Strengthen Your Accounts Receivable Controls with Detelix

Detect AR fraud schemes, eliminate reconciliation gaps, and protect your cash flow with real-time monitoring built for your ERP.

- What Are AR Fraud and Error Controls and Why Are They Critical?

- Fraud vs. Error in the AR Process

- Common AR Fraud Schemes to Monitor

- How Segregation of Duties Reduces AR Risk

- Controls at the Invoicing Stage

- Cash Application Controls

- When a Small Credit Memo Hides a Large Problem

- Credit Memo Fraud Detection

- Preventive vs. Detective Controls Comparison

- Key Performance Indicators for AR Risk Monitoring

- Common Mistakes That Undermine AR Controls

- Does Automation Eliminate or Shift AR Risk?

- Access Controls and Audit Trails

- Building a 90-Day Roadmap for AR Control Excellence

- Choosing an AR Risk Monitoring Solution

- Frequently Asked Questions

In many organizations, the accounts receivable process appears well-managed on the surface. Invoices go out, payments come in, and the ledger closes each month. But underneath that routine, a complex web of manual entries, adjustments, credits, and write-offs creates fertile ground for both unintentional errors and deliberate fraud. When a single misapplied payment can cascade into distorted aging reports, unnecessary collection calls, and hidden cash shortfalls, the need for rigorous accounts receivable fraud and error controls becomes a direct threat to organizational cash flow, profitability, and trust. This guide provides a practical, control-focused approach to understanding, detecting, and preventing the risks embedded in your AR process.

Key Takeaways

- AR fraud and errors produce identical symptoms — effective controls must address both dimensions simultaneously through preventive and detective measures.

- Segregation of duties remains the single most effective structural barrier against AR manipulation, forcing fraud to require collusion rather than solo action.

- Credit memos and write-offs are the highest-risk instruments in AR because they reduce balances without requiring cash inflow, making them preferred concealment tools.

- Daily reconciliation of bank deposits against AR postings is a non-negotiable control — monthly reconciliation leaves a 30-day window for fraud schemes to compound.

- Automation reduces manual errors but introduces systemic risk if matching rules and exception thresholds are not governed through formal change management.

- A focused 90-day improvement plan covering visibility, hardening, and monitoring can deliver measurable results without requiring a multi-year transformation.

What Are Accounts Receivable Fraud and Error Controls and Why Are They Critical for Cash Flow?

Accounts receivable fraud and error controls are the systematic framework of policies, automated monitoring, role-based permissions, and manual verification procedures designed to safeguard every stage of the AR lifecycle — from invoice creation through cash application, credit adjustments, write-offs, and reconciliation. Their purpose is straightforward: ensure that money owed to the organization actually arrives, is recorded accurately, and is reflected truthfully in financial statements.

AR is the primary engine of cash inflow for most businesses. Yet it is also one of the most vulnerable areas for manipulation. High transaction volumes, frequent manual entries, and multiple touchpoints between billing, treasury, and collections create opportunities where errors go unnoticed and fraud can be concealed for months. Distorted DSO figures, unreliable aging reports, and unexpected write-offs are often symptoms of control gaps that could have been caught earlier. The COSO Internal Control — Integrated Framework identifies “Control Environment” and “Risk Assessment” as foundational components; without these in place for AR specifically, receivables anomaly detection and AR risk monitoring become guesswork rather than discipline.

Tip

Start by mapping every manual touchpoint in your AR process end-to-end. Each point where a human can override, adjust, or reclassify a transaction is a potential control gap that deserves a documented preventive or detective control.

What Is the Difference Between Fraud and Error in the AR Process?

The distinction matters because it shapes your response. An error is an unintentional operational failure — a payment keyed to the wrong customer account, an invoice generated with an incorrect price, or a deposit recorded on the wrong date. Fraud, by contrast, is a deliberate act of deception: diverting a customer payment into a personal account, issuing a fictitious credit memo to mask a stolen payment, or writing off a legitimate balance to hide embezzlement.

What makes AR controls especially challenging is that both fraud and error can produce identical symptoms. A spike in unapplied cash, for example, might indicate sloppy data entry or an active lapping scheme. According to ISA 240, auditors are required to maintain professional skepticism precisely because the boundary between innocent mistakes and intentional misstatement is often invisible without proper investigation. Effective accounts receivable fraud and error controls must therefore address both dimensions simultaneously — reducing the likelihood of human mistakes while making deliberate manipulation significantly harder to execute and conceal.

