Stop ERP Fraud Before It Reaches Your Bank Account

Continuous, real-time protection across vendors, payments, permissions, and master data. Talk to a Detelix specialist today.

- Understanding What Defines ERP Fraud

- The Most Common types of ERP fraud

- ERP system vulnerabilities and Technical Weaknesses

- Internal Controls as the Barrier Against Fraud

- Master Data Risks and Bank Detail Changes

- How to Identify ERP Fraud Red Flags

- Mapping Fraud Types to Processes and Controls

- The Financial Impact of Duplicate Payments

- Internal Fraud Versus External Fraud in ERP

- Strategic ERP Fraud Prevention and Auditing

- How Real-Time Monitoring Changes the Equation

- Common Mistakes That Weaken ERP Fraud Defenses

- Strengthening the ERP Control Environment

- Frequently Asked Questions

In many organizations, the ERP system is the operational heart of the business. It processes payments, manages vendors, controls inventory, calculates payroll, and holds the financial data that leadership depends on every day. But because so much value flows through this single environment, it has also become one of the most attractive targets for fraud. When a process depends too heavily on routine approvals, static permissions, or after-the-fact reporting, risk can slip through unnoticed. Understanding the different types of ERP fraud, the ERP system vulnerabilities that enable them, and the ERP fraud risks associated with modern finance operations is the first step toward real control. The scale of the problem is significant — FinCEN reports its Rapid Response Program has interdicted nearly $2 billion on behalf of U.S. cyber-enabled fraud victims, much of it tied directly to business payment workflows.

Key Takeaways

- ERP fraud spans fictitious vendors, invoice manipulation, duplicate payments, master data tampering, and access abuse — each tied to a specific process inside the system.

- Most damaging schemes exploit legitimate credentials and weak segregation of duties, making activity appear authorized until funds have already moved.

- Master data changes, especially bank detail updates just before payment runs, are among the highest-impact fraud vectors and require out-of-band verification.

- Periodic audits and approval workflows alone are insufficient; continuous, real-time monitoring is what closes the gap between detection and loss prevention.

- A structured control framework — mapping each fraud type to its process, warning sign, and preventive control — turns scattered defenses into measurable protection.

Understanding What Defines ERP Fraud

ERP fraud is the manipulation of data, processes, or authorizations inside an enterprise resource planning system to gain an unauthorized financial benefit. It may involve an insider, an external attacker, or a combination of both. The broader category includes common ERP fraud schemes, ERP abuse, and ERP control failures — situations where the system technically functions but the surrounding controls fail to prevent damage. For finance leaders, detecting hidden risks within complex ERP systems requires distinguishing between three overlapping phenomena: honest operational errors, policy abuse that exploits loose controls, and intentional fraud. All three drain profitability, but only real-time visibility into transactions and master data changes allows organizations to separate them quickly and act before losses compound.

Tip

Document every ERP fraud incident — even the small ones — with the process, role, and control that failed. Over twelve months, this becomes the most reliable map of where your real exposure lives.

The Most Common types of ERP fraud

Most ERP fraud falls into a small number of repeatable patterns. Recognizing them by category helps finance, audit, and operations leaders map each risk to the specific process, module, and control that should stop it. The sections below describe the schemes that appear most often in real investigations.

Vendor and Supplier Fraud Schemes

Fictitious vendors remain one of the most damaging vendor fraud in ERP patterns. An employee with access to supplier master data — or an external actor using a compromised account — creates a shell entity, issues invoices, and diverts payments. ERP vendor setup fraud often succeeds because the new vendor passes routine checks while supplier impersonation mimics an existing trusted relationship. Organizations that focus on performing essential supplier verification before the first payment close the window during which these schemes do the most damage.

Did You Know

FinCEN’s Rapid Response Program has recovered nearly $2 billion on behalf of U.S. victims of cyber-enabled business payment fraud — the majority linked to fraudulent vendor and beneficiary instructions processed through routine payment workflows.

