Strengthen Your Payment Controls with Detelix

Proactive fraud detection and continuous ERP monitoring — purpose-built for finance teams that refuse to leave payment security to chance.

- What Exactly Is a Payment Fraud Risk Assessment Framework?

- Why Generic Internal Controls Fail to Stop Payment Fraud

- Mapping Failure Points Across the Procure-to-Pay Cycle

- A Closer Look at Accounts Payable Fraud Risk

- How Do You Build a Risk Register Specifically for Payment Fraud?

- Scoring Payment Risks Without Falling Into Subjectivity

- What Should a Finance Risk Scoring Model Include at Transaction Level?

- Evaluating Whether Your Existing Controls Actually Work

- Why Segregation of Duties Deserves Special Attention in Payments

- The Highest-Risk Event: When a Vendor’s Bank Details Change

- What Does Payment Controls Maturity Really Mean?

- A Four-Level Maturity Model for Payment Controls

- When Is the Right Time to Move from Manual to Automated Risk Assessment?

- What Mistakes Do Organizations Make When Building a Payment Fraud Framework?

- Which Reports and Alerts Matter Most for Ongoing Risk Management?

- How Often Should a Payment Fraud Risk Assessment Be Refreshed?

- Connecting the Framework to Real-Time Protection

- Frequently Asked Questions

In many organizations, payment controls appear robust at first glance. Approval hierarchies exist inside the ERP, invoices go through matching routines, and bank reconciliations run on schedule. Yet payment fraud continues to inflict significant financial damage on businesses of every size. The gap between perceived control and actual control is where risk thrives — and closing that gap requires more than policies on paper. It demands a structured, measurable, and continuously operating payment fraud risk assessment framework that translates known vulnerabilities into prioritized actions, real-time detection, and verifiable prevention.

Key Takeaways

- A payment fraud risk assessment framework is a living system — not a one-time audit checklist — that maps threats across the entire procure-to-pay cycle and produces risk-ranked action plans.

- Generic ERP controls and approval workflows are designed for normal operations, not adversarial behavior; a structured framework exposes the gaps between individual controls that fraudsters exploit.

- Vendor bank account modifications represent the single highest-risk event in the payment cycle and require independent, multi-step verification before any payment is released.

- A four-level maturity model helps organizations objectively measure their control capability and identify when manual processes have reached their ceiling.

- Continuous, real-time monitoring — rather than periodic audits — is the decisive shift that moves finance teams from post-event investigation to pre-event fraud prevention.

What Exactly Is a Payment Fraud Risk Assessment Framework?

A payment fraud risk assessment framework is a dynamic methodology that defines how an organization identifies, measures, prioritizes, and mitigates fraud risks across the entire disbursement cycle. Unlike a one-time internal audit checklist, it operates as a living system. It maps every stage of the procure-to-pay (P2P) process, attaches specific threat scenarios to each stage, evaluates the likelihood and impact of those threats, tests the effectiveness of existing controls, and produces a risk-ranked action plan that evolves as the business environment changes.

The framework is not an abstract governance exercise. It connects directly to operational decisions: which payments require additional approval, which vendor changes trigger verification, which invoice patterns demand investigation, and which process gaps justify investment in payment risk assessment software. When designed correctly, it moves the finance function from reactive investigation to proactive prevention.

Tip

Start by documenting every payment-related process your team performs — including informal workarounds. Frameworks built on official procedures alone miss the ad hoc shortcuts where fraud risk concentrates.

Why Generic Internal Controls Fail to Stop Payment Fraud

Many finance teams rely on a combination of ERP permissions, approval workflows, and periodic audits to manage payment risk. These controls address a portion of the threat landscape, but they share a critical weakness: they are designed for normal operations, not adversarial behavior. A fraudster — whether internal or external — studies the control environment and finds the seams between processes, teams, and systems.

For example, an approval workflow may require two signatories for payments above a threshold. But if a bad actor splits invoices to stay below that threshold, the control never activates. Similarly, ERP user permissions may restrict who can create a vendor record, yet a single employee with both “modify vendor bank details” and “release payment” rights can redirect funds without triggering any alert. A framework forces the organization to think beyond individual controls and evaluate how controls interact, where gaps exist between them, and how adversaries exploit those gaps.

Did You Know

Invoice splitting — deliberately breaking a single purchase into multiple invoices that each fall below the approval threshold — is one of the most common fraud techniques and remains undetectable by approval workflows that evaluate each invoice in isolation.

