Identify and Eliminate ERP Fraud Risks Before They Cost You

Detelix delivers continuous, real-time fraud risk assessment and monitoring for ERP environments — so your finance and audit teams stay ahead of threats, not behind them.

- What an ERP Fraud Risk Assessment Actually Means

- Why Modern Enterprises Cannot Rely on Annual Audits Alone

- The Core Components of a Credible Assessment

- High-Risk Areas Inside the ERP Ecosystem

- How Enterprise Risk Scoring Turns Findings Into Priorities

- Fraud Risk Assessment vs. Vulnerability Assessment: Drawing the Line

- Segregation of Duties: Powerful, But Not Sufficient Alone

- From Point-in-Time Reviews to Continuous Monitoring

- A Practical Step-by-Step Guide to Executing the Assessment

- Common Mistakes That Weaken Assessment Outcomes

- Mapping Business Needs to Real-Time Control Capabilities

- How to Choose a Partner for Your ERP Risk Strategy

- Measuring Whether Your Assessment Actually Worked

- Where ERP Risk Strategy Goes From Here

- Frequently Asked Questions

In many organizations, the ERP system is treated as a fortress. Approvals are configured, permissions are assigned, and reconciliations run on schedule. Yet when fraud occurs, it rarely breaks through the front door — it slips quietly through gaps that exist between processes, roles, and assumptions. An ERP fraud risk assessment is the structured way finance and risk leaders move from the illusion of control to real control. It identifies where internal or external actors could exploit weaknesses in business logic, transaction integrity, and financial exposure, and it builds the foundation for enterprise risk scoring that prioritizes what truly matters.

Key Takeaways

- An ERP fraud risk assessment maps people, processes, permissions, and transactions to identify where controls can fail in practice — not just on paper.

- Annual audits alone are insufficient; continuous monitoring closes the gap between point-in-time reviews and real-time threat detection.

- Enterprise risk scoring transforms a long list of potential issues into a prioritized, actionable plan for finance and audit leaders.

- Segregation of Duties is essential but not complete — it must be paired with anomaly monitoring, compensating controls, and regular permission reviews.

- ERP vulnerability assessments and fraud risk assessments answer different questions; mature organizations run both.

- The most impactful improvements often come from tightening permissions and adding real-time monitoring, not replacing the ERP itself.

What an ERP Fraud Risk Assessment Actually Means

An ERP fraud risk assessment is a proactive, systematic evaluation of the people, processes, permissions, and transactions inside your enterprise resource planning environment. Unlike a generic IT review, it focuses on where a control could fail in practice — not just on paper. The assessment maps how money, goods, and data move through the system, then asks where a motivated insider, a compromised account, or a manipulated workflow could cause damage before anyone notices.

The objective goes beyond basic security. It examines business logic: who can change a vendor bank account, who can approve a payment, and whether those two abilities ever intersect. The output is a quantified view of likelihood and impact that supports enterprise risk scoring and informs where to invest in stronger controls.

Tip

When scoping your assessment, map every financial flow end-to-end before reviewing individual permissions. Understanding the full transaction lifecycle first reveals toxic combinations that a permission-by-permission review will miss.

Why Modern Enterprises Cannot Rely on Annual Audits Alone

ERP systems centralize the most sensitive data an organization holds: vendor records, employee bank details, pricing logic, inventory valuations, and financial postings. That concentration makes them an attractive target — and a single point of failure when controls are weak. A traditional annual audit produces a snapshot. By the time findings are reported, fraudulent transactions may already have cleared, and the conditions that allowed them may have changed.

Continuous fraud risk evaluation in ERP closes that gap. It treats risk as dynamic, not static, and it shifts the organization from reactive review to real-time awareness. This is where Detelix’s hundreds of algorithms ensure every action in the ERP system is cross-checked against business rules and behavioral patterns, so suspicious activity is flagged before money leaves the company. Regulatory guidance reinforces this approach: institutional risk management frameworks now require ongoing risk discussions and mitigation programs rather than one-time reviews, as outlined in official guidance on cyber and information security risk management.

