Take Full Control of Your Distribution and Logistics Payments

Stop overpaying on freight invoices. Detelix provides real-time financial controls that catch errors and fraud before money leaves your organization.

- What Are Distribution and Logistics Finance Controls?

- Why Manual Freight Invoice Audits Fail

- Real Scenario: How a Small Surcharge Became a Massive Loss

- The End-to-End Audit-to-Pay Control Process

- Freight Invoice Fraud Detection

- Distribution Cost Anomaly Monitoring

- Smart Thresholds Without Alert Fatigue

- Pre-Pay vs. Post-Pay Audit Comparison

- Transportation Payment Governance

- Common Segregation of Duties Mistakes

- When ERP, TMS, and WMS Data Falls Out of Sync

- Metrics Every CFO Should Track

- How Automation Impacts ROI

- Where Detelix Fits In

- What to Do When You Suspect Freight Payment Fraud

- Frequently Asked Questions

In distribution and logistics organizations, payment processes for carriers and freight providers generate one of the largest and most complex expenditure pipelines. Freight invoices contain dozens of fields — base rates, fuel surcharges, detention fees, address correction charges, and more — and each one represents a potential entry point for error, overcharging, or outright fraud. When financial controls fail to match the pace and complexity of these transactions, the organization pays more than it should, sometimes without ever realizing it. This article breaks down the principles of financial control in distribution and logistics, presents practical scenarios, and explains how to transform routine monitoring into genuine operational command.

Key Takeaways

- Freight invoices carry unique complexity that standard procurement controls cannot adequately address — purpose-built logistics controls are essential.

- Manual invoice audits catch only a small sample of errors; overcharges of 1% to 3% of total freight spend accumulate silently into significant annual losses.

- Automated pre-payment audits block erroneous charges before money leaves your organization, while post-payment audits identify systemic patterns for contract renegotiation.

- Proper segregation of duties, real-time anomaly monitoring, and a complete audit trail form the backbone of transportation payment governance.

- Cross-system synchronization between ERP, TMS, and WMS eliminates the blind spots where duplicate charges and ghost shipments hide.

- Detelix operates as an independent control layer above your ERP, continuously scanning every sensitive action and alerting in real time when policy violations occur.

What Are Distribution and Logistics Finance Controls — and Why Are They Different from Standard Procurement Controls?

Distribution and logistics finance controls are a system of policies, digital rules, and automated checks designed to ensure that every payment for transportation or distribution services is accurate, authorized, and documented before money is released. Unlike classical procurement controls that rely on a fixed purchase order and an agreed price per unit, logistics pricing fluctuates based on weight, distance, delivery zone, service type, and ad-hoc surcharges. This variability demands a specialized control layer that understands freight rate calculation logic and can validate every line item on an invoice against actual shipment data.

Tip

Map every accessorial charge type your carriers use — liftgate, residential delivery, inside pickup, detention — and build validation rules that cross-reference each charge against the corresponding shipment record. If the service was not requested or confirmed, the charge should be flagged automatically before payment.

The gap between standard procurement controls and logistics-specific controls becomes most visible when organizations try to apply generic three-way matching (PO, receipt, invoice) to freight. A freight invoice rarely matches a single PO line-for-line. Rates depend on actual weight versus dimensional weight, the specific delivery zone, time-of-day surcharges, and dozens of other variables that simply do not exist in a typical material purchase. Without controls that account for these logistics-specific dynamics, overcharges slip through undetected.

Why Manual Freight Invoice Audits Almost Always Fail

The problem is not the team’s competence or intention — it is the sheer volume and complexity involved. A mid-sized distribution organization processes hundreds to thousands of freight invoices per month, each containing multiple rate lines, surcharges, and unique identifiers. A thorough manual audit requires comparing every line against the active rate contract, shipment data (weight, distance, delivery address), and proof of delivery (POD) confirmation. In practice, teams audit a small sample and miss anomalies that accumulate into significant sums over the course of a year.

Did You Know

Industry data consistently shows that freight invoice error rates range between 1% and 3% of total transportation spend. For an organization spending $5 million annually on freight, that translates to $50,000 to $150,000 in overcharges per year — most of which go undetected without automated controls.

Adding to the challenge, when data is scattered across spreadsheets, TMS platforms, and ERP systems, there is no single source of truth. This fragmentation allows errors and duplicate charges to slip through the cracks, remaining unnoticed until the end of the quarter — if they are caught at all. The manual approach also creates a bottleneck: the more invoices the team processes, the less time they can spend on each one, and the higher the probability that a subtle overcharge goes unquestioned.