Mapping Failure Points Across the Procure-to-Pay Cycle

The first operational step in building a framework is mapping the P2P cycle into discrete risk zones. Each zone represents a cluster of activities where fraud can enter or be facilitated. A practical mapping typically includes five zones: vendor onboarding, vendor master data maintenance, invoice receipt and matching, approval and authorization, and payment execution.

Common Fraud Scenarios by Zone

At vendor onboarding, the primary risk is the creation of fictitious vendors — entities that exist only to receive payments. During vendor master data maintenance, the danger shifts to unauthorized changes in banking details, a technique frequently exploited in Business Email Compromise (BEC) attacks. As reported by Israeli media, BEC schemes impersonating senior executives have become one of the most financially damaging fraud types, often targeting the moment when payment instructions are modified. At the invoice stage, duplicate invoices, rounded-amount invoices, and invoices with sequential numbering anomalies represent key red flags. In the approval zone, threshold manipulation, emergency overrides without documentation, and single-point-of-failure authorizations create exploitable weaknesses. Finally, at payment execution, the absence of a final cross-check between approved payment details and current vendor master data is the last missed opportunity to prevent loss.

Tip

Map your P2P risk zones visually using a process flowchart and tag each zone with its top three threat scenarios. This creates a shared reference that both finance and IT teams can use during framework reviews.

