Uncover the Hidden Cost of ERP Fraud Before It Reaches Your Bottom Line

Move from periodic audits to real-time visibility across your ERP processes with Detelix. Get a tailored consultation with our finance risk specialists.

- What is the True Cost of ERP Fraud?

- Breaking Down the Financial Impact

- Why ERP Fraud Goes Undetected for Months

- The Business Cost of Internal Fraud

- Common High-Value ERP Fraud Scenarios

- Mapping Fraud Categories to Business Cost

- Long-Term Business Consequences

- How to Calculate Fraud Exposure

- A Common Mistake in Fraud Risk Management

- Reducing Cost Through Continuous Monitoring

- How Detelix Supports Real Control

- Frequently Asked Questions

In many organizations, financial controls look strong on paper. There are approval flows, ERP permissions, reconciliations, and review procedures. But when a process depends too heavily on routine, manual review, or after-the-fact reporting, risk can still slip through unnoticed. The cost of ERP fraud is rarely a single number on a single invoice — it is the cumulative financial, operational, and reputational damage that unfolds quietly inside sensitive business processes. For CFOs, controllers, and risk leaders, understanding the true cost is the first step toward moving from the illusion of control to real control.

Key Takeaways

- The true cost of ERP fraud extends far beyond the transaction loss — it includes investigation, remediation, disruption, and reputational damage.

- ERP fraud schemes often run undetected for 6 to 24 months, quietly eroding revenue and distorting financial reporting.

- Master data manipulation — especially unauthorized changes to vendor bank details — is one of the highest-risk attack vectors.

- Periodic reviews are insufficient in a real-time transactional environment; continuous monitoring is what stops fraud before funds leave.

- A defensible fraud exposure calculation helps finance leaders turn risk into a measurable, board-level metric.

What is the True Cost of ERP Fraud?

The cost of ERP fraud is not just the sum of stolen funds. It is the total business impact of manipulating ERP processes — from procure-to-pay, to payroll, to vendor master data. A single failure point in a procure-to-pay cycle can generate significant business cost of internal fraud long after the original transaction is settled. The real figure includes direct losses, investigation and recovery expenses, control remediation, and the long-term erosion of profitability and trust. Occupational fraud remains one of the most costly categories of financial loss worldwide, according to the ACFE Reports and Statistics hub, and ERP-driven processes are often where that loss is realized.

Tip

When calculating fraud cost, treat the initial transaction loss as roughly 20% of the total. Budget for investigation, legal review, control remediation, and business disruption as the remaining 80% — that ratio holds consistently across real-world cases.

Breaking Down the Financial Impact of ERP Fraud

To measure the financial impact of ERP fraud, leaders need to separate the event from the aftermath. The transaction loss — funds leaving the organization via fraudulent wires, duplicate payments, or fabricated invoices — is only the visible tip. Detection costs follow: forensic accounting, internal audit time, and legal review. Then come remediation costs: fixing broken workflows, resetting permissions, and patching the control weaknesses that allowed the scheme in the first place. Identifying internal threats at this stage requires specialized tools to detect financial employee embezzlement in real time, before additional transactions compound the loss.

Direct vs. Indirect Costs

Direct costs include fraudulent invoices, payroll ghost employees, and duplicate payments. Indirect costs cover the diversion of management attention, external legal fees, and potential regulatory fines. The hidden layer — the compliance cost of fraud and the audit impact of fraud — often persists for quarters, inflating the total well beyond the original transaction value.

Why ERP Fraud Losses Often Go Undetected for Months

ERP fraud losses statistics consistently show that schemes can run for a year or more before discovery. The reason is structural: control overrides, manual workflow bypasses, and privileged access allow fraudulent activity to blend into legitimate business operations. Master data manipulation is especially dangerous — a small edit to a vendor name, tax ID, or bank account can quietly redirect funds for months. Unauthorized changes to bank account details create one of the most severe vulnerabilities in the payment process, because they exploit a field that rarely receives the same scrutiny as the payment itself.