Invoice and Payment Manipulation

Invoices can be inflated, duplicated, slightly altered, or rerouted to unauthorized bank accounts. Invoice fraud in ERP frequently involves changes made between approval and payment, leaving reviewers convinced the transaction is legitimate. ERP payment fraud and ERP invoice manipulation are also driven externally through email compromise and social engineering. USAID OIG has specifically warned about diversion of electronic funds to false bank accounts and recommends independent telephone verification for any change in beneficiary details.

ERP system vulnerabilities and Technical Weaknesses

Technology choices shape how easily an attacker — insider or external — can operate. Modern ERP environments are highly integrated, which means a weakness in one connected system can expose the entire financial process. ERP security risks multiply when integrations, logs, and configurations are not monitored continuously.

Critical Flaws in Modern ERP Architectures

Integration and API vulnerabilities allow transactions to enter the ERP through paths that bypass normal approval flows. Unmonitored audit trails are equally dangerous — logs that nobody reviews can be ignored, overwritten, or manipulated to hide ERP data tampering. A GAO report on financial management identifies deficiencies in logical access controls, configuration management, segregation of duties, and processing controls as recurring drivers of fraud and error risk. These ERP audit trail issues are not theoretical; they are the mechanisms through which fraud becomes undetectable until the money has already left the organization.

Tip

Inventory every system that posts transactions into your ERP — including RPA bots, EDI feeds, and third-party APIs. Any path that can write data must be monitored with the same rigor as a human user.

Internal Controls as the Barrier Against Fraud

Strong controls are what separate a well-run ERP from a vulnerable one. The point is not to add friction but to ensure that no single person or process can act without independent verification.

The Role of Segregation of Duties

A person who can create a vendor, submit an invoice, and authorize payment in the same system holds the full toolkit for fraud. Segregation of duties in ERP exists to prevent exactly that concentration. GAO’s internal control evaluation guidance stresses the importance of separating authorization, processing, payment, review, and custody functions — a principle that directly drives fraud prevention in procurement and payables.

Addressing Overprivileged Users and Role Conflicts

Least privilege is a simple idea: users should have only the access required for their role, and nothing more. In practice, user role conflicts accumulate over time as employees change jobs, projects end, and legacy permissions are never revoked. NIST’s assessment of access control systems explains how role-based and attribute-based models reduce these risks when paired with periodic reviews, making strong ERP access controls and well-designed ERP internal controls indispensable.

Did You Know

Most large ERP environments contain dozens of unresolved segregation-of-duties conflicts inherited from past role changes. These latent conflicts often remain invisible until a single user with accumulated privileges becomes the center of a fraud case.