Did You Know

According to the ACFE, asset misappropriation — which includes AR fraud schemes like lapping and skimming — accounts for the vast majority of occupational fraud cases, yet it often goes undetected for over a year because the individual losses appear small enough to stay below review thresholds.

Which Types of Accounts Receivable Fraud Schemes Should Organizations Monitor?

Understanding the mechanics of common fraud schemes is the first step toward building targeted controls. The ACFE Fraud Tree classifies these under “Asset Misappropriation,” and within the AR domain, four patterns dominate.

Lapping — How It Works and What the Signs Are

Lapping occurs when an employee who handles incoming payments steals Customer A’s payment and then covers the shortfall by applying Customer B’s subsequent payment to Customer A’s account. The cycle continues, creating a rolling trail of misapplied receipts. Red flags include persistent timing gaps between the date a check is received and the date it is posted, repeated “corrections” to specific customer accounts, and customer complaints about receiving collection notices despite having paid on time.

Skimming and Diversion — Where It Happens in the Process

Skimming involves intercepting cash or check payments before they are recorded in the accounting system. Payment diversion routes electronic payments to unauthorized bank accounts, often by modifying remittance instructions. Both are difficult to detect without independent verification of deposits against bank statements and lockbox reports.

Tip

Implement a lockbox arrangement with your bank where customer payments are directed to a bank-controlled P.O. box. This removes the opportunity for employees to physically handle checks before they are deposited and recorded, eliminating the primary vector for skimming.

Credit Memo Abuse — Using Credits to Hide Shortfalls

An employee issues unauthorized credit memos to reduce a customer’s balance after diverting the actual payment. Because credits do not require incoming cash, they create a “zero-sum” cover that is invisible to standard aging reports. Round-dollar credits, credits issued just below approval thresholds, and credits without linked return documentation are classic warning signs.

Write-off Abuse — Erasing the Evidence

Rather than issuing a credit, the fraudster simply writes off the outstanding balance, declaring it uncollectible. When write-off authority is loosely controlled and no evidence of collection effort is required, this becomes a convenient way to eliminate the trail of a diverted payment.

Did You Know

The median duration of a billing or AR fraud scheme before detection is 24 months, according to ACFE research. Organizations that deploy proactive data analytics cut that detection time by more than half compared to those relying on tips or manual audits alone.