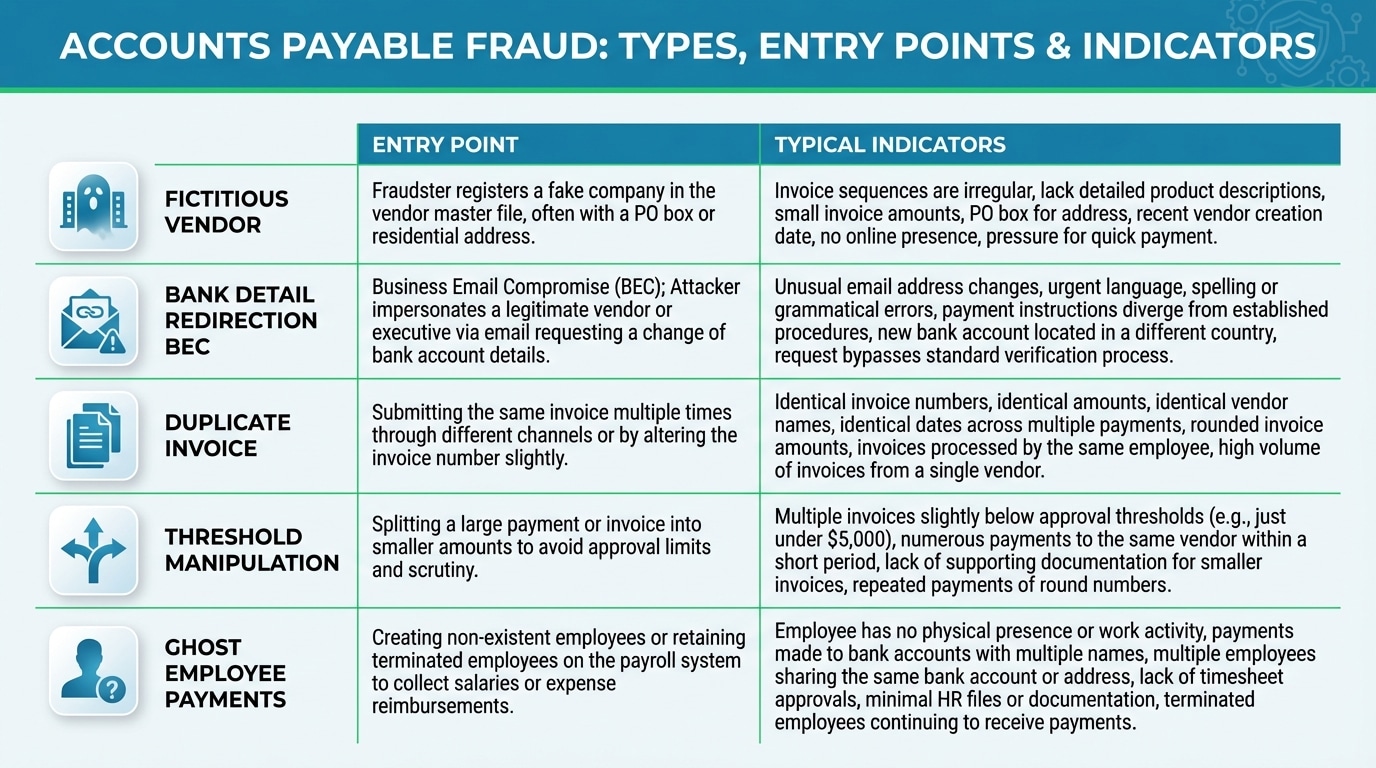

A Closer Look at Accounts Payable Fraud Risk

Accounts payable fraud risk refers to the exposure an organization faces when payments are made based on falsified, manipulated, or erroneous information — or when legitimate processes are deliberately bypassed to divert funds. The scope is broader than most finance leaders initially assume. It includes external threats such as vendor impersonation and invoice fraud, internal threats such as collusion between employees and suppliers, and hybrid threats where external attackers compromise an insider’s credentials or email to alter payment flows.

| Fraud Type | Entry Point | Typical Indicator |

|---|---|---|

| Fictitious vendor | Vendor onboarding | Vendor address matches employee address; no purchase order history |

| Bank detail redirection (BEC) | Vendor master change | Bank account change request via email close to payment run |

| Duplicate invoice | Invoice receipt | Same amount, close dates, similar invoice numbers from same vendor |

| Threshold manipulation | Approval | Multiple invoices just below approval limit from a single vendor |

| Ghost employee payments | Payroll/AP crossover | Payments to bank accounts shared across vendor and payroll records |

Understanding these risk categories is essential because the framework must assign specific detection rules, control requirements, and escalation procedures to each one. A generic “review all large payments” approach will always miss the patterns that fall outside its narrow scope.

Did You Know

Ghost employee payments — where funds are disbursed to fictitious payroll entries — are often detected only when bank account numbers are cross-referenced between the vendor master file and payroll records. Without automated cross-checking, these schemes can persist for years.

How Do You Build a Risk Register Specifically for Payment Fraud?

A risk register transforms abstract risk awareness into a structured, auditable document. For payment fraud, each entry in the register should describe a specific threat scenario — not a vague category. Instead of recording “vendor fraud,” the register should capture “creation of a vendor record with banking details matching an existing employee’s personal account, followed by invoice submission and payment within the same accounting period.”

Each scenario needs five fields: the enabling condition (such as excessive user permissions), the data signal that could reveal it (such as a shared bank account across vendor and employee records), the existing control that should prevent or detect it, the residual risk after that control is applied, and the owner responsible for monitoring and responding. This level of specificity is what separates a functional framework from a compliance document that sits in a drawer.

Tip

When populating your risk register, interview AP clerks and procurement staff individually — not in group settings. People are far more candid about workarounds and control gaps in one-on-one conversations than in workshops where management is present.

Scoring Payment Risks Without Falling Into Subjectivity

Risk scoring is the mechanism that converts identified threats into a prioritized action list. The challenge is ensuring the scoring process reflects reality rather than the biases of the people in the room. A common pitfall in fraud risk workshops is that participants either inflate risks they personally experienced or minimize risks they have not yet encountered.

To counter this, the framework should anchor scoring to quantitative data wherever possible. Transaction logs, exception reports, override frequencies, vendor aging data, and historical incident records all provide objective inputs. The scoring model then combines a likelihood rating (based on frequency of enabling conditions and historical occurrence) with an impact rating (based on potential financial loss, regulatory exposure, and reputational damage). Each rating uses a defined scale — typically 1 to 5 — with explicit criteria for each level.

Sample Likelihood x Impact Matrix

| Likelihood / Impact | Negligible (1) | Low (2) | Moderate (3) | High (4) | Critical (5) |

|---|---|---|---|---|---|

| Rare (1) | 1 | 2 | 3 | 4 | 5 |

| Unlikely (2) | 2 | 4 | 6 | 8 | 10 |

| Possible (3) | 3 | 6 | 9 | 12 | 15 |

| Likely (4) | 4 | 8 | 12 | 16 | 20 |

| Almost Certain (5) | 5 | 10 | 15 | 20 | 25 |

Scenarios scoring above a predefined threshold — for instance, 12 or higher — automatically enter an active remediation cycle with defined timelines and accountability. This prevents the common organizational habit of acknowledging risk but deferring action indefinitely.

