Strengthen Your Treasury Controls with Real-Time Fraud Prevention

Detelix delivers continuous, automated oversight across every payment rail, ERP action, and bank relationship your organization maintains.

- Understanding Treasury Cash Control and Fraud Prevention

- Why Treasury Operations Are a Preferred Target

- What the Typical Payment Fraud Chain Looks Like

- How Treasury Risk Monitoring Differs from Financial Reporting

- Implementing Effective Cash Movement Controls

- Segregation of Duties Without Paralyzing a Small Team

- Building a Payment Authorization Matrix That Works

- Payment Rail Governance Across Settlement Networks

- Why Monthly Bank Reconciliations Are No Longer Enough

- Identifying Bank Reconciliation Anomalies

- Preventing Vendor Bank Detail Change Fraud

- How to Reduce First-Payment Risk for New Vendors

- Is Dual Approval Really Enough?

- Building Smart Alerts for Treasury Risk Monitoring

- Mapping Business Needs to Controls: Where Detelix Fits

- The Speed vs. Security Trade-off in Instant Payments

- Common Mistakes in Treasury Control Design

- Key Performance Indicators for Treasury Control Effectiveness

- Moving Beyond Spreadsheets: A Modern Treasury Control Stack

- Regulatory Expectations and Why They Are Tightening

- Incident Response for Suspicious Transactions

- Frequently Asked Questions

In many organizations, treasury operations appear well-governed on the surface. Approval hierarchies exist, bank accounts are reconciled monthly, and payment policies sit neatly in shared folders. Yet when a fraudulent wire leaves the company, when a vendor’s bank details are quietly altered, or when an internal transfer masks a slow embezzlement scheme, the question is always the same: how did this pass through our controls? The answer usually lies in the gap between documented policy and real-time operational visibility. Treasury cash control and fraud prevention is no longer a checklist exercise — it is an ongoing discipline that demands continuous, automated oversight across every payment rail, every ERP action, and every bank relationship your organization maintains. The sections that follow map the control framework from first principles to practical implementation, giving CFOs, controllers, and treasury managers a clear path from reactive investigation to proactive protection.

Key Takeaways

- Manual treasury controls cannot keep pace with real-time payment rails — continuous automated monitoring is essential to detect fraud before funds become irrecoverable.

- Vendor master data manipulation remains one of the most damaging fraud vectors; out-of-band verification and cooling periods are critical defenses.

- Dual approval alone fails when approvers rubber-stamp, share credentials, or collude — layered anomaly detection closes the gap.

- Dynamic approval thresholds that adjust by account, currency, and destination provide far stronger protection than flat dollar limits.

- Moving from monthly to daily or continuous bank reconciliation transforms a compliance exercise into an active fraud detection mechanism.

- Regulatory expectations in Israel and globally are tightening, making proactive controls a compliance necessity rather than an optional best practice.

Understanding Treasury Cash Control and Fraud Prevention

Treasury cash control and fraud prevention sits at the intersection of two distinct disciplines. Control means preventing an unauthorized or erroneous action from executing — think approval thresholds, segregation of duties, and system-enforced blocks. Monitoring means detecting patterns, anomalies, or policy deviations as they happen, or shortly after, so the organization can intervene before damage compounds.

Traditional treasury environments relied heavily on manual controls: a second signature on a check, a printed bank statement reviewed at month-end, or a phone call to confirm a large wire. These methods worked when transaction volumes were low and payment rails were slow. Today, with real-time payment networks, multi-bank connectivity, and ERP-driven straight-through processing, the window between initiation and irrevocable settlement has shrunk to seconds. Manual oversight alone cannot keep pace.

Tip

Map every payment type your organization processes to its corresponding settlement speed. Start your control redesign with the fastest rails, where the recovery window is shortest and the risk of irrecoverable loss is highest.

Why Treasury Operations Are a Preferred Target for Fraud

Treasury sits at the nexus of money, authority, and external connectivity — making it an attractive attack surface for both insiders and external threat actors. A single compromised credential, an outdated user permission, or a socially engineered “urgent” request can bypass controls that look robust in an audit report. The Bank of Israel has formally acknowledged the escalation of financial fraud, establishing a cross-sector task force to address the phenomenon.

