Stop Fraud Before It Hits Your Bottom Line

Detelix delivers industry-tailored fraud prevention that protects revenue, reduces false positives, and strengthens operational controls across your entire organization.

- Why Universal Fraud Models Create More Problems Than They Solve

- What Is Vertical Fraud Detection and How Does It Differ?

- A Common Mistake: Treating All Sectors as One Risk Pool

- How Fraud Risks Shift Across Key Industries

- Comparing Sector-Specific Fraud Characteristics

- What Technical Capabilities Must an Industry Fraud Prevention Solution Include?

- How Do You Combine Signals to Detect Fraud by Industry?

- How Detelix Strengthens Control Across Business-Critical Processes

- A Scenario That Reveals the Difference Between Monitoring and Control

- Reducing False Positives Without Increasing Exposure

- Which Response Actions Work Better Than Immediate Blocking?

- A Buyer’s Checklist: Evaluating Industry Fraud Prevention Solutions

- How Do You Measure ROI on Fraud Prevention?

- Frequently Asked Questions

Industry specific fraud prevention has become a strategic imperative for organizations operating in competitive, high-velocity business environments. Unlike generic fraud detection tools that apply a single set of rules across every transaction regardless of context, a sector-tailored approach aligns protective controls with the unique workflows, risk profiles, and customer journeys of a specific vertical. When a business relies on broad, one-size-fits-all filters, it often faces a painful trade-off: either block too many legitimate customers and lose revenue, or let too many suspicious actions through and absorb preventable losses. The shift toward business sector fraud prevention reflects a deeper understanding that each industry carries its own threat landscape, and only a control layer designed for that landscape can deliver both protection and operational efficiency.

Key Takeaways

- Generic fraud models produce excessive false positives and miss sector-specific threats because they ignore industry context, customer behavior norms, and unique transaction lifecycles.

- Vertical fraud detection uses machine learning models trained on industry-specific data to achieve higher accuracy and fewer false declines than horizontal alternatives.

- Each sector — retail, banking, insurance, marketplaces, and hospitality — faces distinct fraud patterns that demand tailored signals, thresholds, and response workflows.

- Continuous, real-time monitoring of ERP processes (vendor changes, payroll, payments) catches internal fraud and errors that periodic audits routinely miss.

- Graduated response actions — OTP challenges, brief holds, review queues — preserve customer experience while maintaining strong protection against fraud.

- Measuring fraud prevention ROI requires tracking detection rates, false positive ratios, chargeback trends, and the percentage of transactions requiring manual review.

Why Universal Fraud Models Create More Problems Than They Solve

A horizontal fraud prevention approach treats every sector as though the risks are identical. In practice, the booking window for a hotel reservation and the checkout speed of an e-commerce store create entirely different exposure patterns. When a generic model flags a high-value hotel booking made weeks in advance, it may be applying logic designed for instant-delivery retail — triggering a false positive that damages the guest experience and costs the business a sale. Sector fraud risks vary not only by transaction type but also by customer behavior norms, payment methods, and the timing between purchase and fulfillment.

Tip

Before evaluating any fraud prevention vendor, map your transaction lifecycle from initiation to fulfillment. Identify the moments where fraud risk peaks in your specific workflow — these are the points where generic models most often fail.

The cost of false positives in high-frequency sectors can be staggering. Every wrongly declined transaction represents lost revenue, damaged trust, and potential churn. At the same time, false negatives — fraudulent actions that slip through — accumulate as chargebacks, claims payouts, and regulatory exposure. This is where deep systemic monitoring becomes essential. Platforms like Detelix, whose hundreds of algorithms ensure every action in the ERP system is continuously cross-checked, provide a level of visibility that surface-level transaction filters simply cannot match. The difference lies in understanding the full operational context rather than evaluating isolated data points.

Did You Know

Studies consistently show that false declines cost merchants significantly more than actual fraud losses. For every dollar lost to fraud, businesses lose an estimated $13 to $30 in rejected legitimate orders — revenue that never returns.

What Is Vertical Fraud Detection and How Does It Differ?

Vertical fraud detection refers to the use of machine learning models and rule sets that are trained specifically on data from a single industry. Instead of drawing conclusions from aggregated cross-sector datasets, these models learn what “normal” looks like within a particular ecosystem — banking login patterns, insurance claim frequencies, or marketplace seller behavior. Research into AI-enhanced fraud detection in banking demonstrates that models trained on sector-specific data consistently outperform generic classifiers because they capture nuances that horizontal tools miss entirely.

