Stop Fraud Before It Reaches Your Bottom Line

Detelix delivers industry-calibrated fraud prevention that fits your sector’s exact risk profile. Get expert guidance today.

- What Is Industry Specific Fraud Prevention and Why Does It Outperform Generic Models?

- Why Do Sector Fraud Risks Vary So Significantly?

- How Does Vertical Fraud Detection Work in Practice?

- A Common Mistake: Detection vs. Prevention

- Mapping the Fraud Journey

- Choosing the Right Industry Fraud Prevention Solutions

- Can AI-Driven Models Handle Multiple Verticals?

- Primary Business Sector Fraud Trends This Year

- How to Reduce False Positives Without Losing Revenue

- Comparing Rules-Based and ML-Based Approaches

- What a Vertical Fraud Risk Assessment Requires

- Implementation Timeline

- How to Measure the ROI

- What Risk and Operations Teams Need

- Frequently Asked Questions

In many organizations, fraud prevention still relies on a single set of rules applied uniformly across every department, product line, and customer segment. On paper, this looks efficient. In practice, it creates blind spots that sophisticated attackers exploit ruthlessly. The fraud patterns threatening a retail operation look nothing like those targeting an insurance carrier, a logistics company, or a payroll department. When your controls are generic, the gaps between what your system expects and what actually happens in your specific business environment become an open invitation. Industry specific fraud prevention closes those gaps by calibrating detection, rules, and response protocols to the exact processes, data flows, and risk profiles of your vertical. The result is sharper accuracy, fewer false alarms, and far less damage before anyone notices something is wrong.

Key Takeaways

- Generic fraud controls create exploitable blind spots; industry-specific calibration closes them by aligning detection with your sector’s actual risk profile.

- Vertical fraud detection layers behavioral analytics, device intelligence, and transactional anomaly scoring through an industry-tuned lens, dramatically reducing false positives.

- Each sector has distinct “hot zones” in the fraud journey, from account creation to post-transaction disputes, requiring tailored intervention strategies.

- Blending rules-based controls with ML models provides the optimal balance of auditability, scalability, and adaptability across regulated and high-volume industries.

- Measurable ROI comes from tracking fraud losses prevented, operational cost reductions, and revenue recovered through improved transaction approval rates.

What Is Industry Specific Fraud Prevention and Why Does It Outperform Generic Models?

Industry specific fraud prevention is a structured approach to detecting and stopping fraudulent activity using signals, rules, and models designed around the operational realities of a particular sector. Instead of applying the same thresholds to every transaction regardless of context, a vertical-specific system understands what “normal” looks like in your industry and flags deviations that truly matter.

The practical impact is twofold. First, detection rates climb because the system is trained on patterns relevant to your business sector fraud scenarios, not generic benchmarks. Second, false positives drop significantly because the system does not treat legitimate high-value orders, seasonal spikes, or industry-standard workflows as suspicious. Advanced machine-learning systems tuned for specific verticals can detect up to 95 percent of fraudulent activity while keeping friction for genuine users to a minimum. That balance between protection and usability separates a tailored approach from a one-size-fits-all tool. Where Detelix’s hundreds of algorithms ensure every action in the ERP system is continuously cross-checked, the principle is the same: specificity drives accuracy.

Tip

When evaluating any fraud prevention vendor, ask to see detection benchmarks segmented by your specific industry vertical, not aggregated across all their clients. Aggregated numbers mask performance gaps in your sector.

Why Do Sector Fraud Risks Vary So Significantly Across Different Industries?

The answer comes down to incentives, money trails, and process vulnerabilities. In e-commerce, attackers exploit fast checkout flows to commit card-not-present fraud, return abuse, or promo manipulation. In insurance, the target is often claims diversion, premium fraud, or collusion between agents and policyholders. In manufacturing and supply chain, the risk centers on vendor invoice manipulation, duplicate payments, and inventory theft. Each sector has a different “currency” that fraudsters pursue: cash, goods, loyalty points, sensitive data, or regulatory leverage.

This is precisely why a rule that works well for flagging suspicious refunds in retail may be entirely irrelevant to detecting payroll ghost employees in a services company. The Bank of Israel’s public warning about impersonation fraud illustrates this well: financial institutions face social-engineering attacks that exploit trust in institutional brands, a pattern almost nonexistent in logistics or manufacturing. Understanding sector fraud risks means mapping the specific motivations, methods, and money flows that apply to your vertical.

Did You Know

Financial institutions face impersonation and social-engineering attacks at rates significantly higher than manufacturing or logistics companies, because attackers exploit the inherent trust consumers place in banking brands.

