Stop Duplicate Payments Before They Drain Your Budget

Detelix monitors every outgoing transaction in real time — catching duplicates, anomalies, and policy violations before funds leave your account.

- What Is Duplicate Payment and Transaction Anomaly Detection?

- Why Do Duplicate Payments Occur Even with ERP Controls?

- What Is the Role of Fuzzy Matching Payments in Detection?

- Moving Beyond Duplicates — Anomalous Transaction Analytics Explained

- Which Data Fields Are Critical for Effective Monitoring?

- A Scenario That Illustrates Why Rules Alone Are Not Enough

- How to Implement a Real-Time Financial Leak Prevention Strategy

- Rules-Based Detection Compared to Machine-Learning Approaches

- How to Reduce False Positives Without Missing Real Duplicates

- Assessing the ROI of Automated Detection Systems

- What to Evaluate When Choosing a Detection Solution

- Frequently Asked Questions

In many organizations, financial controls appear robust on paper. Approval workflows exist, ERP permissions are configured, and reconciliation procedures are documented. Yet every year, companies lose significant sums to duplicate payments and undetected transaction anomalies — not because controls are absent, but because they are insufficient against the complexity of modern payment operations. When invoices arrive through multiple channels, vendors change bank details, and payment runs process hundreds of transactions in minutes, the gap between perceived control and actual control becomes a serious financial risk. Understanding how duplicate payment and transaction anomaly detection works — and why it matters — is the first step toward closing that gap and protecting your organization’s bottom line.

Key Takeaways

- Standard ERP duplicate checks rely on exact invoice number matches and routinely miss near-duplicates caused by formatting variations, typos, and resubmissions.

- Fuzzy matching algorithms compare multiple transaction fields simultaneously — vendor name, amount, date, and bank account — to surface payments that are “similar enough” to warrant review.

- Anomalous transaction analytics detect behavioral outliers such as unusual timing, dormant vendor activity, and split payments designed to bypass approval thresholds.

- Combining rules-based detection with machine-learning models creates a layered defense that catches both known patterns and previously unseen fraud tactics.

- Pre-payment blocking delivers the highest ROI because funds never leave the organization — post-payment recovery is slower, costlier, and less certain.

- Detelix integrates directly with ERP environments to provide continuous, real-time monitoring that flags issues before payment files are finalized.

What Is Duplicate Payment and Transaction Anomaly Detection?

Duplicate payment and transaction anomaly detection is a multi-layered defensive strategy that continuously monitors outgoing funds to verify that every payment is legitimate, authorized, and unique. At its core, the process compares pending and completed transactions against historical data, vendor records, and organizational policies to flag irregularities before they cause financial damage.

The scope extends far beyond simple invoice matching. It encompasses identifying double-entered invoices, catching payments routed to modified bank accounts, spotting unusual spikes in vendor billing, and detecting policy violations such as split payments designed to bypass approval thresholds. As a State Comptroller report on computer-aided payment controls has noted, large payment volumes processed through automated systems create inherent exposure to errors, manipulation, and fraud — making automated anomaly detection not optional but essential for financial leak prevention.

Tip

Map every channel through which invoices enter your organization — email, supplier portals, postal mail, EDI — and ensure your detection system ingests data from all of them. A duplicate that arrives via a different channel than the original is one of the most common sources of overpayment.

Why Do Duplicate Payments Occur Even with ERP Controls?

The assumption that an ERP system will catch every duplicate is one of the most costly misconceptions in accounts payable. Standard ERP duplicate checks typically rely on exact matches of invoice numbers. When a vendor submits “INV-2024-0087” and later resubmits the same charge as “INV2024-0087” — without the dashes — the system treats these as two separate, valid invoices.

Common root causes include manual data entry inconsistencies, vendors sending the same invoice via email and through a supplier portal, corrected invoices issued with new reference numbers, and partial payments that create confusion about remaining balances. Communication breakdowns between procurement and accounts payable departments add another layer of risk. In organizations that process thousands of invoices monthly, even a small error rate translates into substantial overpayments. For a deeper technical analysis of how standard ERP checks fail, see why ERP controls fail to stop duplicate payments.

