Turn Your ERP Controls Into Active Fraud Protection

Detelix helps finance, IT, and audit teams move from paper checklists to real-time detection across SAP, Oracle, Priority, and more. Talk to an expert about your control environment.

- What an ERP Fraud Prevention Checklist Actually Does

- Why ERP Systems Are a Primary Target for Enterprise Fraud

- The Essential Controls Every ERP Security Checklist Must Include

- Separation of Duties: The Structural Barrier Against Fraud

- User Access Reviews and the Principle of Least Privilege

- Securing Master Data Before It Becomes a Payment Problem

- Audit Trails and Real-Time Monitoring

- Red Flags That Should Trigger Immediate Review

- Preventing Fraud in the Procure-to-Pay Cycle

- Mitigating Fraud in the Order-to-Cash Cycle

- Business Needs and How Detelix Supports Real Control

- Common Mistakes Organizations Make

- How to Conduct an ERP Fraud Risk Assessment

- Testing Whether Your ERP Controls Actually Work

- Continuous Oversight and Governance

- A Practical Checklist for Immediate Action

- Frequently Asked Questions

In many organizations, ERP systems look fully protected on paper. There are user roles, approval flows, reconciliations, and periodic audits. But when fraud occurs, it rarely announces itself through obvious signals. It slips quietly through gaps between departments, through excessive permissions, through manual overrides, and through master data changes that nobody reviewed in time. An ERP fraud prevention checklist is the structured tool that turns scattered controls into a coherent defense layer — one that your finance, IT, and audit teams can actually operate, measure, and improve over time.

Key Takeaways

- An effective ERP fraud prevention checklist translates abstract controls into concrete, owned, and evidence-backed tasks.

- Segregation of duties, least-privilege access, and master data governance are the structural pillars of fraud prevention.

- Most sophisticated ERP fraud hides in master data changes, approval overrides, and threshold-splitting patterns.

- Continuous monitoring dramatically narrows the window between a suspicious event and the response to it.

- Controls are only real when they have an owner, a review cadence, documented evidence, and a remediation path.

What an ERP Fraud Prevention Checklist Actually Does

An ERP fraud prevention checklist is not a generic security document. It is a living operational map that translates abstract control principles into concrete, verifiable tasks: who reviews what, how often, with what evidence, and what happens when an exception is found. A strong checklist covers access permissions, segregation of duties, master data integrity, audit trails, and continuous monitoring across sensitive business processes.

The value is practical. Instead of relying on memory or on once-a-year audit cycles, teams gain a structured roadmap that reduces blind spots. For platform-specific environments, organizations often combine a broad checklist with a focused framework such as an SAP internal controls audit checklist, ensuring that both general principles and platform-specific risks are addressed. Regulatory guidance reinforces this approach, emphasizing the need for a systematic process to identify, evaluate, and treat IT risks rather than relying on ad-hoc reviews, as detailed in the State Comptroller’s report on government IT risk management.

Tip

Before drafting a new checklist, list every sensitive action a user can perform end-to-end in your ERP without a second person involved. Anything on that list is a priority control gap, regardless of how mature the rest of the program is.

Why ERP Systems Are a Primary Target for Enterprise Fraud

ERP platforms concentrate the most sensitive assets an organization has: vendor master data, payment instructions, procurement approvals, payroll, inventory, and financial reporting. That concentration is exactly what makes them attractive to both internal and external actors. A single user with broad permissions, a weak approval chain, or an unmonitored master data change can redirect payments, hide manipulation, or create fictitious vendors that look completely legitimate inside the system.

The classic fraud triangle — pressure, rationalization, and opportunity — plays out inside ERPs primarily through opportunity. Every excessive permission, every unreviewed override, and every ignored log entry is an opportunity. Audit findings from the State Comptroller’s review of computerized information protection repeatedly show deficiencies in access permission management and insufficient monitoring of sensitive data — the exact gaps that a disciplined enterprise fraud controls program is designed to close.