Real Scenario: How a 12-Shekel Surcharge Became a Half-Million Annual Loss

A distribution organization discovered during an annual audit that one of its carriers had been adding a “liftgate” surcharge to every shipment on a specific route — even when the liftgate service was never actually provided. The per-shipment amount of 12 ILS did not raise suspicion during manual spot checks. But across 3,500 shipments per month over 12 months, the loss reached approximately 504,000 ILS. Without an automated control that compares the service type ordered against the service type billed, no one in the organization identified the discrepancy.

Tip

Never dismiss a small per-unit surcharge as immaterial. Calculate its annualized impact by multiplying the charge amount by the number of affected shipments per month, then by 12. Surcharges under $5 per shipment can easily exceed $100,000 per year at scale.

This scenario is not unusual. Accessorial charges are the most common source of freight overcharges precisely because they are individually small, highly variable, and difficult to validate without access to both the rate contract and the actual shipment execution data. Automated controls that cross-reference service orders against billing data eliminate this blind spot entirely.

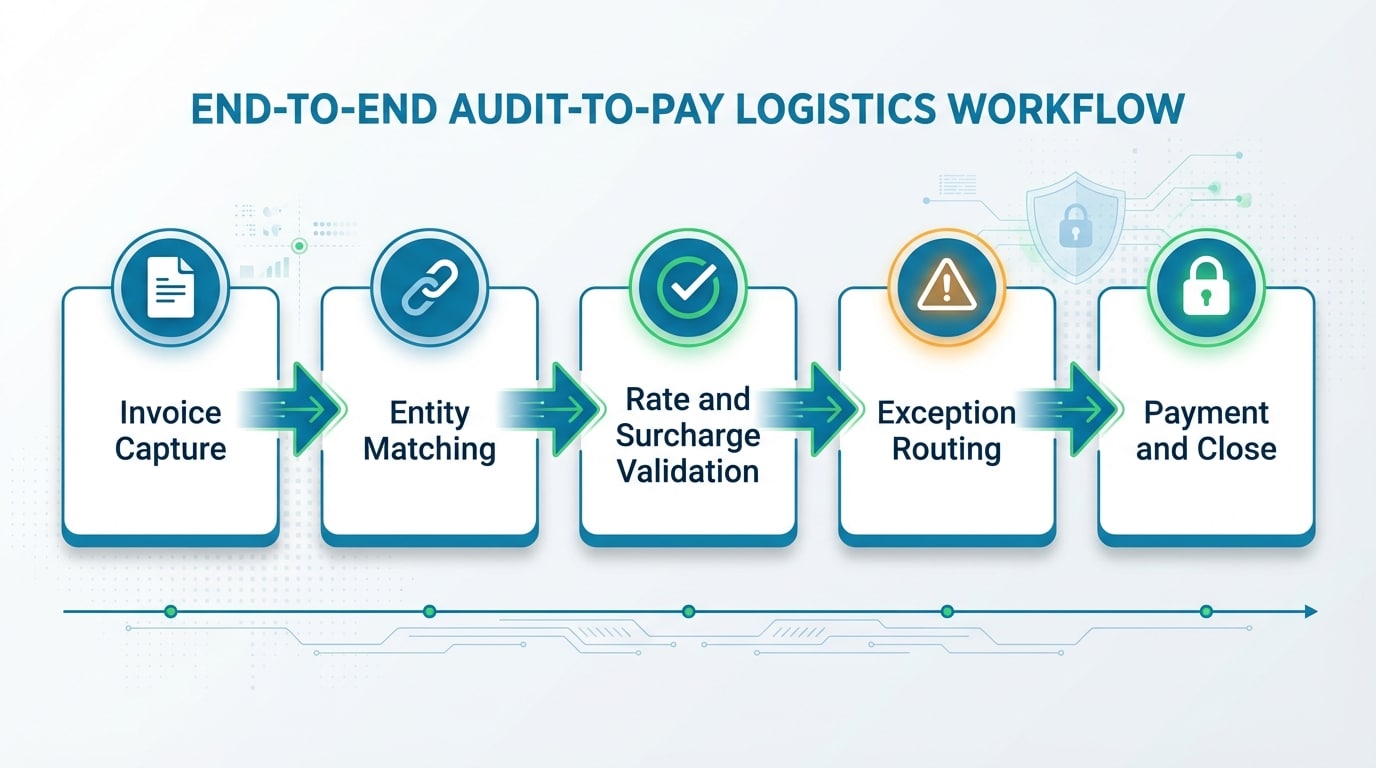

What Does an End-to-End Audit-to-Pay Control Process Look Like in Logistics?

