reduce false positive volumes by 40-60% in financial institutions, while simultaneously increasing the detection rate of genuinely suspicious activity — according to multiple industry benchmark studies.

Is your detection system catching what matters — or burying your team in false alerts? Detelix provides real-time, ML-enhanced monitoring across your entire ERP environment.

Why Do Financial Crime Systems Produce So Many False Positives?

False positives are the industry’s most persistent operational burden. Estimates across the global banking sector suggest that upward of 90% of transaction monitoring alerts turn out to be benign upon investigation. The root causes are well understood: overly broad rules written to avoid missing any suspicious activity, inconsistent or incomplete data, thresholds that have not been recalibrated as customer behavior shifts, and a lack of contextual enrichment that would help the system distinguish between genuinely unusual activity and legitimate but infrequent transactions.

The cost is not just investigator time. Excessive false positives create alert fatigue, where analysts begin to treat every alert as noise — increasing the risk that a genuine red flag is dismissed or deprioritized. They inflate operational costs, extend case resolution timelines, and divert resources from higher-value investigative work. For finance leaders, this is not merely a compliance headache; it is a direct drag on productivity and control effectiveness.

A Practical Approach to Reducing False Positives

Reducing false positives without increasing the risk of missing real threats requires a disciplined, data-driven approach. It starts with data quality: ensuring that customer records are complete, consistent, and regularly updated. Duplicate records, missing industry codes, and outdated contact information all contribute to inaccurate scoring.

Next comes segmentation. Not every customer or transaction type carries the same risk. By grouping entities into risk tiers — based on geography, industry, transaction profile, and relationship history — organizations can apply differentiated thresholds that reflect actual risk rather than blanket rules. A high-volume import-export company will naturally exhibit transaction patterns that would be anomalous for a domestic retail business. Treating them identically guarantees noise.

Closing the Feedback Loop

Perhaps the most underutilized lever is the investigator feedback loop. When an analyst closes a case as a false positive, that outcome should feed back into the detection system to refine future scoring. This closed-loop learning creates a virtuous cycle: each investigated case improves the precision of future alerts. Without it, systems remain static and the same unproductive alerts recur indefinitely.

Tip

Establish a monthly review cadence where your investigation team’s disposition data is analyzed to identify the top five recurring false-positive scenarios. Target those scenarios for threshold adjustment or rule retirement first — this single practice can reduce alert volume by 20-30% within one quarter.

