Automate Your Internal Controls and Eliminate Blind Spots

Move from spreadsheets and sampling to continuous, population-level monitoring across every ERP transaction. Talk to a Detelix specialist today.

- What Exactly Is Internal Controls Automation Software?

- Why Are Organizations Transitioning to Financial Controls Automation?

- How Does Automated Internal Controls Technology Work End to End?

- Continuous Controls Monitoring — the Operational Gold Standard

- How Does an Internal Control Monitoring System Differ from a GRC Platform?

- Which Financial Processes Benefit Most from Automation?

- A Common Mistake: Treating Automation as a Replacement for Internal Audit

- How Does Automation Simplify Audit Readiness and Evidence Collection?

- Reducing False Positives Without Reducing Coverage

- What Integrations Are Essential for Success?

- What Does a Sound Implementation Process Look Like?

- How Do You Measure the ROI of Continuous Controls Monitoring?

- Key Metrics for Long-Term CCM Effectiveness

- Security and Privacy Capabilities You Must Verify

- Does Financial Controls Automation Suit Mid-Sized Companies — or Only Enterprise?

- How to Choose Internal Controls Automation Software That Fits Your Organization

- Frequently Asked Questions

In many organizations, internal controls exist on paper — documented in policy manuals, embedded in approval hierarchies, and reviewed once a year before the external audit. Yet between those periodic check-ups, thousands of transactions flow through ERP systems every day: payments are issued, vendor records are modified, journal entries are posted, and access permissions change. The gap between what leadership believes is controlled and what is actually happening in real time represents one of the most significant sources of financial risk. Internal controls automation software closes that gap by replacing reactive, sample-based testing with continuous, data-driven oversight that covers the entire transaction population.

Key Takeaways

- Internal controls automation replaces manual, sample-based testing with population-level verification across every ERP transaction — every invoice, payment, and master-data change is checked automatically.

- Continuous controls monitoring (CCM) compresses the detection window from weeks or months to hours or minutes, enabling same-day intervention on anomalies and exceptions.

- Automation does not replace internal audit judgment — it frees skilled professionals to focus on analysis, trend identification, and root-cause investigation instead of data gathering.

- Mid-sized organizations often benefit the most from automation due to leaner teams, higher reliance on individual knowledge, and thinner margins for error.

- A focused pilot covering five to ten high-value controls can go live within four to eight weeks and deliver measurable ROI in the first quarter.

What Exactly Is Internal Controls Automation Software?

Internal controls automation software is a platform that connects directly to an organization’s financial and operational systems — primarily the ERP — and executes predefined control tests automatically. Instead of a human pulling a report, filtering for anomalies, and storing evidence in a shared folder, the software performs these steps on a scheduled or real-time basis. It applies business rules, identifies exceptions, triggers alerts, logs every action in a tamper-evident audit trail, and routes open items through a remediation workflow until they are resolved and documented.

Tip

When evaluating automation platforms, prioritize solutions that connect directly to your ERP at the database or API level rather than relying on flat-file exports. Direct integration eliminates the manual upload step that reintroduces the very delays automation is meant to solve.

The core value proposition is straightforward: move from manual, sample-based checking to automated, population-level verification. Every invoice, every payment, every master-data change can be tested against the relevant control rule — not just a random 25-item sample selected two weeks before the auditors arrive.

Why Are Organizations Transitioning to Financial Controls Automation?

Traditional internal control testing is labor-intensive. Finance teams spend weeks extracting data, building spreadsheets, chasing approvals, and compiling evidence binders. The result is a snapshot — accurate only for the moment it was captured. By the time findings are reported, new exceptions may already have occurred. The COSO Monitoring guidance emphasizes that ongoing monitoring is a foundational component of effective internal control, precisely because point-in-time evaluations alone cannot keep pace with organizational change.

Did You Know

According to industry benchmarks, organizations that rely solely on manual internal control testing typically cover less than 5% of their total transaction volume during any given audit cycle. Automated systems test 100% of transactions against every applicable rule.