Did You Know

Organizations that anchor their risk scoring to actual transaction data — rather than relying solely on workshop estimates — reduce scoring bias by an average of 40% and produce action plans that are significantly more aligned with real operational exposure.

What Should a Finance Risk Scoring Model Include at Transaction Level?

While the risk register evaluates scenarios at a strategic level, a finance risk scoring model operates at the transaction level. It assigns a numerical risk score to every payment request, vendor change, or invoice submission as it enters the system. The score determines what happens next: automatic processing, flagged review, mandatory secondary approval, or hard stop.

Effective models draw on multiple variable categories. Vendor-level variables include the vendor’s age in the system, country of registration, frequency of banking detail changes, and whether the vendor has ever been flagged in prior reviews. Transaction-level variables include invoice amount relative to historical averages, rounding patterns, proximity to approval thresholds, payment urgency flags, and whether the invoice was manually entered rather than received through an automated channel. Behavioral variables capture patterns such as a sudden spike in invoice volume from a dormant vendor or a change request arriving just before a scheduled payment run.

The critical design decision is setting thresholds. A score between 0 and 40 might allow straight-through processing. A score between 41 and 70 could trigger a review queue with a 24-hour resolution window. A score above 70 might block the payment entirely until an independent verification is completed. These thresholds must be calibrated to the organization’s risk appetite and adjusted periodically based on false-positive rates and emerging threat patterns.

Your payment controls are only as strong as the risks they actually detect. Let Detelix show you where your gaps are — before a fraudster finds them first.

Evaluating Whether Your Existing Controls Actually Work

A framework is only as strong as its weakest control — and many organizations discover that controls they believed were operating effectively have quietly degraded. The distinction between design effectiveness and operating effectiveness is essential. A control is well-designed if its logic correctly addresses the risk it targets. A control is operationally effective if it consistently performs as designed across all relevant transactions without exception.

Consider a three-way match requirement: purchase order, goods receipt, and invoice must align before payment is authorized. The design is sound. But if the AP team routinely overrides mismatches to meet payment deadlines — and those overrides are not logged or reviewed — the control’s operating effectiveness is near zero. The framework must therefore include periodic testing: sampling overrides, measuring exception rates, reviewing approval logs, and comparing intended control behavior against actual system data. According to audit reports on government payment processes, the failure to verify invoice details before payment execution is a recurring finding, reinforcing the importance of testing controls in practice rather than relying on their existence in policy documents.

Tip

Pull a monthly report of all three-way match overrides and review them for patterns. If the same approver, vendor, or invoice type appears repeatedly, you have found a control gap that needs immediate remediation.

Why Segregation of Duties Deserves Special Attention in Payments

Segregation of duties (SoD) is the single most important structural control in the payment cycle. When one individual can create a vendor, modify banking details, approve an invoice, and release a payment, the entire control environment collapses into a single point of failure. SoD ensures that no single person controls an entire transaction from initiation to completion.

Testing SoD requires more than reviewing an organizational chart. It demands an analysis of actual ERP role assignments and transaction logs. The questions are specific: Can user X both create and approve purchase orders? Can user Y both modify vendor bank accounts and execute payment runs? Can user Z both post invoices and perform bank reconciliations? Findings from state audit reports on corporate governance consistently highlight that inadequate role separation in financial processes enables both undetected errors and deliberate manipulation. Where full segregation is impossible — often in smaller teams — compensating controls such as mandatory log reviews, dual authorization for sensitive changes, and independent reconciliation become non-negotiable.

Did You Know

ERP systems often accumulate role conflicts over time as employees change positions but retain their previous access privileges. A quarterly SoD conflict scan across all active user roles frequently reveals conflicts that no one in the organization was aware of.

The Highest-Risk Event: When a Vendor’s Bank Details Change

If a framework had to prioritize a single scenario above all others, vendor bank account modification would be the clear choice. This is the precise mechanism through which BEC attacks, vendor impersonation schemes, and internal redirection frauds are executed. The attacker does not need to hack a system; they need only convince someone — or exploit a process gap — to change a few digits in a bank account field. Once the next legitimate payment runs, the funds transfer to the attacker’s account.

