Stop Financial Leaks Before They Erode Your Manufacturing Margins

Detelix continuous monitoring software detects duplicate payments, price drift, and cost anomalies across your entire ERP in real time. Get a free assessment today.

- What Is Manufacturing Finance Leak Prevention Software?

- Why Financial Leaks Persist Despite Advanced ERP Systems

- Plant Procurement Fraud Prevention

- Preventing Payment on Duplicate or Near-Duplicate Invoices

- Detecting Price Drift Before It Becomes a Margin Problem

- Catching Quantity Anomalies and Payments for Goods Never Received

- Production Cost Anomaly Detection

- The Role of Inventory Valuation Controls

- Rules vs. Anomaly Detection

- Reducing Alert Fatigue and False Positives

- Connecting Procurement, Production, Inventory, and Finance

- What Data Is Required for Effective Controls

- Implementation Timeline and Process

- Measuring the ROI of Leak Prevention

- What Happens When a Factory Ignores These Controls

- How to Evaluate Software for Manufacturing Finance Leak Prevention

- Frequently Asked Questions

In many manufacturing organizations, financial controls appear robust on paper. There are ERP workflows, approval hierarchies, reconciliation schedules, and periodic audits. Yet every quarter, finance teams uncover overpayments to suppliers, unexplained cost variances on the production floor, and inventory valuations that fail to match physical counts. These are not dramatic fraud events. They are small, persistent financial leaks that individually slip past routine reviews but collectively erode margins and distort financial statements. The challenge is not a lack of process but a lack of real-time visibility across the processes that already exist. Manufacturing finance leak prevention software addresses precisely this gap, providing a continuous control layer that connects procurement, production, inventory, and accounts payable data to detect anomalies before they become losses.

Key Takeaways

- Manufacturing finance leak prevention software bridges the gap between ERP transaction processing and real-time anomaly detection across procurement, production, and inventory.

- Duplicate invoices, price drift from contracts, and unverified goods receipts are among the most common and costly sources of financial leakage in factories.

- Production cost anomaly detection identifies yield problems, labor variances, and overhead misallocations while there is still time to correct them.

- A layered approach combining static business rules with behavioral anomaly detection delivers significantly stronger manufacturing financial controls than either method alone.

- Most organizations see their first actionable findings within weeks of deployment, with direct ROI from recovered overpayments and blocked duplicate payments.

What Is Manufacturing Finance Leak Prevention Software and How Does It Protect Margins?

This category of software belongs to the broader discipline of Continuous Controls Monitoring (CCM), but it is purpose-built for the complexity of a plant environment. Unlike generic analytics dashboards, it ingests transactional data from multiple ERP modules—purchasing, warehouse management, production planning, cost accounting, and accounts payable—and applies hundreds of cross-referencing checks in real time. The goal is to surface “financial leaks”: the cumulative result of duplicate invoices, price deviations from contracts, goods received but never ordered, standard costs that have drifted from reality, and inventory write-offs that nobody questioned.

What makes this approach different from standard accounting reviews is the bridge it builds between floor-level production data and the balance sheet. A cost variance report generated at month-end tells you that something went wrong. Manufacturing finance leak prevention software tells you what went wrong, in which transaction, on which day, involving which supplier or work order—while there is still time to act. For CFOs, controllers, and internal auditors in manufacturing, this shift from reactive reporting to proactive detection represents a fundamental improvement in manufacturing financial controls.

Tip

Start your evaluation by mapping the specific ERP modules your organization uses for procurement, production, and finance. The value of continuous monitoring scales directly with the number of data sources it can cross-reference simultaneously.

Why Do Financial Leaks Persist in Factories Despite Advanced ERP Systems?

Enterprise Resource Planning systems are exceptional at processing transactions. They enforce workflow sequences, manage master data, and generate ledger entries with precision. However, they were not designed to be detectives. An ERP will faithfully record a purchase order, match it to a goods receipt, and post the corresponding invoice—even if that invoice is a near-duplicate of one already paid, or if the unit price deviates from the negotiated contract by just enough to avoid a tolerance flag.