A properly designed process defines clear control checkpoints before any payment is released. The workflow begins with invoice ingestion (EDI, PDF, or supplier portal), continues with automatic entity matching (supplier/carrier identification, shipment number, and POD confirmation), proceeds to rate and surcharge validation against the active contract, classifies anomalies for human review through a defined workflow, and concludes with payment execution, accounting closure, and full documentation.

With this structure in place, the vast majority of clean invoices flow through rapidly with no human intervention, while the finance team focuses exclusively on genuine exceptions that require judgment. The result is faster payment cycles for compliant carriers — strengthening supplier relationships — and tighter control over the exceptions that actually matter.

Hard Stops vs. Soft Alerts: When to Block and When to Flag

A hard stop blocks payment completely. This applies when a duplicate invoice is detected, when the supplier is not verified in the master data, or when a billed rate does not exist in any active contract. A soft alert warns the team but allows processing to continue subject to approval — for instance, when a charge exceeds the route average by 8% or when an unusual but potentially legitimate surcharge appears. The right combination of both mechanisms prevents financial leakage without creating unnecessary delays in the payment pipeline.

Did You Know

Organizations that implement automated pre-payment freight audits typically achieve “straight-through” processing rates above 85%, meaning fewer than 15% of invoices require any manual intervention. This dramatically reduces processing cost per invoice while improving accuracy.

Freight Invoice Fraud Detection: How to Identify Fraud in Carrier Invoices

Detecting fraud in freight invoices relies on three distinct layers. The first is identity verification — confirming who the supplier is and whether the bank account details match the approved master record. The second is consistency verification — determining whether what the invoice claims matches what was actually executed. The third is pattern recognition — identifying statistical anomalies that point to unnatural behavior.

“Ghost shipments” — invoices for transportation that never occurred — are uncovered when no matching POD document exists. Duplicate charges are detected when invoice numbers are suspiciously similar or when the same shipment is billed twice on nearby dates. A sudden change in a supplier’s bank account details is a critical warning sign. Official government advisories have highlighted how phishing attempts specifically target bank account change requests — the same principle applies when a carrier requests a payment detail update. Every such change must undergo independent verification with the supplier through a separate communication channel.

Tip

Establish a mandatory dual-authorization process for any supplier bank account change. Require verification through a separate channel (phone call to a known contact, not the email requesting the change). This single control can prevent the most financially devastating form of payment fraud — business email compromise (BEC).

In the Israeli context, the Tax Authority’s invoice verification service enables organizations to validate invoices using allocation numbers — a fundamental step that prevents fictitious invoices from being processed before payment is made. Integrating this type of external validation into your automated control workflow adds a powerful layer of defense against fraudulent billing.

Distribution Cost Anomaly Monitoring: From Annual Audits to Continuous Control

Anomaly monitoring represents the transition from “annual audit” to “continuous control.” The mechanism builds a statistical baseline for every relevant dimension — cost per kilometer on a given route, average surcharge rate per carrier, cost per order from a specific warehouse — and triggers alerts when a value deviates significantly from the norm. This way, a cost spike in distribution from a northern warehouse does not get absorbed into the overall average but is identified immediately for investigation.

| Monitoring Dimension | Example Anomaly | Business Value |

|---|---|---|

| Route / Zone | 15% increase in cost per km on a major corridor | Identifies incorrect pricing or undocumented route changes |

| Carrier / Supplier | Detention charges from one carrier are 3x the average | Data-driven negotiation or suspicion of unjustified billing |

| Service Type | Express shipment costs rose 22% in one quarter with no volume change | Triggers contract rate verification against actual charges |

| Warehouse / DC | Cost per order from southern DC exceeds 2 standard deviations | Root cause investigation — operational issue or billing error? |

| Accessorial Charge Type | Liftgate charges increased 40% without corresponding order increase | Blocks unjustified charges before payment |

Did You Know

Statistical anomaly detection using standard deviation analysis catches cost deviations that percentage-based thresholds miss. A 5% increase on a high-volume route may represent $50,000, while a 20% increase on a low-volume route may be only $500 — effective monitoring must account for both magnitude and monetary impact.

How to Define Smart Thresholds That Do Not Overwhelm the Team with False Alerts

A fixed threshold (such as “flag every deviation above 5%”) generates excessive noise in a distribution environment with naturally high variability. It is far more effective to define dynamic thresholds that combine three criteria: minimum financial impact (for example, above $150 per event), statistical deviation from a seasonal baseline (for example, more than 2 standard deviations), and persistence — the anomaly recurs across a defined number of shipments or consecutive days. This approach produces fewer alerts, but every alert that surfaces is worth investigating.