The practical outcome is more accurate risk scoring. When a vertical model evaluates a banking customer’s wire transfer request, it considers typical transfer sizes, recipient geographies, time-of-day patterns, and historical behavior within that institution’s context. The same model architecture applied to an e-commerce checkout would use entirely different features — cart composition, device fingerprint, shipping-billing address match, and coupon usage velocity. This contextual precision is the foundation of effective industry fraud prevention solutions.

Tip

Ask your fraud prevention vendor which specific features their models use for your industry. If they cannot articulate sector-specific signal weights — velocity thresholds for retail, behavioral biometrics for banking, document similarity for insurance — the solution is likely a generic horizontal tool with a vertical marketing label.

A Common Mistake: Treating All Sectors as One Risk Pool

One of the most frequent errors organizations make is deploying a fraud platform built for a different vertical and expecting it to perform equally well. A system optimized for card-not-present retail fraud will struggle to detect premium diversion in insurance or fictitious vendor schemes inside an ERP-driven procurement process. The signals, thresholds, and response workflows are fundamentally different. Recognizing this mismatch early — before losses accumulate — is a critical step in building a mature fraud prevention program.

Did You Know

According to the Association of Certified Fraud Examiners, organizations that implement proactive, industry-adapted monitoring detect fraud 50 percent faster and suffer median losses that are roughly half those of organizations relying on passive controls.