Did You Know

Research from accounts payable benchmarking studies consistently shows that organizations without automated duplicate detection experience overpayment rates between 0.1% and 0.5% of total disbursements. For a company processing $100 million annually, that translates to $100,000 to $500,000 in preventable losses every year.

What Is the Role of Fuzzy Matching Payments in Detection?

Fuzzy matching payments is the analytical method that identifies transactions as “similar enough” to warrant review, even when they are not byte-for-byte identical. Unlike exact-match logic, fuzzy matching calculates a similarity score across multiple fields — vendor name, invoice amount, date, bank account, and line-item descriptions — to surface near-duplicates that would otherwise pass unnoticed.

Consider a scenario where “Acme Industries Ltd.” appears in one record and “ACME Industris” in another due to a typo. An exact match would miss this entirely. Fuzzy matching algorithms evaluate character-level similarity, transposed digits in amounts, overlapping date ranges, and normalized addresses to produce a confidence score. When that score exceeds a defined threshold, the transaction is flagged for human review. This capability is particularly valuable for organizations dealing with international vendors, where name transliterations and varied banking formats make exact matching unreliable.

Tip

When configuring fuzzy matching thresholds, start with a higher sensitivity (lower similarity score requirement) and gradually tighten as your team reviews the initial flags. This approach builds a baseline understanding of your data quality before optimizing for precision.

