Stop ERP Fraud Before the Payment Leaves Your Account

Detelix delivers real-time, continuous protection across SAP, Oracle, and NetSuite — closing the gap between detection and prevention.

- Identification and Prevention: ERP Fraud Detection Methods That Actually Work

- Why ERP Environments Demand a Dedicated Detection Approach

- Business Rules: The First Line of Defense

- Anomaly Detection and Machine Learning for Proactive Monitoring

- Master Data Integrity: The Overlooked Attack Surface

- From Periodic Audits to Continuous Automated Fraud Detection ERP

- Mapping Business Needs to Real-Time Control Capabilities

- Reducing False Positives Without Reducing Coverage

- Common Mistakes Organizations Make When Deploying Detection

- Implementation Roadmap: Starting With High-Risk Modules

- Measuring the Effectiveness of ERP Fraud Detection Methods

- The Hybrid Model: Rules, Analytics, and Real-Time Response

- Frequently Asked Questions

In many organizations, financial controls look strong on paper. There are approval flows, ERP permissions, reconciliations, and review procedures. Yet when a sophisticated vendor fraud scheme or a simple duplicate payment slips through, the question leadership asks is always the same: how did this happen inside a system designed to prevent it? The answer usually lies in the gap between having controls and actively enforcing them in real time. Modern Detelix and similar real-time protection platforms provide the infrastructure needed to execute ERP fraud detection methods effectively — combining business rules, anomaly detection, and continuous monitoring across the full population of transactions rather than relying on manual sampling. This is how detecting fraud in ERP shifts from reactive audit to proactive prevention.

Key Takeaways

- Effective ERP fraud detection layers business rules, behavioral analytics, and continuous monitoring rather than relying on any single technique.

- Master data changes — especially vendor bank account modifications — are the most overlooked attack surface and deserve dedicated monitoring.

- Real-time alerts compress detection time from weeks to minutes, enabling intervention before funds leave the organization.

- Calibrated risk scoring and context-aware thresholds are the only way to keep alert volume actionable and avoid fatigue.

- Measuring outcomes — prevented loss, precision rate, time-to-detection — proves control investment value to leadership.

Identification and Prevention: ERP Fraud Detection Methods That Actually Work

Effective ERP fraud detection methods are never built on a single technique. The most resilient programs layer three approaches: deterministic business rules that catch known risk patterns, behavioral anomaly detection that surfaces unknown threats, and continuous monitoring that closes the time gap between an event and its discovery. When these layers operate together, the organization moves from sample-based testing to full population analysis — every invoice, every master data change, every journal entry is cross-checked as it happens.

The practical advantage is clear: instead of discovering a fraudulent payment weeks later during reconciliation, finance teams receive an actionable alert before the money leaves the company. That is the difference between reviewing reports after the fact and actually controlling the process.

Tip

When designing a detection program, map every control to a specific, observable outcome. If you cannot describe the exact alert a rule will generate and the exact action it will prompt, the control is not yet operational — it is still an intention.

Why ERP Environments Demand a Dedicated Detection Approach

Enterprise Resource Planning systems such as SAP, Oracle, and NetSuite concentrate procurement, payments, payroll, inventory, and general ledger activity into a single data environment. That concentration creates efficiency — and exposure. Fraud inside an ERP rarely looks like a single suspicious transaction. It typically involves manipulation of master data, bypassing of approval workflows, or the coordinated use of legitimate permissions for illegitimate outcomes.

Manual sampling cannot keep up with this volume or complexity. Automated fraud detection ERP capabilities are essential because they analyze sequences — who created the vendor, who changed the bank account, who approved the invoice, who released the payment — rather than isolated data points. Governance guidance from public-sector oversight, including the State Comptroller’s guidance on fraud prevention and internal controls, consistently emphasizes that strong control environments require both structural rules and ongoing monitoring of core processes.

Did You Know

According to industry research on occupational fraud, schemes that involve ERP manipulation typically remain undetected for a median of 12 to 18 months — long enough for perpetrators to refine their methods and for recoverable losses to multiply.

Business Rules: The First Line of Defense

Business rules translate known fraud patterns into explicit conditions that trigger alerts. They are the foundation of fraud analytics ERP because they are transparent, explainable, and fast to deploy. A well-designed rule engine flags scenarios such as a vendor bank account change followed within hours by a payment, an invoice number already present in the system, or a purchase order split just below an approval threshold.

Common Rule-Based Indicators

Typical indicators include duplicate invoice detection, round-sum payments outside normal patterns, vendor-employee matches where a supplier shares an address or bank account with a payroll record, and manual journal entries posted outside business hours or at period-end. The logic behind these checks is well established in accounts payable practice, where three-way matching of invoice, purchase order, and goods receipt remains a core integrity control.

