Stop Internal Fraud Before It Drains Your Bottom Line

Detelix continuously monitors every ERP transaction to detect occupational fraud in real time — so you catch schemes in days, not months.

- What Is Occupational Fraud and Why Is It a Critical Risk?

- How Detection Differs from Prevention

- Primary Red Flags for Workplace Fraud Detection

- Which Departments Are Most Susceptible?

- Expense Reimbursement Fraud Scenarios

- Vendor and Invoice Fraud: Identifying Shell Companies

- Are Anonymous Reporting Channels Effective?

- Most Effective Ways to Detect Occupational Fraud

- Can AI and Machine Learning Improve Detection?

- A Common Mistake: Treating Detection as a One-Time Project

- Reducing False Positives Without Missing Real Fraud

- When Does Suspicion Become an Investigation?

- Building a Detection Program That Lasts

- Key Metrics for Measuring Detection Effectiveness

- Frequently Asked Questions

Every organization relies on trusted employees to handle sensitive financial processes — from approving payments and managing vendor records to processing payroll and reconciling accounts. Yet it is precisely this trust, when combined with opportunity and insufficient oversight, that creates the conditions for occupational fraud detection failures. According to industry research, the typical organization loses an estimated five percent of its annual revenue to internal fraud, and the median scheme runs for twelve months before anyone notices. For CFOs, controllers, and internal auditors, the question is no longer whether fraud could happen inside your organization — it is whether your current controls would catch it in time.

Key Takeaways

- Occupational fraud costs organizations an estimated 5% of annual revenue, with the median scheme lasting 12 months before discovery.

- Detection and prevention are complementary disciplines — automated, continuous monitoring closes the gap that periodic audits leave open.

- Red flags span both operational anomalies (sequential invoices, threshold-hugging payments) and behavioral signals (lifestyle changes, refusal to share duties).

- Anonymous reporting channels remain the single most effective discovery method, outperforming internal audits and management reviews combined.

- AI-enhanced detection layers rule-based checks for known schemes with anomaly-detection models for emerging risks, dramatically reducing response times.

- Sustainable programs require ongoing recalibration — treating detection as a continuous discipline, not a one-time project.

What Is Occupational Fraud and Why Is It a Critical Risk for Modern Enterprises?

Employee occupational fraud is the deliberate misuse or misapplication of an employer’s resources by someone who exploits the access and trust granted through their role. Unlike external attacks, these schemes are carried out by insiders who understand approval workflows, system permissions, and reporting blind spots — making them exceptionally difficult to spot through conventional means.

Fraud researchers often frame the problem through the “Fraud Triangle”: Opportunity (weak controls or oversight gaps), Pressure (personal financial stress, lifestyle demands), and Rationalization (the internal justification that “everyone does it” or “I deserve this”). When all three elements converge, the probability of fraud rises sharply. The ACFE 2024 Report to the Nations documents that the median loss per case exceeds $145,000 — and that figure climbs dramatically when senior managers or executives are involved.

Did You Know

Organizations with proactive data monitoring and analysis detect fraud 52% faster than those relying solely on passive detection methods such as confessions or accidental discovery, according to the ACFE.

How Does Occupational Fraud Detection Differ from Fraud Prevention?

Prevention and detection are complementary, not interchangeable. Prevention focuses on closing the door before fraud begins — segregation of duties, approval hierarchies, access restrictions, and clear policies. Detection, on the other hand, assumes that some schemes will bypass preventive controls and concentrates on identifying suspicious activity as early as possible.

The critical metric is the detection gap: the elapsed time between the moment a fraud starts and the moment someone discovers it. Longer gaps mean larger losses. Even organizations with robust prevention programs need a secondary layer that continuously scans for anomalies, because no set of policies can anticipate every creative workaround an insider might devise. This is where automated, real-time monitoring changes the equation — Detelix’s hundreds of algorithms ensure every action in the ERP system is cross-checked against known risk patterns, closing gaps that manual reviews simply cannot cover at scale.

Tip

Map your detection gap for each critical process. Measure the average time between when a suspicious transaction occurs and when your team identifies it. If the gap exceeds 30 days for any high-value workflow, prioritize automated monitoring for that process immediately.