The core issue is what practitioners call the “ERP Gap.” Data silos between procurement, production, and finance modules create blind spots. A purchasing manager may not see that a supplier’s bank details were changed moments before a large payment run. A cost accountant may not know that a specific raw material’s consumption on the shop floor has quietly increased by fifteen percent over three months. International auditing standards, such as ISA 240 on fraud responsibilities, emphasize the need for a “fraud lens” in evaluating controls—an analytical mindset that ERPs simply do not possess on their own. When you add high transaction volumes, multiple plant locations, and the inevitable pressure of manual overrides, it becomes clear why leaks persist even in well-run factories.

Did You Know

According to the Association of Certified Fraud Examiners, the median duration of an occupational fraud scheme is 12 months before detection. In manufacturing environments with high transaction volumes, that window can stretch even longer when controls rely solely on periodic review cycles.

How Does the Software Facilitate Plant Procurement Fraud Prevention?

Factory sourcing is one of the highest-risk areas for financial leakage. The volume of purchase orders, the number of suppliers, and the speed at which materials must arrive create an environment where irregularities can hide in plain sight. Plant procurement fraud prevention relies on linking entities—supplier, employee, invoice, purchase order, site—and analyzing relationships that no single ERP report would reveal.

A critical detection mechanism is the automated three-way match: comparing the purchase order, the goods receipt, and the supplier invoice across quantity, price, and terms. The PCAOB’s Auditing Standard No. 2 Appendix B provides a clear example of this control, including the generation of exception reports for items that do not reconcile. Modern software extends this concept by adding tolerance intelligence—flagging not just hard mismatches but also “soft” deviations that fall just below manual review thresholds. The OECD’s procurement red-flag framework lists contract splitting below authorization limits as a common indicator, and effective software detects exactly this pattern by analyzing order clustering by date, supplier, and commodity.

Identifying Duplicate Vendors and Ghost Suppliers

Duplicate vendor records are among the oldest procurement vulnerabilities, yet they remain surprisingly common. A supplier may appear under slightly different names, with one record holding the legitimate bank account and another redirecting payments elsewhere. Algorithms that analyze naming similarity, shared tax identifiers, overlapping addresses, and identical bank details can surface these duplicates without requiring a massive data-cleansing project. The system flags the overlap; the procurement team investigates and consolidates.

Tip

Run a vendor master deduplication scan as one of your first actions after deploying continuous monitoring. Many organizations discover three to five percent of their active vendor records are duplicates—each one representing a potential avenue for misdirected payments.

Detecting Red Flags in Vendor Master Data Changes

A change to a supplier’s bank account days before a scheduled payment run is a classic red flag—whether it represents a legitimate update or a fraudulent diversion. Effective leak prevention software monitors these master data changes in real time, cross-referencing the timing against upcoming disbursements, the identity of the user who made the change, and whether the change followed the required approval workflow. When something deviates, the alert reaches the right person before money leaves the organization.

Did You Know

Business email compromise (BEC) schemes that target vendor bank account changes cost organizations an estimated $2.7 billion in reported losses in a single year, according to FBI Internet Crime Complaint Center data. Real-time master data change monitoring is one of the most effective countermeasures.