Tip

Review and recalibrate your anomaly thresholds quarterly. Seasonal volume shifts, new carrier contracts, and route changes can all shift the statistical baseline. Thresholds that made sense six months ago may generate either too many false positives or too few real alerts today.

Pre-Pay vs. Post-Pay Audit: A Comparison

| Criterion | Pre-Pay Audit | Post-Pay Audit |

|---|---|---|

| Primary Objective | Prevent incorrect or excessive payment | Identify systemic patterns and improve contracts |

| Timing | Before payment release | After payment (days to months later) |

| Cash Flow Impact | May delay payment on flagged exceptions | No impact on payment timing |

| Loss Prevention Capability | High — blocks funds before they leave | Lower — requires recovery process |

| Analytical Value | Moderate — focused on individual transactions | High — enables trend analysis and term improvements |

In most cases, the optimal approach combines both: automated pre-payment controls that catch clear discrepancies in real time, paired with post-payment audits that uncover opportunities for rate improvements and reduce future disputes. The pre-pay layer protects your cash; the post-pay layer strengthens your negotiating position.

Are your freight payment controls catching overcharges before they become losses? Let Detelix analyze your distribution payment pipeline and show you exactly where the gaps are.

Transportation Payment Governance: Building a Framework That Holds Up Under Audit

Quality governance defines who approves what, under which conditions, how every decision is documented, and how exceptions are handled — without slowing down the supply chain. This framework includes a clear authorization model, segregation of duties (SoD), a defined policy for supplier payment detail changes, and pre-configured escalation rules. The approach mirrors principles applied by government accounting oversight bodies, which implement supervision over commitments, supplier payments, and internal audit through dedicated financial controllers.

Key Governance Components to Define

First, a RACI matrix that specifies responsibility for each process stage: who ingests the invoice, who approves exceptions, who executes payment. Second, a payment detail change policy — every bank account update for a supplier requires dual authorization and verification through an independent channel. Third, complete documentation (audit trail) of every decision: approval, rejection, or dispute, including timestamp and approver identity. Fourth, a structured dispute process with carriers that includes a defined SLA for resolution.

Did You Know

Business email compromise (BEC) attacks that target supplier bank account changes cost organizations an average of $125,000 per incident globally. A simple dual-authorization policy with out-of-band verification can prevent the vast majority of these attacks from succeeding.

Common Segregation of Duties Mistakes in Freight Payments

The most frequent mistake is a situation where the same employee is responsible for managing supplier master data (including bank details), approving invoices, and releasing payments. This concentration creates a single point of failure that enables internal fraud without detection. The minimum required separation involves three distinct roles: one role for managing supplier master data, a second role for approving exceptions and invoices, and a third role for executing the actual payment. Every sensitive change — such as adding a new supplier or updating bank account details — must be documented and approved by a person who is not involved in the payment execution process.

Tip

Audit your SoD matrix at least twice a year. Role changes, employee departures, and system access modifications can silently erode your separation of duties. An automated SoD monitoring tool flags conflicts the moment they appear, rather than waiting for the next internal audit cycle.

When ERP, TMS, and WMS Data Falls Out of Sync

Data desynchronization is the largest blind spot in distribution controls. When the ERP records an order, the TMS manages the shipment, and the WMS documents warehouse dispatch — but all three systems do not communicate in the same language — automatic matching becomes impossible. The result: an invoice that appears valid in one system does not match the data in the other two, and the team is forced to verify manually or, worse, pay without verification.

The solution is consistent entity mapping (supplier, route, shipment, invoice) with uniform identifier keys, combined with event synchronization: order creation, shipment dispatch, delivery confirmation (POD), and invoice receipt. When hundreds of algorithms verify every action within the ERP system, mismatches are identified in real time rather than after the fact.

Did You Know

Studies estimate that poor data quality costs organizations between 15% and 25% of their revenue. In logistics specifically, data inconsistencies between systems are the leading cause of invoice disputes — disputes that consume staff time, delay payments, and damage carrier relationships.

Metrics Every CFO Should Track in Distribution Controls

Measurement is the foundation of control. Without clear metrics, it is impossible to know whether controls are working or merely existing on paper. Five key metrics deserve ongoing attention: the percentage of invoices flagged with anomalies (out of total invoices received), the monetary amount blocked before payment, the average time to resolve an exception (from alert to closure), the dispute rate with carriers, and the percentage of invoices that achieved “straight-through” processing with no manual intervention. Together, these metrics paint a clear picture of control effectiveness and highlight areas that require improvement.