What Are the Primary Red Flags for Workplace Fraud Detection?

Recognizing warning signs early is the foundation of effective workplace fraud detection. Red flags generally fall into two categories: operational anomalies visible in data, and behavioral signals observable in the workplace. Neither category alone proves fraud, but together they build a pattern that warrants investigation.

Operational Anomalies in Accounts Payable and Procurement

Look for sequential invoice numbers from a single vendor, payments consistently just below approval thresholds, duplicate invoice amounts with different reference numbers, vendors sharing a bank account or address with an employee, and purchase orders created after the invoice date. Each anomaly on its own may have an innocent explanation; clusters of anomalies tied to the same employee or vendor rarely do.

Tip

Create a “threshold proximity report” that flags all transactions landing within 5% of approval limits. Fraudsters often learn exactly where the approval ceiling sits and deliberately structure payments just below it to avoid secondary review.

Behavioral Indicators as Supporting Context

The ACFE Global Fraud Survey notes that behavioral red flags — living beyond means, unusually close relationships with vendors, resistance to audits, refusal to take vacations, and insistence on handling tasks alone — are present in a significant majority of confirmed cases. These signals should never be used as sole evidence, but they provide valuable context when data anomalies surface.

Did You Know

In 42% of occupational fraud cases documented by the ACFE, the perpetrator was living beyond their apparent means. This behavioral indicator, when paired with transactional anomalies, significantly increases the confidence level that a scheme is underway.