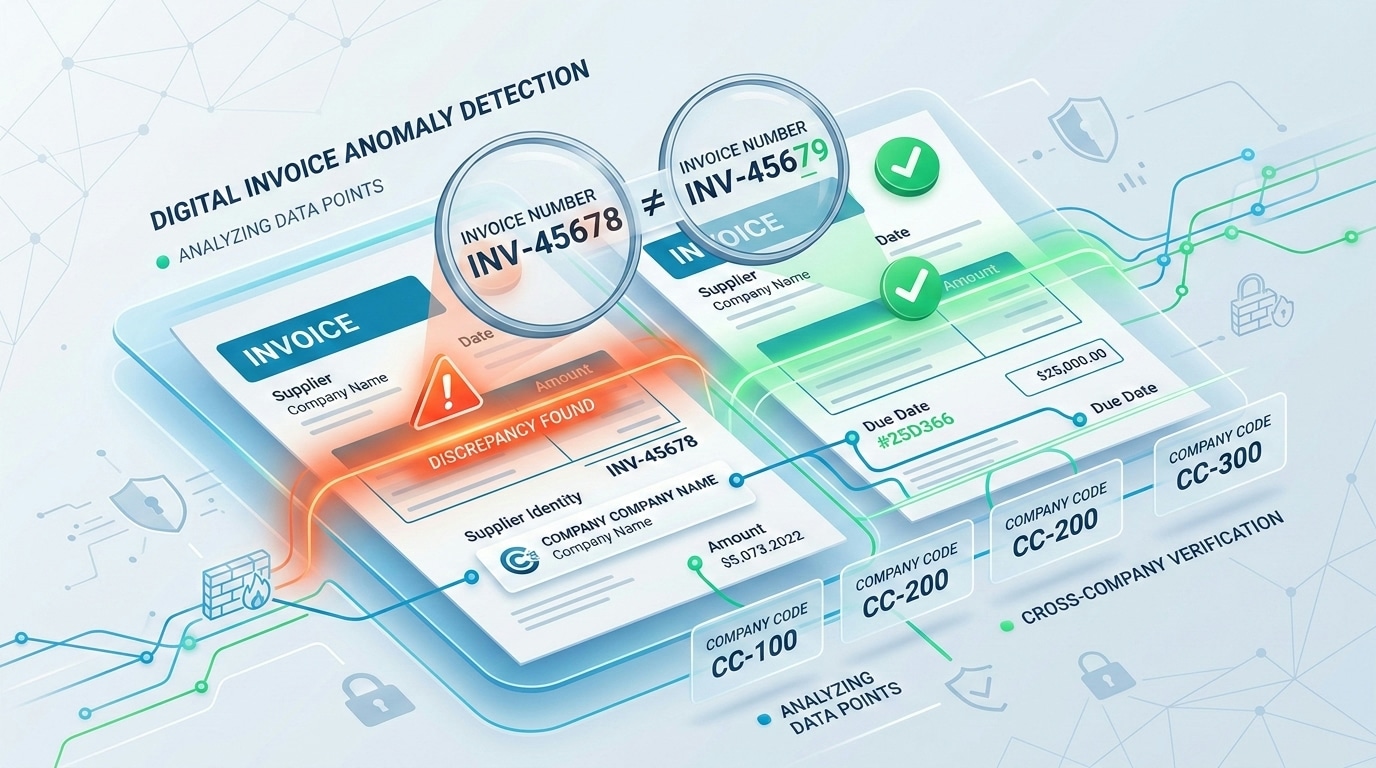

Preventing Payment on Duplicate or Near-Duplicate Invoices

Duplicate invoice detection sounds straightforward, but in practice it is anything but. Sophisticated duplicates do not share the same invoice number. Instead, they involve a slight change in a digit, a rounded amount, a split into two smaller invoices, or submission to two different business units within the same group. Standard ERP duplicate checks, which typically compare invoice numbers within a single company code, miss these variations entirely.

Manufacturing finance leak prevention software approaches the problem differently. It compares invoices across multiple dimensions simultaneously: supplier identity (including fuzzy matches), total amount and line-item amounts, dates, purchase order references, and goods receipt links. It also operates across company codes and plant locations, catching the scenario where the same supplier submits an identical charge to two subsidiaries. The result is a significant reduction in overpayments—often one of the fastest areas to demonstrate measurable ROI.

Tip

When configuring duplicate invoice detection, extend your matching logic beyond the single company code. Cross-entity duplicate payments—where the same supplier bills two subsidiaries for the same service—are among the most commonly missed leaks in multi-plant manufacturing groups.