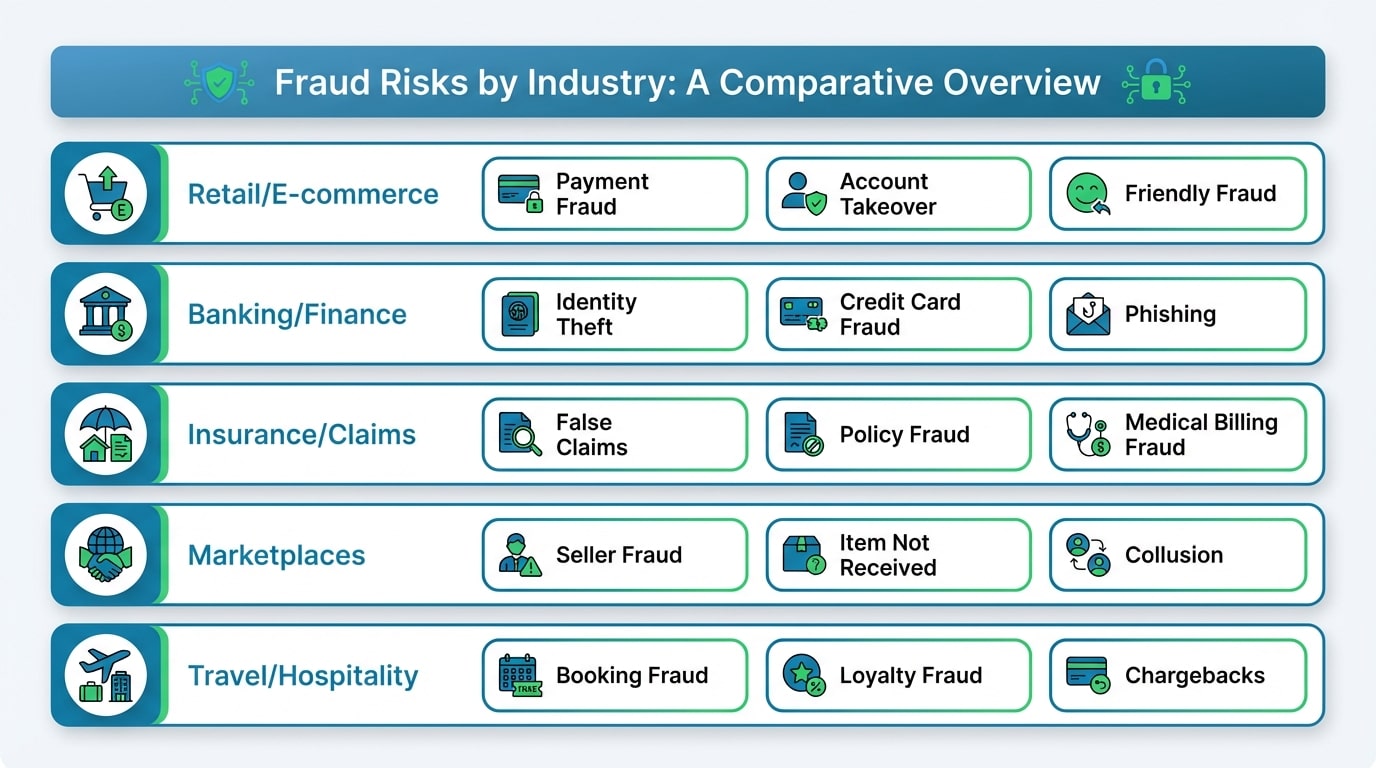

How Fraud Risks Shift Across Key Industries

Retail and E-commerce Exposure Points

The retail sector faces account takeover, payment fraud, promotional abuse, and return manipulation as its primary threats. The most sensitive moments in the customer journey are checkout, address or phone number changes, addition of a new payment method, and refund requests. Fine-tuned ML systems applied to e-commerce environments have been shown to detect up to 95 percent of fraudulent transactions while reducing the volume that requires manual review. The key is applying friction — such as step-up verification — only when the risk score warrants it, so conversion rates remain healthy.

Banking and Financial Services Vulnerabilities

Financial institutions contend with synthetic identity fraud, account opening manipulation, authorized-push-payment scams, and social engineering attacks that make fraudulent actions appear legitimate. Because the consequences of a single missed event can be severe, real-time behavioral analysis combined with device intelligence and network signals is essential. Monitoring transactional anomalies at the pricing and collections level also prevents revenue leakage; Detelix’s Pricing and Discounts Monitoring capability illustrates how continuous oversight of financial pricing structures catches deviations that periodic audits would miss. Regulatory frameworks such as the Bank of Israel’s Directive 411 on AML/CFT and customer identification further underscore the need for robust, real-time controls.

Tip

For financial services teams, integrate your fraud prevention layer directly with your core banking or ERP platform’s API. Real-time access to account history, session context, and transaction metadata dramatically improves risk scoring accuracy compared to batch-based data feeds.

Insurance and Claims Fraud Patterns

Insurance fraud often involves document fabrication, coordinated schemes between policyholders and service providers, and premium diversion by agents. Familial fraud and producer-side embezzlement are particularly difficult to detect in low-touch expense carriers, where verification touchpoints are minimal. The signals that help identify claims fraud include document similarity across submissions, recurring personal details linked to different claimants, suspicious timing of claims relative to policy inception, and hidden relationships between bank accounts, addresses, and phone numbers. An official joint announcement exposing a document forgery ring targeting social insurance benefits demonstrates how sector-specific fraud can persist undetected without process-adapted controls.

Did You Know

Insurance fraud accounts for an estimated 5 to 10 percent of all claims costs across most markets. In property and casualty insurance alone, this translates to tens of billions of dollars in annual losses globally — losses that ultimately drive up premiums for honest policyholders.

Marketplace Fraud: When Both Buyers and Sellers Are Threats

Marketplaces face a dual-sided risk landscape. On the buyer side, account takeover, payment fraud, and refund abuse are common. On the seller side, counterfeit listings, identity spoofing, and triangulation fraud — where a fraudster takes an order, purchases the item with stolen payment credentials, and ships directly to the customer — create complex investigation challenges. Detecting these schemes requires entity resolution: the ability to link accounts, devices, addresses, and behavioral fingerprints across the platform to reveal fraud rings rather than isolated incidents.

The Hospitality and Travel Sector: Long Windows, Late Chargebacks

Travel and hospitality businesses deal with a uniquely extended risk window. A booking made weeks or months before the stay creates a long exposure period during which payment credentials may be reported stolen, chargebacks filed, or loyalty points drained through account takeover. Dynamic risk management that adjusts scores based on time-to-fulfillment and booking value is essential. Monitoring post-booking changes — such as name swaps, room upgrades, or contact detail modifications — adds another layer of protection without disrupting the guest experience.

Comparing Sector-Specific Fraud Characteristics

| Industry | Primary Fraud Types | Key Detection Signals | Typical Response Action |

|---|---|---|---|

| Retail / E-commerce | ATO, payment fraud, refund abuse, promo manipulation | Device fingerprint, velocity, address mismatch | Step-up authentication, order hold |

| Banking / Finance | Synthetic identity, ATO, push-payment scams | Behavioral biometrics, geo anomaly, session risk | Transaction block, OTP, manual review |

| Insurance / Claims | Document forgery, staged claims, premium diversion | Document similarity, entity linkage, timing patterns | Claims triage, investigator routing |

| Marketplaces | Triangulation fraud, seller spoofing, refund abuse | Entity resolution, cross-account linking | Account suspension, payout hold |

| Travel / Hospitality | Booking fraud, loyalty ATO, late chargebacks | Time-to-fulfillment risk, post-booking changes | Dynamic scoring, booking verification |

Is your fraud prevention strategy aligned with your industry’s unique risk profile? Detelix builds sector-aware control layers that catch threats generic tools miss.