The core vulnerability is structural: payment processes combine multiple systems (ERP, banking portal, communication channels), multiple roles (initiator, approver, executor), and multiple external parties (banks, vendors, regulators). Every handoff point is a potential exploit. When organizations rely on periodic reviews rather than continuous visibility, fraudulent transactions can remain undetected for weeks — long enough for funds to become unrecoverable.

Did You Know

According to the Association of Certified Fraud Examiners, the median duration of a payment fraud scheme before detection is 12 months. Organizations with proactive transaction monitoring cut that detection time by more than half.

What the Typical Payment Fraud Chain Looks Like

Most payment fraud follows a predictable sequence, even when the specific technique varies. First, the attacker gains control of a critical data point: a vendor’s bank account number, a user’s login credentials, or a fabricated invoice. Second, the attacker accelerates the process — introducing urgency (“the CEO needs this paid today”) or exploiting a period of low staffing (holiday, weekend batch). Third, the payment is executed through the fastest available rail, minimizing the time window for detection. Fourth, once funds settle, recovery becomes a legal and logistical challenge.

Understanding this chain is essential because effective controls must interrupt it at multiple stages, not just one. A single checkpoint — even dual approval — is insufficient if the preceding data (vendor identity, bank details, invoice legitimacy) has already been compromised.

Tip

Conduct a tabletop exercise with your treasury team that walks through a realistic fraud scenario step by step. Identify exactly where in the chain your current controls would intervene — and where they would not. The gaps you find will prioritize your control investments.

How Treasury Risk Monitoring Differs from Financial Reporting

Treasury risk monitoring is not the same as reviewing a cash-flow report or running a monthly variance analysis. It is the continuous, often automated, surveillance of cash movements and payment behavior against a baseline of expected activity. This includes monitoring transaction amounts relative to historical patterns, flagging payments to new or recently modified beneficiaries, detecting unusual timing (after hours, weekends), and identifying geographic anomalies such as payments routed to jurisdictions the organization does not typically transact with.

The goal is to surface exceptions in near real-time so that a treasury analyst or controller can investigate before a second fraudulent transaction follows the first. Without this layer, organizations are left relying on bank reconciliation — a process that, by design, looks backward.

Did You Know

Organizations that implement real-time transaction monitoring detect fraudulent payments an average of 75% faster than those relying solely on periodic reconciliation and manual review processes.

Implementing Effective Cash Movement Controls

Cash movement controls govern how funds flow between the organization’s own accounts, subsidiaries, banks, and currencies. These movements often receive less scrutiny than vendor payments because they appear “internal.” That assumption is dangerous. A fraudster with access to intercompany transfer functionality can move funds to a controlled account and then externalize them through a less-monitored entity. Effective controls start with defining who is authorized to initiate, approve, and execute each type of movement, and what thresholds apply based on account type, currency, and destination.

Dynamic Approval Thresholds by Account, Currency, and Destination

A flat approval threshold — say, any transfer above $50,000 requires two signatures — ignores the reality that risk varies dramatically by context. A $30,000 transfer to a well-established subsidiary’s operating account carries far less risk than a $10,000 transfer to a newly opened foreign-currency account. Dynamic thresholds adjust based on the specific account, the currency pair, and the destination bank, ensuring that higher-risk movements receive proportionally higher scrutiny without slowing routine liquidity operations.

Dual Control for Sensitive Movements

For high-value or unusual transfers, dual control means two separate individuals must independently authorize the movement, ideally from different functional areas. This is not merely “two clicks” — it requires that the second approver has access to supporting documentation (purpose, source of funds, recipient verification) and a clear obligation to review before approving. Detelix supports this discipline by providing real-time cross-referencing of each movement against policy rules, flagging deviations before the transfer reaches the bank, and ensuring that the approval trail is complete and auditable.

Tip

Review your current approval thresholds and ask: do they differentiate by destination, currency, and account type? If a single dollar threshold governs all transfers regardless of context, you have a structural control weakness that dynamic thresholds can immediately address.

Segregation of Duties Without Paralyzing a Small Team

Segregation of duties (SoD) is a foundational control principle: no single person should be able to initiate, approve, and execute a payment. In large treasury departments, this is straightforward. In smaller teams — common in mid-market companies — strict SoD can feel operationally impossible. The solution is not to abandon the principle but to implement compensating controls.

