Stop ERP Fraud Before It Costs You Millions

Proactive fraud prevention for SAP, Priority, and enterprise ERP environments. Get real-time visibility into your financial controls today.

- What Is ERP Fraud Prevention?

- Detection vs. Prevention: Why the Difference Is Critical

- Why ERP Systems Remain Vulnerable to Fraud

- Practical Scenario: How Vendor Fraud Happens Inside an ERP

- The Common Mistake: Relying Solely on RBAC

- Built-In ERP Controls vs. Dedicated Fraud Prevention

- Segregation of Duties: Preventing Single-Person Control

- Identifying Toxic Role Combinations Before They Become a Problem

- Duplicate Payments and Invoices: Risk in the Details

- Continuous Controls Monitoring: A Game-Changer

- Critical Red Flags to Monitor Inside Your ERP

- How to Reduce False Positives So Alerts Actually Work

- Fraud Risks Across Key Business Processes

- Building Approval Workflows That Prevent Fraud Without Slowing Business

- Must-Have Capabilities in Enterprise Fraud Prevention Software

- ROI of Fraud Prevention: When Does the Investment Pay Off?

- What to Present in an Audit: Logs, Evidence, and Approval Trails

- Frequently Asked Questions

Many organizations believe their financial controls are airtight. Approval workflows exist, role-based permissions are configured in the ERP, account reconciliations happen on schedule, and review procedures run like clockwork. Yet when controls depend too heavily on routine, manual checks, or after-the-fact reporting, risk quietly accumulates beneath the surface. ERP fraud prevention is not simply another technology layer. It is a management discipline designed to restore genuine control over sensitive financial processes before damage occurs rather than investigating it months later.

Key Takeaways

- ERP fraud prevention focuses on blocking unauthorized transactions in real time, not just detecting anomalies after the fact.

- Role-based access controls (RBAC) alone cannot prevent fraud; dynamic Segregation of Duties, continuous monitoring, and risk-based approvals are essential layers.

- Toxic role combinations, vendor master data changes, and duplicate invoices represent the highest-risk vectors inside ERP environments.

- Continuous Controls Monitoring (CCM) examines 100% of transactions rather than quarterly samples, dramatically reducing exposure windows.

- A well-calibrated fraud prevention system reduces false positives through dynamic risk scoring, keeping finance teams focused on real threats.

- Detelix integrates directly with SAP, Priority, and other ERP platforms for rapid deployment without disrupting existing business processes.

What Is ERP Fraud Prevention?

ERP fraud prevention combines controls, permission management, intelligent approval workflows, and continuous monitoring to stop fraud, costly errors, and policy violations before they become payments, accounting entries, or operational damage. The approach centers on proactive prevention rather than retroactive investigation.

In practice, this means blocking unauthorized actions in real time, identifying conflicts in user permissions, monitoring changes to vendor and employee master data, and enforcing dual approvals on sensitive transactions. Everything happens within the business environment itself, the ERP, so finance teams maintain full transparency over what is occurring at any given moment.

Tip

Map every process where money moves, sensitive data changes, or accounting entries are created. These are your fraud prevention priority zones. Start there, not with a blanket approach across every module.

Detection vs. Prevention: Why the Difference Is Critical

Many organizations focus on ERP fraud detection, meaning they identify suspicious activity after the action has already been executed. A duplicate invoice surfaces during a quarterly review. A fictitious vendor is uncovered in an annual audit. The problem is straightforward: by the time the anomaly is discovered, the funds have already left the organization.

ERP fraud prevention, by contrast, aims to block the possibility of executing the fraud from the outset. Rather than asking “what happened?”, the operative question becomes “what is about to happen, and how do we stop it?” Consider this example: a single user creates a new vendor, modifies the vendor’s bank details, and releases a payment, all without a secondary approval. Detection catches this weeks or months later. Prevention blocks it before the payment file is generated.

Did You Know

According to the Association of Certified Fraud Examiners (ACFE), the median duration of a fraud scheme before detection is 12 months. Organizations that implement proactive monitoring reduce that window to weeks or even days.