Automation eliminates “audit fatigue” — the repetitive extraction and review cycles that drain skilled staff. It also improves consistency: the same rule is applied to every transaction, every time, without subjective judgment or oversight fatigue. For finance leaders managing lean teams, that consistency translates directly into reduced risk and reclaimed working hours.

How Does Automated Internal Controls Technology Work End to End?

The lifecycle of an automated control follows a clear sequence: data extraction, rule application, exception identification, remediation workflow, evidence capture, and closure. Understanding each stage helps organizations plan a realistic implementation.

Data Connectors and Entity Mapping

The platform connects to source systems — ERP, banking, payroll, identity management — through APIs or database-level connectors. Raw transactional data is ingested, normalized, and mapped to the relevant business entities (vendors, customers, employees, accounts). Deep integration matters: the richer the data, the more sophisticated the control rules can be.

Rule Definition, Thresholds, and Exception Logic

Control owners define the logic: “Flag any payment above $50,000 that was approved by a single individual,” or “Identify vendor bank-account changes made within 48 hours of a payment run.” Thresholds, whitelists, and severity tiers are configured to focus attention on genuinely risky events rather than routine noise.

Tip

Start with broad thresholds during your initial deployment, then tighten them progressively based on exception review data. This approach lets you calibrate rules against your actual transaction patterns rather than theoretical assumptions.

Remediation Workflow and Audit Trail

When an exception is identified, the system assigns it to the appropriate control owner, tracks the response against an SLA, escalates if unresolved, and logs every action — who reviewed it, what decision was made, and what supporting evidence was attached. According to PCAOB AS 2201, auditors assess operating effectiveness by examining whether controls functioned as designed over the entire period — a time-stamped, immutable audit trail provides exactly that evidence.

Continuous Controls Monitoring — the Operational Gold Standard

Continuous controls monitoring (CCM) takes automation a step further. Rather than running tests on a daily or weekly batch, CCM evaluates controls persistently, often in near-real time, so that a deviation is flagged within minutes of occurring. This matters most in high-risk areas: segregation of duties violations, unauthorized changes to payment instructions, or unusual journal entries posted outside business hours.

Did You Know

Organizations with mature CCM programs report detecting anomalies within hours of occurrence, compared to an average detection window of 205 days for organizations relying on periodic manual reviews, according to fraud detection research.

CCM does not turn detective controls into preventative ones in the strict sense — the transaction has already been recorded. But it compresses the detection window from weeks or months to hours or minutes, giving management the opportunity to intervene before money leaves the organization or before a misstatement propagates into the financial statements. That shift — from “we found it in the annual audit” to “we caught it the same day” — is what makes CCM a preferred model for mature control environments.

How Does an Internal Control Monitoring System Differ from a GRC Platform?

Governance, Risk, and Compliance (GRC) platforms manage policy documentation, risk registers, control catalogs, and compliance workflows at a strategic level. They answer questions like “Which controls map to which risks?” and “Is our control framework complete?” An internal control monitoring system, by contrast, operates at the transactional data level. It answers a different question: “Is this specific control actually working right now, on today’s data?”

Tip

Map your GRC control catalog to the automated monitoring rules in your platform. This creates a direct link between your risk framework and the evidence that each control is functioning — exactly what auditors look for during their assessment of the control environment.

The two are complementary, not interchangeable. A GRC platform may document that “three-way match is required for all purchase orders above $10,000,” but only an automated monitoring system can verify — across every single PO — whether that rule was actually enforced. When the monitoring system generates evidence, the GRC platform catalogs and reports on it. Organizations that confuse the two often end up with well-documented controls that have never been tested against live data.

Which Financial Processes Benefit Most from Automation?