Moving Beyond Duplicates — Anomalous Transaction Analytics Explained

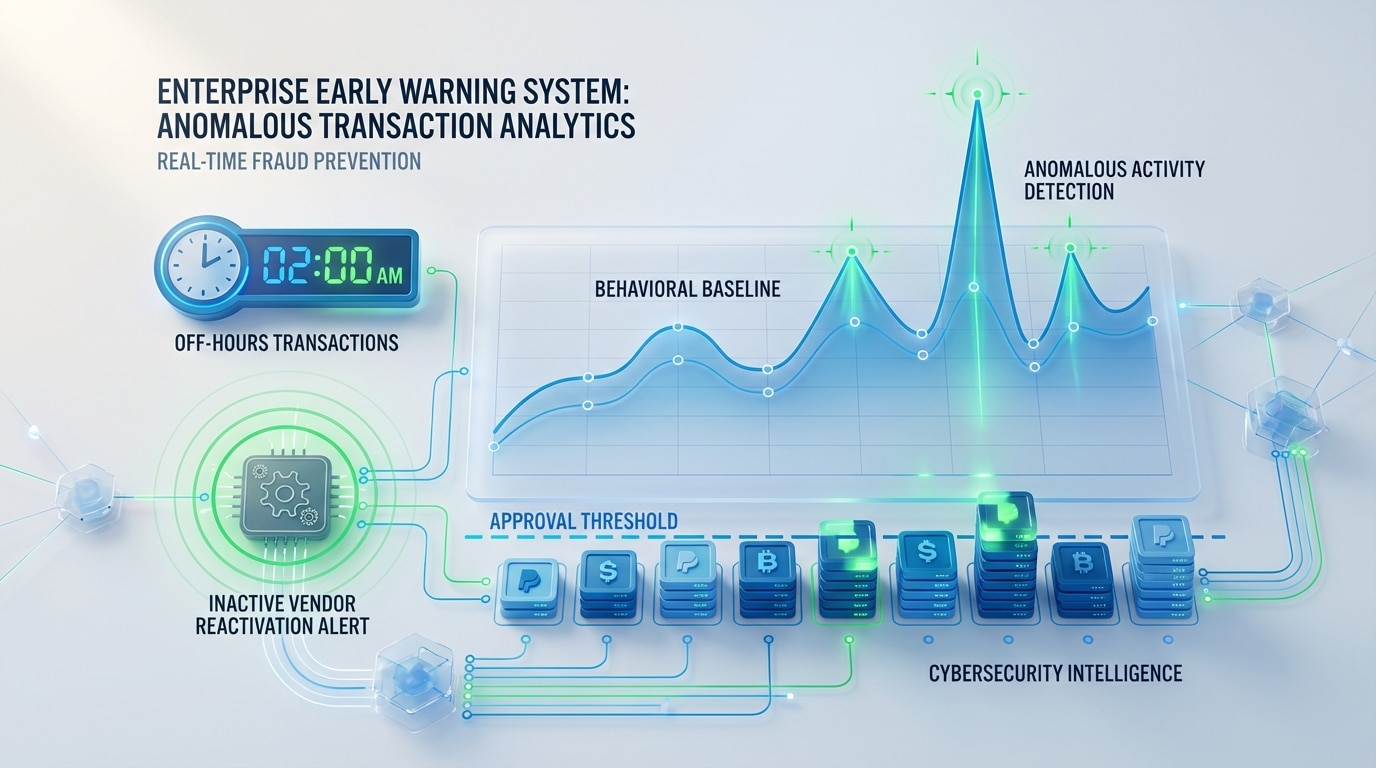

While duplicate invoice detection focuses on finding the same payment twice, anomalous transaction analytics casts a wider net. It uses behavioral baselines and pattern analysis to identify transactions that are unusual relative to historical norms — even when no duplicate exists. A payment processed at 2:00 AM on a holiday, a dormant vendor suddenly receiving large transfers, or a series of payments just below the approval threshold all qualify as anomalies worth investigating.

These analytics serve as an early warning system for both internal fraud and external threats. The Bank of Israel has issued alerts about misuse of bank account details and credit card information, underscoring the real-world risk of unauthorized payment activity. When your detection system can flag a sudden change in a vendor’s bank account immediately — rather than during a quarterly audit — the difference between prevention and recovery becomes the difference between retaining funds and chasing them.

Did You Know

According to the Association of Certified Fraud Examiners, the median duration of a payment fraud scheme before detection is 12 months. Real-time anomaly detection can compress that window from months to minutes, dramatically limiting financial exposure.

Which Data Fields Are Critical for Effective Monitoring?

The accuracy of any detection system depends directly on the quality and breadth of the data fields it examines. Relying on invoice number alone is a recipe for missed duplicates. A comprehensive approach monitors a combination of “strong” identifiers and “soft” contextual fields.

| Field Category | Specific Fields | Detection Value |

|---|---|---|

| Strong Identifiers | Bank Account / IBAN, Invoice Amount + Currency, Vendor Tax ID | High — direct match or near-match produces reliable flags |

| Document References | Invoice Number, PO Number, Goods Receipt Note | High for PO-based processes; variable for non-PO spend |

| Temporal Data | Invoice Date, Payment Due Date, Posting Date | Medium — overlapping or suspiciously close dates raise confidence |

| Soft Identifiers | Vendor Name, Address, Line-Item Descriptions | Supportive — critical when strong identifiers are missing or inconsistent |

Monitoring changes to vendor master data — such as bank account updates or address modifications — is equally important. The Israeli Tax Authority provides a vendor invoice verification service that allows organizations to validate invoice details against official records, reinforcing the principle that verification should happen before payment, not after. Platforms like Detelix continuously cross-check vendor master changes against transaction patterns, adding a proactive layer that catches suspicious modifications before they lead to misdirected funds.

Tip

Establish automated alerts for any change to a vendor’s bank account details within your ERP. Require secondary approval for the first payment made after a bank account modification — this single control prevents a large share of business email compromise (BEC) losses.

A Scenario That Illustrates Why Rules Alone Are Not Enough

Imagine a mid-size manufacturer with 400 active vendors. A procurement clerk creates a new vendor record for “Johnson Electric Co.” without realizing that “Johnson Electrical Company” already exists in the system under a slightly different name and a different internal ID. Over the next quarter, invoices from both records accumulate. The amounts differ slightly because of rounding and currency conversions, and the invoice numbers are entirely distinct. Standard rules-based checks find nothing wrong.

A detection system with fuzzy matching and anomalous transaction analytics, however, would flag the overlap in vendor names, note the similar IBAN structures, and identify that cumulative spending across both records exceeds the category budget by 18%. This is the operational reality that justifies combining duplicate detection with behavioral anomaly analysis — the two capabilities reinforce each other to catch what either one alone would miss.