Why ERP Systems Remain Vulnerable to Fraud, Even with Permissions in Place

ERP systems were engineered to process data efficiently, not to identify sophisticated fraud patterns. Role-based access control (RBAC) defines “who is allowed to do what,” but in practice, permissions tend to expand over time. An employee receives an emergency exception for a critical task, and that elevated access stays open for months or years. Shared user accounts, temporary workarounds that become permanent, and zero monitoring on master data changes all create control gaps that fraud exploits.

Israel’s National Cyber Directorate (CERT) consistently emphasizes the need for continuous monitoring and rapid response because both external and internal attack vectors evolve constantly. ERP systems are attractive targets precisely because they concentrate financial data, payment mechanisms, and accounting records in a single environment.

Tip

Run a quarterly “permission hygiene” review. Export all users with elevated or cross-functional access, compare against current job roles, and revoke anything that no longer matches. Most organizations discover 15-30% of permissions are outdated.

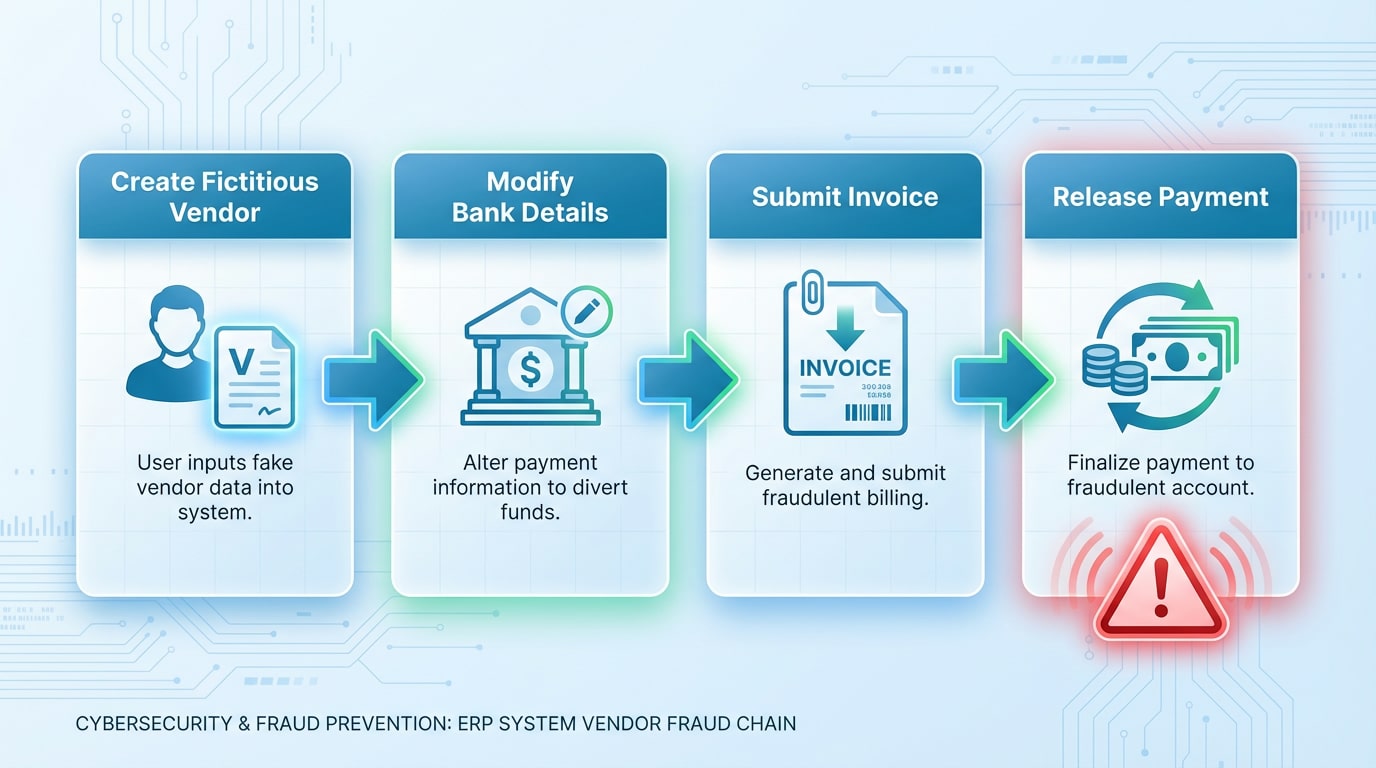

Practical Scenario: How Vendor Fraud Happens Inside an ERP

Vendor fraud is one of the most common risks in the Procure-to-Pay cycle. The classic scenario: an insider creates a fictitious vendor in the system, submits invoices against that vendor, and releases payments to a bank account under their control. An equally common variant: modifying the bank details of a legitimate vendor just before a payment run, diverting funds to a malicious destination.