Robust frameworks treat every bank detail change as a high-risk event requiring independent, multi-step verification. This means confirming the change through a known contact at the vendor — using contact information already on file, not the details provided in the change request itself. It means requiring documented approval from a second authorized individual. It means implementing a “cooling period” during which no payment is released to the new account. And it means automated alerts that flag any payment directed to recently changed banking details. Platforms like Detelix enable organizations to enforce these verification layers in real time, ensuring that no bank detail change slips through to payment execution without proper scrutiny — a critical advantage when manual processes are prone to time pressure and human oversight gaps.

Tip

Implement a mandatory 48-hour cooling period between any vendor bank detail modification and the next payment release to that vendor. This single control dramatically reduces the success rate of BEC-based payment redirection attacks.

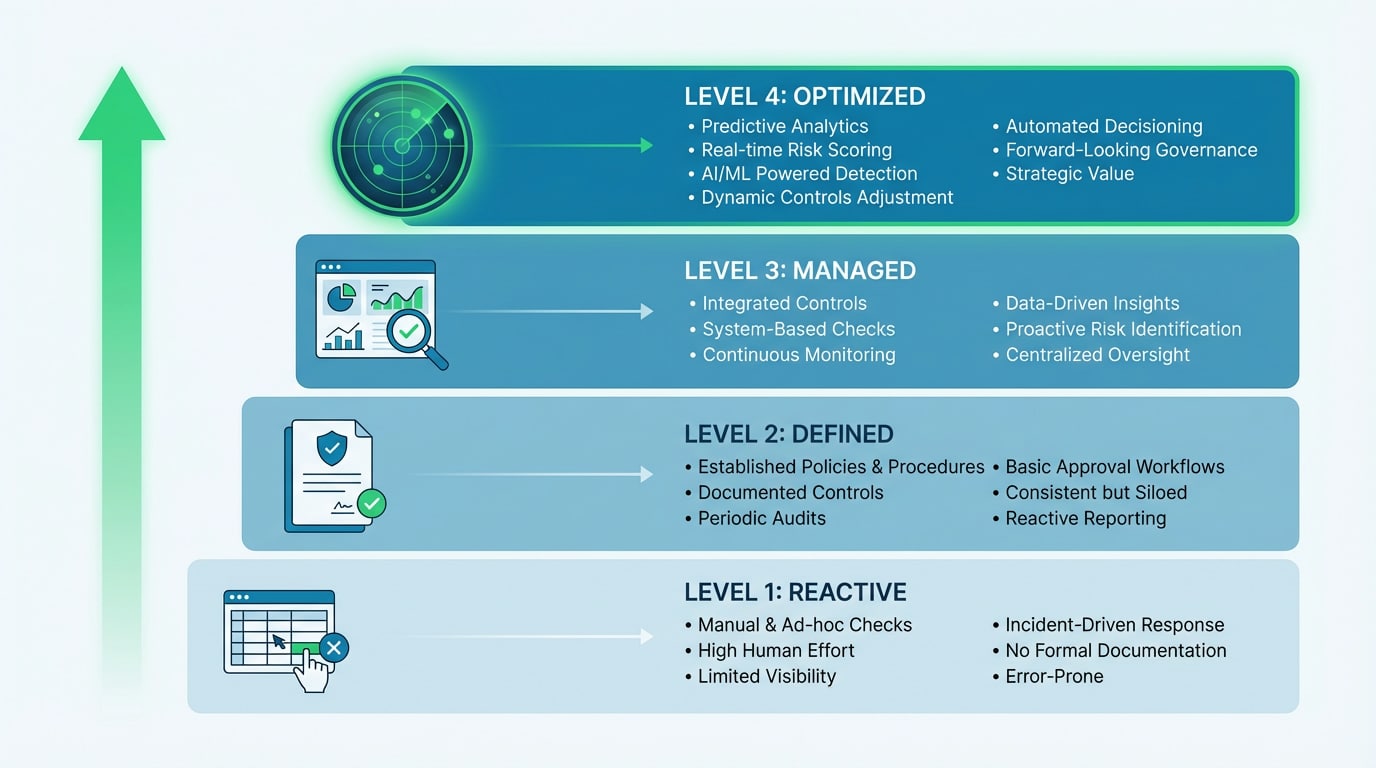

What Does Payment Controls Maturity Really Mean?

Payment controls maturity measures not whether controls exist, but how reliably, consistently, and intelligently they operate. Two organizations may both have “duplicate invoice detection” — but one relies on a manual spreadsheet review while the other runs automated cross-referencing across all vendor IDs, invoice numbers, amounts, and dates in real time. The control is nominally the same; the maturity level is entirely different.

