Turn ERP Fraud Case Studies Into Real Protection

Detelix gives finance, audit, and IT leaders continuous, real-time oversight of sensitive ERP processes — before losses happen.

- What Are ERP Fraud Case Studies?

- How Fraud Occurs Inside an ERP

- Real ERP Fraud Examples and Patterns

- Lessons From Major Enterprise Fraud Incidents

- Why Corporate Fraud Through ERP Goes Undetected

- Early Warning Signs and Red Flags

- Journal Entry Fraud Inside an ERP

- Comparison of ERP Fraud Risks and Controls

- ERP Fraud vs Accounting Fraud vs Payment Fraud

- Building a Prevent–Detect–Respond Framework

- How Detelix Supports Real Control

- Practical Checklist for Finance and Audit Leaders

- Frequently Asked Questions

In many organizations, financial controls look strong on paper. There are approval flows, ERP permissions, reconciliations, and review procedures. Yet when the damage is finally discovered, the same pattern emerges: the fraud was hidden inside routine activity that nobody stopped in time. ERP fraud case studies have become essential reading for CFOs, controllers, and internal auditors because they reveal how ordinary transactions become instruments of loss, how control environments fail silently, and how real-time protection approaches help organizations move from the illusion of control to actual control over sensitive ERP processes.

Key Takeaways

- ERP fraud almost always hides inside routine, approved activity — not obvious anomalies.

- The most damaging schemes exploit master data changes, excessive privileges, and weak journal entry oversight.

- Periodic audits detect fraud too late; continuous, cross-module monitoring is what shortens the damage window.

- Strong controls combine prevention, detection, and response — no single layer is enough.

- Most ERP fraud can be prevented without replacing the ERP, by adding a continuous protective layer over sensitive processes.

What Are ERP Fraud Case Studies and Why Do Organizations Need Them?

An ERP fraud case study is a post-mortem analysis of a fraudulent event in which the ERP system was the stage, the weapon, or the point of failure. It is not a story about software defects; it is a story about how permissions, workflows, master data, and journal entries were used to move money or distort financial reporting. Organizations seek these studies because they want patterns, not headlines: which controls failed, how the scheme was concealed, and what would have detected it earlier.

The search intent behind corporate fraud through ERP is informational. Finance and audit leaders want to map enterprise fraud incidents to their own processes and ask a harder question: could this happen here, and would we see it in time? According to the ACFE 2016 Report to the Nations, understanding how occupational fraud is committed and concealed is the first step toward effective detection.

Tip

When reading any ERP fraud case study, rewrite the incident in your own process language: which of your roles, which of your modules, which of your approvers. If any step reads “we don’t do it that way,” challenge it — that’s usually where the real gap sits.

How Does Fraud Actually Occur Inside an ERP Environment?

ERP systems do not create fraud. They enable it when controls are weak, permissions are excessive, or monitoring is retrospective. The most damaging schemes look like legitimate activity: a new vendor, an approved invoice, a routine payment, a year-end journal entry. The fraud lives inside the normal, which is exactly why manual review rarely catches it in time.

Manipulation of Vendor Master Data and Payments

A common pattern is the quiet modification of an existing vendor — a change of bank account, a slight shift in remittance details — followed by a single payment that appears perfectly ordinary. Shell companies are another variant, created inside the vendor master file and activated through low-value invoices that grow over time. Even minor edits can bypass standard payment workflows when no one cross-checks them. For finance teams reviewing exposure here, the dangers of changing bank account details in ERP systems illustrate how a single unauthorized change can redirect funds before any approver notices.

Exploiting Excessive Privileges and Broken Segregation of Duties

When one user can create a vendor, approve an invoice, and release a payment, the organization has effectively removed the most basic fraud barrier. Privileged and admin accounts used for routine activity compound the risk, because their actions are rarely scrutinized. The GAO Internal Control Management and Evaluation Tool identifies segregation of duties as a core fraud-reduction control and a validity check on transactions.

Manipulating or Hiding Traces in System Logs

When logs are disabled, truncated, or never reviewed, the audit trail collapses. Investigators cannot reconstruct who changed what and when, and the fraud can continue unchallenged. A control environment without reliable logs is not a control environment — it is a reporting environment.

Did You Know

The ACFE Report to the Nations consistently shows that the median occupational fraud scheme runs for 12 to 18 months before detection — and schemes involving management or collusion tend to last even longer and produce materially larger losses.

Real ERP Fraud Examples: the Patterns Worth Recognizing

Rather than memorizing individual scandals, leaders benefit more from recognizing recurring patterns. The most instructive real ERP fraud examples fall into a few repeatable categories, and each one maps to a specific control gap that finance teams typically prioritize when strengthening oversight.