Not every control delivers the same return when automated. The highest-value targets share three characteristics: high transaction volume, high inherent risk, and heavy reliance on manual data gathering. The table below maps the most common process areas to their typical automated controls.

| Process Area | Example Automated Controls | Why It Matters |

|---|---|---|

| Procure-to-Pay (P2P) | Duplicate payment detection, vendor bank-account change alerts, three-way match exceptions | Direct cash leakage and fraud exposure |

| Order-to-Cash (O2C) | Unauthorized credit-limit overrides, unusual refund patterns, pricing deviations | Revenue integrity and customer fraud risk |

| Record-to-Report (R2R) | Journal entries above threshold, weekend/off-hours postings, entries by unauthorized users | Financial statement accuracy and fraud indicators |

| Access and SoD | Conflicting role assignments, dormant privileged accounts, emergency-access usage | Preventative control over authorization risk |

Population testing — checking every transaction instead of a sample — is where automation creates an asymmetric advantage. A manual auditor testing 30 journal entries out of 50,000 may miss the one fraudulent posting. An automated system tests all 50,000 against the same criteria in seconds. Platforms like Detelix leverage hundreds of algorithms to ensure every action in the ERP system is cross-checked against defined rules, covering the full population without adding headcount.

Did You Know

Duplicate payments alone cost organizations an estimated 0.1% to 0.5% of total disbursements annually. For a company processing $500 million in payments per year, that represents $500,000 to $2.5 million in preventable losses — most of which go undetected without automated population-level testing.

A Common Mistake: Treating Automation as a Replacement for Internal Audit

Automation handles execution — the running of tests, the collection of evidence, the routing of exceptions. It does not replace the professional judgment required to design controls, assess risk appetite, or evaluate whether a flagged exception is truly a problem or an acceptable business decision. Internal audit teams that adopt automation effectively shift their focus from data gathering to analysis, trend identification, and root-cause investigation.

The ISA 240 (Revised) standard underscores that auditors must exercise skepticism and evaluate fraud risk indicators — tasks that require human expertise. Automation feeds those experts better data, faster. The result is not fewer auditors, but more effective ones.

Your finance team deserves better than spreadsheets and sampling. Discover how Detelix automates internal controls across your entire ERP transaction population — with real-time alerts and audit-ready evidence.

How Does Automation Simplify Audit Readiness and Evidence Collection?

Ask any controller what happens in the weeks before an external audit, and the answer usually involves late nights, frantic email chains, and last-minute evidence hunts. Automated internal controls change that dynamic entirely. Because every test execution, every exception, and every remediation step is logged with a timestamp and user identity, the evidence package exists before the auditor even requests it.

What auditors need to see is clear: who performed the control, when, what was tested, what was the result, how were exceptions resolved, and what documentation supports the resolution. When that information is generated automatically and stored in an immutable log, audit preparation shrinks from weeks to hours. There is no “document reconstruction,” no missing sign-offs, and no inconsistency between what the policy says and what actually happened.

Tip

Schedule a “mock audit extraction” within the first month after go-live. Pull the evidence package your automated system generates and walk through it as if you were the external auditor. This exercise reveals gaps in documentation or rule configuration early — not during the actual audit.

Reducing False Positives Without Reducing Coverage

One of the fastest ways to undermine an automated control program is to flood control owners with irrelevant alerts. When 70% of flagged items turn out to be benign, people stop investigating — and the genuine exceptions get lost in the noise. Alert accuracy is not a secondary feature; it determines whether the system is trusted and used.

Design Rules Around Risk, Not Around Every Deviation

Effective rule design starts with the risk scenario, not the data field. Instead of “flag every manual journal entry,” a risk-informed rule might be “flag manual journal entries above $25,000 posted by users outside the finance department after 6 PM.” The narrower the rule, the more meaningful the alert.

Severity Tiers and Periodic Tuning

Not every exception carries the same business impact. Tiering alerts by severity — critical, high, medium, informational — lets control owners prioritize effectively. Monthly or quarterly tuning sessions review false-positive rates, adjust thresholds, and retire rules that no longer reflect the current risk landscape. Detelix, for example, achieves a point where 90% of alerts are accurate, enabling organizations to change their control processes with confidence — because teams trust what the system surfaces.

Did You Know

Research on alert fatigue in monitoring systems shows that when false-positive rates exceed 60%, analyst response rates drop below 30%. Keeping alert accuracy above 85% is the threshold where control owners consistently investigate and resolve flagged items.

What Integrations Are Essential for Success?