Tip

Track the “cost per invoice processed” metric alongside accuracy metrics. If your cost per invoice is high but your error detection rate is low, your controls are consuming resources without delivering proportional value. Automation should reduce both the cost per invoice and the error rate simultaneously.

How Automation of Distribution Controls Impacts ROI

Industry data indicates that overcharges on freight invoices typically range between 1% and 3% of total freight expenditure. For an organization with annual transportation spending of $5 million, this represents potential savings of $50,000 to $150,000 per year — solely from preventing overcharges. Added to this is the labor savings: when the majority of invoices flow through automatically, the finance team is freed to focus only on genuine exceptions. Furthermore, a well-organized audit trail significantly reduces the cost and time required to prepare for both internal and external audits.

Did You Know

Organizations that deploy automated freight audit solutions report an average ROI of 5:1 to 10:1 within the first year. The return comes not only from recovered overcharges but also from reduced processing costs, faster dispute resolution, and improved contract compliance visibility.

Where Detelix Fits In — and What It Changes in Practice

Detelix operates as an independent control layer above your ERP system. Instead of relying on periodic reports or manual sampling, the system continuously scans every sensitive action — supplier detail changes, invoice approvals, payment releases — and alerts in real time when anything deviates from defined policy. For distribution organizations, this means there is no need to “search” for problems: the problems come to you before they become losses.

Three practical advantages stand out. First, automatic cross-checking between shipment data, rate contracts, and invoices — at a level of granularity that a human simply cannot sustain at high volume. Second, monitoring of sensitive changes such as supplier bank account updates, which triggers an immediate alert and requires approval according to the SoD policy. Third, automatic documentation of every event and every decision, generating an audit trail that is ready for any review — without additional manual work.

What to Do When You Suspect Freight Payment Fraud

The first step is to freeze the suspected payment immediately. Next, document the event in full: invoice number, supplier, dates, bank account details, and all relevant communications. Notify the responsible party within your organization — CFO, internal auditor, or legal counsel — and initiate an internal investigation. If a cyber incident or impersonation is suspected, report it through the appropriate national cyber reporting channels. A control system that detects the event in real time shrinks the window of damage and enables response before money actually leaves the organization.

Tip

Maintain a documented incident response playbook specifically for payment fraud scenarios. When an alert triggers, the team should know exactly who to contact, what to freeze, and how to preserve evidence — without losing time figuring out the process under pressure.

Detelix Financial Control Solutions

Proactive Monitoring

Continuous scanning of every ERP transaction to detect anomalies, policy violations, and unauthorized changes before they result in financial loss.

Real-Time Alerts

Instant notifications when sensitive actions occur — supplier data changes, payment threshold breaches, and segregation of duties conflicts.

Gatekeeper

Automated approval workflows that enforce authorization policies, block unauthorized transactions, and maintain a complete audit trail.

Experience & Expertise

Over a decade of domain expertise in ERP financial controls, serving distribution, logistics, healthcare, and enterprise organizations.

See Detelix in Action

Frequently Asked Questions

How long does it take to implement automated controls on freight payments?

The timeline depends on ERP complexity and the number of carriers, but full operational deployment typically takes a few weeks. Implementation includes process mapping, rule and threshold configuration, and integration with TMS/WMS data sources.

Do automated controls slow down the payment process for carriers?

The opposite is true. Clean invoices flow faster because they are approved automatically. Only genuine exceptions stop for manual review, which actually improves overall payment cycle time and strengthens relationships with carriers.

What types of fraud are most common in freight invoices?

The three most prevalent types are: duplicate charges on the same shipment, accessorial charges for services that were never provided, and bank account detail changes resulting from impersonation or phishing (BEC). Automated controls detect all three through duplicate detection rules, POD data validation, and master data change monitoring.

Are distribution controls relevant for small and mid-sized organizations?

Absolutely. Smaller finance teams actually face higher risk because there are not enough people to maintain proper segregation of duties and perform thorough manual checks. Automation enables a small team to control high volumes without compromising accuracy.

What is the difference between anomaly monitoring and internal audit?

Anomaly monitoring is a continuous, real-time process that alerts on exceptional events as they occur. Internal audit is a periodic process that examines patterns, policy compliance, and control effectiveness over time. Both are necessary — monitoring prevents immediate losses, while audits improve the system for the long term.

Ready to Close the Gaps in Your Distribution Payment Controls?

Whether you are losing money to freight overcharges, struggling with manual audit bottlenecks, or concerned about invoice fraud, Detelix delivers the real-time visibility and automated enforcement your finance team needs.