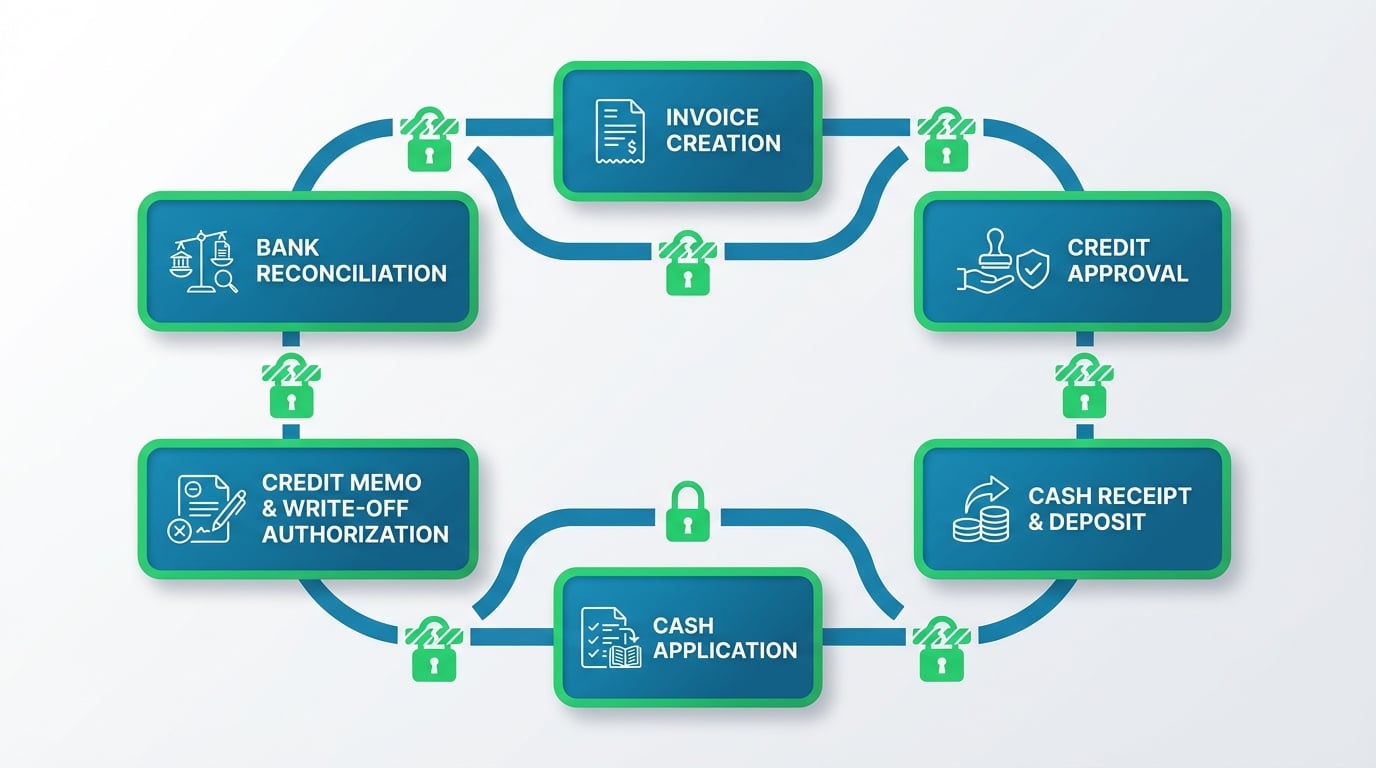

How Does Segregation of Duties Reduce AR Risk?

Segregation of duties is the structural backbone of accounts receivable fraud and error controls. The principle is simple: no single individual should control an entire transaction from start to finish. When one person creates invoices, receives payments, applies cash, authorizes credits, and reconciles accounts, the opportunity for both error and fraud multiplies dramatically — and the chance of detection drops to near zero.

Practical SoD in AR means separating at least these functions: invoice creation, credit approval, cash receipt and deposit, cash application, credit memo and write-off authorization, and bank reconciliation. In smaller teams where full separation is not feasible, compensating controls such as mandatory supervisory review, dual-signature requirements on adjustments above a threshold, and independent reconciliation by someone outside the AR team become essential. Organizations that use real-time monitoring platforms like Detelix gain an additional layer of visibility — the system continuously cross-checks user actions against defined SoD policies and flags violations as they occur, rather than waiting for a quarterly audit.

Tip

Conduct a quarterly ERP access review specifically for AR-related roles. Employee responsibilities shift over time, and accumulated permissions from prior roles create SoD conflicts that are invisible until someone actively looks for them.

What Controls Strengthen the Invoicing Stage Against Errors and Manipulation?

The invoicing stage is where the AR lifecycle begins, and a weak start compounds downstream. Strong invoicing controls include sequential invoice numbering with gap detection, automated price validation against approved price lists, mandatory documentation for discounts or special terms, and a clear period cut-off policy that prevents backdating or forward-dating invoices to manipulate revenue recognition.

Cancellation or modification of an issued invoice should require a documented reason and approval from someone other than the invoice creator. Without these controls, fictitious invoices can be generated to inflate revenue, or legitimate invoices can be suppressed or altered to benefit specific customers — both of which distort AR balances and cash flow forecasts.

Did You Know

Invoice sequence gap analysis is one of the simplest yet most overlooked detective controls. A missing invoice number in a sequential series may indicate a voided document that was never properly authorized — or an invoice that was deliberately suppressed to conceal fraudulent activity.

How Do Cash Application Controls Prevent Unapplied Cash and Misapplication?

Cash application is the process of matching incoming payments to outstanding invoices — the critical bridge between bank activity and the AR sub-ledger. When this bridge is weak, the consequences are tangible: inflated unapplied cash balances, phantom aging entries, unnecessary collection activity, and an environment where lapping schemes can thrive undetected.

Controls on Manual Postings and Who Approves Them

Every manual cash application entry should require a documented reason and a second-level approval. High volumes of manual postings by a single user are a red flag that warrants immediate investigation. Automated matching rules should handle the majority of transactions, with manual intervention reserved for genuine exceptions.

Controls on Partial Application and Payments Without Reference

Partial payments and remittances that arrive without clear invoice references create ambiguity. Controls should include a defined SLA for resolving partial applications, mandatory tagging of the reason for any short-pay, and escalation protocols for payments that remain unapplied beyond a set number of days.