Did You Know

In many documented internal fraud cases, the perpetrator held legitimate credentials for months or years before the scheme was discovered. The breach was not of the system — it was of the control environment that failed to detect routine misuse of approved access.

The Essential Controls Every ERP Security Checklist Must Include

Before diving into process-specific risks, leaders should verify that the foundational layer is in place. An effective ERP security checklist starts with identity and access fundamentals and extends outward to configuration, patching, and monitoring. Multi-factor authentication, session timeouts, password policies, and hardened configurations are baseline — not endpoints. They reduce the risk of account takeover but do nothing to prevent misuse by a legitimate user with excessive rights.

Foundational controls must also protect the confidentiality, integrity, and availability of core data, a principle reinforced across official cyber and information security guidance for sensitive systems.

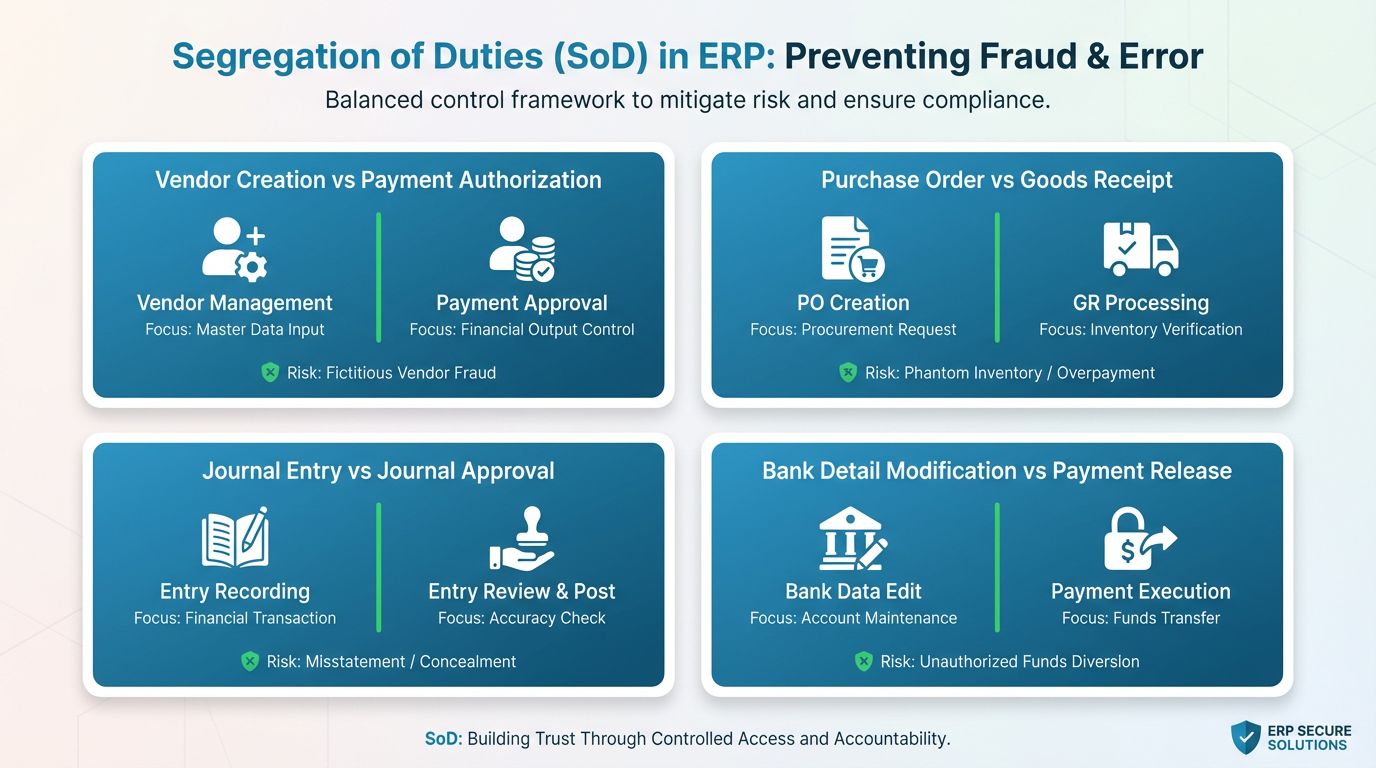

Separation of Duties: The Structural Barrier Against Fraud

Segregation of Duties (SoD) is the single most effective structural control against internal fraud. The principle is simple: no one person should be able to initiate a transaction, approve it, and conceal it. In ERP terms, that means the user who creates a vendor should not be the one who approves a payment to that vendor. The user who enters a purchase order should not be the one who confirms goods receipt for it.