Did You Know

According to the Association of Certified Fraud Examiners, organizations lose an estimated 5% of revenues to fraud each year, and the median fraud scheme runs for 12 months before detection — far longer than the gap between most annual audits.

The Core Components of a Credible Assessment

A meaningful assessment is not a checklist exercise. It is a structured analysis that connects business processes to the controls and permissions that protect them. Two components carry most of the weight.

Process Mapping and Scenario Identification

Start by mapping critical financial flows: Procure-to-Pay, Order-to-Cash, Record-to-Report, and Payroll-to-Payment. For each flow, brainstorm “what-if” scenarios where a control could be bypassed — a vendor created and paid by the same user, a manual journal entry that adjusts revenue at quarter-end, a refund issued without supporting documentation. Each scenario becomes a candidate risk to score and test.

Tip

Involve frontline finance staff during process mapping sessions — they know which approval steps are routinely bypassed for speed and which compensating controls exist only in policy documents, not in practice.

Transactional Vulnerability Analysis

Next, analyze the transactions themselves. Manual journal entries, duplicate payments, round-dollar adjustments, off-hours postings, and rapid sequences of small payments below approval thresholds are all signals worth examining. This stage of ERP vulnerability assessment connects raw data to enterprise risk scoring by quantifying how often and how severely high-risk patterns appear.

High-Risk Areas Inside the ERP Ecosystem

Not all modules carry equal risk. Procurement, payroll, accounts payable, master data management, inventory, and customer refunds consistently rank highest. The reason is simple: these areas combine access to data, the ability to change it, and the authority to trigger payment or movement of value.

Master data deserves particular attention. Unauthorized changes to supplier records, employee bank details, or pricing tables are classic red-flag events because they often precede a fraudulent transaction rather than appearing as one. The dangers of changing bank account details in ERP systems illustrate how a single quiet edit can redirect significant payments before reconciliation catches it.

Did You Know

Master data changes — particularly supplier bank account updates — account for a disproportionate share of large-value ERP fraud cases. Many of these changes are made by authorized users, making behavioral context the only reliable detection signal.

How Enterprise Risk Scoring Turns Findings Into Priorities

Enterprise risk scoring transforms a long list of potential issues into a ranked action plan. The common methodology combines impact, likelihood, and control weakness into a single score, often expressed as (Impact × Likelihood) + Control Weakness. A risk with high financial impact, broad user exposure, and weak detection capability rises to the top; a low-impact risk in a tightly controlled process can be accepted or monitored.

Scoring matters because resources are finite. CFOs and risk leaders need to know where to invest first. Continuous monitoring then feeds dynamic scores that adjust as user behavior, organizational structure, and transaction volumes evolve — so the priority list reflects today’s risk, not last year’s.

Tip

When building your scoring model, weight “control weakness” heavily for processes where no automated monitoring exists. A weak manual control on a high-impact process is far more dangerous than a strong automated control on a lower-impact one.