Tip

Do not treat round-sum payment detection as a low-value rule. Fraudsters frequently use round figures because they feel deliberate and legitimate. Pair the rule with vendor behavior baselines to separate genuine invoices from manufactured ones.

Anomaly Detection and Machine Learning for Proactive Monitoring

Rules catch what you already know to look for. Anomaly detection catches what you do not. Machine learning models build a baseline of normal behavior for users, vendors, cost centers, and transaction flows, then flag deviations that no static rule would anticipate. A controller logging in at an unusual hour, a vendor whose payment frequency suddenly doubles, or a journal entry that statistically resembles prior fraud cases — these are the patterns behavioral analytics surfaces.

The use of data mining and AI for pattern recognition is a mature field in financial control contexts, as explored by academic work on data mining and its applications. When combined with rules, machine learning gives ERP fraud detection methods the ability to evolve alongside new fraudulent tactics rather than remain frozen at the moment of deployment.

Did You Know

Behavioral baselines are most accurate when they are segmented by role, entity, and transaction type. A single global baseline produces more noise than signal, because normal activity varies dramatically between subsidiaries, departments, and process categories.

Master Data Integrity: The Overlooked Attack Surface

Most ERP fraud begins before any transaction is recorded. It starts with a quiet change to a supplier’s bank account, the creation of a near-duplicate vendor record, or the silent elevation of a user’s permissions. If monitoring focuses only on transactions, the preparatory steps remain invisible until the damage is done.

This is why effective detection treats master data as a first-class monitoring target. Every change to a vendor IBAN, every new supplier created, every modification to approval hierarchies should generate a verifiable record and, where risk scores warrant, an alert. Understanding the dangers of changing bank account details in ERP systems is essential, because a single unauthorized modification can redirect legitimate payments to a fraudulent destination before any downstream control has a chance to react.

Master data changes often precede fraudulent payments by hours or minutes. See how Detelix cross-checks vendor modifications against pending transactions in real time.

From Periodic Audits to Continuous Automated Fraud Detection ERP

Periodic audits serve an important purpose, but they operate on a delay. By the time a quarterly review identifies an anomaly, funds may already be gone, vendors dissolved, and evidence degraded. Continuous monitoring compresses the detection gap from weeks to minutes, enabling intervention before the damage occurs.

The economic logic is straightforward: preventing a fraudulent payment is materially cheaper than recovering one. Automated fraud detection ERP reduces mean time to detection by analyzing every transaction as it flows through the system, not a sample pulled months later. This distinction between periodic audit and ongoing supervisory control is a recurring theme in guidance on internal audit practice, which positions continuous monitoring as a complement to — not a replacement for — formal audit cycles.

Tip

Treat continuous monitoring and periodic audit as partners, not competitors. Monitoring catches events as they happen; audit validates that the monitoring itself is working. Drop either one, and coverage gaps appear quickly.