Did You Know

According to the ACFE, the median duration of an occupational fraud scheme before detection is approximately 12 months — and schemes involving senior management or privileged ERP users frequently exceed 18 months before being identified.

The Massive Business Cost of Internal Fraud in ERP Environments

Occupational fraud losses are driven disproportionately by trusted employees with elevated access. When segregation of duties fails — for example, when one person can both create a vendor and approve its payment — revenue erosion becomes a recurring pattern rather than a single event. The impact on cash flow is immediate: unexpected losses disrupt budgeting, delay legitimate supplier payments, and distort management forecasts. Organizations lose a meaningful percentage of annual revenue to fraud each year, largely due to weak internal controls, as documented in the Occupational Fraud 2024: Report to the Nations.

Tip

Review every ERP role that can both create a vendor and approve a payment. Even in small finance teams, that combination should be split across two individuals — the cost of separating the duties is negligible compared to the cost of one successful fraud scheme.

Common High-Value ERP Fraud Scenarios

Not every fraud scheme carries the same price tag. Some exploit payment processes directly; others manipulate payroll or expense modules. Understanding the scenarios most likely to generate large losses helps finance leaders prioritize where to strengthen controls first.

Accounts Payable and Billing Fraud

This category drives most duplicate payment risk and invoice fraud. Vendor fraud in ERP typically involves shell companies, slightly altered vendor names, or fabricated invoices that mirror legitimate spend patterns. External actors increasingly use business email compromise to impersonate real suppliers and change payment instructions at the last moment. BEC scams alone represent tens of billions in reported losses, according to the FBI IC3 public service announcement on BEC.

Payroll and Expense Manipulation

The cost of internal fraud also accumulates through falsified expense reports, inflated reimbursements, and ghost employees embedded inside the ERP payroll module. These schemes are often low-value per transaction but persistent, which is precisely why they escape periodic review.

Did You Know

Ghost employee schemes in ERP payroll modules typically involve amounts small enough to blend into normal payroll variance — under 2% of total payroll — which is exactly why they often run for years without being flagged by standard reconciliation checks.

Ready to see how real-time monitoring can protect your ERP payments, payroll, and vendor master data from the fraud scenarios outlined above?

Mapping Fraud Categories to Business Cost

The following table maps common ERP fraud categories to their typical cost drivers, helping leadership see where exposure is concentrated.

| Fraud Category | Primary Cost Driver | Typical Detection Delay |

|---|---|---|

| Vendor master manipulation | Redirected payments, duplicate vendors | 6–18 months |

| Accounts payable / invoice fraud | Fake invoices, duplicate payments | 3–12 months |

| Payroll fraud | Ghost employees, inflated hours | 12–24 months |

| Expense reimbursement fraud | Falsified receipts, personal expenses | 6–18 months |

| Business email compromise | Diverted wire transfers | Days to weeks, after funds move |

Long-Term Business Consequences Beyond the Balance Sheet

Reputational damage is one of the least quantifiable but most enduring consequences. Investors, banks, and suppliers respond cautiously once an incident becomes visible. Fraud-related business interruption extends the pain: operations slow while systems are audited, permissions are reviewed, and processes are rebuilt. Compliance cost of fraud can include failed financial audits, restated statements, or penalties tied to material weaknesses in financial reporting. The GAO Standards for Internal Control in the Federal Government underscores how weak controls directly translate into improper payments and avoidable loss.

Tip

When building the business case for stronger ERP controls, quantify the reputational variable by estimating the cost of one week of delayed supplier payments and one external audit cycle. Those two numbers alone usually justify the investment in continuous monitoring.