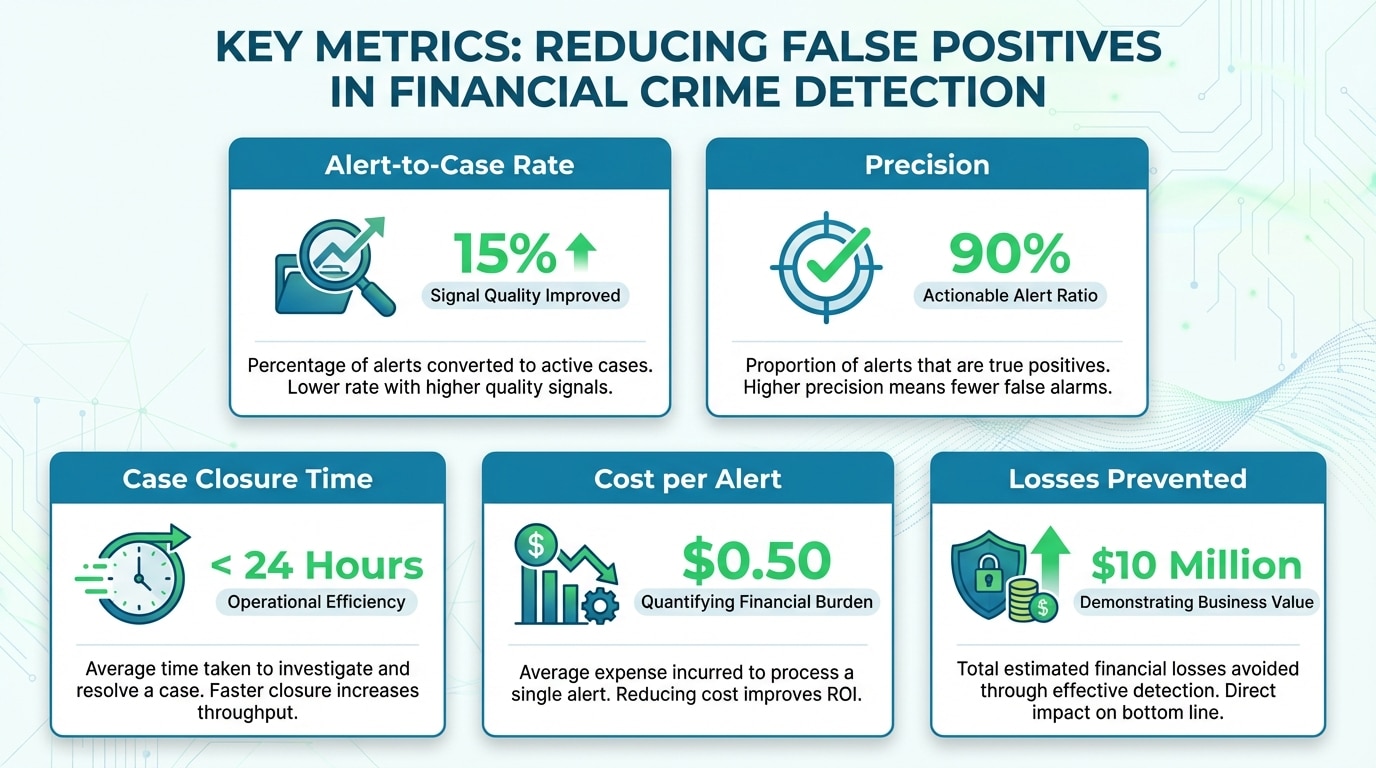

| Metric | What It Measures | Why It Matters |

|---|---|---|

| Alert-to-Case Rate | Percentage of alerts escalated to full investigation | Indicates signal quality |

| Precision | True positives / (True positives + False positives) | Shows how many alerts are actionable |

| Case Closure Time | Average hours from alert to resolution | Reflects operational efficiency |

| Cost per Alert | Total investigation cost divided by alert volume | Quantifies the financial burden of noise |

| Losses Prevented | Value of confirmed fraud or illicit funds intercepted | Demonstrates business value of the program |

How Financial Crime Detection Integrates with KYC and KYB

Know Your Customer (KYC) and Know Your Business (KYB) processes establish the identity and risk profile of every counterparty at onboarding. They answer foundational questions: Who is this person or entity? What is their source of funds? What is their expected transaction behavior? This baseline is the starting point for all subsequent detection activity.

But KYC and KYB are not one-time exercises. Risk profiles change. A company’s ownership structure shifts, a customer’s transaction volume suddenly doubles, or a beneficial owner appears on a newly published sanctions list. Effective detection systems trigger periodic reviews and event-driven reassessments, creating a dynamic risk picture rather than a static snapshot. When detection flags an anomaly, it also re-evaluates the customer’s risk tier — potentially escalating them for enhanced due diligence or restricting certain transaction types until the review is complete.

Did You Know

Event-driven KYC reassessment — triggered by detection alerts rather than calendar-based reviews — can identify material risk changes up to 8 months earlier than traditional annual review cycles, according to regulatory technology benchmarking reports.

What Does a Real-Time Detection Capability Look Like in Practice?

Real-time detection means that every relevant action within a financial workflow is evaluated as it occurs — not hours or days later in a batch report. When a vendor’s bank account is modified in the ERP system, the detection layer immediately cross-checks the change against historical records, flags deviations, and notifies the appropriate control owner. When a payment is initiated to a new beneficiary in a high-risk jurisdiction, the system scores the transaction instantly and can hold it for review before funds are released.

This is where platforms like Detelix deliver measurable value. By operating as a continuous control layer over ERP-driven processes, Detelix enables finance teams to see what is happening right now — not reconstruct events after the damage has occurred. The shift from periodic review to continuous monitoring is the difference between managing risk retrospectively and actually controlling it in real time.

Tip

When transitioning from batch-based to real-time monitoring, start with your highest-value process — typically vendor bank account changes or large payment approvals. Demonstrate measurable risk reduction in that single area before expanding coverage. This builds executive buy-in and reduces implementation risk.

Common Mistakes Organizations Make When Building Detection Programs

One of the most frequent errors is attempting to implement every possible detection scenario simultaneously. Organizations purchase comprehensive rule libraries, activate hundreds of scenarios, and immediately drown in thousands of alerts that their investigation teams cannot process. The result is worse than having no system at all: it creates a false sense of coverage while burying genuine risks under operational noise.

A second mistake is neglecting data quality. No algorithm — whether rule-based or machine-learned — can compensate for incomplete, duplicated, or inconsistent input data. Organizations that invest in detection technology without first investing in data governance typically see poor precision and high operational cost, leading to frustration and eventual system abandonment.

A third and often overlooked error is failing to define clear KPIs from the outset. Without measurable targets — such as alert-to-case conversion rate, average investigation time, or precision by scenario type — teams have no way to evaluate whether the program is improving or deteriorating. Detection without measurement is guesswork.

Did You Know

Organizations that activate more than 50 detection scenarios at launch without a phased rollout plan experience, on average, a 300% increase in alert volume compared to their investigation capacity — leading to backlogs that can take 6-9 months to clear.