Effective controls include verifying bank account changes through an external channel, enforcing dual approval for every vendor master data modification, cross-matching vendor-invoice-bank account relationships, and monitoring for abnormal change frequencies. Organizations can also integrate governmental verification services, such as invoice verification against the Israeli Tax Authority, as an additional control layer. Understanding the dangers of changing bank account details in ERP systems helps identify the most vulnerable points in the process.

Did You Know

In many vendor fraud cases, the fictitious vendor shares a mailing address, phone number, or bank account with an existing employee. A simple cross-reference check between vendor and employee master data can surface these overlaps instantly.

The Common Mistake: Relying Solely on RBAC to Prevent Fraud

RBAC is a necessary foundation, but on its own it cannot effectively prevent fraud in ERP. RBAC defines “who is authorized,” but it does not always detect dangerous combinations of permissions, anomalous activity patterns, or suspicious master data changes that occur just before a payment run.

An organization that relies exclusively on built-in permissions lives under an illusion of control. To transition from perceived control to genuine control, you also need Segregation of Duties (SoD), risk-based approval workflows, continuous monitoring with real-time alerts, and rapid investigation capabilities backed by a complete audit trail.

Tip

Ask your ERP administrator this question: “Can any single user create a vendor, change bank details, and approve a payment?” If the answer is “I would need to check,” your RBAC alone is not enough.

Built-In ERP Controls vs. a Dedicated Fraud Prevention Layer

| Criterion | Built-In ERP Controls | Dedicated ERP Fraud Prevention Layer |

|---|---|---|

| Transaction coverage | Basic rules (exact matching) | 100% of transactions, including fuzzy matching |

| Master data monitoring | Change log without proactive alerting | Real-time alerts on every anomalous change |

| Segregation of Duties | Static, configured once | Dynamic, continuously checked for conflicts |

| Pattern detection | Limited to rigid rules | Analytics + custom rules + risk scoring |

| Audit trail | Exists but scattered across modules | Centralized, with built-in case management |

| Response time | After-the-fact (periodic reports) | Before the damage occurs |

The fundamental difference: an ERP system manages processes, but enterprise fraud prevention software protects those processes from exploitation, whether the source is human error, insider fraud, or an external threat.

Segregation of Duties (SoD): The Control That Prevents One Person from Owning an Entire Process

Segregation of Duties ensures that no single individual can initiate, approve, and conceal an action. For example, if the same user can create a vendor, modify the vendor’s bank details, and authorize a payment, all three stages of a classic fraud scheme sit in one pair of hands.

SoD is also a regulatory requirement. Israel’s Privacy Protection Regulations (Data Security) mandate permission management, documentation, and ongoing controls over information repositories, and the ERP is exactly that kind of repository. Enterprise fraud prevention software maps these conflicts dynamically and alerts when a user accumulates a dangerous combination of permissions.

Did You Know

SoD conflicts tend to accumulate silently. A user who changed departments three years ago may still retain permissions from their previous role. Without dynamic SoD monitoring, these “permission ghosts” remain invisible until exploited.

Your ERP holds your most sensitive financial data. Are you confident no one is exploiting gaps in your controls right now? Talk to Detelix about real-time fraud prevention.