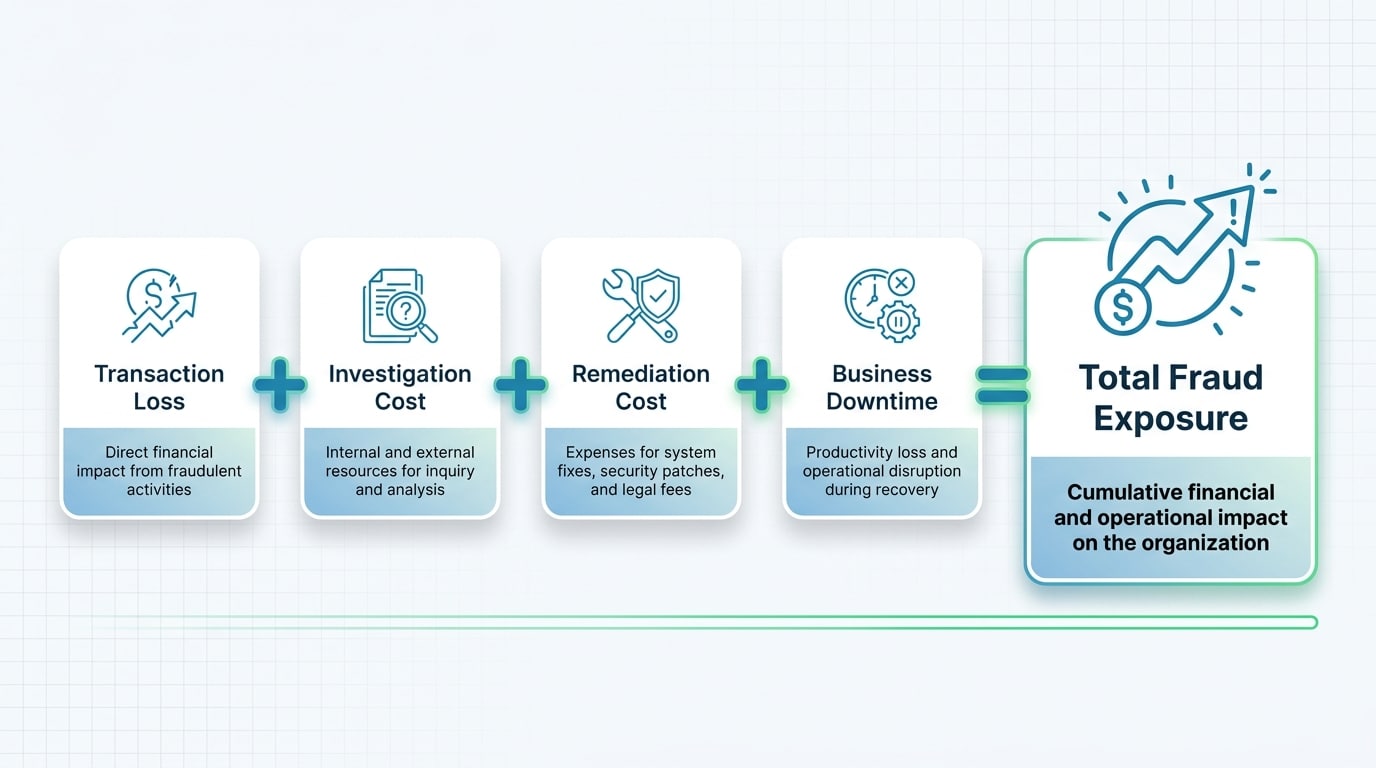

How to Calculate Your Organization’s Fraud Exposure

A simple, defensible formula helps leadership quantify risk before an incident, not after. Fraud exposure equals potential transaction loss, plus cost of investigation, plus cost of remediation, plus business downtime. Applied consistently, this calculation turns fraud risk assessment into a board-level metric rather than a periodic audit note. Anomaly detection — continuously scanning transactions, master data changes, and approval patterns — is the most effective way to lower the cost of undetected fraud, because it shortens the window during which a scheme can compound.