The value of any internal controls automation platform is directly proportional to the quality and breadth of its data connections. The following table outlines the integration categories that matter most.

| Integration Category | Purpose | Impact on Control Quality |

|---|---|---|

| ERP / Financial System | Source of transactional data (AP, AR, GL, inventory) | Enables population-level testing on core financial processes |

| Banking / Payment Platform | Validates payment execution against approved instructions | Detects unauthorized or manipulated outbound payments |

| Identity and Access Management (IAM/SSO) | Provides user-role data for SoD and access reviews | Automates SoD conflict detection and privilege monitoring |

| Ticketing / Workflow System | Tracks remediation and change-management actions | Closes the loop between exception and resolution with evidence |

| Document Management | Stores supporting documentation linked to control evidence | Ensures non-repudiation and retrieval during audits |

The deeper and more real-time these integrations are, the closer the organization gets to true continuous monitoring. Shallow integrations — flat-file exports uploaded manually — reintroduce the very delays and errors automation is supposed to eliminate.

Tip

During vendor evaluation, request a live demonstration of the platform connecting to a system similar to your ERP version. Pay attention to how long the initial data sync takes, how field mapping is handled, and whether changes in the source schema are detected automatically.

What Does a Sound Implementation Process Look Like?

Successful implementations start small and expand deliberately. The most common failure pattern is attempting to automate 200 controls simultaneously, which overwhelms both the technology team and the business stakeholders who own those controls.

Start with Five to Ten “Quick-Value” Controls

Select controls that are high-volume, well-understood, and already have clear data sources. Duplicate payment detection, vendor master-data changes, and basic SoD checks are typical starting points. Proving value on a narrow scope builds organizational confidence and secures executive sponsorship for the next phase.

Define Ownership and Success Metrics Early

Every automated control needs a named owner — someone accountable for reviewing exceptions, tuning rules, and signing off on remediation. A clear RACI (Responsible, Accountable, Consulted, Informed) model prevents ambiguity. Success metrics should be defined before go-live: average time to close an exception, percentage of controls tested at population level, and reduction in manual audit hours.

Did You Know

Organizations that define clear control ownership and RACI models before automation deployment report 40% faster exception resolution times compared to those that assign ownership after go-live, according to internal audit benchmarking studies.

How Do You Measure the ROI of Continuous Controls Monitoring?

ROI manifests in both tangible savings and risk avoidance. Tangible savings include reduced manual testing hours, faster audit preparation, and recovery of overpayments or duplicate disbursements identified before they become losses. Risk avoidance — harder to quantify but often more valuable — includes fraud prevented, regulatory penalties avoided, and reputational damage sidestepped.

Organizations that begin with high-volume P2P controls often see measurable returns within the first quarter: a single detected duplicate payment or fraudulent vendor-bank change can exceed the annual cost of the software. Over time, the “hidden ROI” compounds: stronger compliance posture, improved insurer assessments, and a culture where control is proactive rather than reactive.

Tip

Track and document every exception that results in a recovered payment, prevented loss, or avoided penalty. Building this “value log” from day one gives you concrete data to justify expanding the program to additional process areas and business units.