How Do You Measure the Success of a Financial Crime Detection Program?

Success measurement must balance two dimensions: detection effectiveness and operational efficiency. On the effectiveness side, key indicators include the rate at which alerts convert to confirmed cases, the value of losses prevented or recovered, and the coverage of known risk scenarios. On the efficiency side, organizations should track case closure time, investigator throughput, cost per alert, and the ratio of automated dispositions to manual reviews.

The most mature programs also measure what they are not catching. Periodic look-back exercises — re-running historical data through updated models — can reveal blind spots and quantify the improvement delivered by model refinements. This is not a one-time calibration; it is an ongoing discipline that separates compliance-driven programs from genuinely protective ones.

Tip

Schedule quarterly look-back exercises where you re-run the past 90 days of transaction data through your latest detection model. Compare the results against what was originally flagged. The delta between the two reveals exactly how much your model improvements have increased detection coverage — and gives you concrete data for board-level reporting.

Mapping Detection Capabilities to Business Needs

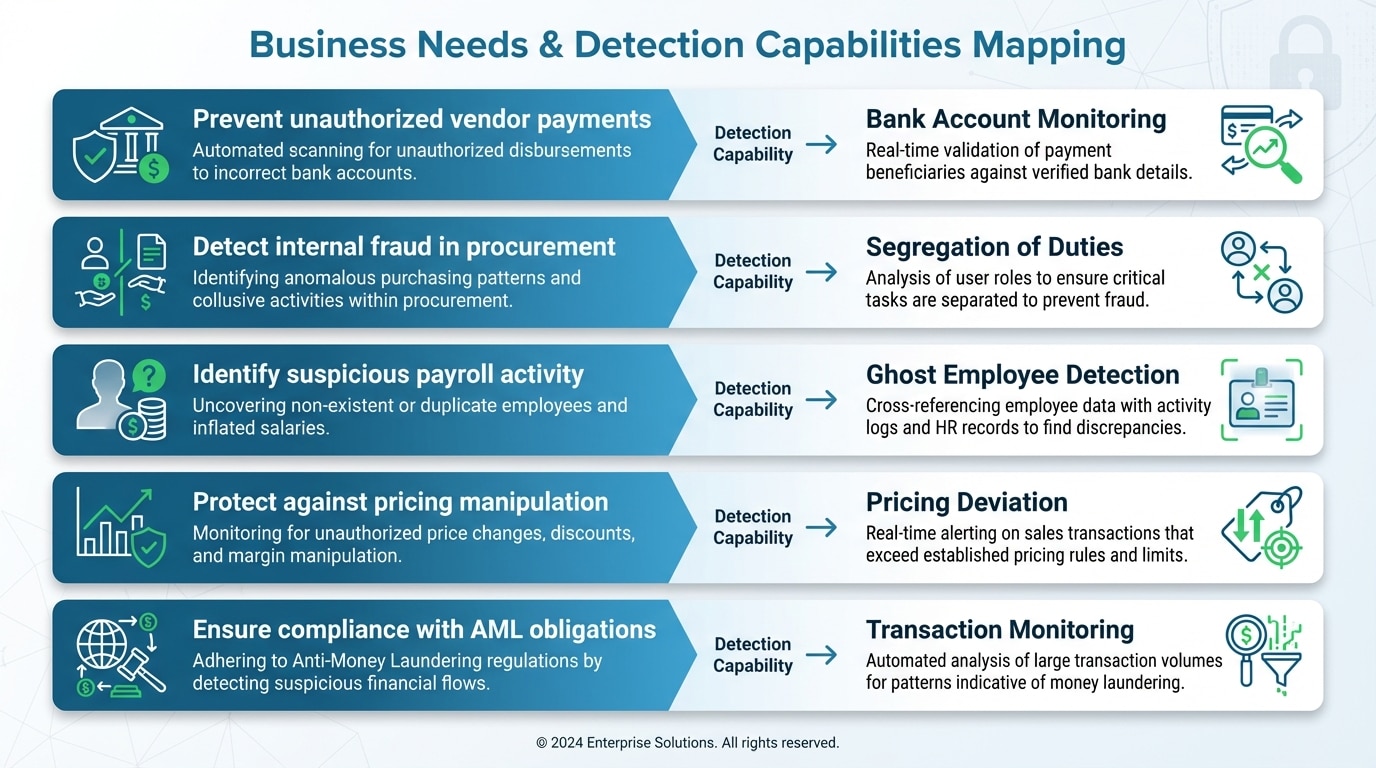

| Business Need | Detection Capability Required | How Detelix Helps |

|---|---|---|

| Prevent unauthorized vendor payments | Bank account change monitoring, dual-authorization enforcement | Real-time alerts on vendor master changes with cross-referencing against approved records |