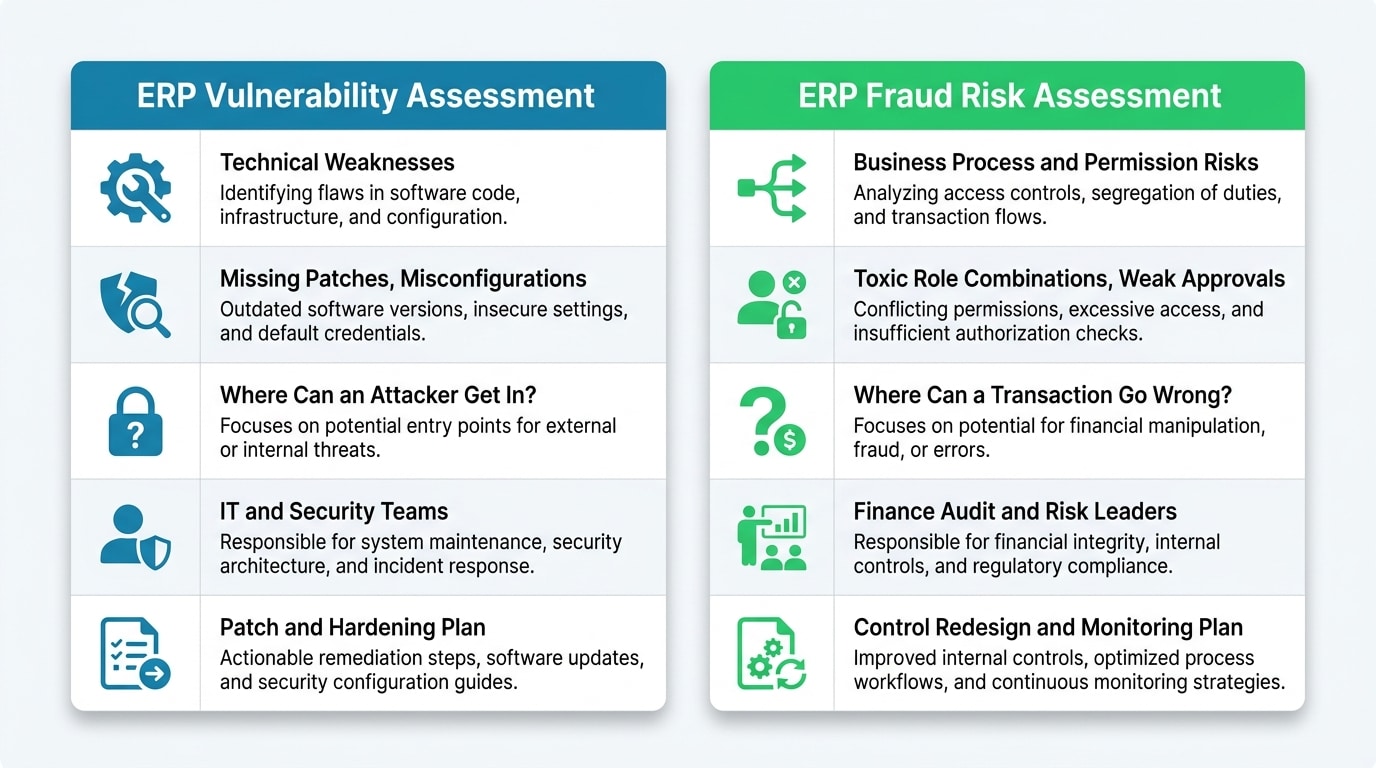

Fraud Risk Assessment vs. Vulnerability Assessment: Drawing the Line

These two terms are often confused, but they answer different questions. An ERP vulnerability assessment looks at the technical surface — patches, configurations, exposed ports, weak credentials, and software bugs. It asks: where is the door unlocked? A fraud risk evaluation in ERP looks at behavior inside the room: who can do what, in what sequence, and with what oversight.

Consider a practical contrast. An unpatched server is a vulnerability. An authorized user who can create a vendor, approve an invoice, and release a payment without a second pair of eyes is a fraud risk. Mature organizations run both assessments because each answers a question the other cannot.

| Dimension | ERP Vulnerability Assessment | ERP Fraud Risk Assessment |

|---|---|---|

| Primary focus | Technical weaknesses | Business process and permission risks |

| Typical findings | Missing patches, misconfigurations | Toxic role combinations, weak approvals |

| Key question | Where can an attacker get in? | Where can a transaction go wrong? |

| Owner | IT and security teams | Finance, audit, and risk leaders |

| Output | Patch and hardening plan | Control redesign and monitoring plan |

Your ERP holds your most sensitive financial data. Are your controls actually keeping pace with the risks inside it?

Segregation of Duties: Powerful, But Not Sufficient Alone

Segregation of Duties (SoD) is one of the most effective controls in any ERP environment. The principle is simple: no single user should control every stage of a sensitive transaction. When the same person can create a vendor, post an invoice, and approve a payment, the conditions for fraud are already in place. In complex ERPs, “toxic combinations” of permissions often hide deep within composite roles, accumulating quietly as employees change positions.