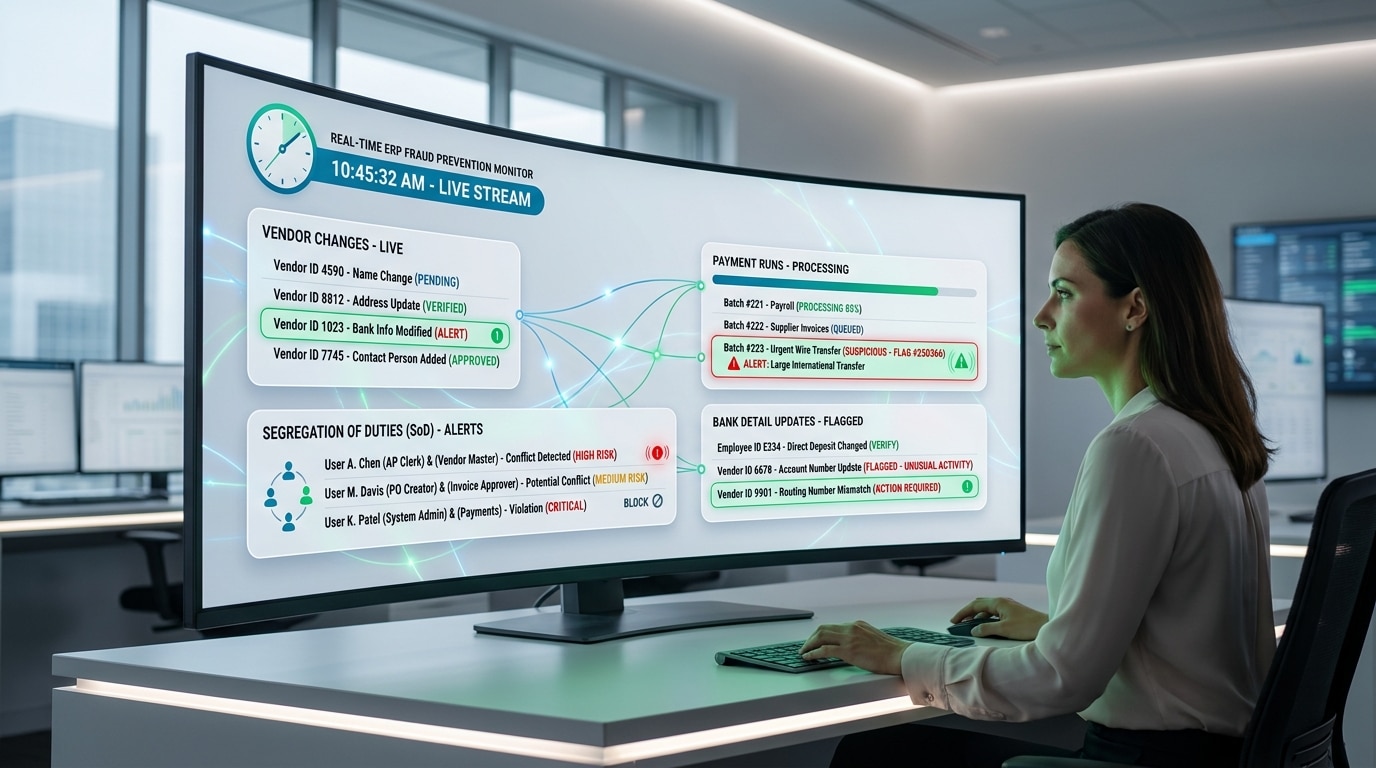

Master Data Risks and Bank Detail Changes

Master data — vendors, employees, GL accounts, payment terms, bank details — is the foundation of every transaction the ERP processes. Fraudsters often prefer master data manipulation over creating new records because altering a trusted existing record attracts less attention. A common scheme involves changing a legitimate supplier’s bank account just before a large payment run, then reverting the change afterward. Understanding the risks associated with changing bank account details is essential, because these ERP master data risks translate directly into unauthorized transactions that standard approval flows rarely catch in time.

Every bank detail change in your ERP is either a legitimate update or the start of a loss. Detelix tells you which, in real time.

How to Identify ERP Fraud Red Flags

ERP red flags include rounded-dollar invoices, duplicate invoice numbers with small variations, payments processed outside normal business hours, new vendors sharing bank details with existing ones, and sudden surges in manual journal entries. ERP fraud indicators also appear in user behavior: logins from unusual locations, repeated failed approvals followed by a successful one, or a single user making rapid changes across several master records. FinCEN’s advisory lists concrete red flags for fraudulent payment instructions, including changed beneficiary details, urgent payment requests, and payments to unfamiliar accounts — all patterns that apply directly to ERP-driven payables. Spotting suspicious ERP transactions depends on continuous ERP anomaly detection rather than periodic review.

Tip

Build a short weekly exception list: new vendors, bank detail changes, manual journals above threshold, and after-hours payments. Even reviewing this list for fifteen minutes a week surfaces most high-risk activity.