How Does Price Drift Get Detected Before It Becomes a Margin Problem?

Negotiated contracts and framework agreements establish the prices a factory should be paying for raw materials, components, and services. Yet “price drift” happens gradually: a supplier invoices at a slightly higher unit price, or substitutes an alternative part number that falls outside the agreement scope. Over hundreds of transactions, these small deviations accumulate into a material impact on cost of goods sold.

The software performs automatic comparisons between each invoice line and the applicable contract, catalog, or historical price baseline. It accounts for currency, unit of measure, volume tiers, and effective dates. Critically, it also identifies workarounds—such as when a buyer selects a non-contracted item code for a material that is clearly covered by an existing framework—by analyzing item descriptions and commodity classifications. This level of scrutiny would be impractical to perform manually at scale, but it is exactly what continuous monitoring was designed for.

Did You Know

Research from procurement analytics firms consistently shows that three to five percent of total spend in manufacturing organizations involves pricing that deviates from negotiated contract terms. For a company spending $100 million annually on materials, that represents $3 to $5 million in potential overpayments.

Catching Quantity Anomalies and Payments for Goods Never Received

In a busy receiving dock, errors happen. A partial shipment is scanned as a full receipt. A return is processed but the credit memo never arrives. Goods are received weeks after the invoice has already been paid. These scenarios are not necessarily fraudulent, but they all result in the organization paying for something it did not fully receive.

| Scenario | How It Creates a Leak | Detection Approach |

|---|---|---|

| Partial receipt recorded as full | Overpayment for undelivered quantity | Quantity match between GR and PO with tolerance analysis |

| GR posted after invoice payment | Payment before physical verification | Timestamp sequencing: payment date vs. receipt date |

| Open GR/IR balance aging | Unresolved liabilities or overstated inventory | Aging report with threshold alerts by supplier and plant |

| Recurring “round number” receipts | Possible fictitious or estimated entries | Pattern analysis on receipt quantities per user and site |

By monitoring these patterns across all receiving locations, the software provides finance teams with a clear picture of where the control process is breaking down and where intervention is needed most urgently.

Your factory generates thousands of transactions every week. How many contain hidden overpayments, price deviations, or unverified receipts? Detelix finds them in real time.

Utilizing Production Cost Anomaly Detection to Stop Waste

Moving from procurement to the production floor introduces a different set of financial risks. Production cost anomaly detection focuses on the gap between what a product should cost to manufacture (the standard) and what it actually cost. When that gap widens beyond expected tolerances, it signals a leak—whether from excessive material consumption, inaccurate labor reporting, or misallocated overhead.

The software continuously compares standard versus actual costs at the level of individual work orders, production lines, shifts, and batches. A sudden spike in material usage for a particular product could indicate a yield problem, a BOM (Bill of Materials) error, or even physical diversion of raw materials. A persistent labor variance on a specific line might point to inaccurate time reporting or an outdated routing. Industrial data frameworks, such as those used by national statistical bureaus to track manufacturing output and labor inputs, rely on exactly these integrated data points to assess operational health. The same principle applies at the company level: when you connect material, labor, and overhead data in real time, you can trace a cost anomaly back to its root cause before it compounds.

Material Consumption, Yield, and Scrap Leakage

Excessive scrap or unexplained yield loss is one of the most direct ways a factory loses money. If a production run consistently uses more raw material than the BOM specifies, the variance flows straight to cost of goods sold. The software flags these deviations by batch, by material, and by operator—allowing production and finance to investigate jointly rather than discovering the problem at month-end close.

Tip

Configure your scrap and yield monitoring to alert at the batch level, not just at the monthly aggregate. A yield issue that compounds silently over four weeks creates a far larger financial impact than one caught and corrected on day two.