Regulatory guidance from professional accounting bodies confirms that segregation of duties is designed specifically to reduce the risk of errors, irregularities, and embezzlement, as described in official information technology examination materials. Still, SoD alone is not a complete defense. It must be paired with anomaly monitoring, compensating controls, and periodic reviews of who actually holds which permissions today.

Did You Know

In many ERP environments, over 30% of identified SoD conflicts involve permissions inherited through composite roles that were never reviewed after initial setup. Users often accumulate access across role changes without anyone removing prior permissions.

From Point-in-Time Reviews to Continuous Monitoring

Periodic assessments tell you what was true on the day of the review. They cannot tell you what is happening right now. Modern fraud schemes exploit exactly that gap: a small permission change made on Monday, a vendor bank update on Wednesday, a payment released on Friday. A quarterly review will not catch that sequence.

Continuous monitoring uses business rules, behavioral analytics, and machine learning to watch sensitive ERP processes as they happen. It compares each action against expected patterns — who normally performs it, when, against which counterparties, and at what amounts. This is where Detelix’s platform supports finance and audit teams by scanning for suspicious changes in payment details and other sensitive activities before they translate into financial loss. The shift is from reviewing reports after the fact to actually controlling the process while it is running.

Tip

When transitioning from periodic reviews to continuous monitoring, start with the three highest-impact processes identified in your last assessment. Build alerting and response workflows for those first — then expand coverage incrementally rather than attempting to monitor everything at once.