Confirming that AR balances are accurate through independent verification is a well-established auditing practice. PCAOB AS 2310 emphasizes the auditor’s responsibility to maintain control over the confirmation process and evaluate exceptions — a principle that finance teams should mirror internally through regular reconciliation of bank and lockbox data against posted AR entries.

Concerned about hidden gaps in your AR controls? Our team specializes in real-time receivables monitoring that catches anomalies before they become material losses.

A Scenario: When a Small Credit Memo Hides a Large Problem

Consider this situation. A collections specialist processes 200 payments per day. Over several months, the specialist begins diverting small customer checks — each under the threshold that triggers a supervisory review. To balance the affected accounts, the specialist issues credit memos citing “pricing adjustment” or “customer goodwill.” Each credit is small enough to avoid the approval matrix. After 18 months, the cumulative loss exceeds the equivalent of an entire quarter’s write-off budget, yet no single transaction ever triggered an alert.

This scenario illustrates why credit memo fraud detection cannot rely solely on threshold-based approvals. It requires pattern analysis: How many credits has this user issued this month compared to peers? Are the same reason codes being used repeatedly? Are credits concentrated on specific customer accounts? This is the domain of receivables anomaly detection — and it is precisely where platforms designed for continuous ERP monitoring, such as Detelix, provide value by correlating user behavior, transaction patterns, and timing across the entire AR sub-ledger in real time.

Tip

Set up a peer-comparison report that benchmarks each AR clerk’s credit memo volume, average credit amount, and most-used reason codes against team averages. A user who consistently issues 3x more credits than peers — even if each individual credit is below the approval threshold — should be flagged for a detailed review.

What Is Credit Memo Fraud Detection and How to Control Adjustments Effectively?

Credit memos are inherently high-risk instruments. They reduce the amount a customer owes without any corresponding cash inflow, making them the preferred concealment tool for AR fraud schemes. A robust credit memo fraud detection framework includes three pillars: documentation requirements, approval governance, and analytical monitoring.

Every credit memo should be linked to a specific original invoice and accompanied by supporting evidence — a signed return authorization, a documented pricing dispute resolution, or a service failure report. The approval matrix should escalate based on both the dollar amount and the frequency of credits issued to the same customer or by the same user. Analytically, finance teams should track round-dollar credits, credits issued just below approval thresholds, credits processed outside business hours, and any credit that closes out an account balance entirely without a corresponding payment.

Comparing Preventive and Detective Controls Across the AR Lifecycle

| AR Process Stage | Preventive Control Examples | Detective Control Examples |

|---|---|---|

| Invoicing | Sequential numbering, price validation, period lock | Gap analysis on invoice sequences, pricing exception reports |

| Cash Application | Automated matching rules, tolerance limits | Daily reconciliation of bank to AR, unapplied cash aging report |

| Credit Memos | Mandatory documentation, tiered approval matrix | Pattern analysis on reason codes, user-level credit frequency |

| Write-offs | Collection-effort documentation requirement, dual approval | Write-off trend analysis by customer/user/period |

| Reconciliation | Segregation of duties between posting and reconciling | Three-way match: bank statement, lockbox, AR sub-ledger |

Did You Know

Organizations that combine both preventive and detective controls experience fraud losses that are significantly lower than those relying on only one type. Preventive controls stop errors and fraud before they occur; detective controls catch what slips through — together they create a layered defense.

What Are the Key Performance Indicators for Effective AR Risk Monitoring?

Metrics transform AR risk monitoring from a subjective exercise into a data-driven discipline. The right KPIs provide early warning signals before a small anomaly becomes a material loss.

Operational KPIs

Track the average number of days to apply incoming cash, the backlog of unapplied payments, the rate of manual adjustments as a percentage of total postings, and the volume of exception-queue items that exceed their resolution SLA. Deterioration in any of these signals either a process bottleneck or a deliberate manipulation that is slowing down the matching process.