What Technical Capabilities Must an Industry Fraud Prevention Solution Include?

An effective solution must combine real-time data streaming, multi-signal risk scoring, configurable rules alongside machine learning models, device and identity intelligence, case management with full audit trails, and the ability to adapt policies per industry and per stage in the customer journey. Entity resolution — linking disparate data points to a single actor — is particularly critical in sectors where fraud rings operate across multiple accounts. Without real-time, day-zero decisioning, organizations are left investigating damage rather than preventing it.

Did You Know

Entity resolution technology can uncover fraud rings that span hundreds of seemingly unrelated accounts. By linking shared device fingerprints, IP addresses, email domains, and shipping addresses, a single investigation can expose coordinated schemes that individual transaction monitoring would never connect.

How Do You Combine Signals to Detect Fraud by Industry?

Effective vertical fraud detection fuses identity signals (email risk, phone verification), device signals (fingerprint, emulator detection), behavioral signals (navigation speed, typing cadence), transactional signals (amount deviation, frequency spikes), and network signals (shared attributes across entities). The weights assigned to each signal category shift depending on the industry context. In banking, behavioral biometrics may carry the highest weight; in e-commerce, device and velocity signals dominate.

Hard Signals Versus Soft Signals

Hard signals are deterministic — document verification, phone carrier lookup, or address validation return a clear pass or fail. Soft signals are probabilistic — typing rhythm, mouse movement patterns, or session duration indicate risk on a spectrum. The most accurate vertical models combine both, using hard signals for gating decisions and soft signals for fine-grained scoring that reduces false positives.

Tip

When calibrating your fraud detection model, start by establishing the baseline weight split between hard and soft signals for your vertical. For banking, allocate roughly 60 percent weight to behavioral and session-based soft signals. For e-commerce, shift 60 percent weight toward device fingerprinting and velocity-based hard signals. Adjust from there based on your own false positive data.

How Detelix Strengthens Control Across Business-Critical Processes

Organizations that operate complex ERP-driven workflows face fraud and error risks that extend well beyond customer-facing transactions. Vendor master changes, payroll adjustments, bank account modifications, and procurement approvals are all sensitive processes where a single unauthorized or erroneous action can cause significant financial damage. Detelix provides a continuous, independent control layer that cross-checks every action against expected patterns and flags deviations in real time — before money leaves the organization. This approach moves teams from after-the-fact investigation to proactive prevention, covering scenarios from employee embezzlement to external payment redirect schemes.

| Business Need | How Detelix Supports It |

|---|---|

| Detect unauthorized vendor bank account changes | Real-time alerts when supplier banking details are modified, with cross-referencing against historical records and external data sources |

| Prevent duplicate or fictitious payments | Automated scanning of payment batches for anomalies, duplicates, and policy deviations before execution |

| Enforce segregation of duties | Continuous monitoring of user actions across ERP roles to identify SoD violations as they occur |

| Identify payroll manipulation | Flagging ghost employees, unusual salary changes, and overtime anomalies through pattern analysis |

| Monitor refund and credit processes | Detecting excessive or irregular refunds and credits that may indicate abuse or collusion |

Tip

Prioritize monitoring the three ERP processes that carry the highest financial risk in your organization first — typically vendor master changes, payment approvals, and user access modifications. A focused rollout on these areas delivers measurable loss reduction within weeks rather than months.

A Scenario That Reveals the Difference Between Monitoring and Control

Consider a mid-sized manufacturing company where a finance clerk modifies a supplier’s bank account details and simultaneously approves a large payment. In a traditional control environment, this might be caught — weeks later — during a reconciliation review. By then, the funds have left the organization. With an industry-adapted real-time control layer, the system flags the combination of a bank account change and a same-day payment approval by the same user as a high-risk event, triggering an immediate alert to the controller. The payment is held for review. The difference between these two outcomes is the difference between managing risk on paper and actually controlling it.

Did You Know

The median duration of occupational fraud schemes is 12 months before detection, according to global fraud research. Organizations with real-time continuous monitoring cut that detection window to days or hours — dramatically reducing cumulative financial damage.