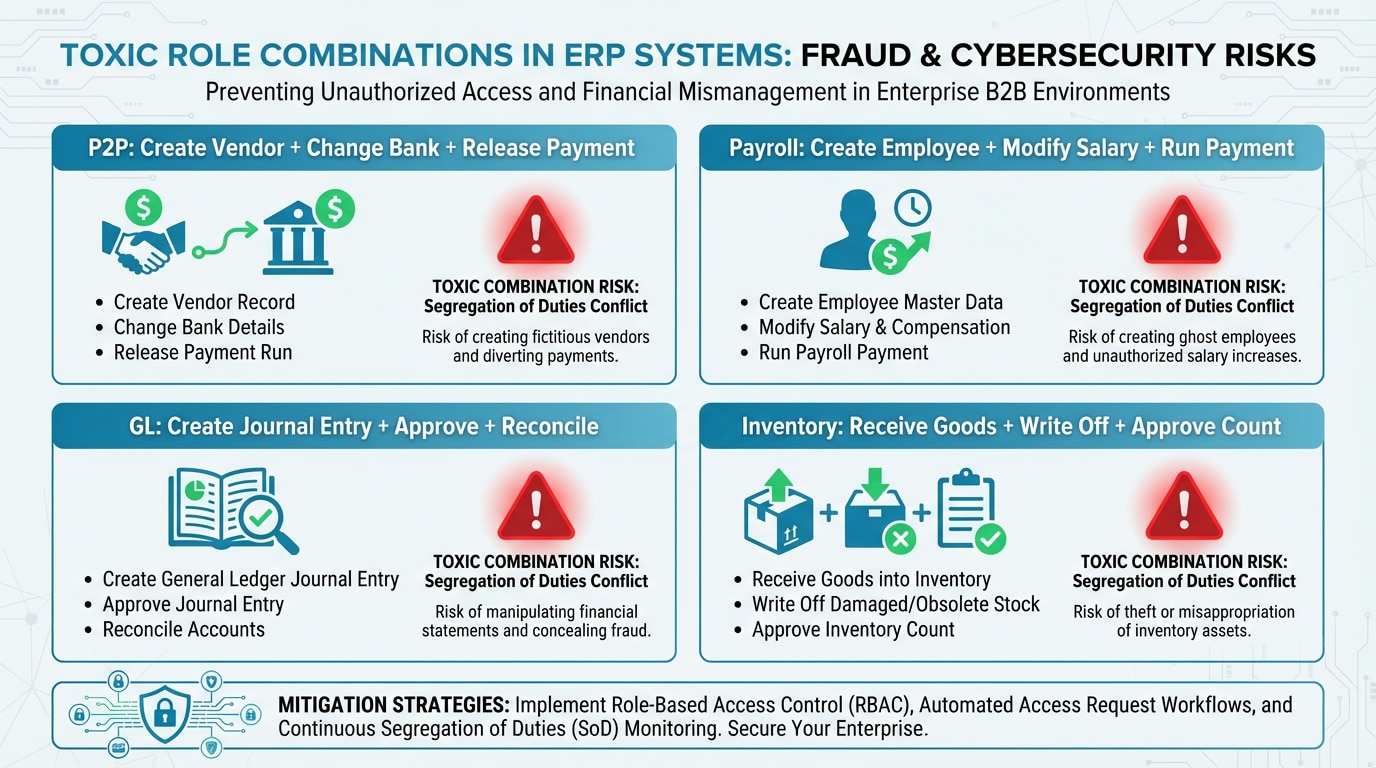

How to Identify Toxic Role Combinations Before They Become a Problem

Toxic combinations are permission sets that allow a single user to execute an entire chain of action without external oversight. Identifying them requires mapping every sensitive operation, create, approve, pay, post, reconcile, and checking who actually holds more than one role in the chain.

| Process | Toxic Combination Example | Risk |

|---|---|---|

| P2P | Create vendor + change bank details + release payment | Fictitious vendor with direct payment |

| Payroll | Create employee + modify salary + run payroll | Ghost employee or salary inflation |

| General Ledger | Create journal entry + approve + perform reconciliation | Concealing embezzlement through accounting entries |

| Inventory | Receive goods + write off inventory + approve count | Inventory theft documented as “adjustment” |

This check must run continuously, not just at the time a role is initially defined. Permissions change, employees move between departments, and “temporary fixes” become permanent fixtures.

Tip

Create a “toxic combination matrix” for your top five business processes. Review it monthly against actual user assignments. Automate the comparison if possible, because manual checks at scale are error-prone and often skipped.