Risk KPIs

Monitor the credit-memo-to-sales ratio over time, write-off trends segmented by customer type and employee, the frequency of post-date changes on invoices or payments, and the concentration of adjustments by individual users. The ACFE 2024 Report to the Nations found that organizations using proactive data monitoring and analytics detect fraud significantly faster than those relying on tips or traditional audits alone.

| KPI Category | Metric | Red-Flag Threshold (Example) |

|---|---|---|

| Operational | Days to Apply Cash | Above 3 business days consistently |

| Operational | Manual Adjustment Rate | Exceeds 15% of total postings |

| Risk | Credit Memo / Sales Ratio | Above 2% of monthly revenue |

| Risk | Write-offs by Single User | More than 40% of total write-offs |

| Risk | Unapplied Cash Balance | Growing for 3+ consecutive periods |

Tip

Build a monthly AR risk dashboard that visualizes these KPIs with trend lines rather than point-in-time snapshots. A single elevated reading may be noise, but a three-month upward trend in manual adjustment rates or unapplied cash balances almost always signals a problem worth investigating.

Common Mistakes That Undermine AR Controls Even When Policies Exist

Having a policy manual does not mean having real control. One of the most common mistakes is treating SoD as a one-time setup rather than an ongoing discipline — roles change, employees cover for each other during vacations, and ERP permissions accumulate over time without periodic review. Another frequent failure is allowing “legacy” customers or high-value accounts to bypass standard credit memo or write-off approval processes because “we know them.” Fraud exploits exactly these exceptions.

A third mistake is reconciling only at month-end. When reconciliation happens 30 days after the fact, a lapping scheme or diversion has already had a full cycle to bury itself deeper. Daily or at least weekly reconciliation of key AR sub-ledger balances against bank data is a non-negotiable control for any organization that takes receivables anomaly detection seriously.

Did You Know

ERP permission creep is one of the most frequently cited findings in internal audit reports. Employees who change roles often retain their previous access rights, and within 18 to 24 months, a significant portion of users in a typical AR department hold conflicting permissions that violate SoD policies.

Does Automation in the AR Process Eliminate or Shift the Risk?

Automation reduces repetitive manual errors and increases consistency — but it introduces a different category of risk. If an automated matching rule is misconfigured, it will propagate the same error across thousands of transactions before anyone notices. If exception thresholds are set too loosely, items that should be flagged for human review will be auto-posted. This is the “automation paradox”: the efficiency gain is real, but so is the potential for systemic, scaled errors.

Governance over automation means treating matching rules, auto-posting thresholds, and exception routing logic as controlled assets. Changes to these rules should follow a formal change-management process with testing and approval. Exception management — the items automation cannot resolve — must remain a high-touch human process with clear ownership and SLAs. Detelix addresses this challenge by sitting as an independent monitoring layer above the ERP: it does not replace your automated processes but continuously verifies that the results those processes produce are consistent, complete, and free of anomalies that suggest either rule misconfiguration or deliberate manipulation.

Tip

Treat your ERP’s automated matching rules like code in a software project — version-control every change, require sign-off from both IT and finance before deployment, and schedule periodic audits to confirm the rules still align with current business logic and risk tolerance.

How Do Access Controls and Audit Trails Protect the AR Process?

Role-based access controls ensure that users can only perform actions appropriate to their function. A cash application clerk should not have the ability to authorize write-offs. A billing coordinator should not be able to modify customer bank details. When permissions are aligned with responsibility — and when every action is logged in an immutable audit trail — the ability to commit and conceal fraud drops sharply.

Essential practices include quarterly access reviews to remove accumulated permissions, real-time alerts on sensitive actions such as credit memo creation above a threshold or changes to customer master data, and retention of audit logs that capture the user, timestamp, before-and-after values, and the workstation or IP address involved. These logs are not just useful for investigations after the fact — they are the raw material that powers receivables anomaly detection and continuous AR risk monitoring.

Did You Know

Immutable audit trails serve a dual purpose: they deter fraud by making employees aware that every action is recorded, and they provide the forensic evidence needed to reconstruct a fraud timeline when an investigation is triggered. Organizations with comprehensive audit logging resolve fraud cases faster and recover more losses.

Building a Practical 90-Day Roadmap for AR Control Excellence

Improving accounts receivable fraud and error controls does not require a multi-year transformation. A focused 90-day plan, broken into three waves, can deliver measurable results.

What to Fix First When Resources Are Limited

Days 1 to 30: Visibility and Stabilization. Map your current AR process end-to-end, identify every point where manual intervention occurs, and reconcile your unapplied cash backlog. Perform a baseline SoD review against your ERP permission sets. The goal is to see clearly before you act.

Days 31 to 60: Hardening. Implement or tighten your credit memo and write-off approval matrix. Remove conflicting ERP roles identified in the first wave. Establish daily reconciliation between bank deposits and AR postings. Define exception-queue SLAs for cash application.