Common SoD Conflicts to Audit Immediately

Vendor creation combined with payment authorization. Purchase order entry combined with goods receipt. Journal entry creation combined with journal approval. Bank detail modification combined with payment release. Each of these combinations, even in a single user, creates a direct path to undetected fraud.

Compensating Controls for Smaller Teams

Where full SoD is structurally impossible, compensating controls must take over: mandatory independent review of every transaction above a defined threshold, automated alerts on conflicting actions performed by the same user, and monthly reconciliation with evidence retained. Audit reports on fraud prevention consistently highlight weak SoD as a recurring failure, as documented in the State Comptroller’s report on preventing embezzlement and fraud in municipal corporations.

Tip

When full SoD is not achievable, document the compensating control precisely: who performs the independent review, by when, using what evidence, and where that evidence is stored. A compensating control without a written owner is not a compensating control — it is a gap.

User Access Reviews and the Principle of Least Privilege

The Principle of Least Privilege means every user receives exactly the access required to perform their role — nothing more. In practice, privilege creep is one of the most common findings in ERP audits: long-tenured employees accumulate permissions as they change roles, former employees retain active accounts, and service accounts operate with administrator rights that were never reviewed.

A disciplined user access review identifies orphaned accounts, dormant high-privilege users, conflicting role combinations, and temporary access that was never revoked. Access must be removed immediately upon termination or role change — not at the next quarterly review. Regulatory guidance on data protection strongly reinforces the “need to know” principle as a cornerstone of information security.

Did You Know

Privilege creep is most common among employees who transfer internally. Because the new role is added without the old permissions being removed, tenured staff often hold the broadest access in the organization — and are rarely flagged in a standard access review.

Securing Master Data Before It Becomes a Payment Problem

Master data is the quiet battlefield where most sophisticated ERP fraud takes place. A small change to a vendor’s bank account number, made shortly before a scheduled payment run, can divert funds to an attacker with almost no visible trace. Payment terms, credit limits, tax identifiers, and contact details are all high-risk fields that deserve the same scrutiny as financial transactions themselves.

High-Risk Master Data Fields to Monitor

Bank account numbers and payment instructions. Vendor status (active/blocked). Payment terms and discount terms. Credit limits and risk categories. Contact emails used for confirmation workflows. Any change to these fields should trigger a mandatory workflow with dual approval and independent verification against an external source — not just against another internal record.

Tip

Verify vendor bank changes by calling a phone number already on file from a previous verified interaction — never the number provided in the change request itself. Attackers frequently supply a number they control alongside the new bank details.

Audit Trails and Real-Time Monitoring

An ERP fraud prevention checklist is only as strong as the evidence it can produce. Without a complete, tamper-resistant audit trail, you cannot investigate incidents, prove accountability, or detect patterns. Essential logs include login attempts, permission changes, master data modifications, manual journal entries, approval overrides, and transactions executed outside normal business hours.

The most effective monitoring connects technical events to business risk. A change to a vendor’s bank details three hours before a payment run is not just a log entry — it is a red flag. Multiple payments structured just below an approval threshold are not just transactions — they are a pattern. The State Comptroller’s review of information security in government databases emphasizes log retention and review as a regulatory baseline, not an optional enhancement.