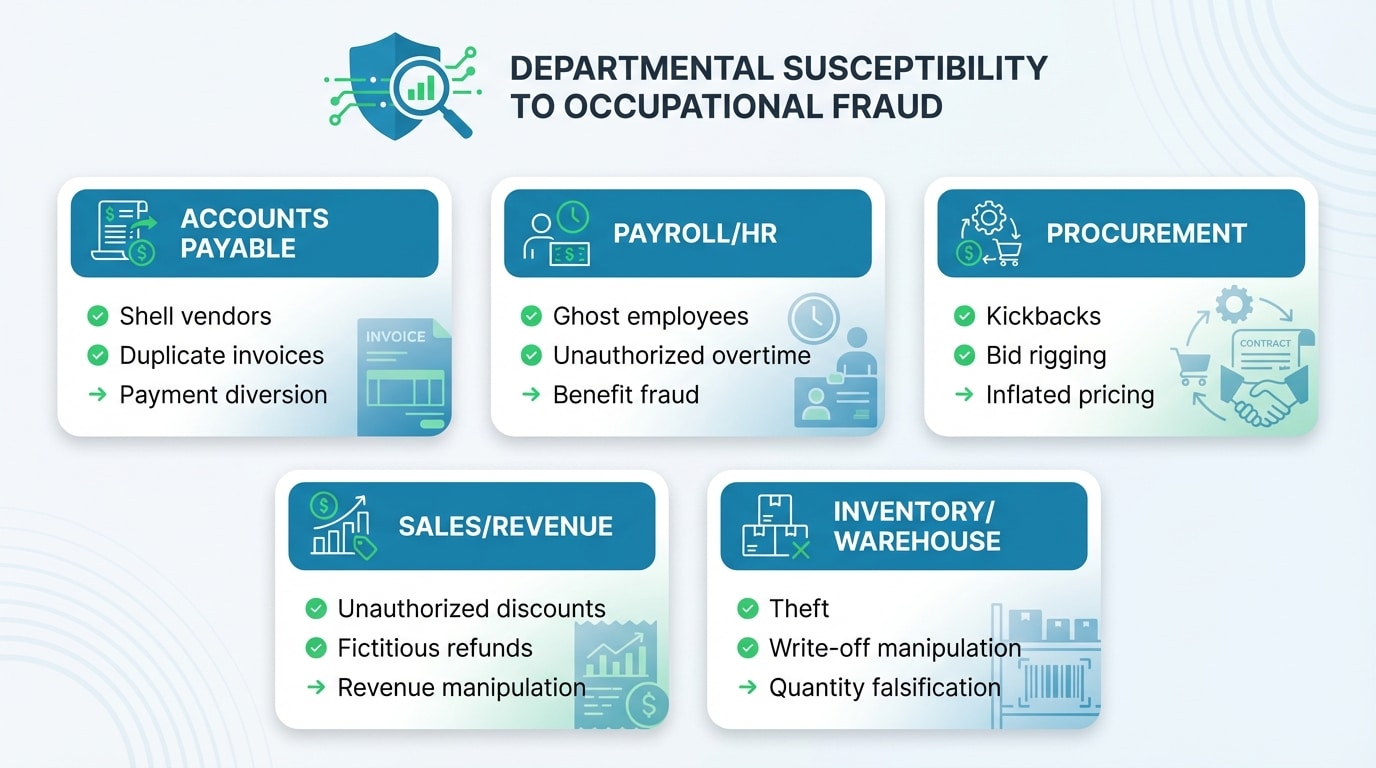

Which Departments Are Most Susceptible to Employee Occupational Fraud?

While fraud can originate anywhere, certain departments carry inherently higher risk due to their direct access to money, assets, or financial records. Accounting and finance teams handle payment approvals and journal entries. Procurement manages vendor relationships and purchasing decisions. Operations controls inventory and logistics. Sales teams influence pricing, discounts, and customer refunds.

| Department | Common Scheme Types | Key Detection Approach |

|---|---|---|

| Accounts Payable | Shell vendors, duplicate invoices, payment diversion | Vendor master-data cross-checks, IBAN change alerts |

| Payroll / HR | Ghost employees, unauthorized overtime, benefit fraud | Headcount reconciliation, attendance vs. payment matching |

| Procurement | Kickbacks, bid rigging, inflated pricing | Spend analysis, single-source vendor concentration |

| Sales / Revenue | Unauthorized discounts, fictitious refunds, revenue manipulation | Pricing & Discounts Monitoring, refund pattern analysis |

| Inventory / Warehouse | Theft, write-off manipulation, quantity falsification | Cycle counts vs. system records, shrinkage trend analysis |

Understanding where risk concentrates allows you to allocate detection resources proportionally rather than spreading them uniformly across the organization.

Tip

Rank your departments by fraud risk using a simple matrix: access to funds multiplied by transaction volume multiplied by the number of control weaknesses identified in your last audit. Focus your first round of automated monitoring on the top two departments in the ranking.

Expense Reimbursement Fraud: A Scenario That Slips Through Standard Approvals

Consider a mid-level manager who submits the same receipt twice — once as a scanned PDF, once as a photograph — attached to different expense reports weeks apart. Each claim falls comfortably below the threshold that triggers secondary review. Over eighteen months, small duplications accumulate into a significant loss. Standard approval workflows rarely catch this because the approver sees each report in isolation, without cross-referencing historical submissions.

Effective detection here requires automated matching: comparing receipt images or hashes, flagging identical amounts on adjacent dates, and benchmarking individual spending against peer-group averages. When your system can surface these patterns in real time, you move from hoping an auditor will eventually notice to knowing the moment a duplicate appears.

Did You Know

Expense reimbursement fraud has the lowest median loss per scheme among occupational fraud categories — approximately $50,000 — but it also has the highest frequency of occurrence, meaning it affects more organizations more often than costlier scheme types.

Vendor and Invoice Fraud: Identifying Shell Companies Through Data Cross-References

Shell vendor schemes are among the costliest forms of employee occupational fraud. An employee creates a fictitious supplier in the ERP, routes invoices for services never rendered, and approves payment — sometimes cycling the funds back to a personal account. The scheme thrives on weak vendor onboarding controls and limited post-payment review.

To detect occupational fraud of this type, organizations should cross-reference vendor bank account details against employee payroll records, flag vendors registered at residential addresses, monitor vendors with unusually high invoice volumes relative to their setup date, and investigate cases where the same person both creates the vendor record and approves the payment. Automated ERP monitoring makes these cross-checks continuous rather than periodic, eliminating the window of opportunity that annual audits leave open.

Your ERP holds the evidence — Detelix surfaces it automatically. Detect shell vendors, duplicate invoices, and payment anomalies before they become losses.

Are Anonymous Reporting Channels Really Effective for Discovery?