Did You Know

Vendor master file duplication rates in large ERP systems typically range between 1% and 5% of total vendor records. Each duplicate vendor record creates a separate pathway for undetected double payments, multiplying the financial risk with every new entry.

Your ERP catches exact matches. Detelix catches everything else — fuzzy duplicates, behavioral anomalies, and vendor master manipulation. See how continuous monitoring protects your payment integrity.

How to Implement a Real-Time Financial Leak Prevention Strategy

Implementing effective detection does not require a multi-year IT transformation. The practical workflow follows a clear sequence: connect a data source, normalize and enrich the data, apply detection logic, route alerts for review, and measure outcomes. The key is starting with a focused scope and expanding methodically.

The Detection Workflow in Practice

Data ingestion begins by connecting to the ERP’s accounts payable module or payment file output. The system normalizes vendor names, standardizes currency formats, and removes formatting inconsistencies. Detection rules and similarity algorithms then scan every incoming invoice and every pending payment against the full transaction history. When a potential duplicate or anomaly is identified, it is scored by severity and routed to the appropriate reviewer with a clear explanation of why the flag was raised.

Where Detelix Fits into This Workflow

Detelix integrates directly with ERP environments to perform continuous, real-time monitoring across sensitive financial processes. Rather than generating a batch report after the fact, the platform flags issues as transactions enter the system — before the payment file is finalized. This approach shifts the organization from reactive recovery to proactive prevention. For organizations concerned about revenue-side leakage as well, Detelix extends monitoring to areas like automated pricing and discount monitoring, ensuring that financial integrity is maintained on both sides of the ledger.

Tip

Begin your implementation by focusing on your top 50 vendors by spend volume. These accounts represent the highest financial exposure and will generate the most impactful early results — building organizational confidence in the system before expanding coverage.