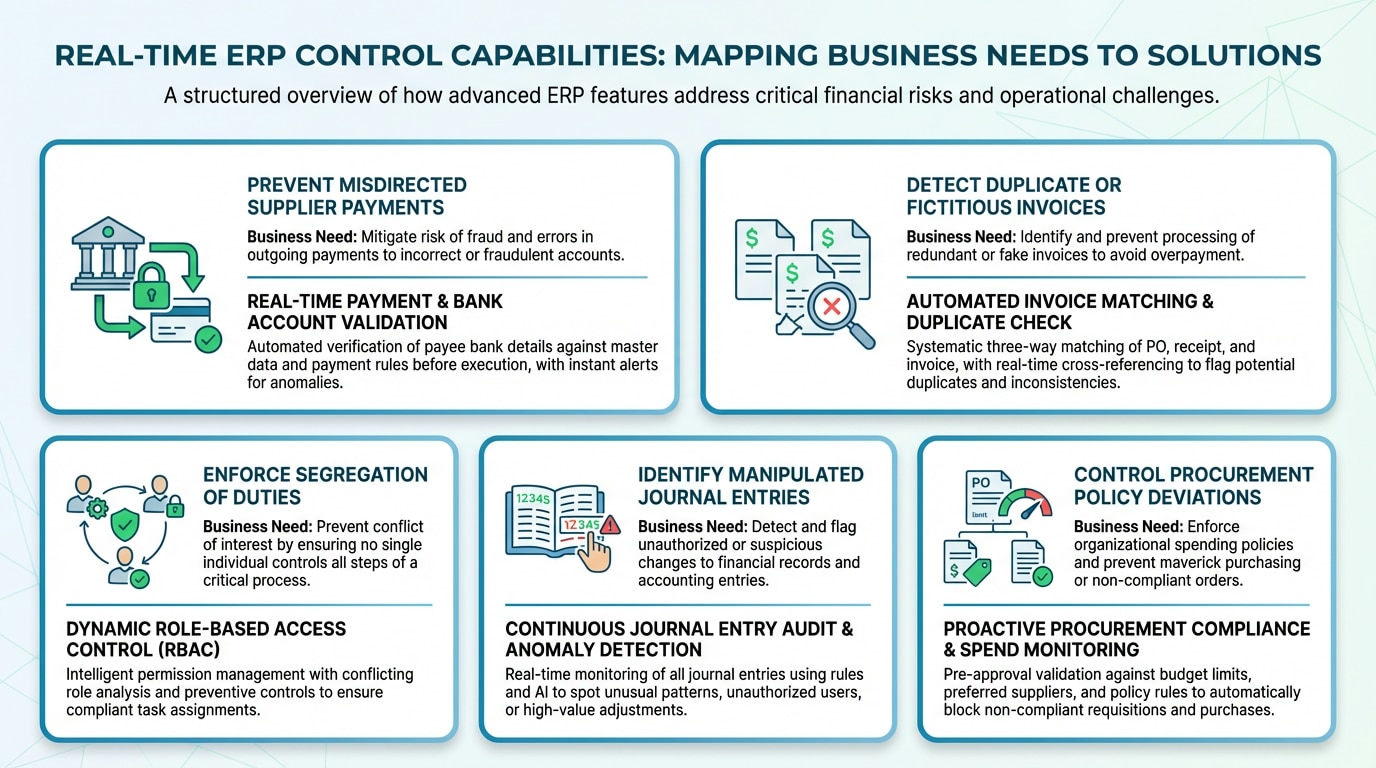

Mapping Business Needs to Real-Time Control Capabilities

Different process areas generate different risk signatures. The table below maps common control needs to the practical capabilities a real-time protection layer should deliver.

| Business Need | Risk Indicator | How a Real-Time Platform Helps |

|---|---|---|

| Prevent misdirected supplier payments | Bank account change immediately before payment release | Cross-checks master data changes against pending payments and alerts before release |

| Detect duplicate or fictitious invoices | Identical invoice numbers, amounts, or near-duplicate vendor records | Full-population matching across invoices, POs, and vendor files |

| Enforce segregation of duties | One user creating, approving, and releasing a transaction | Continuous monitoring of role combinations and workflow bypasses |

| Identify manipulated journal entries | Manual postings at period-end, round sums, unusual accounts | Behavioral analytics on journal entry patterns and user activity |

| Control policy deviations in procurement | Split POs below approval thresholds | Aggregation analysis across related transactions and vendors |

Reducing False Positives Without Reducing Coverage

Alert fatigue is the silent failure mode of fraud detection programs. When teams are flooded with low-quality alerts, genuine risks get ignored. The goal of mature fraud analytics ERP is not maximum sensitivity — it is operational precision. That means calibrating thresholds to the specific rhythm of the business, segmenting rules by entity or transaction type, and applying risk scoring so the highest-priority anomalies rise to the top of the queue.

Context matters. A seasonal spike in a retail subsidiary is not the same as an unexplained surge in a services division. Emergency payment workflows used during crisis periods should not generate the same alert weight as routine activity. Well-calibrated systems separate these contexts automatically, preserving signal while suppressing noise.

Did You Know

In mature programs, precision rates — the share of alerts that become confirmed findings — typically climb from under 10% in the first months of deployment to 40% or higher after 12 months of calibration. The improvement comes almost entirely from tuning, not from new rules.

Common Mistakes Organizations Make When Deploying Detection

Even well-funded programs stumble on predictable errors. Treating fraud detection as a one-time project rather than an ongoing capability is the most common. Others include relying solely on ERP-native controls that only enforce what was configured at implementation, deploying machine learning without explainability so investigators cannot justify alerts, and neglecting master data monitoring in favor of transaction-only analysis.

Another frequent gap is failing to define clear ownership. Without assigned responsibility across finance, internal audit, and IT, alerts accumulate without resolution. Detection only creates value when it connects to a defined investigation and response workflow.

Tip

Before deploying a new detection rule, answer three questions: who will review the alert, within what time frame, and with what authority to act. If any answer is unclear, the rule will generate noise rather than protection.