Yes — and the data is clear. Tips remain the single most common way occupational fraud is discovered, responsible for more detections than internal audits, management reviews, and external audits combined. The ACFE’s research on fraud awareness shows that organizations with active reporting hotlines detect fraud significantly faster and incur substantially lower median losses.

For a reporting channel to work, however, it must be supported by a clear non-retaliation policy, multiple submission methods (phone, web form, email), communication to both employees and third-party vendors, and a structured triage process that ensures every report is reviewed and escalated appropriately. A hotline that exists on paper but is poorly publicized or rarely monitored offers little real protection.

Tip

Publicize your reporting channel at least quarterly through internal communications, and include it in vendor-facing contracts. Organizations that actively promote their hotlines receive 46% more tips than those that only mention the channel during onboarding.

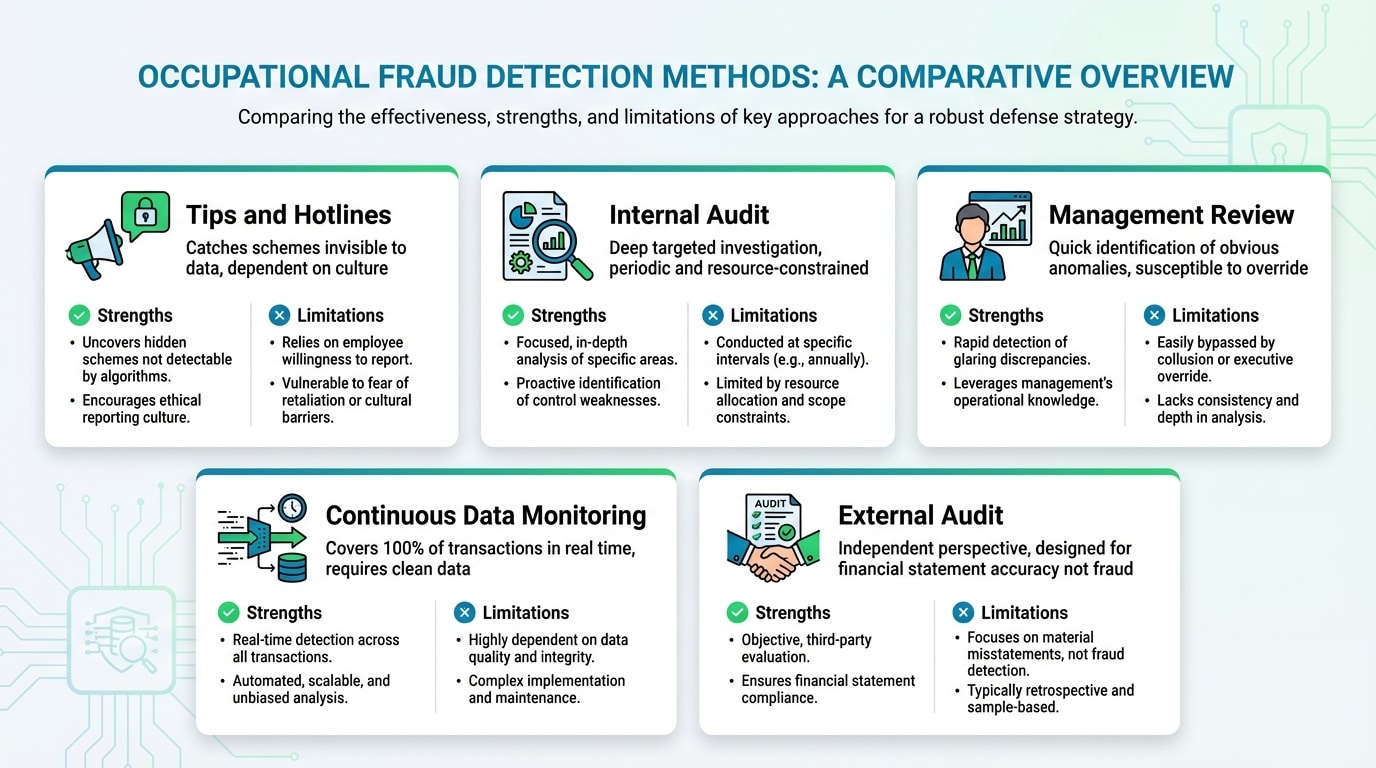

What Are the Most Effective Ways to Detect Occupational Fraud Today?