A Common Mistake: Treating Fraud Risk as a Periodic Exercise

Many finance teams still rely on quarterly reviews, sample-based testing, or end-of-month reconciliations to catch irregular activity. By the time those reports surface an anomaly, the funds are usually gone and the trail is cold. The mistake is not the review itself — it is the assumption that periodic checks are sufficient in a real-time transactional environment. ERP processes run continuously; controls must run continuously as well.

Did You Know

Sample-based testing in traditional audit methodology typically covers less than 5% of transactions. In a modern ERP that processes thousands of entries daily, a fraudulent pattern can run through the remaining 95% for an entire audit cycle without being sampled once.

Reducing the Cost of ERP Fraud Through Continuous Monitoring

Real-time fraud prevention controls change the equation. Instead of discovering duplicate vendors or unauthorized transactions after the payment run, continuous monitoring flags them before funds leave the organization. This is the difference between detective controls, which document what already happened, and preventive controls, which stop the event from completing. Automated cross-checks on vendor bank changes, out-of-hours activity, workflow overrides, and unusual approval patterns turn ERP oversight from a reactive function into a live defensive layer.

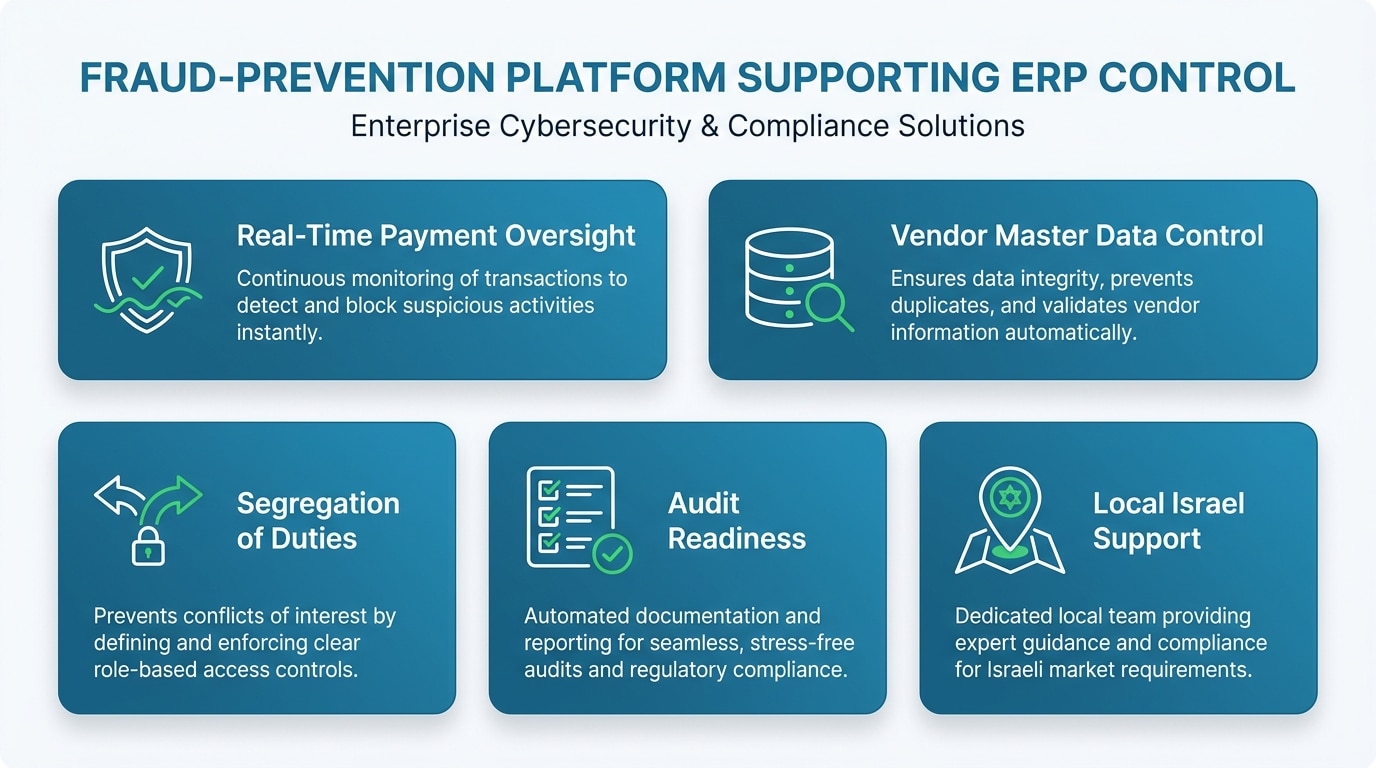

How Detelix Supports Real Control Over ERP Processes

Detelix is built for finance and risk leaders who need visibility into sensitive ERP processes as they happen. The table below maps common business needs to how the platform supports them in practice.

| Business Need | How Detelix Supports It in Practice |

|---|---|

| Real-time oversight of payments | Continuous scanning of transactions and alerts on anomalies before funds are released |

| Control over vendor master data | Monitoring of bank account changes, duplicate vendors, and suspicious edits |

| Segregation of duties enforcement | Cross-checking of approval chains and detection of workflow overrides |

| Fit for organizations operating in Israel | Local implementation, support, and alignment with finance practices used by Israeli businesses |

| Audit readiness | Traceable alerts and documented exceptions that support internal and external audits |

Protecting Profit by Securing the ERP Core

The cost of ERP fraud is controllable when organizations prioritize strong ERP internal controls, continuous monitoring, and disciplined management of privileged access. The most expensive fraud is the one that has not been found yet — because every day it continues, the total business impact grows. Moving from routine checks to real-time visibility is what separates managing activity from actually controlling it.