If one person must handle multiple roles due to headcount constraints, introduce mandatory daily reviews by a non-operational manager, enforce system-level logging of every action, and require periodic independent audits of high-risk transactions. The key is ensuring that no action goes unobserved, even if it cannot be fully separated.

Did You Know

Research from the ACFE shows that organizations with fewer than 100 employees suffer median fraud losses nearly twice as large as larger organizations, primarily because smaller teams struggle to maintain effective segregation of duties.

Building a Payment Authorization Matrix That Actually Works

A payment authorization matrix defines who may approve what, at which amount, through which payment rail, and under which conditions. On paper, most organizations have one. In practice, the matrix often diverges from what the ERP system actually enforces. Legacy permissions accumulate over years of staff turnover; service accounts retain broad access; and “emergency” overrides become permanent. The matrix is only as strong as its implementation in the system — and the regularity with which it is reviewed.

RACI for Payment and Cash Movement Processes

A RACI matrix (Responsible, Accountable, Consulted, Informed) for treasury processes clarifies ownership at every step. The person responsible for entering a payment is not the same person accountable for its accuracy; the compliance officer may need to be consulted for cross-border transfers; and the CFO should be informed of any exception approvals. Documenting this explicitly — and mapping it into system workflows — eliminates ambiguity and reduces the risk of “assumed” approvals.

Periodic Access Reviews and What to Check

Access reviews should occur at least quarterly for treasury-related roles. The review must verify that every user’s permissions match their current job function, that no dormant accounts retain active access, and that service or system accounts are documented and justified. Organizations that integrate this review with an automated control layer can detect permission drift continuously rather than discovering it during an annual audit.