Detection methods range from traditional to technology-driven, and the most resilient programs layer several approaches together.

| Detection Method | Strengths | Limitations |

|---|---|---|

| Tips and Hotlines | Catches schemes invisible to data (e.g., collusion, kickbacks) | Dependent on culture and trust; volume of false reports |

| Internal Audit | Deep, targeted investigation capability | Periodic, resource-constrained, reactive |

| Management Review | Quick identification of obvious anomalies | Susceptible to override by senior fraudsters |

| Continuous Data Monitoring | Covers 100% of transactions in real time | Requires clean data and tuned rules to avoid alert fatigue |

| External Audit | Independent perspective | Designed for financial statement accuracy, not fraud detection |

The shift across industries is unmistakable: organizations are moving from reliance on periodic reviews toward proactive, continuous monitoring. When your system scans every transaction as it occurs — flagging deviations from policy, unusual patterns, and control bypasses — you gain the ability to intervene before money leaves the organization rather than investigating months after the fact.

Did You Know

Organizations using continuous transaction monitoring detect fraud 58% faster than those relying on traditional periodic audits alone. The median loss for organizations with proactive monitoring is also roughly half that of organizations without it.

Can AI and Machine Learning Improve Workplace Fraud Detection?

Rule-based detection is essential for catching known schemes: duplicate invoices, payments above threshold without approval, IBAN changes before large transfers. But experienced fraudsters learn the rules and design schemes that stay just outside the parameters. This is where machine-learning models add value — they identify statistical anomalies, cluster unusual behaviors, and score transactions by risk without being constrained by predefined thresholds.

That said, AI is not a silver bullet. Research published in 2025 on algorithmic deception highlights challenges around transparency, data quality, and the risk of false positives when models are poorly calibrated. The most practical approach combines a rules layer for known fraud patterns with an anomaly-detection layer for emerging risks, topped by human review for final judgment. Detelix applies this layered methodology, cross-checking actions across HR, finance, and procurement modules so that context — not just isolated data points — drives each alert.

Tip

When evaluating AI-driven fraud detection tools, ask the vendor to demonstrate their false positive rate on a dataset similar to your transaction profile. A system that generates thousands of alerts daily without actionable context will exhaust your team faster than manual reviews ever did.

A Common Mistake: Treating Detection as a One-Time Project

Many organizations invest in a fraud risk assessment, implement a set of controls, and then move on — treating detection as a completed project rather than an ongoing discipline. Fraud schemes evolve as processes change, new employees join, systems are upgraded, and business relationships shift. A detection rule that was effective two years ago may no longer match the way your ERP is configured today.

Sustainable programs require periodic recalibration: reviewing alert effectiveness, updating rules to reflect process changes, and measuring detection accuracy over time. According to GAO’s Standards for Internal Control, monitoring activities must be embedded into normal operations and evaluated regularly to ensure they continue to operate effectively.

Did You Know

The GAO Green Book emphasizes that monitoring should be “ongoing” — built into routine operations rather than conducted as separate, periodic exercises. Organizations that embed detection into daily workflows reduce their average fraud duration by more than 50%.

How Do You Reduce False Positives Without Missing Real Fraud?

Alert fatigue is one of the most common reasons detection programs fail in practice. When analysts receive hundreds of low-quality alerts daily, they begin to dismiss warnings reflexively — and eventually miss the one that matters. Reducing noise without reducing coverage requires several deliberate strategies.

First, segment alerts by business context: a payment pattern that is normal for one department may be anomalous for another. Second, use dynamic thresholds that adjust to seasonal volumes or project-based spending rather than static limits. Third, maintain clean master data — duplicate vendor records, outdated employee files, and inconsistent coding generate a disproportionate share of false alerts. Fourth, implement a severity scoring model that prioritizes alerts by amount, frequency, and the sensitivity of the process involved. Finally, measure precision and recall over time so you can tune parameters based on actual outcomes.

Tip

Schedule a monthly “alert quality review” where your team evaluates the top 20 alerts from the prior month. Track how many led to genuine findings versus false positives, and use those ratios to adjust detection thresholds and scoring weights.