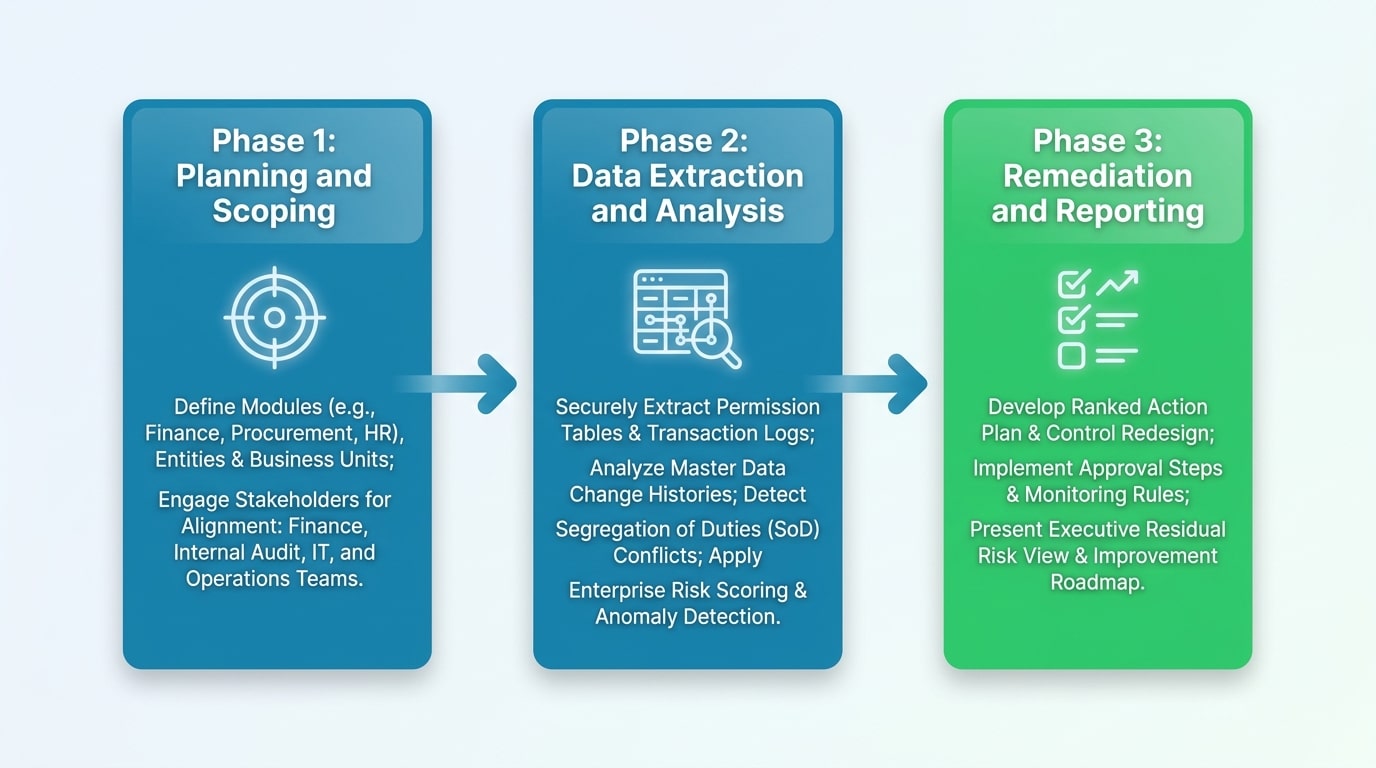

A Practical Step-by-Step Guide to Executing the Assessment

Phase 1: Planning and Scoping

Define which modules, entities, and processes are in scope. Prioritize areas with the highest financial exposure or recent change — newly implemented modules, post-merger integrations, or processes flagged in prior audits. Align stakeholders from finance, internal audit, IT, and operations on objectives and timeline.

Phase 2: Data Extraction and Analysis

Pull permission tables, transaction logs, master data change histories, and approval records. Run analytics to identify SoD conflicts, unusual transaction patterns, dormant accounts with active permissions, and master data changes lacking proper authorization. This is where enterprise risk scoring takes shape.

Phase 3: Remediation and Reporting

Translate findings into a prioritized action plan. Each finding should map to a control: redesign a role, add an approval step, implement a monitoring rule, or accept the risk with documented justification. Reporting should give executives a clear view of residual risk after remediation.

Common Mistakes That Weaken Assessment Outcomes

Even well-funded assessments fail when they fall into predictable traps. The first mistake is treating the exercise as a compliance checkbox rather than a business protection effort. The second is producing a “data dump” of thousands of low-context findings that overwhelm rather than inform. The third is ignoring compensating controls — a permission conflict on paper may already be mitigated by an effective monitoring rule, and a real conflict may exist where no exception report is reviewed.

The fourth mistake is failing to revisit the assessment. Organizations change. New modules are added, employees move between roles, approval thresholds shift. An assessment that is not refreshed becomes a historical document rather than a control instrument.

Did You Know

Research on internal control failures consistently finds that the controls most likely to be bypassed are manual ones performed by a single reviewer under time pressure — precisely the controls that appear strongest on paper during annual audits.