Duplicate Payments and Invoices: The Risk Hiding in Small Details

Duplicate payments are not always the result of malicious intent. Frequently they stem from human error. But whether caused by a typo or deliberate exploitation, the financial impact is identical: money leaving the organization unnecessarily. The challenge intensifies when duplicates are not exact matches. A data entry mistake in an invoice number, an invoice split into two amounts, or a minor variation in the vendor name can all bypass basic duplicate checks.

Effective controls combine hard stops (automatic blocking of exact duplicates) with fuzzy matching (flagging high-similarity records for manual review). Equally important is a clear exception handling mechanism that allows the AP team to process legitimate exceptions without paralyzing the workflow. For a deeper dive, read about detecting duplicate payments in ERP and the practical approaches to handling them.

Did You Know

Research indicates that approximately 0.5% to 2% of all business payments are duplicates. For an organization processing 50,000 payments annually, that translates to 250 to 1,000 duplicate payments per year, representing significant financial leakage even without any intentional fraud.

What Is Continuous Controls Monitoring, and Why Does It Change the Game?

Continuous Controls Monitoring (CCM) is automated, ongoing monitoring that examines 100% of transactions, changes, and permission actions in the system, not a 5% quarterly sample. Instead of discovering an anomaly during an internal audit that occurs once per quarter, CCM delivers alerts in real time or near-real time.

Detelix implements this approach through purpose-built algorithms that operate in the background against the ERP environment. Every sensitive action, a bank detail change, vendor creation, off-hours payment, unusual journal entry, is checked against a set of rules and business context. Anomalies receive prioritization based on risk level. The result: the finance team focuses on cases that genuinely demand attention, rather than drowning in a sea of data.

Tip

When implementing CCM, start with three to five high-value rules rather than attempting to monitor everything at once. A “bank detail change followed by payment within 48 hours” rule alone can surface the majority of payment diversion attempts.

Critical Red Flags to Monitor Inside Your ERP

The most significant red flags connect three layers: permissions, master data changes, and financial transactions. Each flag in isolation may appear innocuous. The combination between them creates a clear risk picture.

Master Data Red Flags

Bank account changes for a vendor close to a payment run. A new vendor created without a corresponding purchase order. A vendor address that matches an employee address. A new employee record created directly in the payroll module without an HR entry.

Transaction Red Flags

Payments processed outside normal business hours. Payment splitting into amounts below the approval threshold. Round-number invoices at unusual amounts. Abnormally high payment volume to a new vendor. Manual journal entries at quarter-end without a supporting source document.

Did You Know

Fraudsters who split payments to stay below approval thresholds often follow predictable patterns. Three payments of $9,800 to the same vendor within a week, each just under a $10,000 threshold, is a textbook red flag that automated monitoring catches instantly.