When Does Suspicion Become an Investigation?

Not every alert warrants a full investigation — but every alert deserves a documented triage decision. A structured escalation framework typically moves through three stages: initial review (is there a legitimate business explanation?), preliminary assessment (does the pattern persist after accounting for known factors?), and formal investigation (evidence preservation, legal involvement, forensic analysis).

The critical rule is confidentiality. Premature disclosure can lead to evidence destruction, collusion, or legal liability. Before confronting any individual, secure digital logs, restrict system access where necessary, and involve legal counsel or forensic specialists who understand chain-of-custody requirements.

Did You Know

In approximately 22% of occupational fraud cases, the perpetrator attempted to destroy evidence after learning they were under suspicion. Maintaining strict confidentiality during the triage and preliminary assessment stages is essential to preserving the integrity of your investigation.

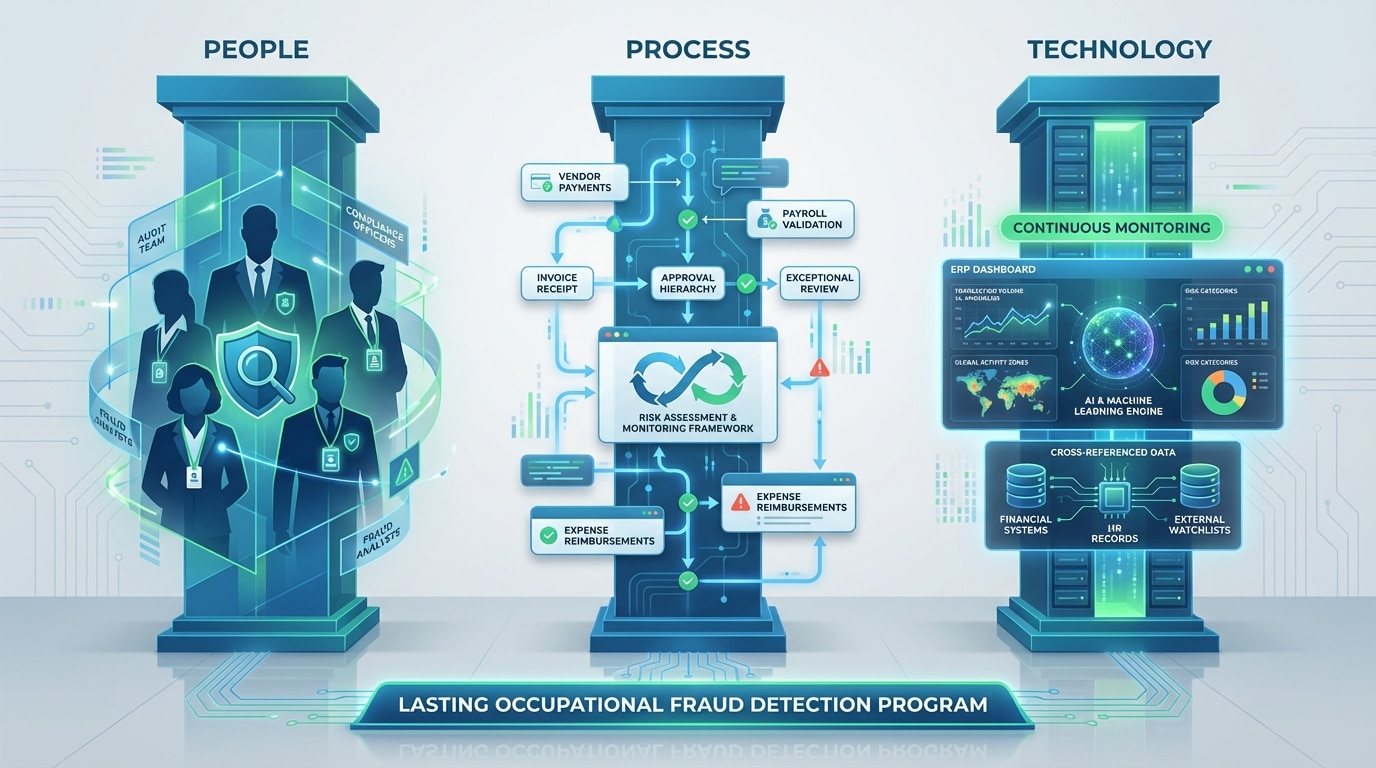

Building a Detection Program That Lasts: People, Process, Technology

A resilient occupational fraud detection program rests on three pillars. People: assign clear ownership — typically a combination of internal audit, finance, and compliance — and ensure investigators have the authority and skills to act. Process: map your highest-risk workflows (vendor payments, payroll, expense reimbursements, inventory adjustments), define fraud scenarios for each, and establish response protocols. Technology: deploy continuous monitoring that covers every transaction, not just samples, and integrates data from multiple ERP modules for cross-referencing.

This is where Detelix adds measurable value for organizations across Israel and internationally. The platform connects directly to your ERP environment, applies hundreds of pre-built and customizable detection algorithms, and delivers prioritized alerts to the right stakeholders — so your team can focus on investigation and resolution instead of manual data extraction. The result is not just better detection, but stronger organizational confidence that sensitive processes are continuously protected.