Procure-to-Pay fraud often starts with collusion between a buyer and a vendor, where invoices are inflated or duplicated inside an otherwise legitimate purchasing flow. Payroll fraud frequently involves ghost employees added to the HR or payroll module, with salaries routed to controlled bank accounts. Inventory fraud hides physical theft behind system adjustments — write-offs, reclassifications, or “damaged goods” entries that never existed. Each case looks clean inside a single transaction; the signal only emerges when you compare thousands of actions over time. This is where cracking hidden errors, frauds, and sophisticated manipulations becomes a question of continuous cross-checking rather than sampling.

Lessons From Major Enterprise Fraud Incidents

Large-scale enterprise fraud incidents rarely stem from a single technological failure. They reveal a hybrid breakdown: weak governance, excessive trust in tenured employees, siloed oversight, and a culture that tolerates workflow bypasses in the name of efficiency. Trust is not a control. The people closest to the process often have the deepest knowledge of its blind spots.

The ACFE 2014 Global Fraud Study shows that internal control weaknesses contribute to nearly half of all occupational fraud cases. The lesson is consistent: fraud develops over time, exploits a chain of small weaknesses, and is rarely stopped by the same approval layers it learned to navigate.

Tip

Identify the three people in your organization whose actions are almost never challenged. Build a specific monitoring policy for their activity in the ERP. High-trust users are not higher-risk because of intent — they are higher-risk because their actions are rarely reviewed.

Why Does Corporate Fraud Through ERP Go Undetected for Years?

Detection delays are not accidental — they are structural. Alert fatigue trains teams to dismiss exceptions. The silo effect leaves IT managing permissions while Finance manages payments, with neither side looking at cross-functional data. And when workflow bypasses become normalized for “efficiency,” a fraudster simply hides among the efficient bypassers.

Three additional factors extend the lifespan of corporate fraud through ERP: scattered data across modules, rare manual spot-checks, and no clear ownership of exception follow-up. The result is a long gap between the first suspicious action and the moment someone connects the dots — usually after significant damage.

Did You Know

Most organizations discover internal fraud through tips rather than controls — meaning the system that was supposed to prevent the fraud was not the one that caught it. Continuous monitoring shifts detection back into the control environment where it belongs.

Early Warning Signs: Practical Red Flags for ERP Fraud

Red flags become useful only when they are operational — things a team can check this week, not abstract risk categories. The most valuable indicators live at three levels: the user, the transaction, and the master data.

User-Level Indicators

Logins outside working hours, shared account usage, repeated access to unrelated modules, and manual overrides that leave no explanation. These behaviors rarely prove fraud on their own, but in combination they warrant immediate review.

Transactional-Level Indicators

Round-number invoices, payments split just below approval thresholds, frequent reversals, vendor changes made shortly before payment, and unusually fast approvals without supporting documentation.

Master Data Indicators

Vendors sharing bank accounts with employees, multiple vendors created within a short window for the same service, or repeated edits to remittance details. The PCAOB Audit Focus on Journal Entries similarly flags unusual or unauthorized entries, particularly around period-end, as persistent fraud indicators.

Every week your ERP runs without continuous oversight is another week suspicious vendor changes, split payments, and questionable journal entries can slip through unnoticed.

How Journal Entry Fraud Looks Inside an ERP

Journal entries are the final frontier for fraudsters who need to balance the books after moving cash. Inside an ERP, a fraudulent entry often looks identical to a legitimate one: a manual posting, a vague description, a familiar account. What distinguishes it is the pattern — reversals that clear a balance while the cash is already gone, period-end adjustments with no supporting documentation, or unusual accounts touched only once a year.

Manual journal entries with sparse metadata, posted by users who rarely work in that module, deserve automatic scrutiny. Continuous monitoring of posting behavior — not just amounts — is what separates detection from discovery-after-the-fact.

Tip

Run a quarterly report filtering for manual journal entries posted in the last five business days of any period, by users who post fewer than five entries per year. This single query surfaces a disproportionate share of the most suspicious postings.

Comparison: Sources of ERP Fraud Risk and Where Controls Fail

The table below maps common fraud patterns to the modules involved, the control that typically fails, and the recommended detective or preventive response. It is designed as a working reference, not a marketing comparison.

| Fraud Type | How It Happens | Module | Early Warning Sign | Failed Control | Recommended Control |

|---|---|---|---|---|---|

| Fictitious vendor | Shell company added to master file | Vendor Master / AP | New vendor, low-value invoices | Master data review | Independent vendor verification |

| Bank detail change | Remittance redirected before payment | Vendor Master | Bank edit close to payment date | Change control | Out-of-band verification |

| Duplicate payments | Same invoice paid twice | Accounts Payable | Matching amounts, close dates | Three-way match | Automated duplicate detection |

| Ghost employee | Fake record in payroll | HR / Payroll | No tax ID, shared bank account | HR-to-payroll reconciliation | Cross-check of active employees |

| Journal entry manipulation | Manual posting to conceal theft | General Ledger | Period-end entries, vague descriptions | JE review | Continuous JE monitoring |

| SoD bypass | One user performs full cycle | All transactional modules | Single-user approvals | Role design | Role-based access with conflict detection |