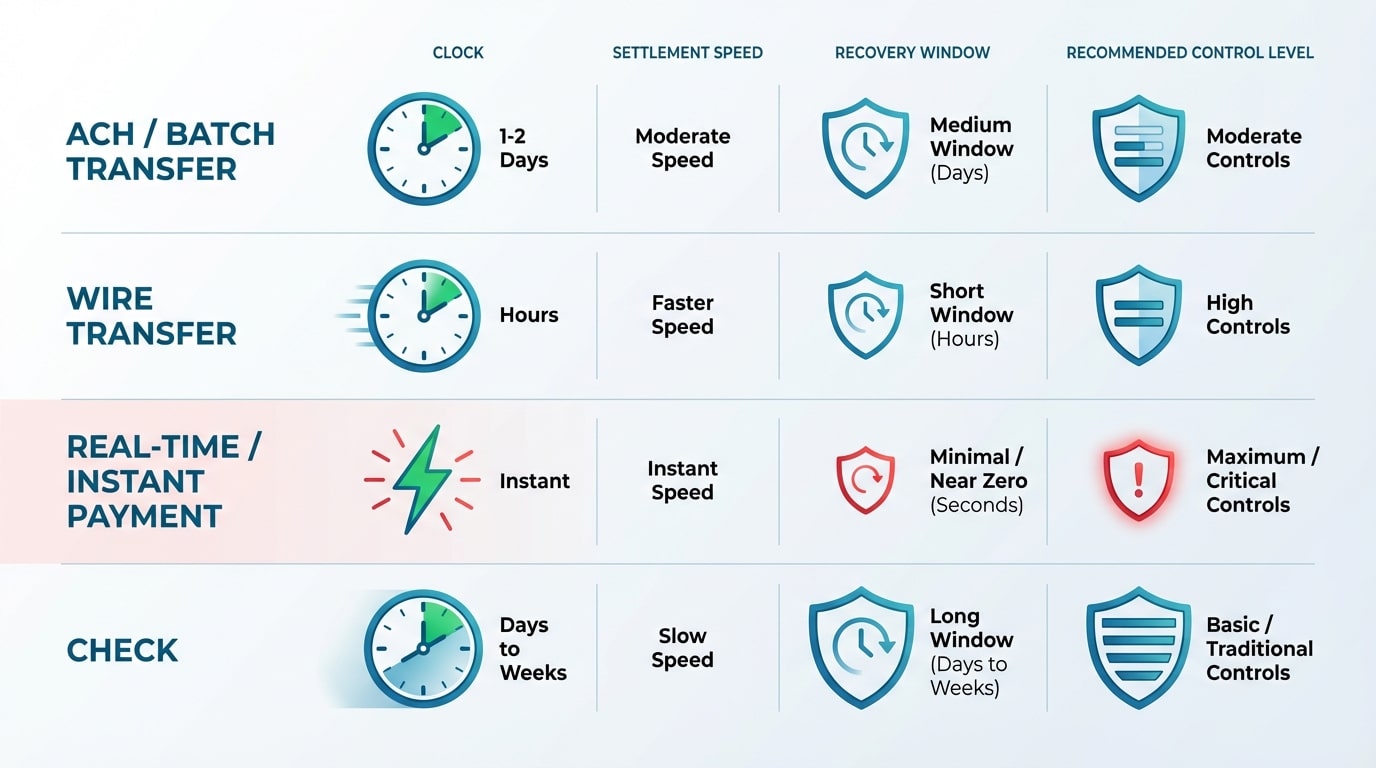

Payment Rail Governance: Managing Risk Across Different Settlement Networks

Not all payment rails carry the same risk profile. A standard ACH batch processed overnight allows time for review and recall. A real-time wire or instant payment settles in seconds, leaving virtually no recovery window. Payment rail governance establishes which rails are approved for specific transaction types, vendor categories, and amount ranges. It also defines escalation procedures: what happens when someone requests a wire for a transaction that policy designates as ACH-only? Without explicit governance, the fastest rail tends to become the default — and speed is the enemy of control.

| Payment Rail | Settlement Speed | Recovery Window | Recommended Control Level |

|---|---|---|---|

| ACH / Batch Transfer | 1-2 business days | Moderate (recall possible within hours) | Standard dual approval above threshold |

| Wire Transfer | Same day / hours | Narrow (minutes to hours) | Enhanced verification + out-of-band confirmation |

| Real-Time / Instant Payment | Seconds | Near zero | Highest tier: pre-release block + senior approval |

| Check | Days to weeks | Wide (stop-payment possible) | Positive pay + reconciliation matching |

Your treasury controls are only as strong as your weakest payment rail. Get a comprehensive assessment of your control gaps from Detelix’s fraud prevention specialists.

Why Monthly Bank Reconciliations Are No Longer Enough

Monthly reconciliation was designed for a world of paper statements and batch processing. In that world, a 30-day review cycle was reasonable. Today, when a fraudulent wire can settle in seconds and a compromised vendor payment can repeat daily, waiting until month-end to match bank records against the general ledger means the organization is perpetually looking at stale data. The gap between transaction execution and reconciliation review is where fraud hides. Moving to daily — or even continuous — automated reconciliation dramatically reduces this exposure. It also transforms reconciliation from a compliance exercise into an active fraud detection mechanism.

Tip

Calculate the total value of payments your organization processes between reconciliation cycles. If that number represents a material loss exposure, the business case for daily or continuous reconciliation writes itself.

Identifying Bank Reconciliation Anomalies Before They Become Losses

Anomalies in bank reconciliation fall into predictable categories, and classifying them systematically is the first step toward effective triage. Not every mismatch signals fraud — but certain patterns demand immediate investigation.

Five Common Anomaly Types in Bank Reconciliation

| Anomaly Type | Example | Potential Risk |

|---|---|---|

| Date mismatch | Payment recorded in ERP on day X, clears bank on day X-3 | Backdated entries to hide timing manipulation |

| Amount rounding | Invoice for $9,997 paid as $10,000 | Skimming or rounding fraud over many transactions |

| Unmatched bank debit | Bank shows outflow with no corresponding ERP record | Unauthorized payment or direct bank manipulation |

| Long-standing open items | Reconciling item unresolved for 60+ days | Masked embezzlement or process failure |

| Duplicate clearings | Same invoice reference clears twice | Duplicate payment fraud or system error |

When Is an Anomaly “Noise” and When Is It “Risk”?

The distinction lies in context and repetition. A single date mismatch in a high-volume account may reflect normal clearing delays. The same mismatch recurring for a specific vendor, or appearing exclusively on a particular approver’s transactions, shifts from noise to a pattern that warrants investigation. Effective monitoring platforms apply contextual rules — analyzing the anomaly relative to the account’s baseline, the vendor’s history, and the user’s behavior — rather than triggering alerts on every deviation. This is where organizations that rely on Detelix’s team of control and fraud-prevention experts gain a practical advantage: the platform’s logic is calibrated to distinguish operational noise from genuine risk indicators.