Red Flags That Should Trigger Immediate Review

Certain patterns repeat across fraud investigations with striking consistency. Knowing them in advance allows teams to build detection rules rather than react after losses occur.

| Red Flag Scenario | Typical Risk | Recommended Action |

|---|---|---|

| Bank details changed close to payment run | Payment diversion | Hold payment, verify by independent channel |

| Split invoices below approval threshold | Approval bypass | Aggregate review, adjust threshold rules |

| New vendor paid within days of creation | Ghost vendor scheme | Independent vendor verification |

| Admin activity outside business hours | Unauthorized access or abuse | Forensic log review |

| Manual journal entries near period close | Financial statement manipulation | Independent approval and documentation |

Wondering if these red flags are already firing inside your ERP — and simply going unseen? Let our team review your control landscape and show you exactly where the blind spots are.

Preventing Fraud in the Procure-to-Pay Cycle

The Procure-to-Pay (PTP) cycle is where most financial fraud actually materializes. Fictitious invoices, duplicate payments, inflated pricing, bid-rigging, and ghost vendors all live inside this flow. Three-way matching — aligning purchase order, goods receipt, and invoice — remains the most effective preventive control, but only when exceptions cannot be silently overridden.

Manual payment overrides deserve special attention. They should be rare, fully documented, approved by someone outside the payment chain, and reviewed independently every month. Any vendor created and paid within a short window should be automatically flagged for verification before funds leave the organization.

Did You Know

Ghost vendor schemes often use real business registration numbers purchased or reused from legitimate inactive companies. Standard “does the vendor exist?” checks pass — which is why independent verification against tax authorities or banking confirmations matters far more than a name search.

Mitigating Fraud in the Order-to-Cash Cycle

The Order-to-Cash (OTC) cycle carries its own fraud profile: unauthorized credit memos, excessive discounts, unjustified write-offs, manipulated pricing, and concealment of inventory theft through adjustments. Controls should focus on who can issue credits, who can override pricing, who can write off receivables, and how those actions are reviewed.

Frequent reconciliation between sales records, shipments, and cash receipts is essential. Customer credit limit changes, particularly upward adjustments, should require documented justification and independent approval. Manual transactions that bypass the standard workflow deserve the highest level of scrutiny.

Tip

Review the top ten users by credit memo issuance every month. Concentration of credit activity in a small number of accounts is one of the clearest warning signs of receivables manipulation and should be explained, not assumed.

Business Needs and How Detelix Supports Real Control

Checklists define what should happen. The harder question is whether those controls are actually operating in real time. The table below maps common business needs to the practical value organizations gain from a real-time control layer.

| Business Need | How Real-Time Control Helps |

|---|---|

| Detect suspicious master data changes before payment | Continuous cross-checks on vendor and bank detail modifications with immediate alerts |

| Catch SoD conflicts that emerge over time | Ongoing analysis of permission combinations rather than annual snapshots |

| Reduce dependence on manual review | Automated detection of threshold splits, duplicates, and off-hours activity |

| Strengthen audit readiness | Structured evidence and documented exception handling available on demand |

| Give leadership real visibility | Clear alerts tied to business risk, not only technical events |

Common Mistakes Organizations Make in ERP Fraud Prevention

The most frequent mistake is treating the checklist as generic rather than tailored to actual processes. Copy-paste frameworks rarely match how procurement, finance, and operations truly work in a specific organization. The second common mistake is focusing almost entirely on IT security — MFA, patches, passwords — while leaving process-level controls like SoD, master data workflows, and transaction monitoring under-reviewed.

Other recurring failures include one-time reviews instead of continuous oversight, unclear ownership of each control, and absence of documented exception handling. A control without an owner is a control that will quietly erode.