Labor and Overhead Variances That Signal Inaccurate Costing

When reported labor hours diverge significantly from standard routings, it may indicate that the routing is outdated, that overtime is being misallocated, or that production efficiency has changed without a corresponding update to the cost model. Overhead absorption variances often follow the same pattern. Detecting these discrepancies early preserves the integrity of product costing and prevents distorted margin analysis.

The Role of Inventory Valuation Controls in Financial Accuracy

Incorrect inventory valuation is a primary source of “phantom profits” in manufacturing. If raw materials or finished goods are carried at inflated values—because standard costs have not been updated, slow-moving stock has not been written down, or inter-warehouse transfers have masked losses—the balance sheet overstates assets and the income statement overstates margins. The correction, when it inevitably comes, arrives as a painful quarterly write-down.

International accounting standards under IAS 2 require that inventory be measured at the lower of cost and net realizable value (NRV), with clear guidance on which cost components to include. Inventory valuation controls embedded in leak prevention software enforce these principles continuously. They monitor for outdated standard costs, flag items whose market value has dropped below carrying cost, identify abnormal manual adjustments, and track transfers between warehouses that could obscure obsolescence. The outcome is a more accurate balance sheet and fewer surprises during close.

Did You Know

A study of manufacturing restatements found that inventory-related misstatements accounted for a disproportionate share of financial corrections. The most common cause was not fraud but the failure to update standard costs and write down slow-moving stock on a timely basis.

Rules vs. Anomaly Detection: Which Approach Delivers Real Control?

A common question from finance leaders evaluating manufacturing financial controls is whether to rely on static business rules or on data-driven anomaly detection. The honest answer is that both are necessary, and neither is sufficient alone. Rules excel at catching known, well-defined problems: an invoice exceeding a specific threshold, a payment to a blocked vendor, or a tolerance breach on a three-way match. Anomaly detection excels at surfacing unknown problems: a supplier whose invoicing pattern has changed subtly over six months, a cost center whose overhead allocation has drifted without any single transaction triggering a rule.

The PCAOB’s Auditing Standard No. 2 articulates a key principle: effective internal controls typically combine preventive and detective mechanisms. Rules are preventive—they block or flag before execution. Anomaly detection is detective—it identifies patterns that have already occurred but have not yet been investigated. Platforms like Detelix integrate both approaches; our hundreds of algorithms ensure every action in the ERP system is cross-checked against rules and behavioral baselines simultaneously. This layered approach is what transforms routine monitoring into real control.

Tip

When building your control framework, start with rules for your highest-risk, best-understood scenarios (duplicate payments, three-way match failures), then layer anomaly detection on top to catch the patterns you have not anticipated yet. Review and refine thresholds quarterly based on investigation outcomes.

Reducing Alert Fatigue and False Positives in a High-Volume Factory

One of the most practical challenges in deploying continuous monitoring in manufacturing is the sheer volume of transactions. A mid-sized factory may generate thousands of purchase orders, goods receipts, and production confirmations every week. If the system flags even a small percentage without proper prioritization, the finance team drowns in alerts and stops trusting the tool.

The solution lies in risk scoring and contextual grouping. Instead of presenting every deviation as an equal-priority alert, the software assigns a risk score based on the monetary impact, the historical behavior of the supplier or cost center, the nature of the deviation, and the proximity to a payment event. Related anomalies are grouped into a single investigation case rather than scattered across dozens of individual alerts. The COSO Monitoring guidance emphasizes that effective monitoring systems must evolve over time, incorporating feedback from investigators to refine thresholds and reduce noise. This continuous improvement loop is what separates a useful control tool from an ignored one.

Did You Know

Organizations that implement risk-scoring and contextual grouping in their continuous monitoring systems typically reduce false positive rates by 60 to 80 percent within the first six months, according to internal benchmarking data from CCM deployments across manufacturing sectors.