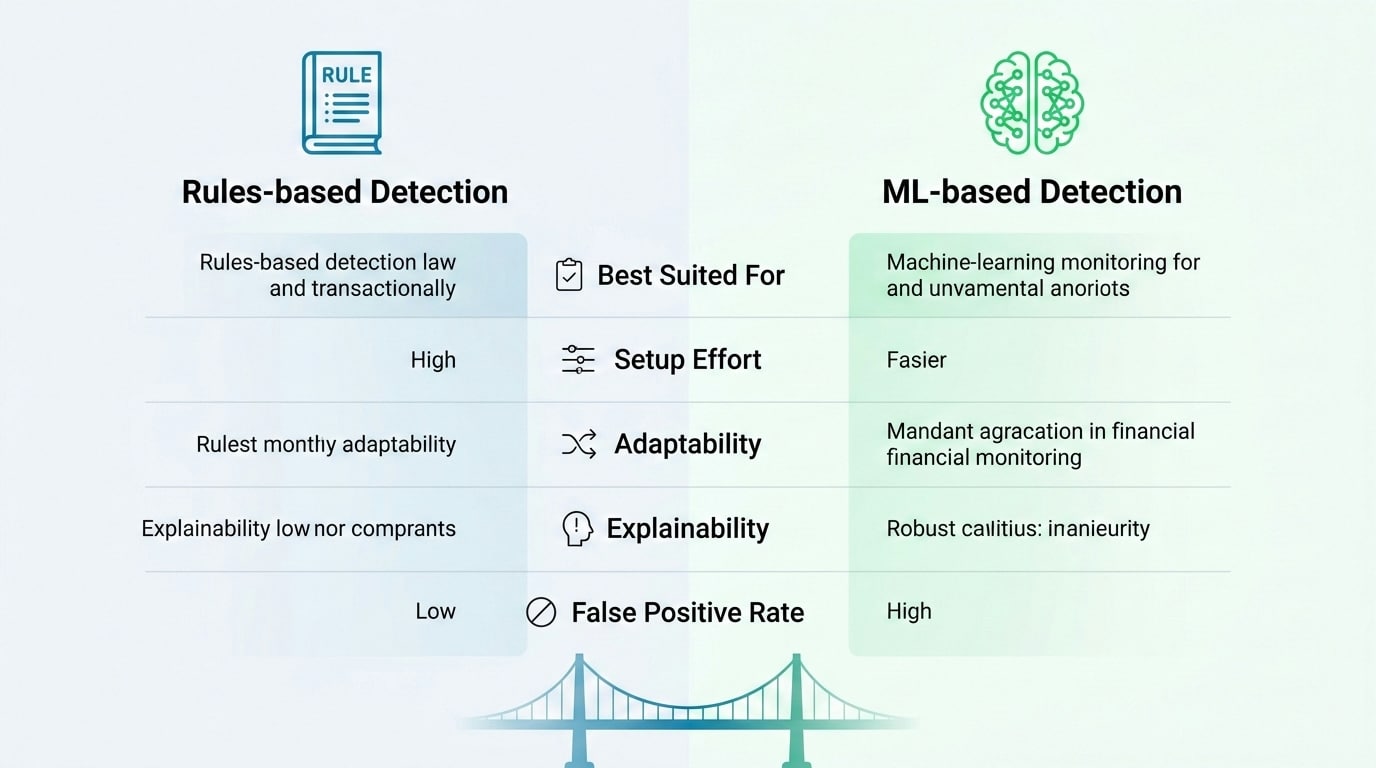

Rules-Based Detection Compared to Machine-Learning Approaches

| Criterion | Rules-Based Detection | ML-Based Anomaly Detection |

|---|---|---|

| Best suited for | Known patterns: exact duplicates, policy thresholds, mandatory field checks | Unknown patterns: behavioral shifts, complex multi-field combinations, evolving fraud tactics |

| Setup effort | Lower — define rules based on known risks | Moderate — requires historical data and model training |

| Adaptability | Manual updates needed when business processes change | Learns from new data; adapts over time |

| Explainability | High — each flag traces to a specific rule | Variable — depends on model transparency and scoring logic |

| False positive rate | Can be high if rules are too broad | Generally lower with proper tuning, but requires feedback loops |

The most effective implementations combine both approaches. Rules handle the clear-cut scenarios — same vendor, same amount, same date — while machine-learning models surface the subtle, previously unseen anomalies that no one thought to write a rule for. This layered strategy is what transforms payment monitoring from a checkbox exercise into genuine financial control.

Did You Know

Organizations that layer machine-learning anomaly detection on top of rules-based systems report detecting 30% to 40% more suspicious transactions than those relying on rules alone. The incremental findings typically include split payments, round-tripping schemes, and vendor collusion patterns.

How to Reduce False Positives Without Missing Real Duplicates

A detection system that generates hundreds of unactionable alerts every week quickly loses the trust of the finance team. Reducing false positives while maintaining high detection coverage requires a deliberate approach. Risk scoring assigns a weighted severity to each flag based on how many matching fields align, the dollar amount at stake, and the vendor’s risk profile. A $50 alert on a trusted, long-standing supplier scores differently than a $50,000 alert on a newly onboarded vendor with a recently changed bank account.

Dynamic thresholds adjust sensitivity by spend category and vendor type. Managed exception lists — whitelists with expiration dates — allow routine transactions to pass without generating noise, while the system still monitors for anomalies within whitelisted patterns. Critically, every analyst decision (confirm, dismiss, escalate) feeds back into the scoring model, creating a continuous improvement loop. Detelix builds this feedback mechanism directly into its alert workflow, so the system becomes more precise with every review cycle rather than remaining static.

Tip

Review your false positive rate monthly and set a target below 20%. If the rate exceeds that threshold, examine whether the noise is concentrated in specific vendor categories or transaction types — then adjust thresholds for those segments rather than reducing sensitivity globally.

Assessing the ROI of Automated Detection Systems

Measuring the return on investment for duplicate payment and transaction anomaly detection requires tracking both direct and indirect value. Direct savings include the total dollar amount of duplicate payments blocked before execution and funds recovered from overpayments identified after the fact. Indirect savings encompass reduced dependency on expensive recovery audit firms, fewer hours spent by AP staff on manual spot checks, and lower audit remediation costs.