How Does Vertical Fraud Detection Work in Practice?

Vertical fraud detection layers multiple signal types, including device intelligence, behavioral analysis, velocity checks, network-graph relationships, and transactional anomalies, but interprets them through an industry-specific lens. A sudden change in shipping address means something different for a high-value electronics retailer than it does for a SaaS subscription platform. Similarly, an unusual login time triggers different risk scores depending on whether the user is a bank customer or a warehouse operator.

Which Detection Layers Are Common in Vertical Solutions?

Most mature industry fraud prevention solutions combine several layers: hard rules for regulatory compliance and known-bad indicators; statistical and machine-learning models for pattern recognition at scale; behavioral analytics that track how users interact with interfaces; device fingerprinting to identify repeat offenders; graph-based link analysis that exposes coordinated fraud rings; and a case-management layer where analysts investigate, tag outcomes, and feed results back into the system. The key difference from generic tools is that each layer’s thresholds, features, and weightings are calibrated to the vertical’s baseline behavior.

Tip

Map your organization’s baseline behavior for at least 90 days before activating automated blocking rules. This calibration period lets the system learn what “normal” genuinely looks like in your specific environment, preventing a wave of false positives at launch.

A Common Mistake: Treating “Detection” and “Prevention” as the Same Thing

Detection tells you something suspicious happened. Prevention stops damage before it materializes. In an industry context, that distinction is critical because the cost of a wrong decision varies dramatically between sectors. In a high-margin subscription business, blocking a legitimate customer costs future lifetime value. In a payments environment governed by chargeback regulations, letting a fraudulent transaction through triggers financial penalties and reputational harm.

Effective industry specific fraud prevention combines both: it detects anomalies in real time and applies the right intervention for the sector. That might mean step-up authentication for a borderline transaction in banking, a temporary hold for manual review in insurance claims, or an automatic block on a known-bad device in retail. The intervention must fit the industry’s tolerance for friction and its regulatory obligations.

Did You Know

A false decline in e-commerce does not just lose the immediate sale. Research shows that up to 40 percent of customers who experience a false decline will never return to the merchant, making the lifetime revenue impact far greater than the single blocked transaction.

Mapping the Fraud Journey: Which Events Should Your System Capture?

Fraud rarely begins at the moment of payment. It starts earlier, at registration, account recovery, profile changes, or even in support interactions. Mapping your industry’s “fraud journey” means identifying every touchpoint where an attacker could plant a seed, build trust, or extract value.

| Event Stage | Retail / E-Commerce Risk | Financial Services Risk | Enterprise / ERP Risk |

|---|---|---|---|

| Account Creation | Synthetic identity, fake accounts for promo abuse | Identity theft, money-mule onboarding | Unauthorized vendor creation |

| Login / Access | Credential stuffing, bot attacks | Account takeover (ATO) | Privilege escalation, SoD violations |

| Profile Change | Shipping address switch before order | Bank account change before payout | Vendor bank-detail modification |

| Transaction | Card-not-present fraud, triangulation | Unauthorized transfers, premium diversion | Duplicate invoices, inflated amounts |

| Post-Transaction | Return abuse, chargeback fraud | Dispute manipulation | Unauthorized credit notes, inventory write-offs |

Every industry has a different “hot zone” in this journey. Capturing the right events and enriching them with contextual data is the foundation of vertical fraud detection.

Tip

Audit your event-capture pipeline quarterly. Many organizations discover that critical data points, such as profile-change timestamps or device metadata at login, are not being logged. Closing these data gaps is often the single highest-ROI improvement you can make to your fraud detection accuracy.

Choosing the Right Industry Fraud Prevention Solutions: A Practical Checklist

When evaluating solutions, the conversation should move beyond feature lists and focus on operational fit. Here are the criteria that matter most for teams managing sector fraud risks on a daily basis.

First, check whether the platform offers pre-built use-case templates for your vertical. These dramatically shorten deployment time and reflect real-world attack patterns. Second, assess real-time decision-making capability: can the system intervene before money leaves the organization, or does it only generate reports after the fact? Third, evaluate explainability. When a transaction is flagged, can your analysts understand why, and can you justify the decision to a customer or regulator?

Fourth, look at policy simulation and tuning. A strong platform lets you model the impact of a rule change before it goes live, reducing the risk of over-blocking. Fifth, consider how the solution handles pricing anomalies, unauthorized discounts, or financial leakages specific to your domain. Capabilities like ML-Based Fraud Detection for Pricing demonstrate the kind of specificity that generic tools simply cannot offer. Finally, confirm that integration paths (API, SDK, ERP connectors) align with your technology stack.