Maturity assessment matters because it reveals the gap between the organization’s current capability and the capability required to manage its actual risk exposure. A high-volume AP department processing thousands of invoices monthly cannot sustain a Level 1 (reactive, manual) control environment without accumulating undetected losses over time. Understanding your current maturity level is the prerequisite for building a realistic improvement roadmap.

A Four-Level Maturity Model for Payment Controls

| Maturity Level | Characteristics | Vendor Management | Invoice/Payment Controls | Monitoring |

|---|---|---|---|---|

| Level 1 — Reactive | Ad hoc, manual, spreadsheet-dependent | No formal onboarding; changes untracked | Basic approval workflow; no duplicate check | Post-incident investigation only |

| Level 2 — Defined | Written policies; inconsistent enforcement | Onboarding form exists; bank changes require email approval | Three-way match in ERP; overrides not reviewed | Quarterly audit sampling |

| Level 3 — Managed | Automated screening; exception queues; KPIs tracked | Automated duplicate vendor check; bank change triggers review queue | Duplicate detection; tolerance-based matching; override logging | Monthly exception reports; trend analysis |

| Level 4 — Optimized | Real-time risk scoring; continuous monitoring; data-driven adaptation | Risk-scored vendor changes; independent verification enforced | Real-time scoring per transaction; hard stops on high-risk items | Continuous alerts; anomaly detection; automated escalation |

Most organizations find themselves between Level 2 and Level 3. The transition to Level 4 typically requires dedicated payment risk assessment software that integrates with the ERP to monitor transactions as they occur, rather than after they have been completed.

Did You Know

Organizations operating at Maturity Level 4 detect payment anomalies an average of 15 times faster than those at Level 2 — and recover a significantly higher percentage of misdirected funds because early detection preserves the window for bank reversal.

When Is the Right Time to Move from Manual Controls to Automated Risk Assessment?

The honest answer is: earlier than most organizations think. The trigger is not a single dramatic fraud event — it is the accumulation of conditions that make manual control unsustainable. When the volume of transactions exceeds what a team can meaningfully review. When the number of vendors grows beyond what relationship-based verification can cover. When override rates climb because controls slow down legitimate operations. When audit findings repeat year after year without resolution. Any of these conditions signals that manual processes have reached their ceiling.

Detelix addresses this transition by functioning as an independent control layer over ERP processes. Rather than replacing existing workflows, it continuously cross-checks transactions, vendor data changes, approval patterns, and payment executions against configurable risk rules. The result is that the finance team receives actionable alerts on genuine anomalies instead of drowning in false positives or missing real threats buried in transaction volume. This is the practical difference between managing activity and actually controlling it.

Tip

Track your AP team’s override rate monthly. If overrides exceed 10% of matched invoices, your controls are creating friction without protection — a clear signal that automated, risk-scored processing would deliver both faster throughput and stronger security.

What Mistakes Do Organizations Make When Building a Payment Fraud Framework?

The most frequent mistake is treating the framework as a one-time project with a completion date. Fraud tactics evolve, business processes change, new vendors are onboarded, and employee roles shift. A framework that was accurate twelve months ago may have significant blind spots today. The second common error is over-indexing on external threats while ignoring internal risk. Employee collusion, policy workarounds, and unauthorized process shortcuts account for a substantial share of payment losses. Third, many organizations build frameworks that generate impressive documentation but lack operational teeth — no one is assigned to act on the findings, exception queues are not monitored, and risk scores are not connected to approval workflows.

Did You Know

According to multiple occupational fraud studies, the median duration of an internal fraud scheme is 12 months before detection. Frameworks that are reviewed only annually effectively guarantee that any active scheme has at least a full year to operate undetected.

Which Reports and Alerts Matter Most for Ongoing Risk Management?

A framework without operational reporting is a framework that exists only in theory. The reports that drive real control are those that surface actionable exceptions in time for intervention. Key reports include: vendor master changes in the last 30 days (with focus on banking details), payments directed to recently modified accounts, invoices that triggered override or manual match, transactions scoring above the risk threshold that were approved without documented justification, and SoD conflict activity logs showing users who executed conflicting roles within the same period.

Alerts should be tiered by severity. A low-severity alert might notify a team lead of a pattern worth monitoring. A high-severity alert should immediately halt the payment process and require explicit clearance before proceeding. Detelix’s approach to alert management ensures that severity levels are calibrated to the organization’s specific risk profile, reducing alert fatigue while maintaining vigilance over genuinely high-risk events.