The Israeli Ministry of Finance has acknowledged the need for technological solutions for managing, controlling, and tracking payments in government projects — a recognition that manual oversight cannot scale. For private-sector organizations, the math is straightforward: if a system prevents even a fraction of a percent of annual disbursements from being duplicated, the cost of the platform is recovered many times over.

Pre-Payment Metrics Versus Post-Payment Metrics

Pre-payment blocking is the highest-value metric because the money never leaves the organization. Track the count and cumulative amount of payments stopped before the payment run. Post-payment recovery — while still valuable — involves vendor negotiations, credit notes, and processing time. Additional KPIs to monitor include average alert resolution time, false positive rate trend over quarters, percentage of total spend covered by automated checks, and reduction in policy violations over time.

Did You Know

The cost of recovering a duplicate payment after it has been executed is estimated at 10 to 15 times the cost of preventing it in the first place — factoring in staff time, vendor communication, credit note processing, and the opportunity cost of delayed cash flow.

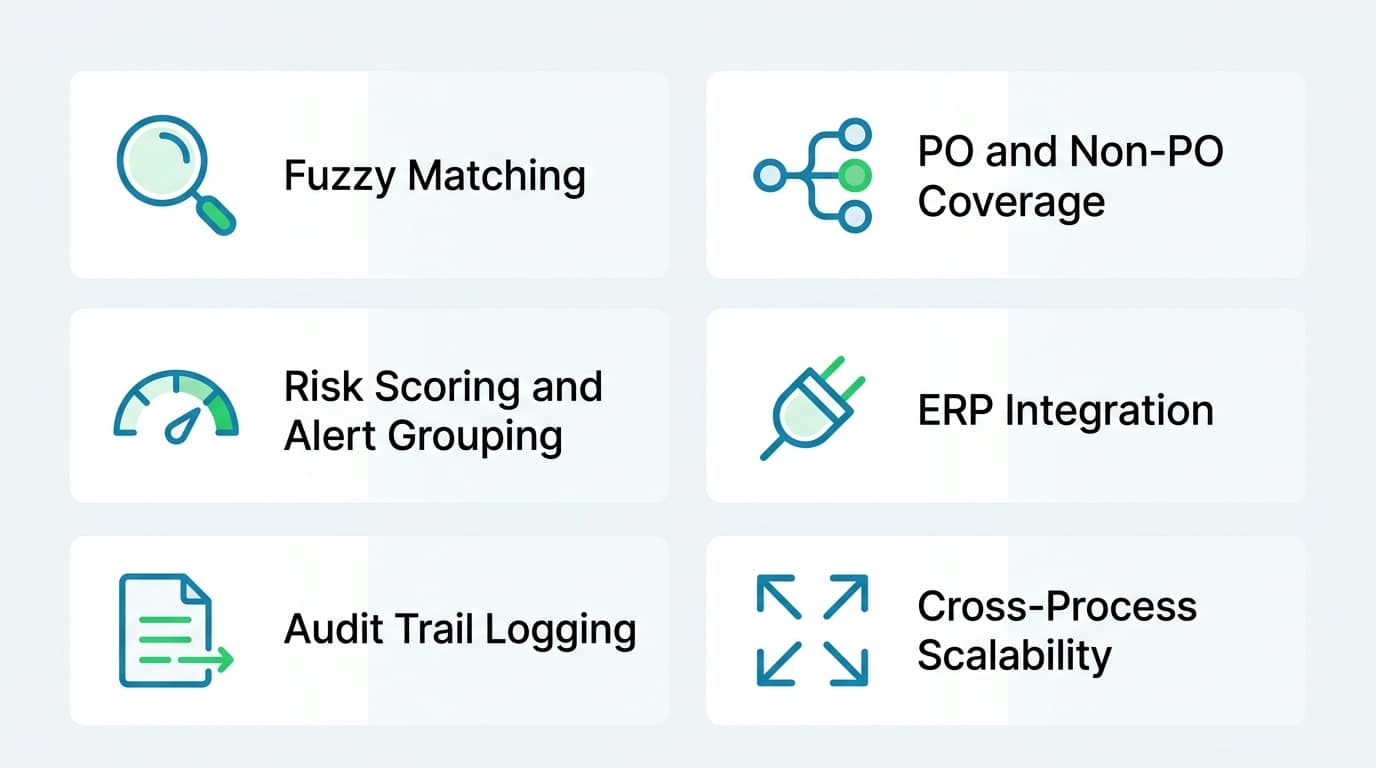

What to Evaluate When Choosing a Detection Solution

Not every tool that claims to detect duplicates delivers the same depth of protection. When evaluating solutions, focus on capabilities that directly affect detection quality, operational efficiency, and auditability. Below is a practical checklist mapped to real business needs.