Did You Know

Organizations using pre-built vertical use-case templates typically reach production-ready deployment 60 to 70 percent faster than those building custom rule sets from scratch, because templates encode real-world attack patterns already validated in the field.

Your fraud risks are unique to your industry. Your prevention strategy should be too. Talk to Detelix about vertical-specific fraud controls built for your operational reality.

Can AI-Driven Models Handle Multiple Vertical Fraud Detection Use Cases?

Yes, but only if the underlying architecture separates the signal layer from the policy layer. A well-designed platform ingests a broad set of signals (device data, behavioral patterns, transactional metadata) through a shared engine, then applies vertical-specific policy “packages” that define what is normal, what is suspicious, and what triggers an intervention. This is fundamentally different from running one generic model and hoping it works for everyone.

The concept of transfer learning in AI allows models pre-trained on large fraud datasets to be fine-tuned rapidly for a new vertical with less data. However, governance matters: each vertical model needs its own performance monitoring, threshold management, and feedback loop. Detelix applies this principle within ERP environments, using dedicated algorithms for processes like supplier payments, bank reconciliation, and payroll, each with its own risk logic and alerting thresholds rather than a single monolithic ruleset.

Tip

When deploying ML models across multiple business units, maintain separate performance dashboards for each vertical. A model that shows 95 percent precision overall may be performing at 80 percent in one critical segment, and aggregated metrics will hide that gap entirely.

What Are the Primary Business Sector Fraud Trends to Watch This Year?

Several converging trends are reshaping the threat landscape across industries. AI-generated deepfakes and synthetic identities are making traditional identity verification less reliable. Automated bot attacks now account for a growing share of account-creation and credential-stuffing attempts in retail and financial services. According to recent reporting on Israel’s National Cyber Directorate data, cyber-related alerts to organizations surged by 350 percent in 2025, a figure that underscores the expanding attack surface.

Collusion between insiders and external actors remains one of the hardest patterns to detect with generic tools, because it mimics normal multi-party workflows. And in the public sector, fraudulent claims and impersonation schemes continue to evolve. Each of these trends reinforces the need for industry-calibrated detection: a bot-detection layer tuned for e-commerce checkout flows operates very differently from one designed to protect ERP procurement processes.

Did You Know

Cyber-related alerts to Israeli organizations surged by 350 percent in 2025 according to the National Cyber Directorate, reflecting an attack surface that is expanding far faster than most organizations’ detection capabilities can keep pace with.

How to Reduce False Positives Without Losing Revenue

False positives are not just an inconvenience. They are a measurable cost. Every legitimate transaction blocked erodes revenue, damages customer trust, and increases operational load on review teams. The path to fewer false positives runs through three practices: graduated decision-making, vertical-specific thresholds, and continuous feedback loops.

Graduated decision-making replaces binary approve/decline logic with a spectrum of responses. Instead of blocking a transaction outright, the system may request additional verification, limit the order value, or route the case for rapid manual review. Vertical-specific thresholds acknowledge that a $2,000 single-item purchase is routine in electronics but unusual in grocery delivery. And feedback loops, where every decision outcome (confirmed fraud, false alarm, or legitimate) is tagged, allow models to retrain on real results, steadily improving precision over time.

Tip

Establish a weekly false-positive review cadence where analysts examine the top 20 declined transactions from the previous week. Consistently feeding these outcomes back into the model creates a compounding improvement in precision that no amount of rule-writing can match.

Comparing Rules-Based and ML-Based Approaches by Industry Context

| Criterion | Rules-Based Approach | ML-Based Approach |

|---|---|---|

| Speed of deployment | Fast — immediate policy enforcement | Requires data collection and training period |

| Adaptability to new patterns | Low — manual updates needed | High — learns from evolving data |

| Explainability | High — logic is transparent | Varies — depends on model type |

| False-positive rate | Higher in complex environments | Lower when properly tuned for vertical |

| Best fit | Regulatory blocklists, hard policy, known-bad indicators | Behavioral anomalies, complex signals, large-scale scoring |

| Risk of evasion | High — attackers learn the rules | Lower — models generalize across variants |

In most industries, the optimal strategy blends both. Rules provide immediate, explainable control over known risks, which is essential for compliance and audit. ML extends detection to novel attack patterns that no rule author anticipated. The balance shifts depending on the sector: heavily regulated industries lean more on rules for auditability, while high-volume digital businesses lean more on ML for scalability.

Did You Know

Attackers routinely reverse-engineer rules-based fraud systems by testing transactions at incrementally different values and patterns. ML models are significantly harder to game because they generalize across attack variants rather than relying on fixed thresholds.