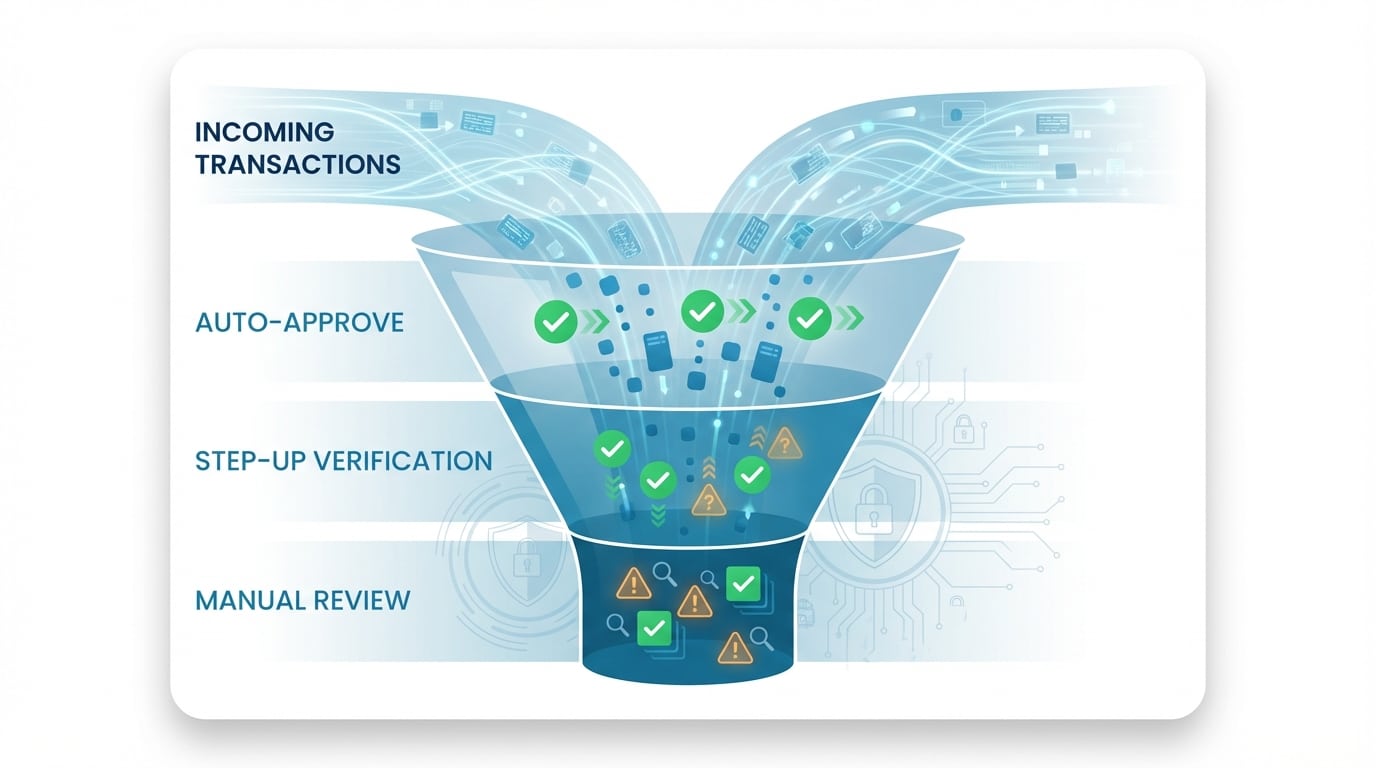

Reducing False Positives Without Increasing Exposure

False positives erode trust in any fraud prevention system. When analysts are overwhelmed with alerts that turn out to be legitimate, they begin to ignore signals — and real fraud slips through. The solution lies in graduated response actions calibrated to sector-specific thresholds. Instead of blocking every suspicious event outright, an effective system applies proportional friction: requesting OTP verification for moderate-risk actions, routing high-risk events to manual review, and auto-approving actions that fall within well-established behavioral baselines.

Which Response Actions Work Better Than Immediate Blocking?

Outright transaction blocks should be reserved for the highest-confidence fraud signals. For everything else, the following graduated responses preserve customer experience while maintaining protection: one-time password challenges, document upload requests, enhanced payer authentication via OTP, brief processing delays that allow for background verification, and routing to a specialized review queue. The right mix of these actions depends on industry norms — what a banking customer expects differs from what a marketplace buyer will tolerate.

Did You Know

Organizations that replace binary block/allow decisions with a three-tier graduated response framework (auto-approve, challenge, block) typically reduce false positive rates by 30 to 50 percent while maintaining or improving their overall fraud catch rate.