| Detect internal fraud in procurement | Segregation of duties analysis, duplicate invoice detection | Continuous SoD monitoring across ERP roles with automated exception flagging |

| Identify suspicious payroll activity | Ghost employee detection, payroll anomaly scoring | Automated cross-checks of payroll records against HR data and banking details |

| Protect against pricing manipulation | Discount and pricing deviation analysis | ML-driven monitoring of pricing patterns to flag unauthorized discounts or margin erosion |

| Ensure compliance with AML obligations | Transaction monitoring, sanctions screening, SAR workflow | Integration with ERP data flows to provide continuous monitoring and audit-ready documentation |

How Long Does It Take to Implement a Detection System?

Implementation timelines vary significantly based on the complexity of the organization’s data landscape, the number of ERP systems in play, and the maturity of existing control processes. However, the most successful implementations follow a phased approach rather than a “big bang” deployment. A focused MVP — covering two or three high-risk scenarios with clean data from a single source system — can typically be operational within weeks, not months.

From that initial foundation, organizations expand coverage incrementally: adding new data sources, activating additional scenarios, and refining thresholds based on early investigation outcomes. This iterative model reduces risk, accelerates time-to-value, and builds organizational confidence progressively. Detelix supports this approach by offering modular deployment across specific process areas — supplier payments, bank reconciliation, inventory, or payroll — so that each phase delivers immediate, measurable control improvement.

Did You Know

Organizations that adopt a phased implementation approach — starting with 2-3 high-priority scenarios and expanding quarterly — achieve full ROI on their detection investment an average of 40% faster than those attempting comprehensive deployment from day one.

Is your organization confident that its current controls can detect financial crime in real time — before losses materialize and before regulators come asking? If the answer is uncertain, it may be time to evaluate how continuous, automated monitoring can strengthen your control environment across every sensitive financial process. Reach out to the Detelix team to explore how real-time detection and prevention can work for your organization.

Detelix Financial Crime Detection Solutions

Proactive Monitoring

Continuous, automated surveillance of all ERP financial processes to detect anomalies and suspicious patterns before they escalate into losses.

Real-Time Alerts

Instant notifications on critical changes — vendor bank accounts, unusual payments, and authorization breaches — delivered to the right stakeholders immediately.

Gatekeeper

Preventive controls that intercept high-risk actions at the point of execution — blocking unauthorized changes before damage occurs.

Experience & Expertise

Over a decade of domain expertise in ERP fraud prevention, backed by ISO 27001 and ISO 27799 certifications for enterprise-grade security.

See Detelix in Action

Frequently Asked Questions

What is the most common type of corporate financial crime?

Vendor fraud and fictitious invoicing consistently rank among the most prevalent forms of corporate financial crime. They exploit the high volume of routine payment flows and often go undetected in organizations that lack automated cross-checking between purchase orders, goods receipts, and invoices. Employee embezzlement through payroll manipulation and expense fraud are also frequently encountered.

How does financial crime detection differ from Anti-Money Laundering?

Anti-Money Laundering (AML) is a subset of financial crime detection. AML focuses specifically on identifying attempts to disguise the origins of illicitly obtained funds. Financial crime detection is broader — it also covers fraud, bribery, sanctions violations, tax evasion, and insider threats. In practice, many detection systems address both AML and broader fraud risks through overlapping data, rules, and analytical methods.

Can AI completely replace human investigators?

No. AI and machine learning dramatically improve the speed and accuracy of initial screening and alert generation, but human judgment remains essential for contextual evaluation, case escalation, regulatory reporting, and decision-making on complex or ambiguous cases. The optimal model is augmentation — technology handles volume and pattern recognition, while experienced investigators focus on the cases that require nuanced analysis.

Why should small businesses care about financial crime prevention?

Small businesses are frequently targeted precisely because they are perceived to have weaker controls. A single significant fraud event — a redirected payment, a compromised vendor account, or an internal embezzlement scheme — can represent a material percentage of a small company’s revenue. Additionally, businesses of all sizes face regulatory obligations related to anti-money laundering and sanctions compliance, depending on their industry and jurisdiction.

What is case management in the context of financial crime alerts?

Case management is the structured workflow that follows an alert. It includes assigning the alert to an investigator, gathering supporting evidence, documenting findings, making a disposition decision (escalate, close, or file a suspicious activity report), and maintaining a complete audit trail. Effective case management ensures consistency, accountability, and regulatory defensibility across every investigated alert.

Ready to Detect Financial Crime in Real Time?

Stop investigating after the damage is done. Detelix gives your finance team the visibility and control to catch suspicious activity the moment it happens — across every critical ERP process.