| Business Need | What to Look For in a Solution |

|---|---|

| Catch near-duplicates, not just exact matches | Fuzzy matching across multiple fields with configurable similarity thresholds |

| Cover both PO and non-PO spend | Flexible detection logic that adapts when purchase orders or goods receipts are unavailable |

| Minimize analyst fatigue | Risk scoring, alert grouping, and clear explanations for every flag |

| Integrate without disrupting operations | Direct ERP connectors with non-intrusive, read-level access — no changes to core system |

| Maintain audit trail | Full logging of every alert, decision, and exception with timestamps and user IDs |

| Scale across processes | Ability to extend monitoring to payroll, vendor master changes, procurement, and refunds |

Detelix addresses these requirements by functioning as an independent control layer over the ERP. It connects to existing data without altering workflows, applies both rule-based and behavioral detection logic, and provides finance leaders with a real-time dashboard that shows exactly what is happening across sensitive payment processes — turning the aspiration of full visibility into an operational reality.

Tip

During vendor evaluation, request a proof-of-concept using your own historical payment data. A credible solution provider will demonstrate detection results against your actual transactions — not just a generic demo dataset — so you can quantify the value before committing.

Detelix Financial Control Solutions

Proactive Monitoring

Continuous, real-time surveillance of sensitive financial processes to detect irregularities before they escalate into losses.

Real-Time Alerts

Instant notifications when duplicate payments, anomalous transactions, or policy violations are detected across your payment workflows.

GateKeeper

An automated pre-payment validation layer that blocks suspicious transactions before funds are released from your organization.

Experience & Expertise

Decades of domain knowledge in financial controls, ERP integration, and fraud prevention — applied directly to your organization’s risk profile.

See Detelix in Action

Frequently Asked Questions

Can automated detection replace traditional financial audits?

Automated detection does not replace audits — it transforms them from periodic, backward-looking exercises into continuous, real-time oversight. Instead of reviewing a sample of transactions months after the fact, your system pre-filters and flags issues as they occur. Auditors can then focus their expertise on investigating confirmed anomalies rather than hunting for needles in a data haystack. The result is a more efficient audit process with higher coverage and faster resolution.

How do detection systems handle multiple currencies and international vendors?

Effective systems normalize currency values to a base denomination at the time of comparison, accounting for exchange rate fluctuations within a defined tolerance. For international vendors, the platform standardizes name formats, addresses, and banking identifiers (IBAN, SWIFT) to ensure that cross-border transactions receive the same level of scrutiny as domestic payments. Without this normalization, organizations with global supply chains face significant blind spots.

Is it possible to detect anomalies in employee expense reports and corporate card transactions?

Yes. The same detection principles — duplicate identification, behavioral baselines, and policy compliance checks — apply to expense claims and corporate card statements. Common findings include the same receipt submitted by different employees, personal charges disguised as business expenses, and round-number claims that exceed per-diem limits. Extending detection to these areas closes a frequently overlooked leakage channel.

What happens when a duplicate is discovered after payment has already been executed?

Post-payment discovery triggers a recovery workflow: the finance team generates a debit memo or credit request, contacts the vendor with supporting documentation, and tracks the refund through to completion. While recovery is possible, it is significantly more costly and time-consuming than pre-payment prevention. This is precisely why real-time detection — catching the issue before the payment file is sent to the bank — delivers the highest operational and financial value.

Ready to Close the Gap Between Perceived Control and Actual Control?

Every payment run is an opportunity to prevent losses — or an undetected risk. Let Detelix show you what your current systems are missing with a real-data proof of concept.