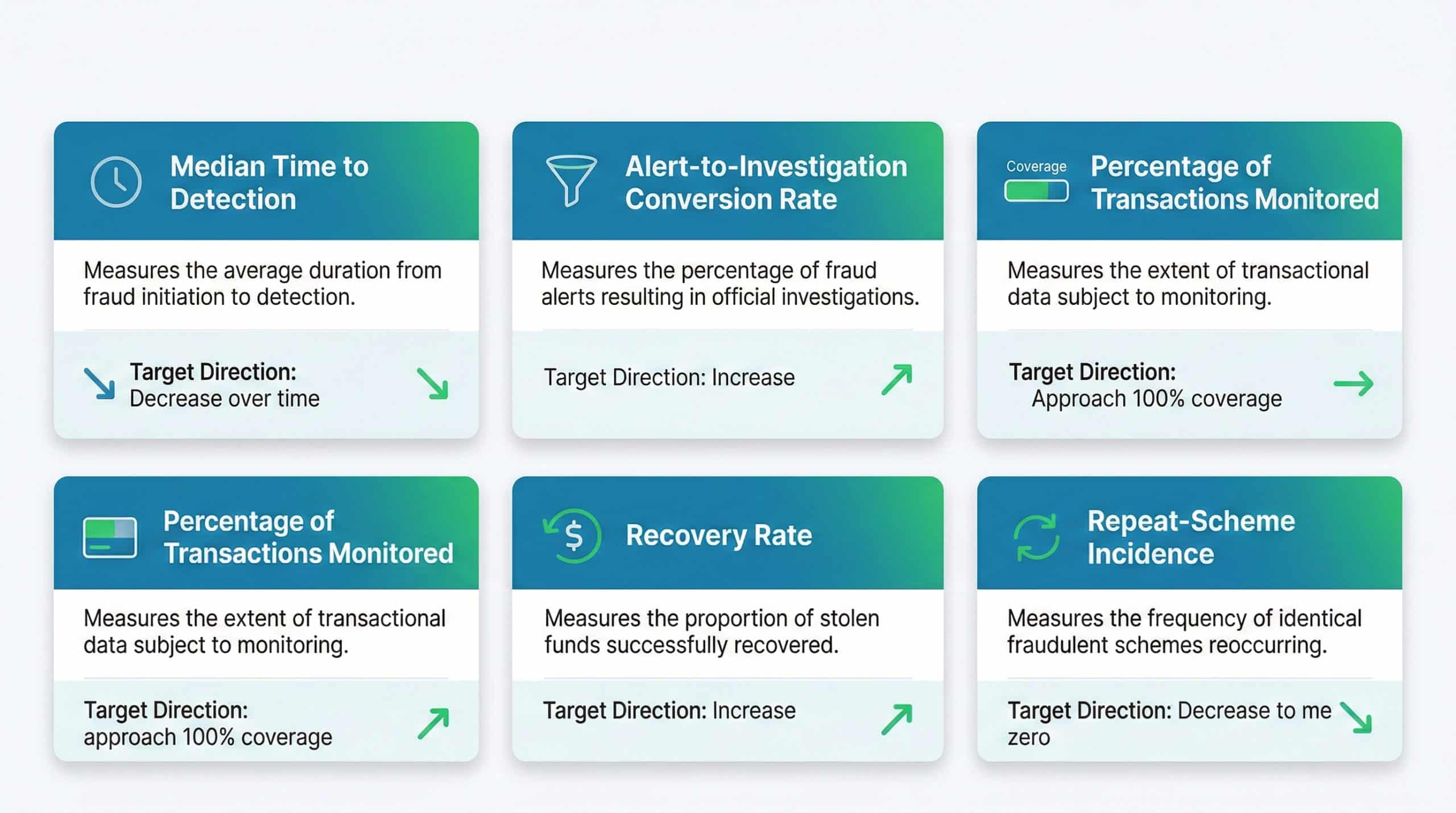

Key Metrics for Measuring Detection Effectiveness

| Metric | What It Tells You | Target Direction |

|---|---|---|

| Median time to detection | How quickly schemes are identified after they begin | Decrease over time |

| Alert-to-investigation conversion rate | Quality of alerts — are they actionable? | Increase (fewer false positives) |

| Percentage of transactions monitored | Coverage breadth — are you scanning everything or just samples? | Approach 100% |

| Recovery rate | How much of the lost amount is recovered post-detection | Increase |

| Repeat-scheme incidence | Whether the same type of fraud recurs after remediation | Decrease to zero |

Tracking these metrics quarterly allows leadership to demonstrate program value, justify continued investment, and identify areas where controls or detection logic need refinement.

Detelix Fraud Detection Solutions

Proactive Monitoring

Continuous, automated scanning of every ERP transaction against hundreds of fraud detection algorithms — catching anomalies before they become losses.

Real-Time Alerts

Instant, prioritized notifications delivered to the right stakeholders when suspicious activity is detected — enabling rapid investigation and response.

Gatekeeper

Pre-payment validation that blocks high-risk transactions before funds leave your organization, adding a critical prevention layer to your detection program.

Experience & Expertise

Decades of fraud investigation experience distilled into detection logic built by practitioners who understand how real-world schemes operate.

See Detelix in Action

Frequently Asked Questions

How long does the average occupational fraud last before detection?

Industry data consistently shows a median duration of twelve to eighteen months. Schemes involving senior executives tend to run longer because their authority allows them to override or bypass controls that would flag lower-level employees. Continuous monitoring dramatically shortens this window by surfacing anomalies as they occur rather than waiting for periodic audits.