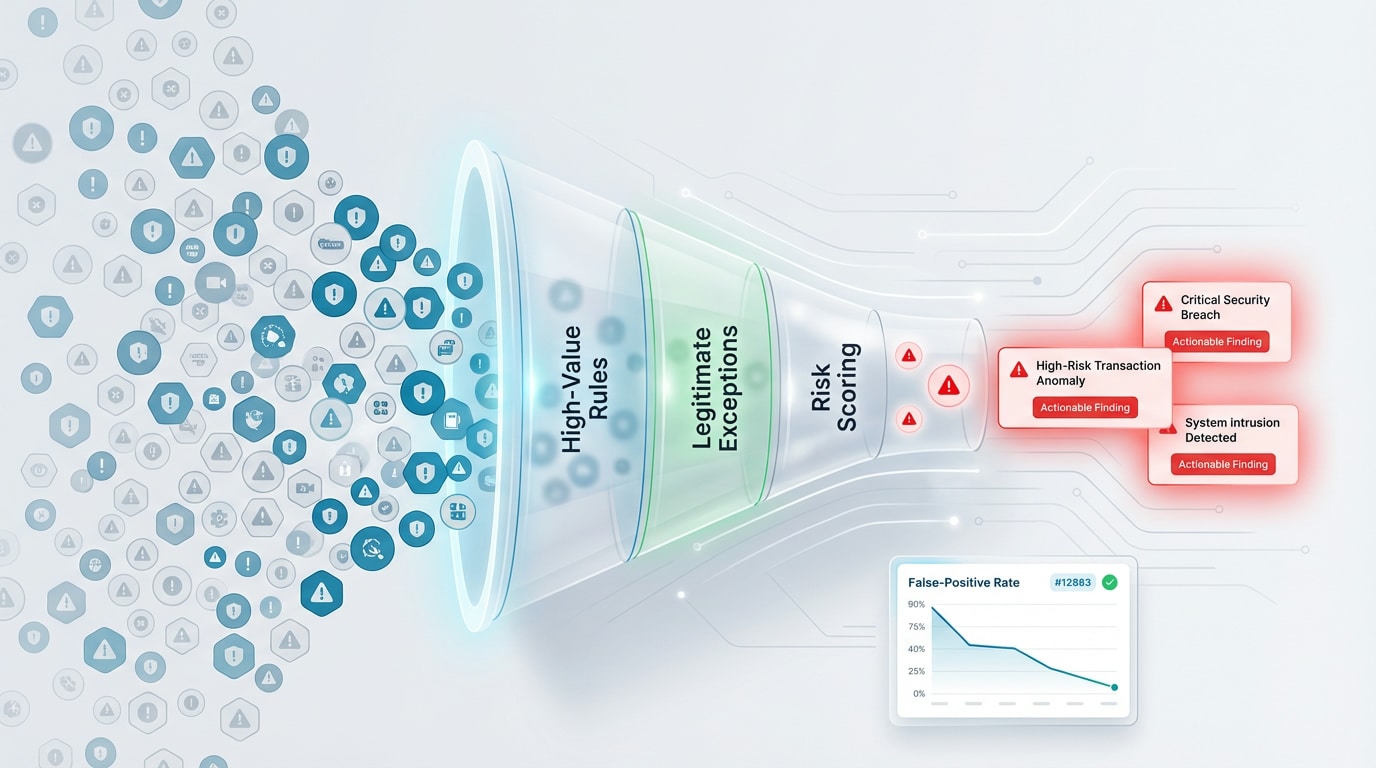

How to Reduce False Positives So That Alerts Actually Work

One of the greatest challenges in any ERP fraud detection system is alert fatigue. If the team receives hundreds of alerts daily and most are false positives, they stop paying attention, which is no less dangerous than having no monitoring at all. The solution is gradual, context-based calibration.

Step one: begin with a small rule set that delivers high business value (e.g., bank change plus payment within 48 hours). Step two: add legitimate exceptions to the system (established vendors that change banks through a formal process). Step three: measure the alert-to-real-case ratio and calibrate accordingly. Detelix provides dynamic risk scoring that prioritizes findings by severity, ensuring the finance team sees what requires immediate action first.

Tip

Track your “alert-to-investigation” ratio weekly during the first 90 days. A healthy system should convert at least 20-30% of alerts into actual investigations. If the ratio drops below 10%, your rules need tightening.

Fraud Risks Across Key Business Processes

ERP system fraud risks concentrate in processes where money moves, sensitive data changes, or accounting records are created. Each business process generates unique “control points” where fraud can hide.

Procure-to-Pay (P2P)

Fictitious vendors, duplicate invoices, payment without goods receipt, and payment diversion through bank detail changes. This is where the majority of direct financial losses are concentrated. Key controls include new vendor verification, three-way matching, and master data change monitoring.

Payroll and Human Resources

Ghost employees, unauthorized salary changes, and inflated overtime payments. Key controls include cross-referencing employee lists between HR and the payroll module, monitoring anomalous salary data changes, and checking for employees who appear in only one module.

Did You Know

Ghost employee fraud can persist for years when payroll and HR systems are not cross-referenced automatically. In one documented case, a payroll clerk maintained 23 fictitious employees for over four years before an external audit flagged the discrepancy.

Building Approval Workflows That Prevent Fraud Without Slowing Business

An effective approval process is risk-based, not “approve everything.” If every action requires dual approval, the team learns to rubber-stamp without actually reviewing, and the control loses its value. The right approach: require additional approval only when a risk trigger is present, such as an unusual amount, a new vendor, a master data change, or a deviation from agreed terms.

Approval levels should be tiered by amount thresholds and action type. Master data changes (address, bank, payment terms) should always require a second, independent approval. Every legitimate exception is documented with a reason, so the audit trail makes clear why an approval was granted and who granted it.