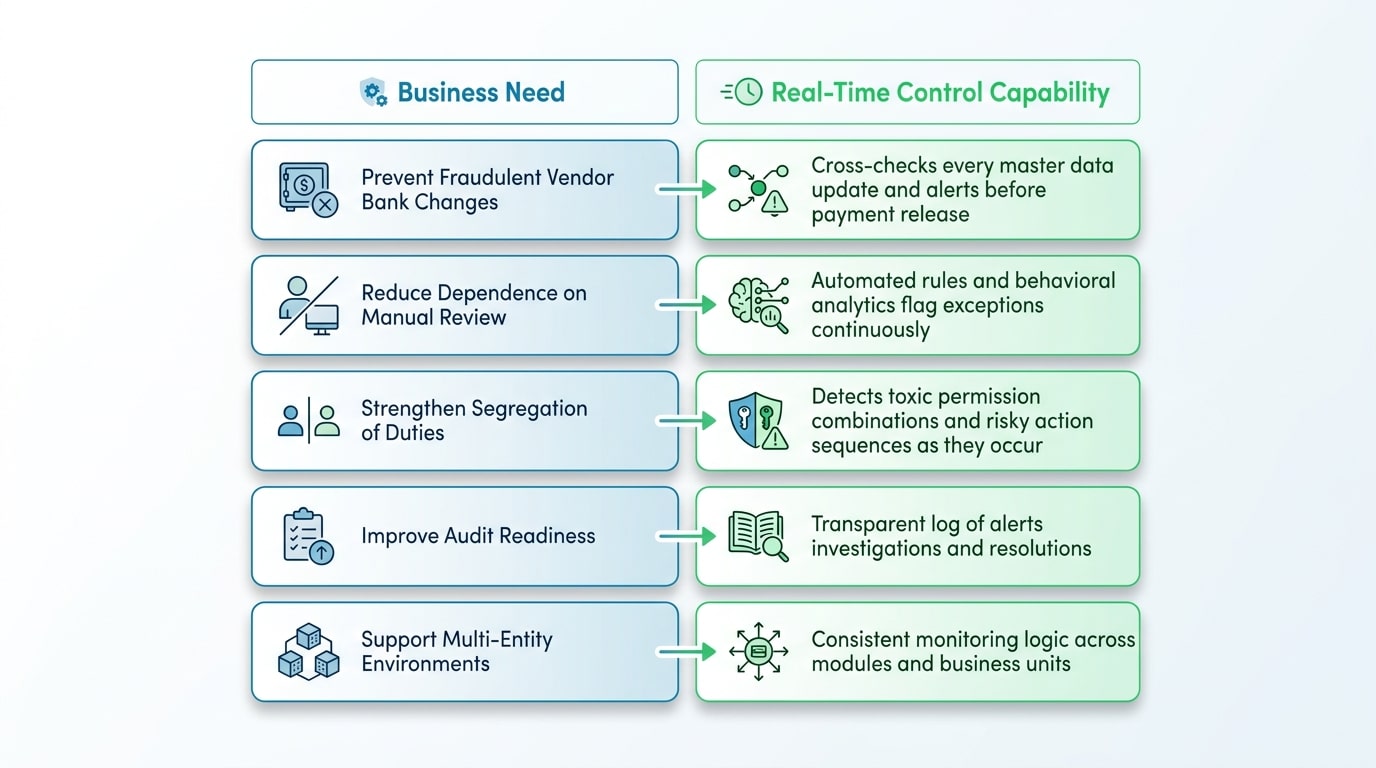

Mapping Business Needs to Real-Time Control Capabilities

One of the most useful exercises during an assessment is connecting each identified risk to a concrete protective capability. The table below illustrates how common business needs translate into the kind of continuous, real-time control that a platform like Detelix provides — without replacing the ERP itself.

| Business Need | How a Real-Time Control Layer Helps |

|---|---|

| Prevent fraudulent vendor bank changes | Cross-checks every master data update against verified sources and alerts before payment release |

| Reduce dependence on manual review | Automated rules and behavioral analytics flag exceptions continuously, not only at month-end |

| Strengthen segregation of duties | Detects toxic permission combinations and risky action sequences as they occur |

| Improve audit readiness | Maintains a transparent log of alerts, investigations, and resolutions for reviewers |

| Support multi-entity environments | Applies consistent monitoring logic across modules and business units in Israel and abroad |

Tip

Use the business-need-to-control mapping exercise as a communication tool with your CFO or audit committee. Translating technical findings into business language — “this prevents us from paying a fraudulent vendor” — drives faster approval and resource allocation for remediation.

How to Choose a Partner for Your ERP Risk Strategy

Selecting an evaluation partner is itself a control decision. Look for teams that understand both business processes and deep ERP architecture — not one without the other. A strong partner asks about your procurement workflow before asking about your database version. They build realistic fraud scenarios specific to your industry, not generic templates.

Equally important, the partner should deliver actionable remediation, not only findings. A report that ranks 800 issues without context is not useful. A report that identifies the 20 highest-impact risks, explains the business consequence, and proposes specific control changes is the deliverable that finance and audit leaders can act on.

Measuring Whether Your Assessment Actually Worked

An assessment is only valuable if it changes outcomes. Useful indicators include the number of high-risk SoD conflicts resolved, the reduction in master data changes lacking dual approval, the time from anomaly detection to investigation, and the percentage of payments reviewed by automated rules before release. Tracking these metrics over time turns enterprise risk scoring into a living KPI for finance and security departments.