Detelix Solutions for ERP Fraud Prevention

Proactive Monitoring

Continuous, real-time scanning of ERP transactions and master data changes to surface anomalies as they occur — not months later.

Real-Time Alerts

Immediate notifications on suspicious activity, vendor bank changes, and approval overrides — giving finance teams time to act before funds are released.

ERP Gatekeeper

Preventive controls on sensitive ERP processes, enforcing segregation of duties and blocking high-risk actions before they complete.

Proven Experience

Decades of specialized expertise supporting finance, audit, and risk leaders with tailored fraud prevention solutions.

See Detelix in Action

Frequently Asked Questions

What is ERP fraud?

ERP fraud is any scheme that manipulates ERP processes, data, or access rights to divert funds, falsify records, or bypass controls. It includes vendor fraud, payroll fraud, duplicate payments, and master data manipulation.

How much do businesses typically lose to internal fraud?

Global studies show that organizations lose a meaningful percentage of annual revenue to occupational fraud each year. ERP fraud losses statistics indicate that the longer a scheme runs, the higher the total cost — with many cases detected only after 12 months or more.

Why is ERP fraud more expensive than a simple theft?

Because the transaction loss is only the first layer. Investigation, legal review, remediation of controls, operational disruption, and reputational damage often exceed the original amount diverted.

What are the hidden costs of ERP fraud?

Hidden costs include management time, delayed month-end closings, external audit pressure, strained vendor relationships, and decisions made on distorted financial data.

How can a company identify the early red flags of fraud?

Red flags include unusual vendor bank changes, transactions outside normal hours, repeated workflow overrides, duplicate vendor records, and invoices that closely resemble legitimate ones. Continuous monitoring surfaces these signals as they occur.

Can small businesses survive a major ERP fraud event?

Smaller organizations are often more exposed because a single incident can consume a significant share of working capital. Preventive controls are especially important where recovery margins are thin.

How does segregation of duties reduce the cost of internal fraud?

Segregation of duties ensures that no single person can both initiate and approve a sensitive action. It reduces the opportunity for unilateral manipulation and increases the likelihood that irregular activity is caught before payment.

Ready to See What Real Control Looks Like?

Are your current controls detecting irregular activity in time to stop it, or only documenting it afterward? Move from routine monitoring to real control over your ERP processes.