Is fraud detection different for small businesses compared to large enterprises?

Yes. Small businesses often lack formal segregation of duties — meaning one person may handle vendor setup, invoice approval, and payment execution. This concentration of authority creates significant opportunity. For smaller organizations, automated detection tools become even more vital because they compensate for the control gaps that larger teams naturally mitigate through role separation.

What is the first step in starting a workplace fraud detection program?

Conduct a comprehensive fraud risk assessment. Map every sensitive process — payroll, vendor payments, expense reimbursements, inventory, bank reconciliations — and identify where opportunity, access, and inadequate oversight intersect. This assessment becomes the blueprint for which detection rules to prioritize and which controls to strengthen first.

Can occupational fraud be completely eliminated?

No control environment can guarantee zero fraud. The realistic goal is to minimize opportunity, maximize the probability of early detection, and create a deterrent effect strong enough that potential fraudsters perceive the risk of getting caught as too high. Organizations that combine strong preventive controls with continuous, real-time detection achieve the lowest loss rates.

How do organizations balance employee privacy with fraud monitoring?

Effective programs focus on transactional data and process compliance rather than personal surveillance. Monitoring whether a payment followed the correct approval path, whether a vendor record was changed before a large transfer, or whether expense claims contain duplicates does not require monitoring personal communications or tracking physical movements. Transparency about what is monitored — communicated through clear policies — builds trust rather than eroding it.

Ready to Close the Detection Gap in Your Organization?

Move from periodic audits to continuous, real-time fraud detection across your most sensitive ERP processes. Speak with the Detelix team to see how layered monitoring protects your bottom line.