A Buyer’s Checklist: Evaluating Industry Fraud Prevention Solutions

| Evaluation Criterion | What to Look For |

|---|---|

| Industry data expertise | Does the provider have models trained on data from your specific vertical? |

| Integration depth | Can the platform connect to your ERP, CRM, and payment systems without extensive custom development? |

| Real-time decisioning | Are risk scores generated before the transaction is finalized, not after? |

| Explainability | Can analysts understand why a specific action was flagged, with clear reason codes? |

| Policy flexibility | Can you adjust thresholds, rules, and workflows without vendor involvement? |

| Audit trail | Does the system maintain a complete, immutable log of every decision and override? |

| Entity resolution | Can it link related accounts, devices, and addresses to identify coordinated fraud? |

| Deployment speed | How quickly can you go from integration to production-level protection? |

Tip

During vendor evaluation, request a proof-of-concept using your own historical data. A provider confident in their vertical expertise will demonstrate measurable improvements in detection accuracy and false positive reduction against your actual transaction patterns — not just a generic demo dataset.

How Do You Measure ROI on Fraud Prevention?

The return on investment from industry specific fraud prevention is measured across several dimensions: direct loss reduction (fewer successful fraud events), operational efficiency (lower manual review volume), customer experience improvement (fewer false declines), and regulatory compliance (reduced exposure to penalties and remediation costs). Key performance indicators include fraud detection rate, false positive rate, average time from alert to resolution, chargeback ratio, and the percentage of transactions requiring manual intervention. Organizations that track these KPIs consistently can demonstrate the financial impact of their fraud prevention investment to executive stakeholders.

Did You Know

A well-implemented industry-specific fraud prevention program typically delivers ROI within the first quarter of deployment. The combination of reduced chargebacks, lower manual review costs, and recovered revenue from fewer false declines often exceeds the total cost of the platform by a factor of three to five within the first year.

Detelix Fraud Prevention Solutions

Proactive Monitoring

Continuous, automated oversight of ERP transactions and business processes to detect anomalies and policy violations before they cause financial damage.

Real-Time Alerts

Instant notifications when suspicious activities or control violations are detected, enabling immediate investigation and response across all business-critical processes.

Gatekeeper

An independent control layer that validates payments, vendor changes, and sensitive transactions against predefined rules before execution — stopping fraud at the gate.

Industry Experience

Decades of domain expertise across banking, insurance, retail, and enterprise sectors — delivering fraud prevention strategies tailored to each vertical’s unique risk profile.

See Detelix in Action

Frequently Asked Questions

What makes industry specific fraud prevention different from general fraud detection?

General fraud detection applies uniform rules and models across all transactions regardless of context. Industry specific fraud prevention tailors its signals, thresholds, and response actions to the unique risk profile and operational workflows of a particular business vertical — resulting in higher accuracy, fewer false positives, and better alignment with customer expectations.

Can a single platform handle multiple industry verticals?

Some platforms offer configurable frameworks that support multiple verticals through modular rule sets and industry-specific ML models. The critical factor is whether the platform allows independent configuration per vertical, rather than forcing all business units into a shared risk logic that dilutes accuracy.

How long does it typically take to deploy an industry-tailored fraud prevention solution?

Deployment timelines vary based on integration complexity and the maturity of existing data infrastructure. Organizations with well-structured ERP and transaction data can often reach production-level protection within weeks. Those requiring significant data normalization or custom integrations may need a phased rollout over several months.

How does fraud prevention connect to regulatory compliance requirements like KYC and AML?

Fraud prevention and compliance are deeply interconnected. Effective customer identification (KYC) reduces account-opening fraud; transaction monitoring supports AML obligations; and audit trails generated by fraud prevention systems provide evidence for regulatory reporting. The Bank of Israel’s KYC and AML directive exemplifies how regulators expect financial institutions to integrate these controls into a unified risk management framework.

What role does behavioral analysis play in vertical fraud detection?

Behavioral analysis captures how a user interacts with a system — navigation patterns, typing speed, session duration, and decision sequences. These soft signals are especially valuable in verticals like banking and insurance, where fraudsters may possess correct credentials but cannot replicate the behavioral fingerprint of a legitimate account holder.

Are Your Controls Preventing Fraud — or Just Documenting It?

If your team spends more time investigating past incidents than stopping active threats, your control environment needs an upgrade. Detelix helps organizations transition from reactive reporting to real-time, sector-aware protection.