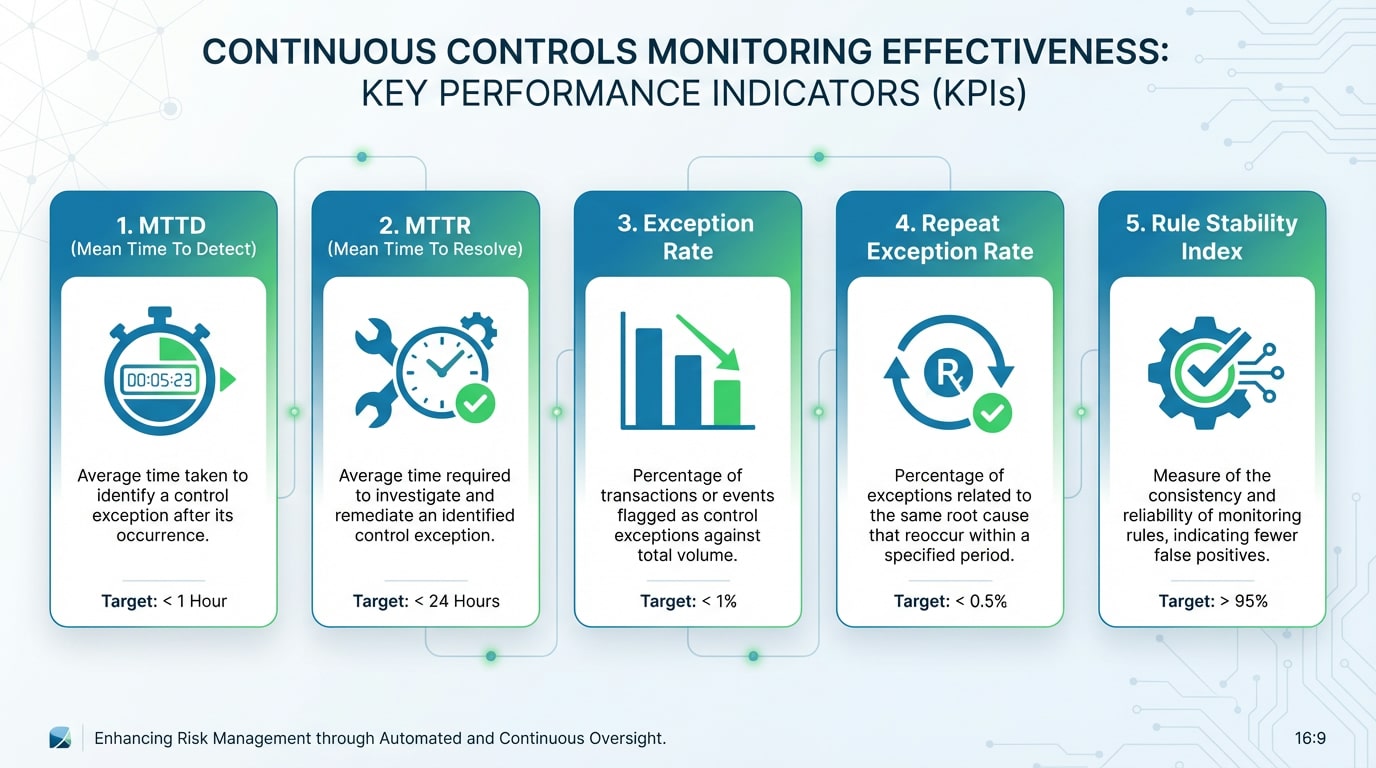

Key Metrics for Long-Term CCM Effectiveness

Measuring success is not a one-time exercise. The following KPIs and KRIs (Key Risk Indicators) provide a framework for ongoing evaluation.

Exception rate per 1,000 transactions — tracks whether the control environment is improving or deteriorating over time. Mean time to detection (MTTD) — measures how quickly an anomaly is identified after it occurs. Mean time to remediation (MTTR) — measures how quickly a confirmed exception is resolved and documented. Repeat exception rate — identifies systemic process failures that require root-cause correction rather than individual remediation. Rule stability index — tracks how often rules need modification due to system changes, indicating integration resilience.

Did You Know

The repeat exception rate is often the single most revealing metric in a CCM program. A high repeat rate on the same control rule signals a systemic process failure — not just an individual error — and should trigger a root-cause analysis rather than repeated individual remediation.

Security and Privacy Capabilities You Must Verify

An internal controls monitoring system, by nature, has read access to some of the most sensitive data in the organization — financial transactions, employee records, access logs. The security posture of the platform itself must be at least as strong as the controls it monitors. Role-based access ensures that a control owner reviewing AP exceptions cannot access payroll data. Encryption at rest and in transit protects data from interception. Comprehensive logging of who accessed what evidence, and when, closes the “who watches the watchers” question. The NIST SP 800-53A Rev. 5 framework provides detailed assessment procedures for evaluating such security controls — a useful benchmark when conducting vendor due diligence.

Tip

Request the vendor’s SOC 2 Type II report and verify that it covers the specific trust services criteria relevant to your use case — particularly security, availability, and confidentiality. A SOC 2 report that only covers security without availability may leave gaps in your due diligence.