Organizations that adopt this discipline gain something beyond fewer incidents: they gain executive confidence. Leaders can answer the difficult question — “How exposed are we, really?” — with evidence rather than assumption.

Where ERP Risk Strategy Goes From Here

An ERP fraud risk assessment is a journey, not a destination. The systems change, the people change, and so do the threats. What endures is the discipline of mapping risk to controls, scoring what matters, and monitoring continuously. Treat enterprise risk scoring as a standard metric, refresh your fraud risk evaluation in ERP after every material change, and pair point-in-time reviews with real-time visibility. That combination is what separates organizations that manage activity from those that actually control it.

If your organization relies on ERP for sensitive financial processes, the question is no longer whether to perform a fraud risk assessment — it is how quickly you can pair it with continuous, real-time control. Want to see how Detelix helps finance, audit, and risk leaders detect exceptions before damage occurs? Get in touch with our team to discuss your ERP environment and the controls that matter most to your business.

Detelix ERP Fraud Prevention Solutions

Proactive Monitoring

Continuously monitors ERP activity against hundreds of business rules to detect suspicious behavior before financial damage occurs.

Real-Time Alerts

Delivers instant notifications when high-risk transactions, master data changes, or permission anomalies are detected in your ERP system.

Gatekeeper

Intercepts sensitive ERP actions — including vendor bank updates and payment releases — for verification before they execute.

Deep ERP Expertise

Backed by decades of ERP architecture and financial process knowledge, Detelix translates complex risks into clear, prioritized controls.

See Detelix ERP Fraud Prevention in Action

Frequently Asked Questions

What is the difference between a standard audit and a fraud risk evaluation in ERP?

A standard audit verifies that controls exist and produces an opinion at a point in time. A fraud risk evaluation in ERP focuses specifically on where fraud could occur, examines toxic permission combinations and transaction patterns, and produces a prioritized risk score with specific remediation steps. The two are complementary, not interchangeable.

How often should an enterprise risk scoring update occur?

At minimum, annually. In practice, scoring should be refreshed after any material change — a new module, a reorganization, a merger, a significant permission redesign, or a notable incident. Continuous monitoring tools update underlying signals daily, so the formal score is always based on current data.

Can we perform an ERP vulnerability assessment without disrupting operations?

Yes. Most assessments rely on read-only data extraction from logs, permission tables, and transaction histories. Active testing is scheduled with IT and typically conducted in non-production environments or during low-activity windows. A well-planned assessment should not interrupt business operations.

Does Segregation of Duties count as a full ERP fraud risk assessment?

No. SoD analysis is a critical component, but it covers only one dimension — who can do what. A full assessment also examines transaction patterns, master data changes, approval workflows, exception monitoring, and compensating controls. Treating SoD as the entire program leaves significant blind spots.

Can we improve fraud controls without replacing our ERP?

In most cases, yes. The greatest gains usually come from tightening permissions, redesigning approval flows, adding real-time monitoring, and strengthening master data governance. Replacing an ERP is rarely the right answer to a control problem; the configuration and oversight around the system matter far more than the system itself.

How long does an ERP fraud risk assessment typically take?

For a mid-sized organization with defined processes, a focused assessment can be completed in a few weeks. For global enterprises with multiple entities, complex permissions, and many integrations, the work may extend to several months and include phased remediation. Scope, data availability, and stakeholder engagement drive the timeline more than company size alone.

Who should own the ERP fraud risk assessment internally?

Ownership is usually shared. Finance and internal audit drive the business risk perspective, IT provides system access and technical context, and risk leadership coordinates priorities. Executive sponsorship from the CFO or CRO ensures findings translate into action rather than sitting in a report.

Ready to Move From Reviewing Risk to Controlling It?

Pair your next ERP fraud risk assessment with continuous, real-time detection. Detelix helps finance, audit, and risk leaders catch exceptions before damage occurs — across every module, entity, and process that matters to your business.