Connecting Procurement, Production, Inventory, and Finance Into a Single Control Layer

The most powerful capability of manufacturing finance leak prevention software is its ability to trace a financial anomaly from the ledger all the way back to the operational event that caused it. A cost variance on a finished goods line can be decomposed into its material, labor, and overhead components. A material variance can be traced to a specific purchase order, a specific supplier invoice, and a specific goods receipt. An inventory discrepancy can be linked to a production backflush that consumed more than the BOM specified.

This cross-module traceability is what allows finance and operations to collaborate on root-cause analysis instead of debating whose data is correct. It also provides the audit trail that external auditors and regulators expect. Without this integrated view, each department operates in its own silo, and the organization lacks the visibility needed to identify where value is actually being lost.

Tip

When presenting continuous monitoring results to leadership, trace at least one finding from the financial anomaly all the way back to the originating operational transaction. This end-to-end traceability demonstrates the system’s value far more effectively than aggregate statistics alone.

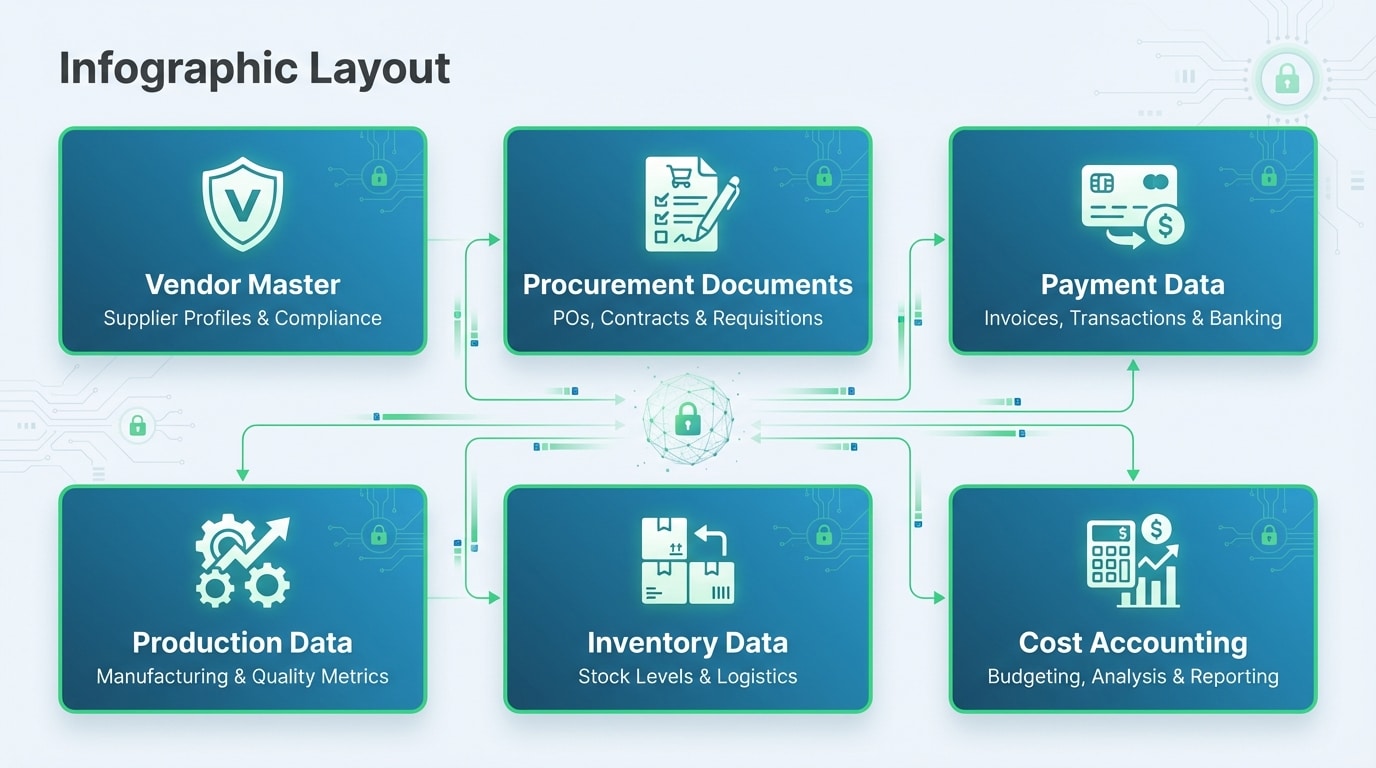

What Data Is Required to Establish Effective Manufacturing Financial Controls?