Did You Know

Studies show that over 60% of reconciliation anomalies flagged by rule-based systems turn out to be false positives. Context-aware monitoring platforms can reduce false positive rates by 40-70%, allowing treasury teams to focus on genuine threats.

Preventing Vendor Bank Detail Change Fraud in an Approved Process

Vendor master data fraud — where an attacker or insider modifies a vendor’s bank account to redirect payments — remains one of the most common and damaging fraud vectors globally. The Bank of Israel’s supervisory authority has warned the public about impersonation-based fraud schemes that exploit exactly this mechanism.

Effective prevention requires structural separation: the person who receives a bank detail change request must not be the same person who approves it. Verification must occur through an independent channel (out-of-band) — for example, calling the vendor at a phone number sourced independently, not from the change request itself. Additionally, implementing a “cooling period” of 24-72 hours between the approval of new bank details and the release of the first payment provides a critical buffer for detection.

Tip

Establish a mandatory 48-hour cooling period for all vendor bank detail changes. During this window, no payments should be released to the updated account. This single control has prevented millions in losses at organizations that implement it consistently.

How to Reduce First-Payment Risk for New Vendors

The first payment to a new vendor is inherently high-risk because there is no historical pattern to compare it against. A fraudster who successfully creates a fictitious vendor — or compromises the onboarding process for a real one — faces the least resistance on the initial transaction. A dedicated “first-payment control” protocol should include identity verification against independent registries, confirmation of the bank account through a micro-deposit or bank letter, a reduced payment threshold for the initial transaction, and enhanced post-payment monitoring for the first 30 days. These steps add minimal friction but significantly reduce the probability of a successful fraud on an untested payment relationship.

Is Dual Approval Really Enough? Three Scenarios Where It Fails

Dual approval is widely regarded as a strong control — and it can be, when implemented correctly. However, it fails in at least three common scenarios. First, when both approvers are rubber-stamping without reviewing supporting evidence (invoice, contract, delivery confirmation). Second, when one approver delegates their credentials or shares access during absence. Third, when collusion exists — two individuals cooperating to push through a fraudulent payment.

The control is only as strong as the independence and diligence of each approver. Organizations that layer automated anomaly detection on top of dual approval — flagging transactions that deviate from expected patterns even after two human approvals — close the gap that human judgment alone cannot fill.

Did You Know

The ACFE’s 2024 Report to the Nations found that collusion between two or more employees increases the median fraud loss by a factor of five compared to single-perpetrator schemes. Dual approval cannot protect against the very collaboration it assumes will prevent fraud.

Building Smart Alerts for Treasury Risk Monitoring Without Drowning the Team

Alert fatigue is one of the most cited reasons why monitoring systems fail in practice. If every minor deviation triggers a notification, the treasury team quickly learns to ignore alerts — including the critical ones. Smart alert design requires three elements.

First, severity classification: not all anomalies carry equal risk, and the system must distinguish between informational, warning, and critical alerts. Second, contextual rules: a $50,000 payment to a long-standing domestic vendor is different from a $50,000 payment to a newly added foreign beneficiary, even though the amount is identical. Third, alert consolidation: multiple related deviations on the same transaction should generate a single, enriched alert rather than five separate notifications. Detelix addresses this by allowing organizations to define alert hierarchies tied to specific accounts, vendors, payment rails, and user roles — ensuring that the right person sees the right signal at the right time.

Tip

Track your alert-to-action ratio monthly. If fewer than 20% of treasury alerts result in a meaningful investigation or confirmed finding, your rules are too broad. Refine by adding contextual filters — vendor tenure, payment rail, time of day, and historical baseline — to improve signal quality.