What a Vertical Fraud Risk Assessment Actually Requires

Before choosing or deploying any solution, a structured risk assessment maps where your organization is most vulnerable within your specific industry context. This is not a generic checklist exercise. It requires analyzing your actual transaction data, dispute history, process workflows, and user-behavior patterns to identify which fraud scenarios carry the highest probability and impact.

Useful data inputs include transaction types and volumes, chargeback and dispute rates by segment, refund and return patterns, login and device metadata, address and shipping anomalies, customer tenure and lifetime value, and support-ticket patterns that may indicate social-engineering attempts. The output should be a prioritized risk map that tells your team where to invest first, not a theoretical catalog of every possible threat. Detelix supports this approach by providing continuous visibility into sensitive ERP processes, so the risk assessment is not a one-time snapshot but an evolving picture updated with every transaction.

Tip

Include your customer support team in the risk assessment process. Support agents often see early indicators of fraud, such as unusual account-recovery requests, social-engineering attempts, or patterns in complaint types, that never appear in transactional data alone.

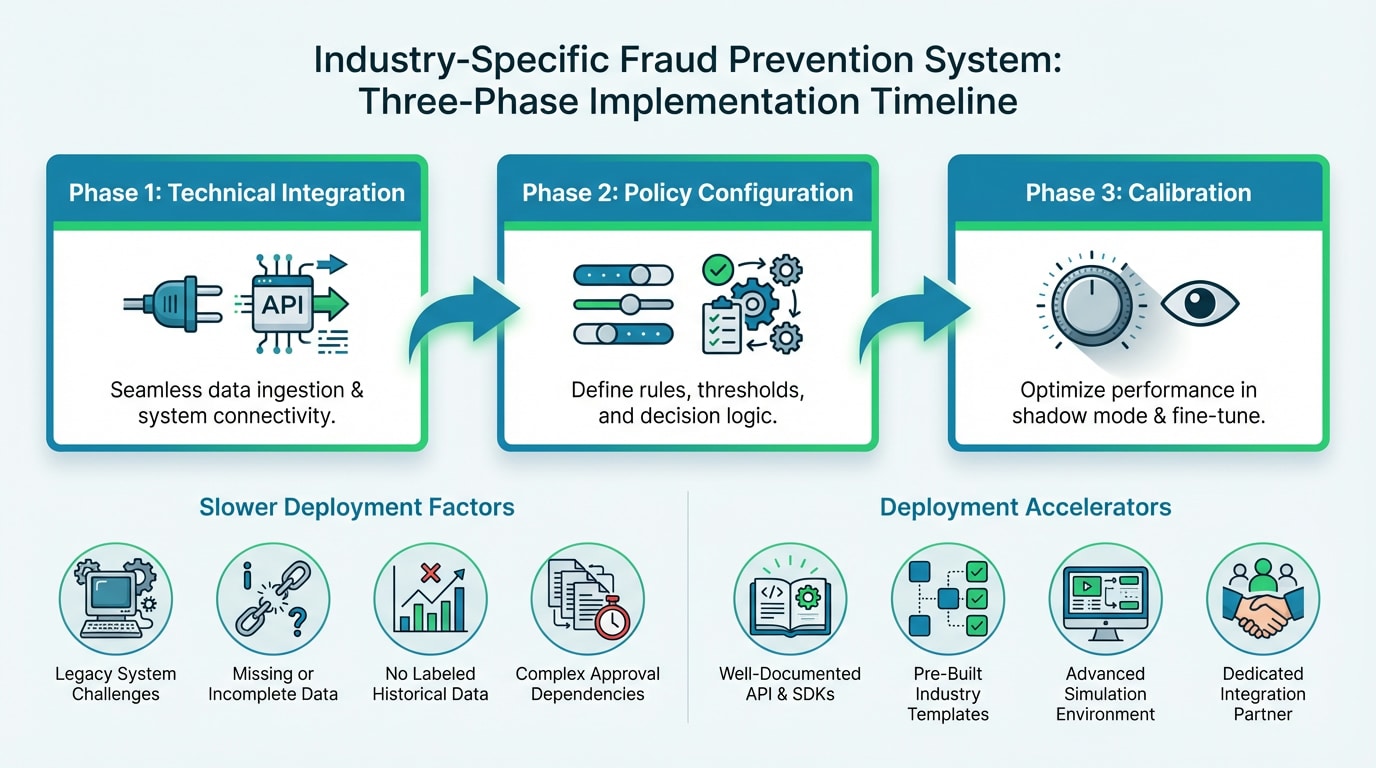

Implementation Timeline: What Affects How Fast You Go Live?