Implementation Roadmap: Starting With High-Risk Modules

Successful deployment begins where exposure is highest and evidence is cleanest. Accounts Payable, vendor master data, general ledger journal entries, and payroll are typical starting points. Launch in monitoring mode first to tune thresholds, then progressively enable blocking or hold actions as confidence builds.

Segregation of duties deserves explicit attention. The principle that no single user should control multiple stages of a sensitive process is foundational to audit practice, as reinforced in professional materials on audit fundamentals and separation of functional roles. Detection systems should flag not only direct SoD violations but also indirect ones created through delegation, temporary access, or emergency overrides.

Did You Know

Indirect segregation-of-duties violations — created through temporary access grants, emergency overrides, or chained delegations — are often more dangerous than direct ones because they appear compliant on paper while effectively concentrating authority with a single user.

Measuring the Effectiveness of ERP Fraud Detection Methods

Detection programs need quantitative proof of value. The metrics that matter most are not alert volume but outcome-based: reduction in mean time to detection, value of losses prevented, ratio of confirmed findings to total alerts, and reduction in manual reconciliation effort. These measures connect control investment to business results that leadership can defend.

| Metric | What It Measures | Why It Matters |

|---|---|---|

| Mean time to detection | Hours or days between an event and its identification | Shorter times mean greater ability to prevent loss |

| Precision rate | Confirmed findings as a share of total alerts | Indicates whether the system generates actionable signal |

| Prevented loss value | Monetary value of blocked or reversed transactions | Directly quantifies return on the control investment |

| Coverage rate | Share of transactions analyzed across the population | Full coverage eliminates sampling blind spots |

| Investigation cycle time | Average time to close an alert with a decision | Reflects operational maturity of the response workflow |

The Hybrid Model: Rules, Analytics, and Real-Time Response

The strongest ERP fraud detection methods combine three elements that no single technique can deliver alone. Business rules provide explainable, fast-acting coverage for known patterns. Anomaly detection identifies deviations that rules cannot anticipate. Real-time alerts and workflow integration convert detection into prevention by stopping suspicious actions before they complete.

This hybrid model is what transforms fraud analytics ERP from a reporting exercise into an operational control layer. It gives finance and audit leaders full visibility into sensitive processes, reduces dependence on manual review, and creates the conditions for acting before money leaves the organization. The objective is not simply to monitor activity — it is to control it with accurate, timely information.

Detelix ERP Fraud Prevention Solutions

Proactive Monitoring

Continuous analysis of every ERP transaction and master data change, closing the gap between events and detection.

Real-Time Alerts

Immediate notifications when suspicious patterns emerge, enabling intervention before fraudulent payments are released.

Gatekeeper Controls

Enforced checks on vendor master data, segregation of duties, and approval workflows across your ERP environment.

Industry Experience

Decades of applied expertise deploying fraud analytics across SAP, Oracle, and NetSuite for enterprise finance teams.

See Detelix in Action

Frequently Asked Questions

What is ERP fraud detection?

ERP fraud detection is the process of identifying suspicious patterns, control violations, and anomalies within the data and workflows of an Enterprise Resource Planning system. It differs from general fraud detection because it analyzes process sequences, user permissions, and master data changes in addition to individual transactions.

How do you detect fraud in an ERP system?

Detection relies on layering business rules, behavioral anomaly analysis, and continuous monitoring across transactions, master data, and user activity. The most effective approaches analyze the full population of events rather than manual samples, enabling earlier intervention.

What are the best ERP fraud detection methods?

The best methods combine rule-based indicators for known risks, machine learning for behavioral anomalies, real-time alerts for immediate response, and master data monitoring to catch preparatory actions such as vendor bank account changes.

Can duplicate invoices be detected automatically?

Yes. Automated fraud detection ERP tools match invoices across fields including number, amount, vendor, date, and purchase order reference, flagging exact and near-duplicates for review before payment release.

How do you reduce false positives in ERP fraud detection?

Reduce false positives by calibrating thresholds to business context, segmenting rules by entity or transaction type, combining multiple indicators into risk scores, and separating seasonal or emergency activity from routine baselines.

Is machine learning necessary for fraud analytics ERP?

Machine learning adds meaningful value when sufficient data and quality labels exist, but it does not replace foundational business rules. The strongest programs use ML to extend rule-based detection, not substitute for it.

Where should an organization start implementing ERP fraud detection?

Start with high-risk, high-volume modules such as Accounts Payable, vendor master data, and general ledger journal entries. Launch in monitoring mode, tune thresholds, then expand coverage as operational confidence grows.

Ready to Move From Routine Monitoring to Real Control?

See how real-time alerts, continuous monitoring, and layered detection methods can help your team prevent costly errors and fraud before damage occurs.