How Often Should a Payment Fraud Risk Assessment Be Refreshed?

The framework’s risk register and scoring model should be formally reviewed at least annually — but specific components require more frequent attention. Vendor risk scores should update dynamically as new data becomes available (a vendor that changed bank details twice in six months presents a different risk profile than one with stable records over five years). Control effectiveness testing should occur quarterly at minimum. Threshold calibration should be revisited whenever the organization experiences a material change: a merger, a new ERP module rollout, a significant increase in vendor count, or an identified incident. The principle is straightforward — the assessment frequency should match the pace at which the risk environment changes.

Tip

Set calendar reminders for quarterly control testing and tie annual framework reviews to your fiscal year-end close process. Embedding the review cycle into existing financial workflows ensures it happens consistently rather than being postponed indefinitely.

Connecting the Framework to Real-Time Protection

The ultimate goal of a payment fraud risk assessment framework is not to produce a document — it is to produce a state of continuous, verifiable control. Every element discussed above — risk mapping, scoring models, control testing, SoD enforcement, exception management — reaches its full potential only when embedded into the organization’s daily operational rhythm. This is where the distinction between periodic assessment and continuous monitoring becomes decisive.

A well-implemented framework, supported by technology that monitors ERP processes in real time, transforms the finance function’s relationship with risk. Instead of discovering a duplicate payment during a quarterly reconciliation, the team catches it before execution. Instead of learning about a redirected vendor payment weeks after the funds left the account, an alert fires the moment the bank detail change deviates from expected patterns. This shift — from post-event investigation to pre-event intervention — is what separates organizations that manage fraud from organizations that prevent it.

Detelix Payment Fraud Prevention Solutions

Proactive Monitoring

Continuous surveillance of ERP transactions and vendor data changes to identify fraud patterns before payments are executed.

Real-Time Alerts

Tiered, severity-based alerts that escalate genuine anomalies to the right stakeholders — reducing noise and accelerating response.

GateKeeper

Automated verification of vendor bank detail changes with independent confirmation workflows and cooling period enforcement.

Experience & Expertise

Decades of combined expertise in financial controls, ERP security, and fraud investigation — backing every solution we deploy.

See Detelix in Action

Frequently Asked Questions

What is the difference between a fraud risk assessment and an internal controls assessment?

A fraud risk assessment focuses specifically on identifying how fraud could occur, who could perpetrate it, and which controls are designed to prevent or detect it. An internal controls assessment has a broader scope that includes financial reporting accuracy, regulatory compliance, and operational efficiency. The fraud-specific lens forces a more adversarial perspective — asking not just “does the control exist?” but “how could someone bypass it?”

Can automation actually reduce payment fraud, or does it just shift the risk?

Automation reduces fraud when it is layered on top of well-designed controls. It eliminates manual errors, enforces consistent rule application across every transaction, and detects patterns invisible to human reviewers at scale. The risk shifts only if automation is implemented without proper configuration, threshold management, and ongoing calibration — which is why the framework must govern the technology, not the other way around.

Is segregation of duties enough to prevent accounts payable fraud?

SoD is necessary but not sufficient. It prevents one individual from controlling an entire process, but it does not prevent collusion between two authorized individuals, nor does it detect anomalies within transactions that each participant processes in good faith. SoD must be combined with transaction-level monitoring, exception reporting, and independent verification procedures to form a complete defense.

How do you handle payment fraud risk in smaller organizations with limited staff?

Smaller teams often cannot achieve full role separation. In these environments, compensating controls become critical: mandatory dual authorization for high-risk actions, independent log reviews by a senior leader, automated alerts for sensitive changes, and periodic external review. Technology plays an especially important role here because it provides the monitoring layer that a small team cannot sustain manually.

What should you look for in payment risk assessment software?

Key capabilities include real-time integration with the ERP, configurable risk scoring rules, automated detection of duplicate invoices and vendor anomalies, SoD conflict monitoring, tiered alerting with escalation workflows, and comprehensive audit trails. The software should function as an independent layer — not dependent on the same permissions and processes it is designed to monitor.

Ready to Close the Gaps in Your Payment Controls?

Your framework is only as strong as the technology enforcing it. Discover how Detelix continuous ERP monitoring turns your risk assessment into real-time fraud prevention.