Deploying an industry-specific fraud prevention system typically involves three phases: technical integration (connecting data sources and transaction flows), policy configuration (setting up vertical-specific rules, thresholds, and workflows), and calibration (running in shadow mode to tune models before they make live decisions).

Factors that extend the timeline include legacy systems with limited API access, incomplete event capture (missing critical data points), absence of labeled historical data for model training, and dependency on multiple internal teams for approvals. Factors that accelerate it include well-documented APIs, pre-built industry use-case templates, simulation environments for policy testing, and a dedicated implementation partner who understands your vertical. Most organizations can reach initial production within weeks if the data infrastructure is ready. Full optimization typically unfolds over the first two to three months as feedback loops mature.

Did You Know

Shadow mode deployment, where the fraud system scores transactions but does not block them, typically reveals 15 to 25 percent more tuning opportunities than static rule-testing alone, because it exposes model behavior against real production traffic patterns.

How to Measure the ROI of a Specialized Fraud Prevention Strategy

ROI measurement for industry fraud prevention solutions should capture both direct savings and indirect business gains. On the savings side, track the reduction in fraud losses (gross and net of recovered funds), the decrease in chargeback and dispute fees, and the drop in manual-review volume and associated labor costs. On the gains side, measure improvements in transaction approval rates, customer conversion at checkout or onboarding, and time-to-decision for flagged cases.

A useful formula: Net ROI = (Fraud losses prevented + Operational cost reduction + Revenue recovered from improved approvals) – (Platform cost + Cost of additional authentication steps). Review these metrics monthly, segmented by product line, geography, and customer cohort, to identify where the system delivers the most value and where further tuning is needed.

What Risk and Operations Teams Need from Their Platform

For the analysts and managers who work with the system daily, technical sophistication means nothing if they cannot investigate quickly, understand decisions, and close the loop. The non-negotiable capabilities are: clear decision documentation (why was this flagged?), a full audit trail for every action, case-management workflows that route alerts to the right person, outcome tagging so resolved cases feed back into model improvement, and role-based permissions that enforce segregation of duties within the tool itself. These requirements intensify in regulated environments where external auditors expect demonstrable controls and where the national cyber authority’s reporting framework may require structured incident documentation.

Detelix Fraud Prevention Solutions

Proactive Monitoring

Continuous surveillance of ERP transactions and business processes to detect anomalies before they escalate into losses.

Real-Time Alerts

Instant notifications when suspicious activity is identified, enabling rapid response and minimizing exposure windows.

GateKeeper

Automated enforcement of segregation of duties and approval workflows to block unauthorized actions at the source.

ML-Based Pricing Fraud Detection

Machine-learning algorithms that identify pricing anomalies, unauthorized discounts, and financial leakages across your operations.

See Detelix in Action

Frequently Asked Questions

Can a single platform serve multiple industries without sacrificing detection accuracy?

Yes, provided it separates its core signal-processing engine from its policy layer. A multi-vertical platform applies shared capabilities like device intelligence, behavioral analytics, and graph analysis while maintaining distinct policy packages, thresholds, and use-case templates for each sector. This architecture delivers both breadth and depth.

How does industry specific fraud prevention affect customer experience?

When calibrated correctly, it improves the experience. Because the system understands what normal behavior looks like in your vertical, it subjects fewer legitimate users to friction. Step-up verification is applied selectively, only when risk signals genuinely warrant it, rather than blanket-applied to every transaction.

Is labeled historical data essential for deploying vertical fraud detection?

Labeled data accelerates model training and improves precision from day one. However, organizations with limited labeled history can start with rules-based detection and unsupervised anomaly models, then transition to supervised ML as labeled outcomes accumulate over the first months of operation.

How often should vertical fraud models be retrained or updated?

Continuous monitoring of model performance is critical. Most organizations retrain or recalibrate models on a monthly or quarterly cycle, depending on transaction volume and the pace of change in attack patterns. Rules should be reviewed whenever a new fraud scenario is identified or when false-positive rates trend upward.

What role does segregation of duties play in industry-specific fraud controls?

Segregation of duties (SoD) is a foundational control that prevents any single individual from executing and approving a sensitive action. In an ERP context, this means the person who creates a vendor record should not be the same person who approves payment to that vendor. Industry-specific platforms enforce SoD policies tailored to the workflows that matter most in each sector.

Ready to Align Your Fraud Controls with Your Industry’s Real Risks?

Are your current fraud controls truly calibrated for the threats your sector faces? Move from generic monitoring to vertical-specific protection that covers your critical business processes in real time.