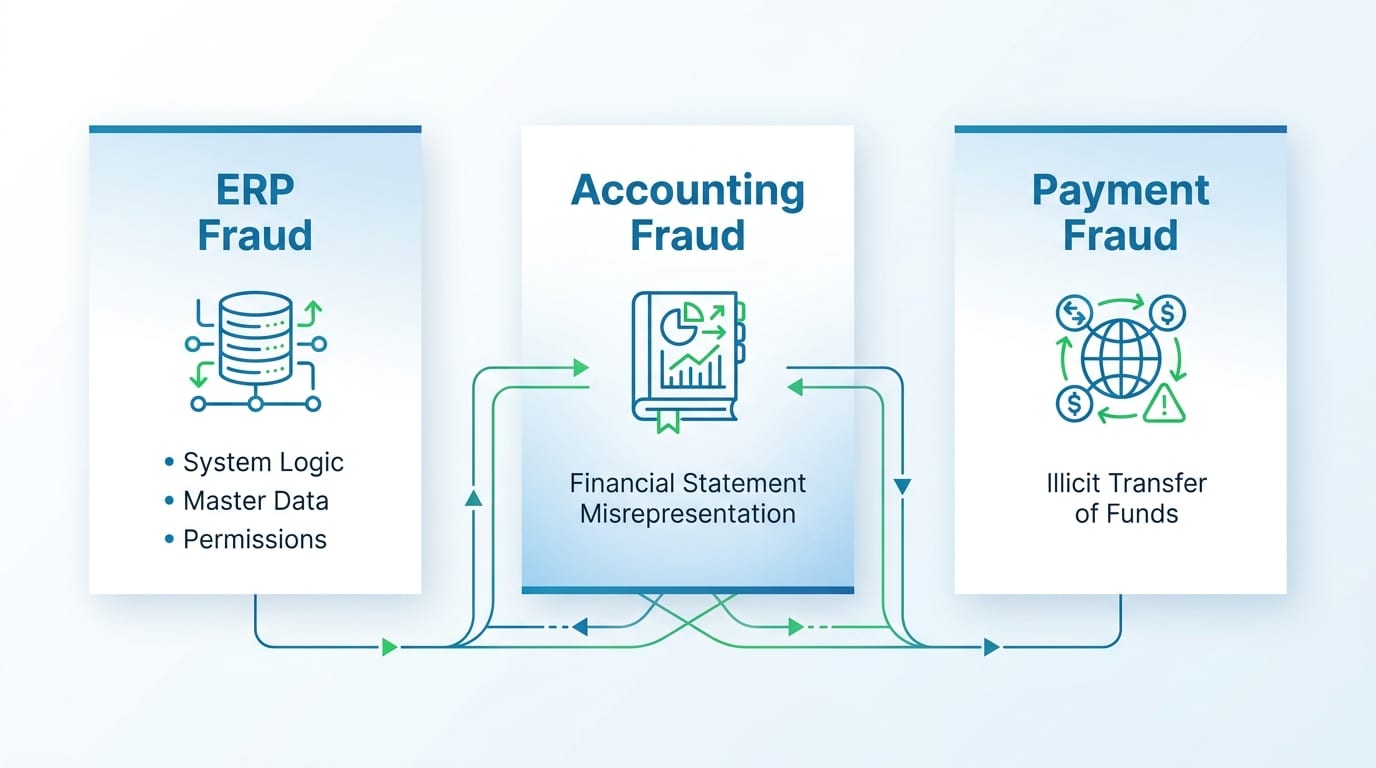

Differentiating ERP Fraud, Accounting Fraud, and Payment Fraud

These terms overlap in practice but describe different layers. ERP fraud focuses on the system’s logic, master data, and permissions — the how. Accounting fraud focuses on the misrepresentation of financial statements — the why. Payment fraud focuses on the actual illicit transfer of funds — the result. A single incident frequently involves all three, which is why oversight that monitors only one layer leaves the others exposed.

A platform like Detelix is designed to bridge these layers by cross-checking activity across master data, transactions, and postings in real time, so an anomaly in one layer is evaluated against behavior in the others before the payment leaves the organization.

Did You Know

Regulatory frameworks such as SOX and ISO standards increasingly expect organizations to demonstrate not only that controls exist, but that they are continuously monitored and that exceptions are documented and resolved — shifting the bar from “control design” to “control operation.”

Building a Prevent–Detect–Respond Framework

Effective control environments do not rely on a single line of defense. They combine three reinforcing layers that work together across sensitive ERP processes.