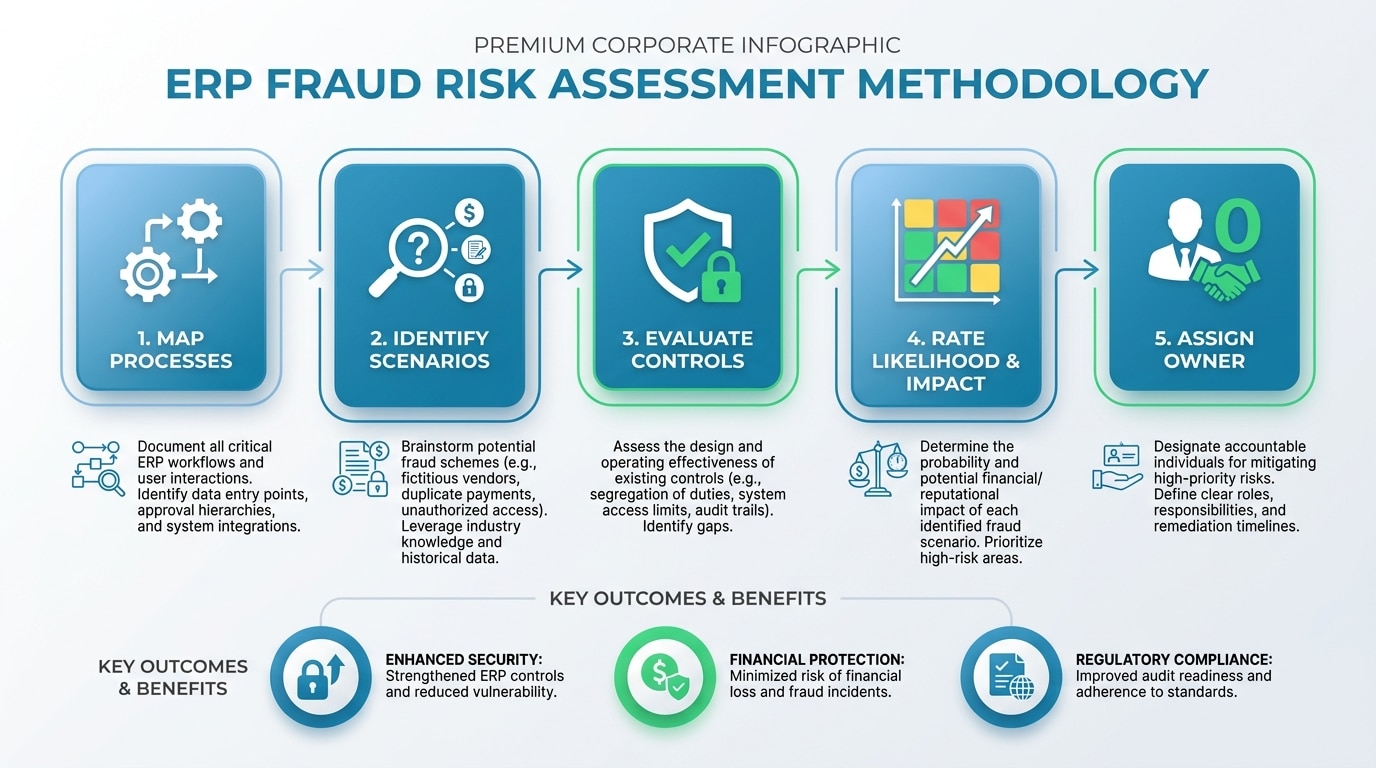

How to Conduct an ERP Fraud Risk Assessment

A meaningful fraud risk assessment starts with the business, not the system. Map the sensitive processes first: payments, vendor onboarding, credit memos, journal entries, payroll, inventory adjustments. For each, identify realistic fraud scenarios — not theoretical ones. Then evaluate which controls exist, which are operating effectively, and where the gaps are.

Rate each gap by likelihood and impact. Assign an owner. Define a remediation timeline. And most importantly, define how you will verify that the new control actually works — not just that it was documented.

Did You Know

Fraud risk assessments that begin with the IT system rather than the business process routinely miss the highest-impact scenarios. Process-first mapping consistently surfaces risks that a purely technical review never reaches.

Testing Whether Your ERP Controls Actually Work

Defining a control and operating a control are two different things. Testing effectiveness requires walkthroughs, sampling of real transactions, comparison between policy and actual behavior, and analysis of cases where the workflow was bypassed. Design effectiveness asks whether the control would work if followed. Operating effectiveness asks whether it is followed in practice.

Evidence matters. A control without evidence of execution cannot be relied on by auditors, regulators, or leadership — and cannot be trusted to prevent loss.