Mapping Business Needs to Practical Controls: Where Detelix Fits

| Business Need | How Detelix Helps in Practice |

|---|---|

| Real-time visibility into ERP payment actions | Continuous scanning of payment transactions, vendor changes, and approval flows as they occur inside the ERP |

| Detection of vendor master data tampering | Automated cross-checking of bank detail changes against historical records and independent verification triggers |

| Segregation of duties enforcement | Monitoring of user actions to detect SoD violations or compensating control gaps across treasury workflows |

| Reduction of false-positive alerts | Context-aware alert engine that analyzes deviations relative to account, vendor, and behavioral baselines |

| Audit-ready documentation | Complete, timestamped trail of every flagged event, investigation, and resolution for regulatory and internal audit requirements |

The “Speed vs. Security” Trade-off in Instant Payment Rails

Instant payment networks offer undeniable operational benefits: faster settlement, improved supplier relationships, and better cash-flow predictability. But speed compresses the control window. Once an instant payment is released, there is no recall mechanism. This means pre-release controls must be airtight.

Organizations using instant rails should enforce pre-release verification for any payment above a defined threshold, restrict instant-rail access to a limited set of pre-verified beneficiaries, and require that any new beneficiary added to the instant-rail whitelist undergoes the full vendor verification protocol. The trade-off is not “speed or security” — it is designing controls that operate at the speed of the rail.

Did You Know

Real-time payment volumes globally grew by over 42% in 2023 alone, yet fewer than 30% of organizations using instant rails have implemented pre-release controls calibrated to the speed of settlement. This gap represents one of the fastest-growing fraud exposure points in corporate treasury.

Common Mistakes Organizations Make When Designing Treasury Controls

Several recurring errors undermine otherwise well-intentioned control frameworks. Applying a single approval threshold across all payment types ignores the varying risk profiles of different rails and beneficiaries. Treating internal transfers as inherently safe overlooks a well-documented fraud vector. Relying on bank reconciliation as the primary fraud detection tool means discovering problems weeks after they occur. Failing to update user permissions after role changes creates exploitable gaps.

And assuming that technology alone solves the problem — without clear governance, ownership, and escalation procedures — leads to expensive systems that generate data no one acts on. The most resilient treasury functions combine automated monitoring with human judgment, clear accountability, and a culture that treats every anomaly as worth understanding.

Tip

Run a “control gap audit” by listing every payment-related role change in the last 12 months and checking whether the corresponding ERP permissions were updated within 48 hours. Most organizations find that at least 15-20% of role transitions result in lingering access that violates their own authorization matrix.

Key Performance Indicators for Treasury Control Effectiveness

Measuring the effectiveness of treasury controls requires more than counting the number of alerts generated. Meaningful KPIs include: the average time between a suspicious transaction and its investigation (detection-to-response latency); the percentage of vendor bank detail changes verified through out-of-band confirmation before payment release; the number of reconciliation anomalies resolved within SLA versus those escalated; the ratio of false-positive alerts to confirmed exceptions (a proxy for alert quality); and the frequency of access reviews completed on schedule. These metrics provide the CFO and audit committee with tangible evidence that controls are not just designed but operating effectively.

| KPI | Target Benchmark | Why It Matters |

|---|---|---|

| Detection-to-response latency | Under 4 hours | Shorter response windows reduce the probability of secondary fraudulent transactions and increase fund recovery rates |

| Vendor bank change verification rate | 100% out-of-band verified | Unverified bank detail changes are the primary vector for payment redirection fraud |

| False positive ratio | Below 30% of total alerts | High false positive rates cause alert fatigue and desensitize the team to genuine threats |

| Access review completion | 100% quarterly on schedule | Delayed reviews allow permission drift and create exploitable windows for unauthorized access |

| Reconciliation anomaly resolution within SLA | Above 90% | Unresolved anomalies accumulate risk and may mask ongoing fraud or systemic process failures |

Moving Beyond Spreadsheets: What a Modern Treasury Control Stack Looks Like

Many treasury teams still manage critical controls through spreadsheets — manual reconciliation templates, approval trackers in Excel, and email-based exception handling. This approach introduces human error, lacks audit trails, and scales poorly. A modern control stack integrates directly with the ERP and banking platforms, applies rule-based and behavioral analytics to every transaction, and generates structured, actionable alerts with full context.

The transition does not require replacing the ERP or the banking infrastructure. Platforms like Detelix operate as an independent control layer that sits alongside existing systems, continuously cross-checking actions against policy without disrupting operational workflows. This architectural approach means faster deployment, lower integration risk, and immediate visibility gains.

Regulatory Expectations and Why They Are Tightening

Regulators worldwide — and in Israel specifically — are raising the bar for financial controls in electronic channels. The Bank of Israel’s Directive 367 on remote banking explicitly addresses the need for robust identification, authentication, anomaly monitoring, and customer alerts in digital banking operations.