| Data Category | Core Elements | Enhanced Elements (Deeper Analysis) |

|---|---|---|

| Vendor Master | Name, tax ID, bank details, status | Ownership records, related-party flags |

| Procurement Documents | POs, contracts, goods receipts, invoices | Framework agreements, catalog prices, RFQ history |

| Payment Data | Payment runs, cleared items, bank statements | Payment terms, early-payment discounts taken |

| Production Data | Work orders, BOMs, routings, confirmations | Quality inspection results, rework orders |

| Inventory Data | Stock movements, valuations, cycle counts | Aging reports, warehouse transfer logs, write-off approvals |

| Cost Accounting | Standard costs, actual costs, variance postings | Activity rates, overhead allocation keys |

At a minimum, the system needs vendor master data, purchasing documents, goods receipts, invoices, payment records, inventory movements, BOMs, work orders, and standard versus actual cost postings. As the organization adds HR and authorization data, contract details, and quality records, the software’s ability to detect subtle patterns and reduce false positives improves significantly. Detelix, for example, is designed to connect to existing ERP environments and begin generating actionable findings from available data without requiring a lengthy data-cleansing phase first.

How Long Does Implementation Take and What Does the Process Look Like?

A common concern among finance leaders is that deploying a new control layer will be a multi-year IT project. In practice, modern manufacturing finance leak prevention software follows a phased approach that delivers early value. The typical sequence begins with data connectivity—establishing automated feeds from the ERP. Next comes entity mapping: aligning vendor records, material masters, and organizational hierarchies so the system understands your specific business structure.

The first use cases are usually deployed in procurement and accounts payable, because these areas offer the fastest, most measurable returns. The system runs in parallel with existing processes, generating findings that the finance team validates. Based on that feedback, thresholds are refined and additional use cases—production cost monitoring, inventory valuation controls—are activated. Most organizations see their first actionable alerts within weeks, not months. Detelix supports this phased rollout with pre-built control libraries tailored to manufacturing environments, which significantly reduces the configuration effort compared to building controls from scratch.

Did You Know

Pre-built control libraries for manufacturing environments typically contain 200 to 400 individual detection rules and anomaly patterns covering procurement, production, inventory, and accounts payable—eliminating the need to design each control from scratch and reducing deployment time by months.

Measuring the ROI of a Leak Prevention Strategy

Return on investment in this domain is unusually tangible. The most direct metric is “recovered value”—the sum of overpayments identified and recovered, duplicate invoices blocked before payment, and contract-price deviations corrected. Beyond direct savings, organizations measure the reduction in hours spent on manual reconciliation and investigation, the improvement in month-end close accuracy, and the decrease in external audit findings related to procurement and inventory controls.

There is also a deterrence effect that is harder to quantify but no less real. When employees and suppliers know that every transaction is being monitored in real time, the likelihood of intentional manipulation decreases. This “culture of compliance” compounds over time, reducing the total volume of exceptions and allowing the finance team to focus on strategic analysis rather than firefighting.

A Practical Scenario: What Happens When a Factory Ignores These Controls?

Consider a mid-sized manufacturer with three plants and over two thousand active suppliers. Without continuous monitoring, the following issues accumulate silently over twelve months: several hundred thousand dollars in duplicate or near-duplicate invoice payments across subsidiaries; a raw material supplier whose invoiced price gradually exceeded the contract rate, resulting in six figures of overpayment; a production line with a persistent yield issue that went undetected because variance reports were only reviewed quarterly; and an inventory of slow-moving finished goods carried at full standard cost despite market prices having dropped below production cost. Each issue, individually, might have been caught eventually—during an annual audit, a supplier renegotiation, or a physical inventory count. But “eventually” means after the cash has left the company and after the financial statements have been filed.