Mapping Fraud Types to Processes and Controls

A practical way to strengthen the control environment is to connect each fraud type to the exact process where it occurs and the control that should prevent it. The table below offers a simple mapping finance and audit leaders can use as a starting point.

| Fraud Type | Primary ERP Process | Key Warning Sign | Preventive Control |

|---|---|---|---|

| Fictitious vendor | Supplier master data | New vendor with incomplete documentation | Independent vendor verification before first payment |

| Invoice manipulation | Accounts payable | Rounded amounts, duplicate numbers | Three-way match and exception review |

| Bank detail change fraud | Vendor master data | Change just before payment run | Out-of-band verification of the change |

| Duplicate payment | Payment processing | Same invoice across periods | Cross-period duplicate detection |

| Access abuse | User roles and permissions | User performing multiple sensitive steps | Segregation of duties enforcement |

| Inventory manipulation | Stock adjustments | Unexplained write-offs or corrections | Independent review of adjustments |

The Financial Impact of Duplicate Payments

Duplicate payments sit in a gray zone between error and fraud. Sometimes they reflect weak controls — an invoice entered twice, a payment released in two runs, or a credit memo never applied. In other cases, they are deliberate, used to conceal embezzlement by creating a pattern that looks like a routine mistake. Either way, the financial drain is real and often larger than leadership assumes. Duplicate payment fraud is particularly challenging because standard ERP controls compare invoice numbers within narrow windows and miss variations in formatting, vendor entries, or timing. Strengthening payment fraud controls requires broader cross-checks, and identifying duplicate payments in ERP systems through continuous monitoring is one of the highest-return investments in reducing ERP financial fraud.

Did You Know

Recoveries of duplicate payments typically fall between 0.1% and 0.5% of total payables spend. For a billion-dollar payables run, even the lower end represents seven-figure value recovered purely from detection logic.

Internal Fraud Versus External Fraud in ERP

The profile of an ERP fraud case differs sharply depending on who is behind it. Internal actors use legitimate access, know the approval flow, and often understand which controls are manual or weak. External actors rely on phishing, credential theft, and impersonation to gain that same access. Both converge inside the ERP, which is why the same detection logic — behavior analysis, master data change monitoring, and exception alerting — applies to both. The table below highlights the practical differences that matter to finance and audit teams.

| Dimension | Internal Fraud | External Fraud |

|---|---|---|

| Typical actor | Employee, manager, privileged user | Attacker, impersonator, compromised vendor |

| Entry point | Legitimate credentials | Phishing, BEC, stolen credentials |

| Preferred target | Master data, approvals, journal entries | Payment instructions, vendor bank details |

| Detection difficulty | High — activity looks authorized | Moderate — often shows external indicators |

| Core mitigation | Segregation of duties, monitoring | Verification, access hardening, training |

Strategic ERP Fraud Prevention and Auditing

Strong ERP fraud prevention is built on a framework, not a list of tools. Begin with a structured fraud risk assessment that maps each sensitive process to its potential fraud scenarios and existing controls. Follow with a regular ERP audit cycle covering permissions, master data changes, exceptions, and integrations. Reinforce the program with leadership accountability and clear ownership of every control. COSO’s guidance on fraud deterrence and structured risk management programs confirms that governance, anti-fraud controls, and continuous evaluation are the pillars of effective protection. This is the foundation of mature ERP governance.

Tip

Assign a named owner to every key control — not a department, an individual. Ownership with a name on it closes faster than ownership assigned to a team inbox.

How Real-Time Monitoring Changes the Equation

Traditional controls rely on sampling, periodic reviews, and reports that arrive after the fact. Real-time monitoring changes the equation by continuously cross-checking actions as they happen — a new vendor created, a bank detail changed, an approval bypassed, a payment approaching an unusual threshold. When exceptions surface immediately, the organization moves from reviewing reports to actually controlling the process. Detelix is built for this mode of operation. It connects to sensitive ERP processes, applies configurable rules, and alerts the right people before a transaction becomes a loss. The table below shows how common business needs map to what the platform delivers in practice.