Does Financial Controls Automation Suit Mid-Sized Companies — or Only Enterprise?

A common misconception is that automation is only justified for large, publicly traded companies subject to SOX compliance. In reality, mid-sized organizations often have the most to gain. Their finance teams are smaller, their processes more reliant on individual knowledge, and their margin for error thinner. A single accounts-payable clerk who both creates vendors and approves payments represents a segregation-of-duties risk that an enterprise might catch through periodic audit but that a mid-sized company may never detect without automated monitoring.

Modern platforms offer pre-built control libraries and templated workflows that reduce implementation complexity. A mid-sized company can go live with a focused set of P2P and access controls in weeks, not months — and immediately gain visibility that was previously impossible without dedicated audit staff.

How to Choose Internal Controls Automation Software That Fits Your Organization

The market offers a range of solutions, and the right choice depends less on feature count than on fit. Consider these evaluation criteria before committing to a demo or pilot.

Essential Questions for the Demo and Pilot

Ask the vendor to demonstrate a control relevant to your actual data — not a pre-built demo environment. Can the system connect to your specific ERP version? How long does it take to define a new rule? Can a non-technical control owner manage exceptions without IT involvement? What does the audit-trail export look like? These practical questions reveal more than any feature matrix.

Common Selection Mistakes

Over-automation is a real risk: attempting to automate controls for which reliable data does not yet exist leads to false results and eroded trust. Another frequent mistake is choosing a platform that requires heavy customization for every rule change, creating long-term dependency on consultants. Look for a solution that balances configurability with simplicity — powerful enough to handle complex multi-entity environments, intuitive enough for a finance manager to operate day to day.

Tip

During your pilot, have a non-technical finance team member create a new control rule and manage an exception through resolution without vendor assistance. If they cannot do it independently, the platform may create long-term dependency that offsets the efficiency gains.

Detelix Continuous Controls Monitoring Solutions

Proactive Monitoring

Continuous oversight of ERP transactions with automated rule execution and population-level testing across all financial processes.

Real-Time Alerts

Instant notification of control exceptions, SoD violations, and anomalous transactions with severity-tiered routing to control owners.

GateKeeper

Automated fraud prevention engine that validates vendor data, payment instructions, and master-data changes before they execute.

Industry Experience

Decades of domain expertise in financial controls, audit readiness, and regulatory compliance across diverse industries and ERP environments.

See Detelix in Action

Frequently Asked Questions

Can automated controls test 100% of transactions instead of a sample?

Yes. This is one of the primary advantages. Unlike manual testing, which is constrained by time and cost to small samples, automated controls apply the same rule to every transaction in the population. The result is comprehensive coverage that dramatically reduces the chance of missing a material exception.

How long does a typical implementation take?

A focused pilot — covering five to ten controls with existing data connectors — can be live within four to eight weeks. Broader rollouts across multiple process areas and geographies typically take three to six months, depending on data complexity and organizational readiness.

What happens when the ERP system is upgraded or changed?

System changes can affect data structures, field mappings, and integration points. A well-designed automation platform includes change-detection mechanisms that alert administrators when source data schemas shift. Regular regression testing after major ERP updates is a best practice to ensure control rules continue to operate as intended.

Is continuous controls monitoring relevant for organizations not subject to SOX?

Absolutely. CCM addresses operational risk, fraud prevention, and process integrity — concerns that apply to every organization regardless of regulatory mandate. Private companies, non-profits, and government entities all benefit from knowing that their controls are functioning continuously, not just during audit season.

How does automation handle segregation of duties (SoD) conflicts?

The system maps user roles and permissions against a predefined SoD conflict matrix. When a user is assigned conflicting access — for example, the ability to both create a vendor and approve a payment — the system flags the conflict immediately, routes it for review, and logs the resolution. This replaces the quarterly or annual SoD review cycle with persistent, real-time monitoring.

Ready to Move from Sampling to Full-Population Control?

Every week of delay is another week of unmonitored transactions and preventable losses. Let the Detelix team show you what continuous, automated internal controls look like for your specific ERP environment.