For corporate treasury teams, this regulatory direction signals that controls once considered “best practice” are becoming mandatory expectations. Organizations that proactively implement continuous monitoring, structured alert management, and documented investigation procedures position themselves ahead of compliance requirements rather than scrambling to retrofit controls after a regulatory finding.

Did You Know

The Bank of Israel’s Directive 367 requires financial institutions to implement real-time anomaly detection and customer notification mechanisms for electronic banking channels — a standard that forward-looking corporate treasury teams are now adopting voluntarily as a competitive governance advantage.

Incident Response: What to Do When a Suspicious Transaction Is Detected

Detection without response is meaningless. Every treasury function needs a documented incident-response playbook that covers four phases. First, containment: immediately freeze the transaction or account if technically possible, and preserve all evidence (timestamps, user logs, communication records). Second, investigation: determine whether the anomaly is a false positive, a process error, or a confirmed fraud attempt, involving internal audit or legal counsel as warranted.

Third, remediation: correct the control gap that allowed the incident, whether it is a permission issue, a process bypass, or a vendor data compromise. Fourth, reporting: notify relevant stakeholders — management, audit committee, and where required, regulatory authorities or law enforcement. In Israel, cyber-related incidents including phishing and impersonation can be reported through the National Cyber Directorate’s reporting channel.

Tip

Pre-assign roles for each of the four incident response phases before an incident occurs. When a suspicious transaction surfaces at 4:45 PM on a Friday, you need everyone to know their responsibilities without searching for the playbook.

Detelix Fraud Prevention Solutions

Proactive Monitoring

Continuous surveillance of ERP transactions, vendor changes, and approval workflows to detect anomalies before they become losses.

Real-Time Alerts

Context-aware alerting engine that prioritizes genuine threats over noise, delivering actionable signals to the right stakeholders.

Gatekeeper

Automated pre-release payment controls that enforce policy compliance and block unauthorized transactions before funds leave the organization.

Industry Experience

Deep domain expertise in treasury controls, fraud prevention, and regulatory compliance across financial services, healthcare, and enterprise sectors.

See Detelix in Action

Frequently Asked Questions

What is the single most effective control for preventing payment fraud?

There is no single silver bullet. The most effective approach is layered: combining segregation of duties with real-time transaction monitoring, out-of-band verification for sensitive changes (such as vendor bank details), and automated anomaly detection. Each layer catches what the others might miss, creating a control environment that is significantly harder to circumvent than any individual measure.

How often should bank reconciliation be performed to catch fraud early?

Monthly reconciliation is insufficient for fraud detection purposes. Organizations with meaningful payment volumes should reconcile daily at minimum, and ideally implement continuous automated matching. The shorter the reconciliation cycle, the smaller the window in which fraudulent transactions can remain undetected and unrecoverable.

Can small treasury teams implement effective fraud prevention without large budgets?

Yes. Small teams face tighter SoD constraints, but compensating controls — mandatory manager reviews, system-enforced approval thresholds, automated alerts for high-risk actions, and periodic independent audits — can achieve strong protection. Platforms designed as independent control layers, such as Detelix, are specifically built to add automated oversight without requiring large teams to operate them.

How do we reduce false-positive alerts without missing real threats?

The key is contextual alerting. Rather than applying uniform rules across all transactions, define baselines per account, vendor, and payment rail. Set alert severity tiers so that only genuinely anomalous activity reaches human reviewers at the highest priority. Consolidate related alerts into a single enriched notification. And continuously refine rules based on investigation outcomes — confirmed false positives should feed back into the detection logic.

What role does ERP integration play in treasury fraud prevention?

ERP integration is critical because the ERP is where payment instructions originate, vendor master data is maintained, and approval workflows execute. A control platform that monitors ERP actions in real time — such as changes to vendor bank details, creation of new vendors, or approval overrides — can detect fraud indicators at the point of origin, before funds leave the organization. Without ERP-level visibility, treasury controls are limited to what the banking system reports after the fact.

Ready to Close the Gap Between Policy and Real-Time Control?

Stop relying on monthly reviews to catch what continuous monitoring surfaces in seconds. Talk to the Detelix team about protecting your treasury operations today.