Continuous Oversight and Governance Across Finance, IT, and Audit

Fraud prevention fails when it belongs to no one. Finance owns the transactional risk. IT owns the platform and access layer. Internal audit owns independent assurance. None of them can succeed alone. A governance framework defines how they coordinate — who reviews what, how exceptions are escalated, and how controls evolve as the business changes.

The shift most organizations need to make is from periodic snapshot audits to continuous controls monitoring, where sensitive activity is reviewed as it happens rather than months later. Strategic IT governance frameworks, such as those described in official government IT governance guidance, emphasize exactly this cross-departmental coordination as a structural requirement.

A Practical Checklist for Immediate Action

A usable checklist should contain, for each control: a clear description, an owner, a risk rating, a review frequency, the required evidence, and the remediation path when a gap is found. The table below summarizes the priority items most organizations should validate first.

| Control Area | Priority Check | Suggested Frequency |

|---|---|---|

| User access | Orphaned accounts, admin rights, privilege creep | Quarterly |

| Segregation of duties | Conflicting role combinations | Quarterly |

| Master data | Bank detail and vendor status changes | Continuous |

| Payments | Threshold splits, duplicates, off-hours activity | Continuous |

| Journal entries | Manual entries near period close | Monthly |

| Audit logs | Permission changes and override events | Continuous |

Detelix ERP Fraud Prevention Solutions

Proactive Monitoring

Continuous oversight across sensitive ERP processes — access, master data, and transactions — so exceptions surface as they happen, not months later.

Real-Time Alerts

Business-risk-driven alerts on suspicious master data changes, threshold splits, and off-hours activity, delivered to the right owners for fast response.

Gatekeeper Controls

Preventive guardrails for vendor onboarding, bank detail changes, and payment release — stopping high-risk actions before funds leave the organization.

Expert Experience

Decades of hands-on ERP audit and fraud-prevention expertise across SAP, Oracle, Priority and more — applied to your actual processes, not a template.

See Detelix in Action

Frequently Asked Questions

What is the fastest way to start an ERP fraud prevention checklist?

Begin with the highest-risk areas: user access, segregation of duties, master data changes, and payment controls. Document what exists today, identify the most obvious gaps, and assign an owner to each. A focused starting point is far more effective than a comprehensive framework that nobody operates.

How do you identify high-risk access permissions?

Look for administrator rights, cross-process permissions, permissions that enable both transaction creation and approval, and accounts belonging to former employees or inactive users. Any permission that allows a user to complete a sensitive action end-to-end deserves immediate scrutiny.

What is the difference between preventive and detective controls?

Preventive controls stop a risk before it occurs — approval workflows, SoD rules, and access restrictions. Detective controls identify a risk after it has happened — audit logs, exception reports, and reconciliations. A mature program uses both, because prevention is never absolute and detection alone is too late.

Does a small business need the same ERP controls as a large enterprise?

The principles are identical; the implementation scales. Smaller organizations may not achieve full SoD, but they must compensate with independent reviews, dual approvals for sensitive actions, and disciplined monitoring of exceptions. The risk does not shrink with company size.

How often should SoD conflicts be reviewed?

Structural SoD should be reviewed at least quarterly, and whenever roles are modified or employees change positions. Continuous monitoring of conflicting actions performed by the same user adds an essential real-time layer between reviews.

How can technology automate fraud detection within an ERP?

Automated platforms can continuously cross-check master data changes, monitor permission conflicts, flag transactions that match known fraud patterns, and alert the right people in real time. This moves organizations from periodic review to ongoing control, reducing both the window of opportunity and the cost of investigation.

Is MFA enough to prevent ERP fraud?

No. MFA reduces the risk of account takeover but does not address misuse by legitimate users with excessive permissions, weak process controls, or unreviewed master data changes. It is a necessary baseline, not a complete defense.

Move From Checklist to Real Control

If your ERP controls look strong on paper but you cannot see exceptions the moment they occur, it is time to close that gap. Talk to Detelix about turning your checklist into active, continuous protection.