Tip

Calculate a rough estimate of your organization’s leak exposure before beginning a vendor evaluation. Multiply your annual accounts payable volume by conservative error rates (0.5 to 1 percent for duplicates, 2 to 3 percent for price drift) to establish a baseline. The resulting figure almost always justifies a closer look at continuous monitoring.

How Should You Evaluate Software for Manufacturing Finance Leak Prevention?

Not all solutions are created equal. When assessing options, consider whether the software can operate across multiple ERP modules and company codes simultaneously, rather than addressing procurement and production in separate silos. Evaluate the depth of its detection logic: does it go beyond simple rule-based checks to include behavioral analysis and entity-relationship mapping? Ask how the system handles false positives—does it offer risk scoring, contextual grouping, and a feedback mechanism for investigators?

Equally important is the question of implementation speed and ongoing maintenance. A solution that requires months of custom development before producing its first finding may not deliver value fast enough to justify the investment. Look for platforms with pre-configured control libraries for manufacturing, the ability to connect to your ERP without major middleware projects, and a clear workflow for routing alerts to the right team members for investigation and resolution.

Detelix Continuous Monitoring Solutions

Proactive Monitoring

Continuous, automated oversight of all ERP transactions to detect financial anomalies, duplicate payments, and control gaps before they become losses.

Real-Time Alerts

Instant, risk-scored notifications for high-priority anomalies—delivered to the right team members with full transaction context for rapid investigation.

Gatekeeper

Preventive control layer that blocks high-risk transactions—such as payments to flagged vendors or duplicate invoices—before they execute in the ERP.

Experience & Expertise

Decades of combined expertise in financial controls, ERP systems, and manufacturing operations—backed by ISO 27001 and ISO 27799 certifications.

See Detelix in Action

Frequently Asked Questions

Can this software detect innocent human errors, or only intentional fraud?

It detects both. In fact, the majority of financial leaks in manufacturing result from unintentional errors—data entry mistakes, outdated master data, misconfigured tolerances—rather than deliberate fraud. The software does not distinguish intent; it surfaces the anomaly. Whether the root cause is a typo or a scheme is determined during the investigation that follows.

Does deploying continuous monitoring slow down day-to-day operations?

No. The monitoring runs in parallel with existing ERP processes, analyzing transaction data as it is created. It does not insert approval steps or delay payments unless the organization specifically configures it to block high-risk transactions. The standard approach is to alert and investigate, not to halt the business.

How does the system handle factories in different countries with different ERP instances?

Leading solutions are designed to normalize data across multiple ERP systems, company codes, currencies, and languages. This is critical for manufacturing groups with global operations, because many of the most damaging leaks—such as cross-entity duplicate payments—are invisible when each site is monitored in isolation.

What is the typical payback period for this type of investment?

Many organizations recover the cost of the software within the first few months of operation, based solely on duplicate payments identified and contract-price deviations corrected. The payback period depends on transaction volume and the maturity of existing controls, but it is common for the first significant finding to exceed the annual license cost.

Is this relevant only for large manufacturers, or also for mid-market companies?

Mid-market manufacturers often face higher relative risk because they have fewer dedicated control staff and less segregation of duties. The volume of transactions may be lower, but the impact of a single undetected overpayment or cost anomaly on a smaller revenue base is proportionally larger. The software scales to fit the complexity of the organization.

Is Your Factory Operating With Real Control or Just the Appearance of It?

If procurement errors surface only during quarterly reviews and inventory adjustments consistently surprise you at year-end, there is a gap between the controls you believe you have and the visibility you actually need. Close that gap with Detelix.