Tip

Set approval thresholds that are meaningful for your organization’s size. A $5,000 threshold for a company processing $500 million annually creates noise. A $50,000 threshold for a mid-market company may be too loose. Calibrate to your average transaction profile.

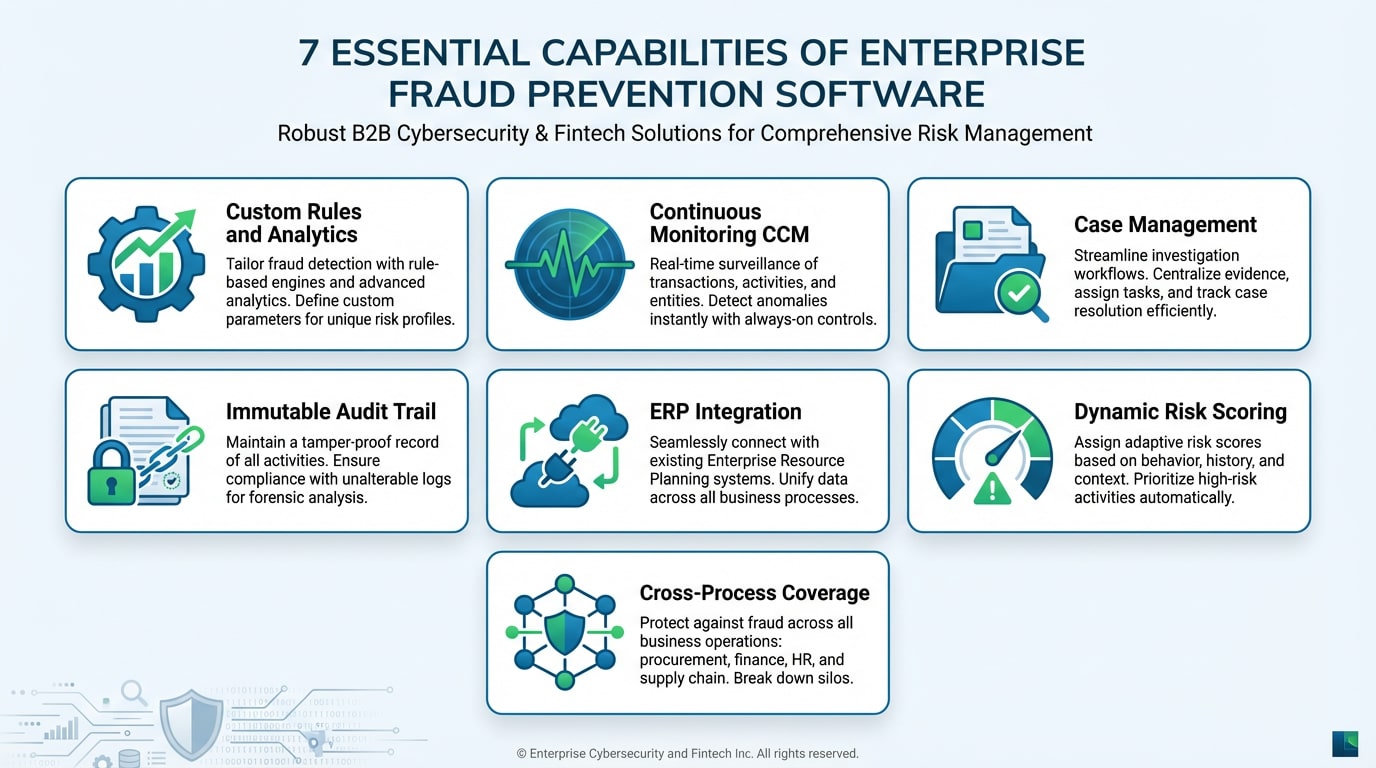

Must-Have Capabilities in Enterprise Fraud Prevention Software

When selecting an ERP fraud prevention solution, a specific set of capabilities separates an effective tool from yet another dashboard with data. Here are the key criteria to evaluate:

| Capability | Why It Is Critical |

|---|---|

| Custom rules and analytics | Every organization is different; generic rules generate noise |

| Continuous monitoring (CCM) | Quarterly sampling misses 95% of transactions |

| Case management | A finding without a follow-up process is a finding forgotten |

| Immutable audit trail | Evidence for audits, compliance, and litigation |

| Integration with existing ERP | Rapid deployment without changing existing processes |

| Dynamic risk scoring | Prioritizing findings to prevent alert fatigue |

| Cross-process coverage | Fraud crosses modules; the solution must see all of them |