Days 61 to 90: Monitoring and Measurement. Deploy receivables anomaly detection — whether through your ERP’s built-in reporting, a dedicated platform like Detelix, or a structured manual review cadence. Define the KPIs from the table above and assign ownership. Schedule a monthly risk review meeting where the finance team examines trends, investigates flagged items, and documents resolutions.

How to Define a Control Owner for Every Key Control

Every control needs a named individual — not a department — who is responsible for its execution and for reporting when it fails. Document each control, its owner, the evidence that proves it operated, and the escalation path when an exception is found. This “control inventory” becomes the foundation for both internal audit testing and continuous improvement.

Tip

Create a simple control matrix spreadsheet listing each AR control, its owner, execution frequency, evidence type, and last-tested date. Review it monthly during your risk meeting. This one document transforms AR governance from informal practice to auditable process.

How to Choose an AR Risk Monitoring Solution Without Overloading Your Team

The right solution should integrate directly with your ERP and banking data, require minimal manual data preparation, and provide actionable context — not just alerts but explanations of why a transaction was flagged. Look for case management workflows that allow your team to investigate, document, and resolve exceptions within the same platform, and ensure that every manual override is captured in a comprehensive audit trail.

| Business Need | How Detelix Addresses It |

|---|---|

| Real-time visibility into AR anomalies | Continuous scanning of ERP transactions with alerts triggered as exceptions occur, not at month-end |

| SoD monitoring across AR roles | Automated cross-checking of user actions against defined segregation policies with instant violation flags |

| Credit memo and write-off pattern analysis | Behavioral analytics that identify unusual concentrations by user, customer, amount, or timing |

| Audit-ready documentation | Immutable logs and case management records that demonstrate control operation to internal and external auditors |

Detelix Fraud Prevention Solutions

Proactive Monitoring

Continuous real-time surveillance of ERP transactions to detect anomalies, policy violations, and suspicious patterns before they escalate into material losses.

Real-Time Alerts

Instant notifications triggered by high-risk AR events such as unauthorized credit memos, SoD violations, and unusual write-off patterns across your organization.

Gatekeeper

Automated enforcement of segregation of duties and approval workflows that prevent conflicting actions from being executed by a single user in your ERP system.

Experience

Deep industry expertise in cybersecurity and ERP fraud prevention, backed by ISO 27001 and ISO 27799 certifications and years of enterprise deployments.

See Detelix in Action

Frequently Asked Questions

Can small businesses benefit from AR fraud and error controls, or is this only for large enterprises?

Every organization that issues invoices and collects payments faces AR risk. In fact, smaller teams often have less natural segregation of duties, which makes compensating controls and monitoring even more important. Scaled solutions that connect to standard ERP systems make it feasible for mid-sized businesses to implement real-time AR risk monitoring without dedicating a large internal team.

How often should AR reconciliations be performed?

Best practice is daily reconciliation of bank deposits to AR postings. At a minimum, weekly reconciliation is necessary to catch discrepancies before they accumulate. Monthly reconciliation alone leaves too wide a window for errors to compound and for fraud schemes like lapping to remain hidden.

What is the single most effective control against AR fraud?

There is no single “silver bullet,” but segregation of duties combined with independent reconciliation consistently ranks as the most effective structural barrier. When no single person controls an entire transaction flow, fraud requires collusion — which is statistically less common and harder to sustain. Adding continuous receivables anomaly detection on top of SoD creates a layered defense.

How does receivables anomaly detection differ from standard AR reporting?

Standard AR reports show balances, aging, and totals at a point in time. Receivables anomaly detection analyzes patterns across transactions, users, and time periods to identify deviations from expected behavior — such as a sudden spike in manual adjustments by one user or a cluster of credits to a single customer. It moves from “what happened” to “what looks unusual and why.”

Are automated cash application systems immune to fraud?

No. Automated systems reduce manual errors but can be exploited if matching rules are manipulated or if exception handling is not properly governed. Governance over the rules themselves — including change control, testing, and periodic audits — is essential to prevent automation from becoming a new vulnerability.

Ready to Close the Gaps in Your Accounts Receivable Controls?

Are your current AR controls truly preventing damage — or simply documenting it after the fact? Discover how real-time visibility into your AR transactions can help detect risk before it becomes a loss.