| Business Need | How Detelix Supports It |

|---|---|

| Visibility over vendor master data changes | Continuous monitoring with alerts on sensitive field updates |

| Early detection of duplicate or suspicious payments | Cross-period checks and anomaly rules across payment runs |

| Control over segregation of duties gaps | Detection of user activity that crosses conflicting roles |

| Fast response to bank detail changes | Real-time alerts before the next payment cycle |

| Audit readiness | Documented exceptions, actions, and resolution trails |

Common Mistakes That Weaken ERP Fraud Defenses

Even well-run finance teams fall into recurring traps. Treating permissions as a one-time setup rather than an ongoing review is among the most common. Relying exclusively on approval workflows without monitoring what happens between approvals is another. Assuming that a cloud ERP is automatically safer than an on-premise one ignores the fact that configuration, user management, and process design remain the customer’s responsibility. Finally, many organizations confuse the existence of a policy with the enforcement of a control — a policy documents intent, while a control produces evidence that intent is being followed. Closing these gaps is less about adding tools and more about aligning people, process, and technology around ERP compliance controls that actually operate.

Did You Know

In most shared-responsibility cloud ERP models, the provider secures the infrastructure while the customer remains fully responsible for user roles, process configuration, and monitoring — which is where the vast majority of fraud originates.

Strengthening the ERP Control Environment

The full landscape of enterprise resource planning fraud types — from fictitious vendors and invoice manipulation to access abuse and master data tampering — shows why software alone is not enough. Process design, permission hygiene, continuous ERP monitoring, and leadership accountability must align. When they do, the organization moves from the illusion of control to real control: knowing what is happening right now, acting before damage occurs, and protecting financial integrity across every sensitive process.

Detelix ERP Fraud Prevention Solutions

Proactive ERP Monitoring

Continuous oversight of sensitive ERP processes, from vendor master data to payment runs, with configurable rules tuned to your organization.

Real-Time Alerts

Immediate notifications for suspicious transactions, bank detail changes, and segregation-of-duties conflicts — before money moves.

ERP Gatekeeper

Independent verification layer for high-risk events — new vendors, bank account updates, and out-of-pattern payments — with documented resolution trails.

Audit & Experience

Years of hands-on ERP fraud experience packaged into playbooks, reviews, and audit-ready evidence for finance and compliance leaders.

See Detelix in Action

Frequently Asked Questions

Which type of ERP fraud is the most damaging?

Fictitious vendor and bank detail change schemes often cause the largest single losses because they redirect legitimate payment flows and can remain undetected across multiple cycles. Duplicate payment fraud tends to be more frequent but smaller per incident, while access abuse enables almost every other category.

How can you identify a fictitious vendor inside an ERP?

Look for vendors with incomplete master data, bank details matching another supplier, addresses resembling employee addresses, invoices with rounded amounts, and activity concentrated in short periods. Independent verification before the first payment is the most effective control.

Is ERP fraud limited to the finance department?

No. Procurement, inventory, payroll, and customer refunds are all exposed. Any process that involves authorizations, master data, or payments inside the ERP is a potential fraud surface.

Is cloud ERP safer than on-premise ERP against fraud?

Cloud ERP can provide stronger infrastructure security, but fraud usually originates in process and permission design, not infrastructure. The customer remains responsible for configuring roles, monitoring activity, and enforcing segregation of duties.

How often should user access reviews be performed?

At minimum quarterly for sensitive roles, and immediately after role changes, terminations, or major process updates. Continuous monitoring of privileged activity between reviews is equally important.

What is the difference between ERP fraud and an operational error?

Errors are unintentional and usually random in pattern. Fraud is intentional, repeatable, and designed to avoid detection. The same control weaknesses enable both, and continuous monitoring helps distinguish the two by surfacing patterns rather than isolated incidents.

How do integrations with external systems create fraud risk?

APIs, file imports, bank connections, and third-party tools can allow data to enter or leave the ERP without going through standard approval flows. Without monitoring, these pathways become blind spots that attackers and insiders can exploit.

Ready to Move from Reporting to Real Control?

Every sensitive ERP action — new vendors, bank changes, journal entries, payments — should be verified in real time, not reviewed after the fact. Detelix makes that possible.