Detelix meets these criteria through direct integration with ERP environments like SAP and Priority, with rapid deployment that requires no changes to the existing system. The core advantage is the ability to see the complete picture, vendors, payments, permissions, inventory, and payroll, from a single vantage point, with alerts that translate into action rather than just numbers on a screen.

ROI of Fraud Prevention: When Does the Investment Pay Off?

The numbers speak for themselves: stopping a single significant fraudulent payment, whether from a fictitious vendor, payment diversion, or duplicate payment, often covers the cost of the solution for years. But ROI is not measured solely in money saved.

Operational efficiency improves because the team stops searching for needles in haystacks. Audit readiness increases because a structured audit trail exists. Regulatory compliance strengthens because controls are documented and auditable. And most importantly, management regains genuine control over financial processes, not the perceived control that comes from reviewing monthly reports after the fact.

Did You Know

Organizations with proactive fraud prevention programs recover an average of 54% more losses compared to those that rely solely on passive detection, according to ACFE research. The cost of prevention is consistently a fraction of the cost of investigation and recovery.

What to Present in an Audit: Logs, Evidence, and Approval Trails

Internal or external auditors require proof that controls not only exist but actually function. A reliable audit trail includes: who performed the action, when, from which environment, what changed (old value vs. new value), who approved, and what the justification was if an exception occurred.

Detelix provides built-in case management where every finding is documented with anomaly details, actions taken, and the final decision. This creates an audit trail that is immediately accessible to the audit team, with no need to dig through scattered technical logs across multiple modules.

Detelix ERP Fraud Prevention Solutions

Proactive Monitoring

Continuous, automated monitoring of all ERP transactions and master data changes to detect anomalies before they result in financial loss.

Real-Time Alerts

Instant notifications on suspicious activities, permission conflicts, and policy violations with dynamic risk scoring and prioritization.

GateKeeper

Automated enforcement of Segregation of Duties policies and approval workflows that block high-risk actions before execution.

Experience

Decades of domain expertise in financial controls and ERP security, delivering tailored fraud prevention strategies for every industry.

See Detelix in Action

Frequently Asked Questions

Does Continuous Controls Monitoring replace internal audit?

No. CCM is a tool that serves internal audit, not a replacement for it. It provides auditors with real-time data, targeted findings, and complete documentation so they can focus on risk analysis and evaluation rather than manual data collection.

How long does it take to implement an ERP fraud prevention solution?

Cloud-based solutions with pre-built ERP integrations can go live within a few weeks. Detelix, for example, connects directly to your ERP environment and begins monitoring without requiring changes to existing processes or a lengthy IT project.

Is the solution relevant for mid-sized organizations, or only large enterprises?

Fraud and errors are not size-dependent. Mid-sized organizations are often more vulnerable precisely because of smaller teams and less Segregation of Duties. A modular solution allows you to start with the most sensitive processes and expand gradually.

How does ERP fraud prevention help with regulatory compliance in Israel?

Regulatory requirements such as the Privacy Protection Regulations (Data Security) mandate documentation, permission management, and ongoing controls over information repositories. An ERP fraud prevention solution generates the required infrastructure: audit trails, access monitoring, documented Segregation of Duties, and evidence that controls are functioning in practice.

What about false positives? Will the team be flooded with false alerts?

A well-designed system starts with a focused rule set and calibrates gradually. Dynamic risk scoring ensures that only high-severity anomalies reach immediate attention. In practice, teams report a significant reduction in manual review time after an initial calibration period of a few weeks.

Do You Truly Know What Is Happening Inside Your ERP Right Now?

Whether it is a bank detail change occurring at this moment, a duplicate invoice about to enter a payment run, or a permission conflict created a month ago and never addressed, the difference between reactive and proactive organizations is real-time visibility. Take control of your financial processes today.