Preventive controls include hard-coded segregation of duties, multi-layer approvals, and validation rules on master data. Detective controls include continuous anomaly monitoring, exception reporting, and regular vendor and user access reviews. Response readiness includes preserved audit trails, documented investigation procedures, and clear ownership of exception closure. The NIST Privileged Account Management fact sheet reinforces that monitoring privileged activity is essential for responding quickly to internal threats — a principle that applies equally to ERP super-users.

Tip

For every detective control you add, define in advance who owns the exception, how fast it must be closed, and what happens if it isn’t. Detection without ownership produces alert backlogs, not protection.

How Detelix Supports Real Control Across Sensitive ERP Processes

Rather than replacing existing ERP controls, Detelix adds a continuous protective layer over them. The table below maps common business needs to the way this approach works in practice.

| Business Need | How Continuous Protection Helps in Practice |

|---|---|

| Visibility into sensitive changes | Real-time alerts on vendor bank detail edits, privileged actions, and master data changes |

| Detection of anomalies across modules | Cross-checks between procurement, AP, HR, and GL data instead of siloed review |

| Reduced dependence on manual sampling | Automated scanning of every transaction rather than periodic audits |

| Investigation readiness | Preserved, structured audit evidence for internal audit and forensic review |

| Fit for organizations operating in Israel and abroad | Configurable controls aligned with local process and regulatory context |

| Faster response before money leaves | Alerts generated while the transaction is still in the approval window |

Did You Know

Many organizations discover, after deploying continuous ERP monitoring, that the majority of initial alerts are not fraud at all — they are process errors, unauthorized shortcuts, and stale access rights. Cleaning these up tightens the control environment before any fraud attempt occurs.

A Practical Checklist for Finance, Audit, and IT Leaders

The recurring lesson from ERP fraud case studies is that proactive monitoring costs far less than reactive recovery. A focused action list helps translate insight into control.

This month: review SoD conflicts by role and user; scan for duplicate or near-duplicate vendors; audit every action taken by super-user accounts; verify that audit logs are active and retained; and confirm that bank detail changes trigger independent verification before any payment is released. These steps do not require a system replacement — they require a shift from periodic review to continuous, automated oversight.

Tip

Start with the one process where a single successful fraud would cause the largest financial or reputational damage. Secure that process with continuous monitoring first, then expand. Scope creep kills ERP control initiatives more often than budget ever does.

Detelix Protection for Sensitive ERP Processes

Proactive Monitoring

Continuous oversight of master data, transactions, and journal entries — catching anomalies before they become losses.

Real-Time Alerts

Immediate notifications on sensitive changes — vendor bank details, privileged actions, split payments, and more.

ERP Gatekeeper

A continuous protective layer over your existing ERP — enforcing segregation of duties and stopping high-risk transactions in time.

Proven Experience

Years of hands-on expertise protecting sensitive ERP environments for organizations operating in Israel and abroad.

Frequently Asked Questions

What are the red flags for a vendor bank account change?

Requests arriving by email only, urgency around an upcoming payment, domains that look similar but are not identical, and changes made shortly before a scheduled remittance. FBI guidance on Business Email Compromise recommends verifying every change through a trusted, independent channel.

Can segregation of duties really be bypassed?

Yes. The most common bypass is management override, where a senior user approves their own action or pressures others to do so. Temporary access grants that are never revoked, and emergency approvals used for routine work, are equally risky.

How long does the average ERP-related fraud last?

ACFE data across editions consistently shows that occupational fraud runs for roughly 12 to 18 months before detection. Schemes involving executives or collusion tend to last longer, which is why continuous monitoring matters more than annual review cycles.

What is the difference between fraud in the ERP and an operational error?

Intent is the legal distinction, but operationally the patterns differ: errors are usually random and visible in reconciliation, while fraud is deliberate, repeated, and structured to avoid detection. Both require control — but fraud requires continuous cross-checking.

How is journal entry fraud typically detected in internal audit?

Through analysis of entries posted at period-end, manual entries with vague descriptions, entries made by users outside their normal module, and reversal patterns that clear balances without operational justification.

Which ERP processes are most exposed to fraud risk?

Procure-to-pay, vendor master data maintenance, payroll, bank reconciliation, inventory adjustments, customer refunds, and manual journal entries. These are the processes where sensitive value moves and where control breakdowns cause the largest losses.

Can corporate fraud through ERP be prevented without replacing the system?

Yes. Most fraud losses are enabled by weak controls around the ERP, not by the ERP itself. A continuous protection layer that monitors transactions, master data changes, and privileged activity strengthens control without disrupting existing operations.

Ready to Move From Routine Monitoring to Real Control?

Would you see a suspicious vendor change, a split payment, or an unusual journal entry in time to stop it? Let’s find out together.